China

China is providing limited stimulus, promoting tech and trade, and maintaining a tariff truce with the US in 2026. Structural flaws and great power struggle continue to cast dark clouds over the long run.

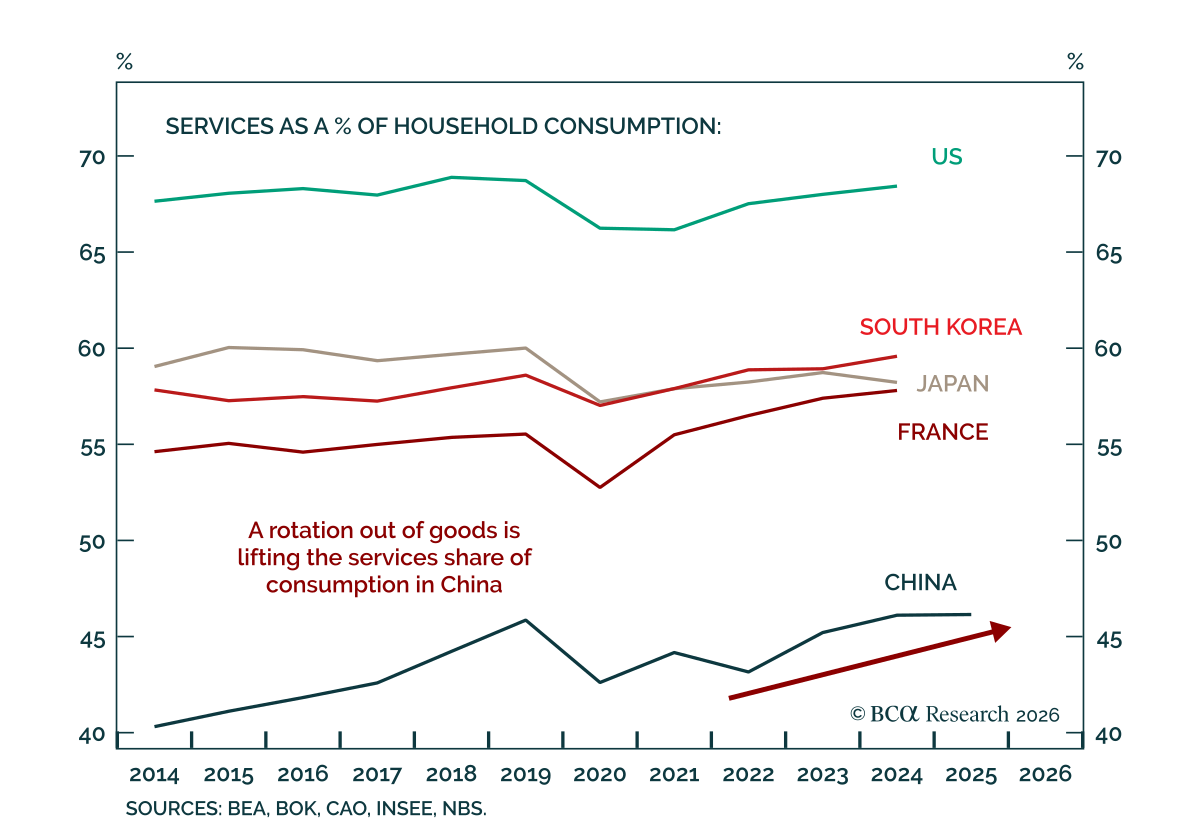

