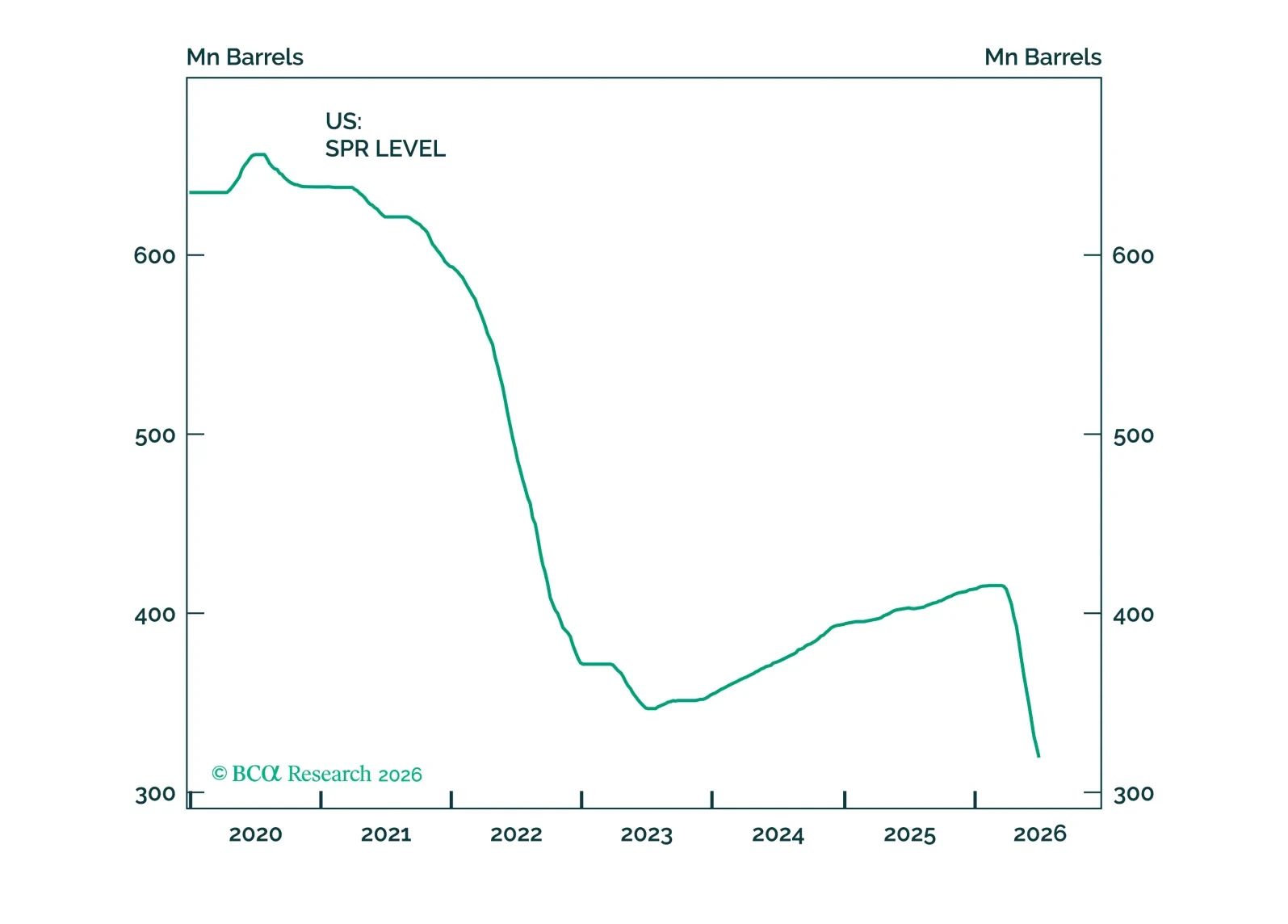

Oil

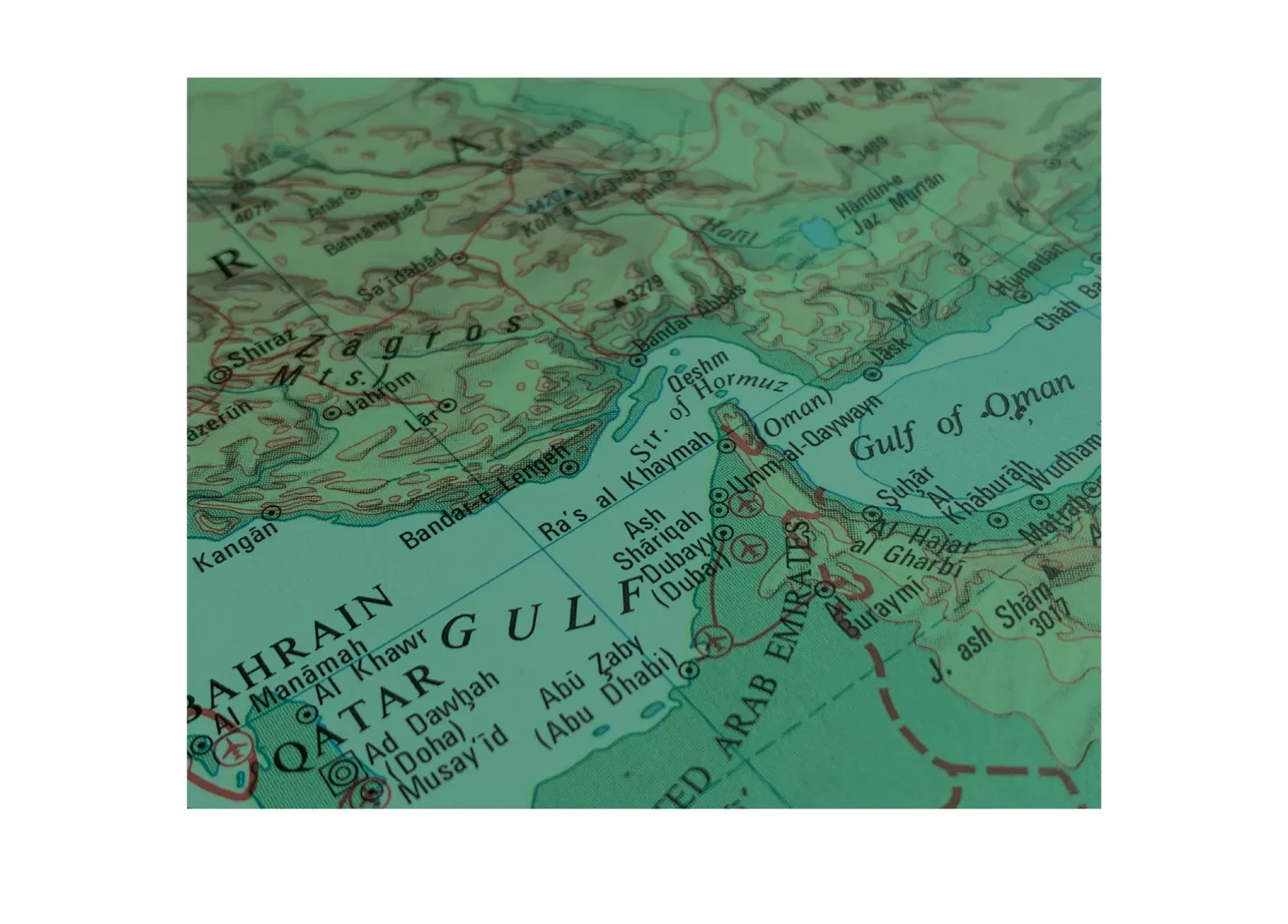

The Strait of Hormuz is a unique geographical feature. Other than the Bosporus and Dardanelles Straits that allow passage between the Mediterranean and the Black Sea (via the Sea of Marmara), there are very few other such, economically valuable, choke points. What many armchair geopolitical strategists consider “critical” naval routes – Strait of Malacca, Panama Canal, Suez – are really just pathways of convenience. “Nice to haves” – in that they significantly reduce sailing times – as opposed to the “must have” that is Hormuz.