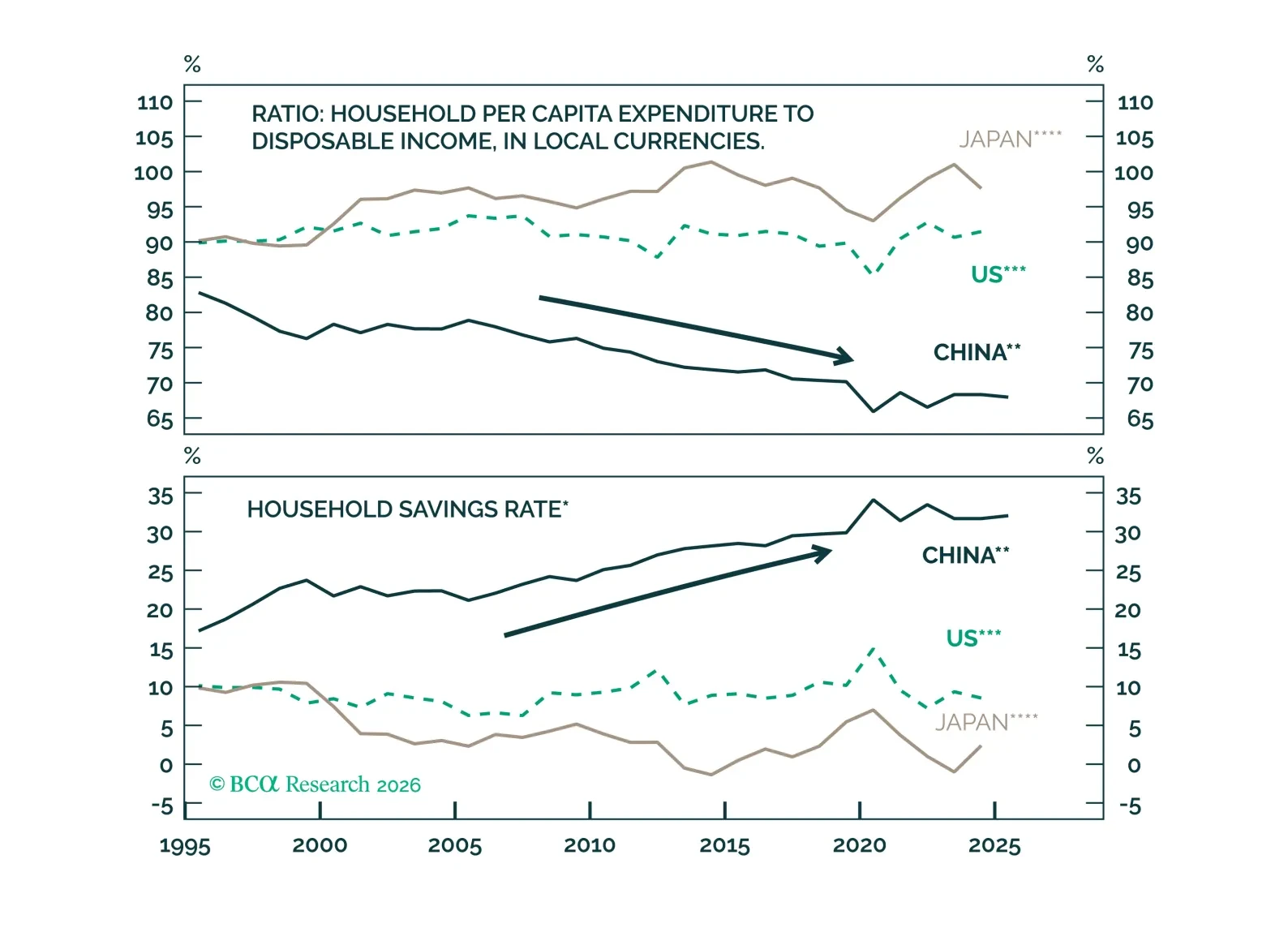

This report analyzes the structural and cyclical factors driving service spending in Chinese households and highlights sectors with promising investment opportunities for the next 6 to 12 months.

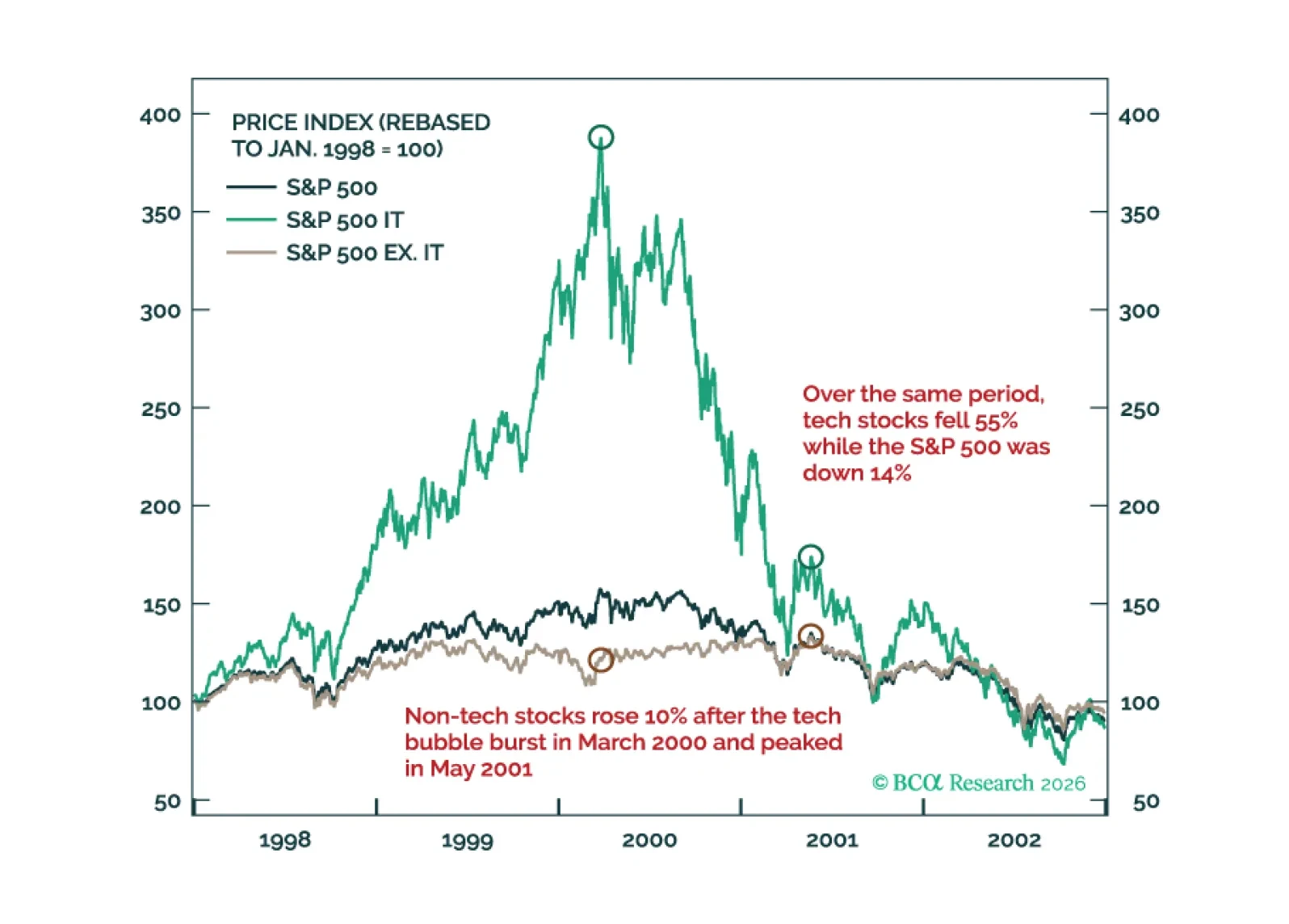

Much like the 2000 episode, we expect this year to unfold in two stages: A “Great Rotation” from tech stocks to non-tech names in the first half of 2026 followed by a broad-based selloff in stocks in the second half on the back of a weakening US economy.

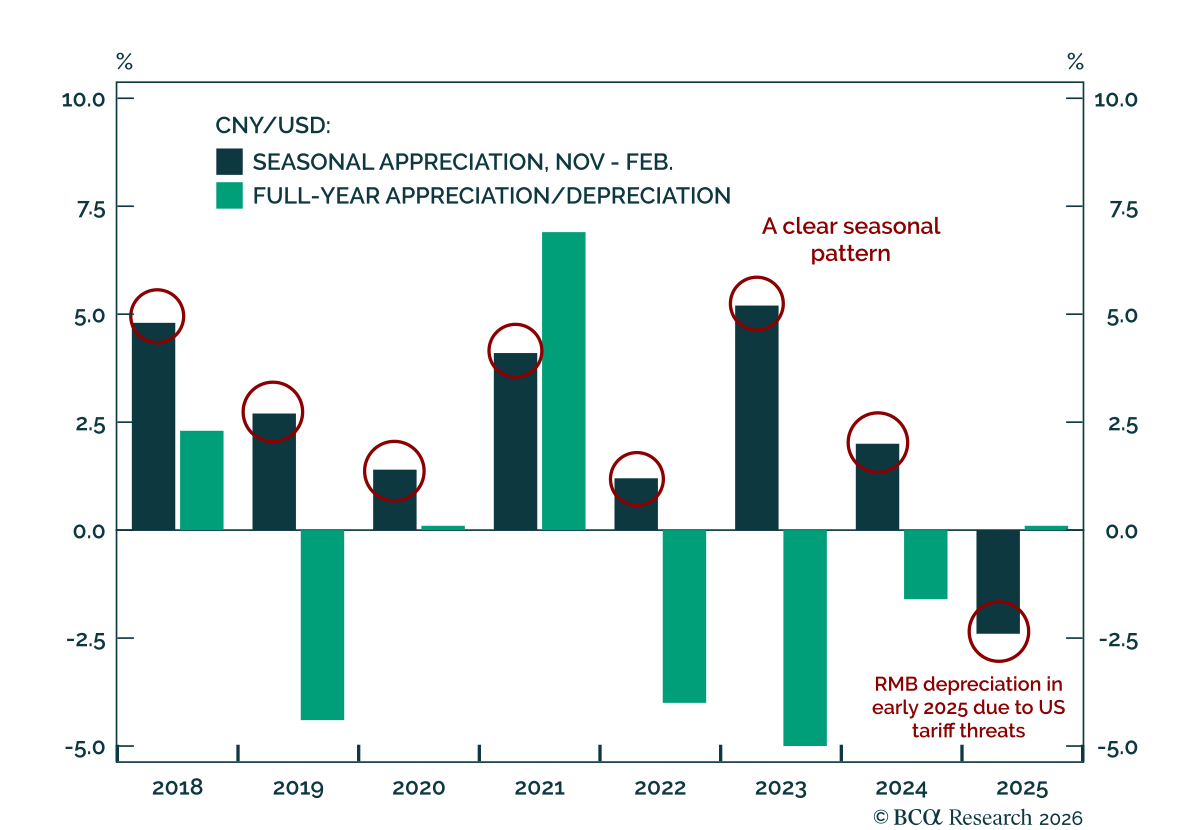

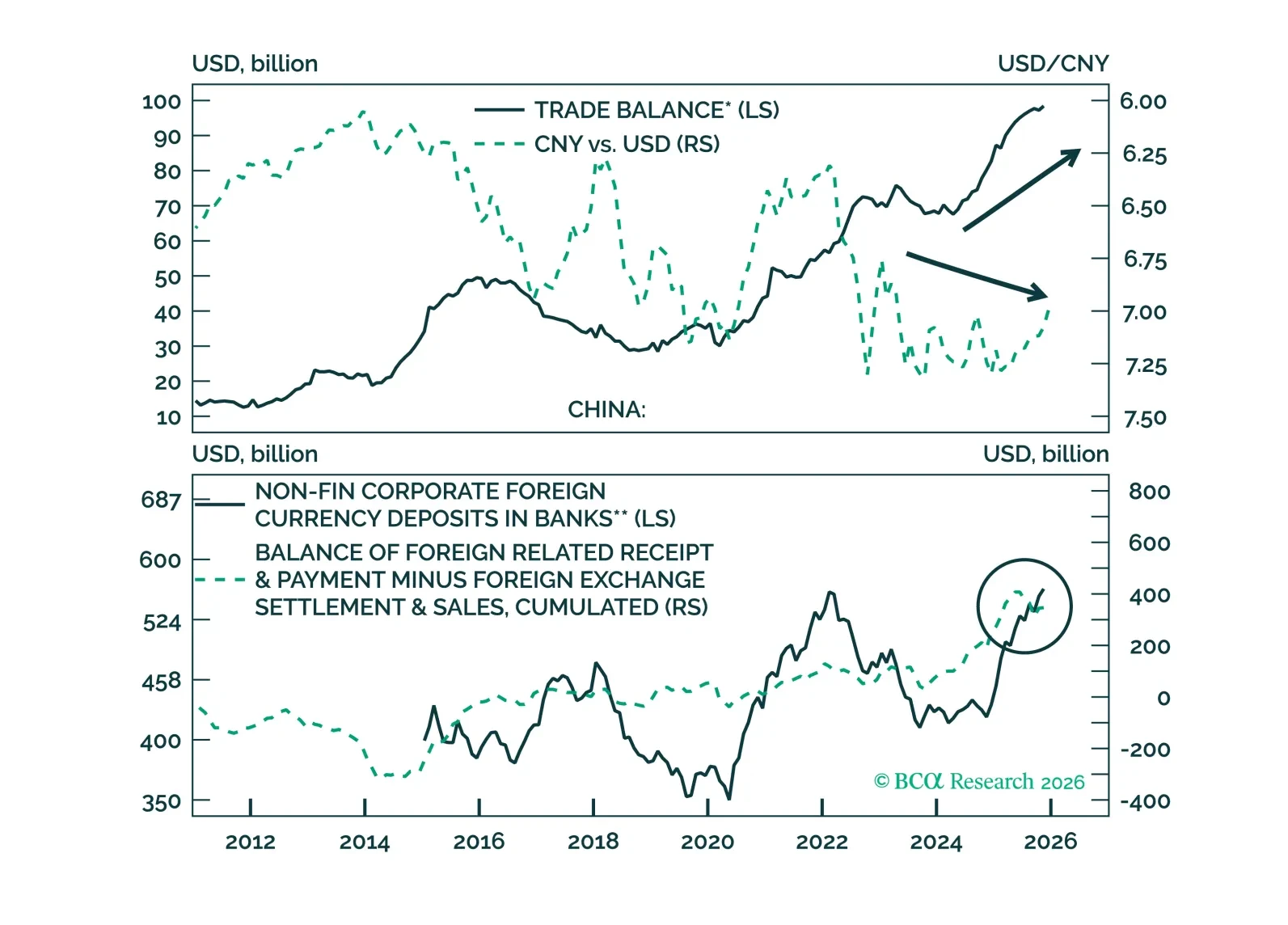

We explain the underlying catalysts for the RMB’s seasonal appreciation, and assess the upside potential for the currency in 2026.

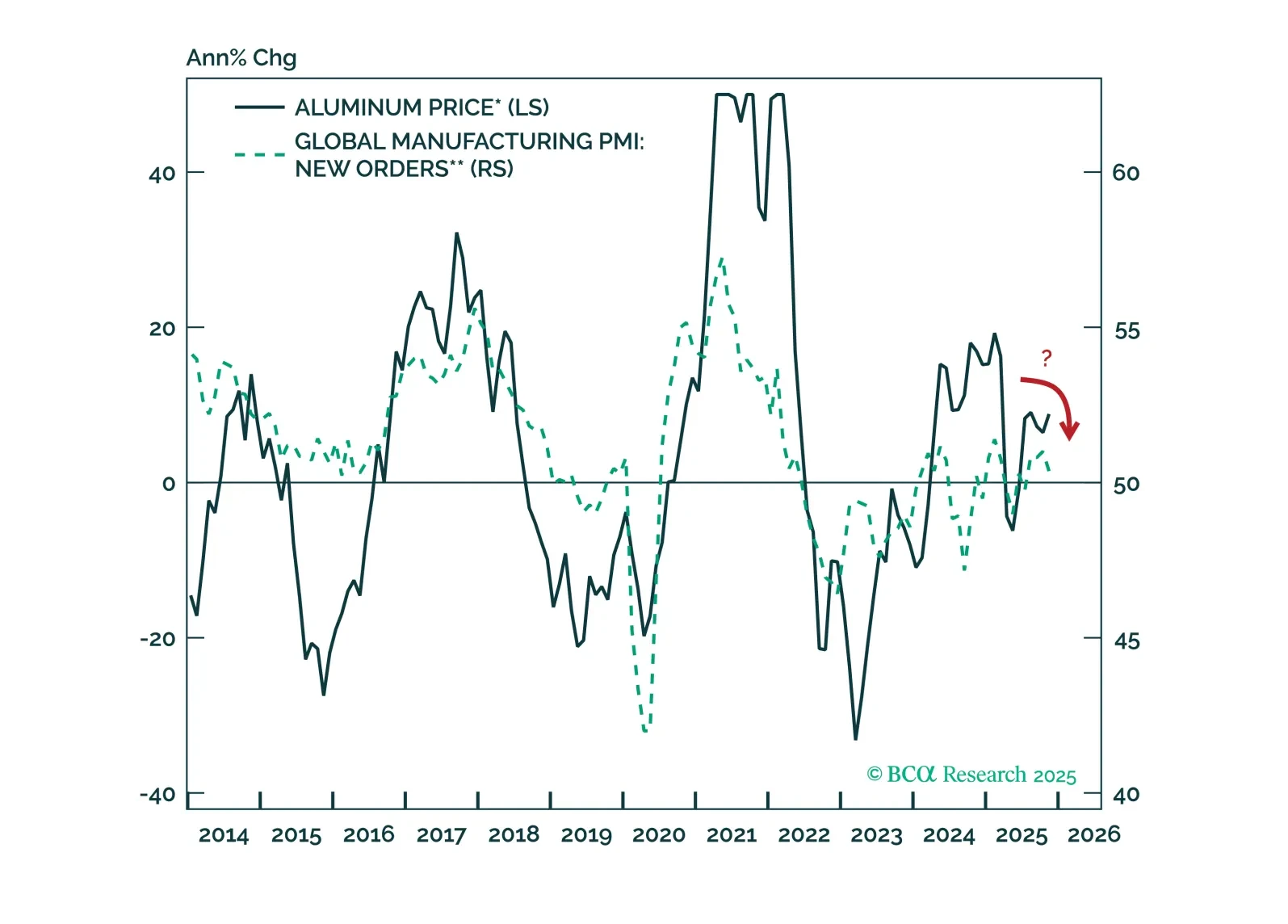

The forces that have recently propelled aluminum prices will remain supportive over the near term. However, beyond the coming months, aluminum prices will retreat as bearish cyclical pressures overwhelm over the course of 2026.