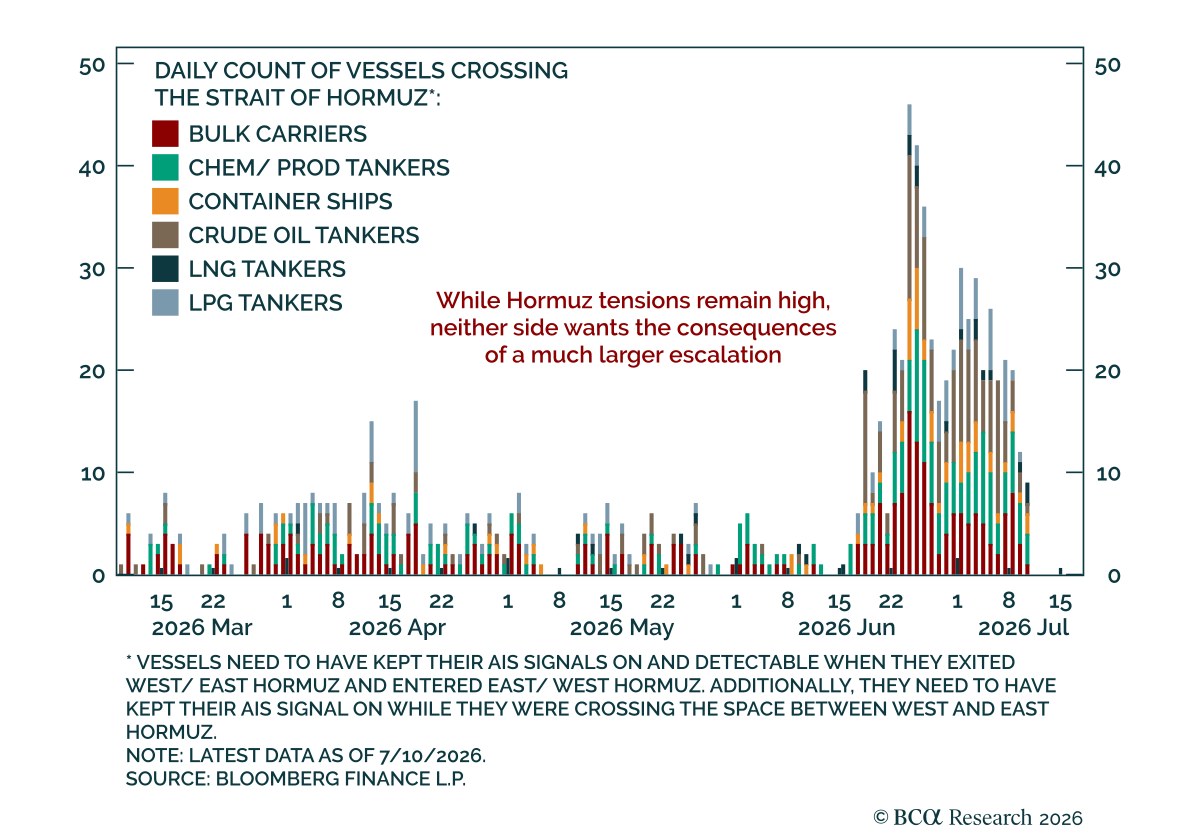

In our last update on the Iran-US conflict, we noted that both sides in the conflict (all three, if we include Israel) were “coloring inside the lines.” By that we meant that they were abiding by the “red lines” of kinetic activity established in the heat of the first iteration of the Iran conflict. Specifically, we noted that investors should watch carefully for any sign that attacks were spreading beyond military facilities.

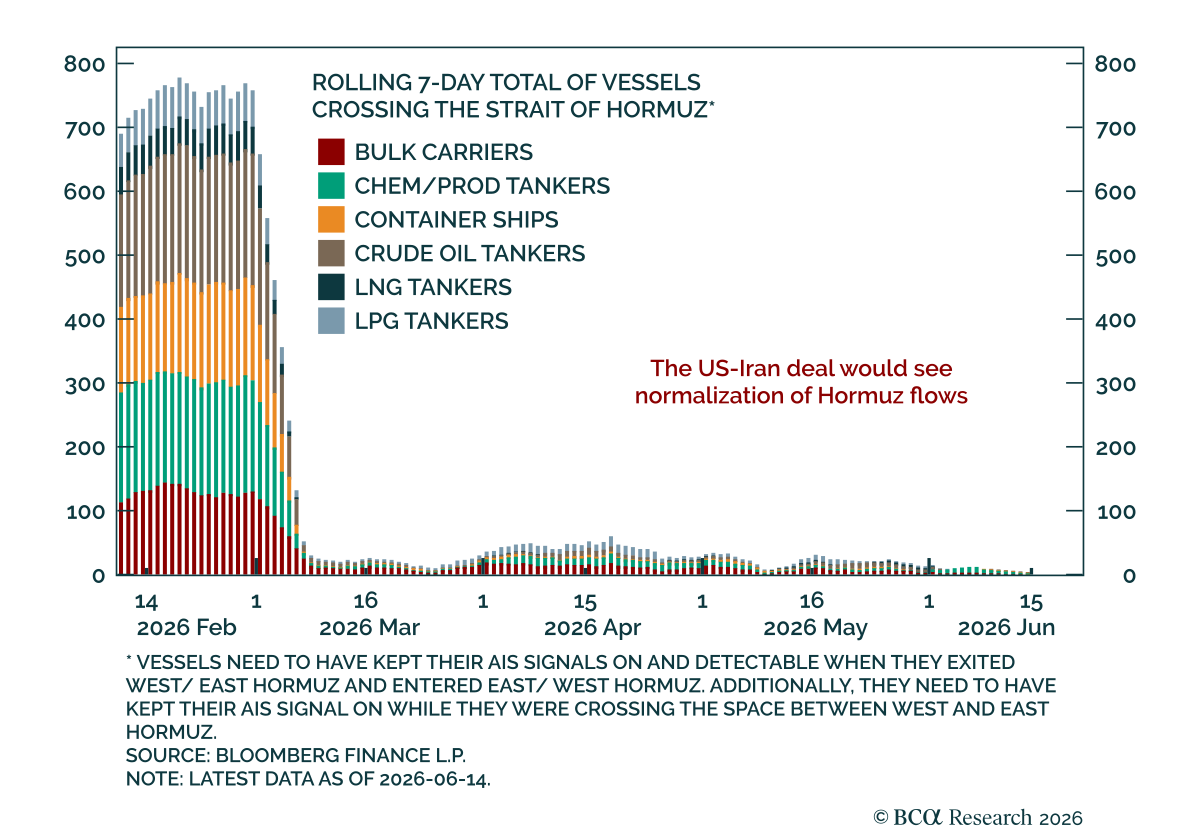

The US and Iran have engaged in a dramatic increase in kinetic activity over the past several days. It all appears to have started on July 6-7, when Iran allegedly attacked several ships in the Strait of Hormuz, vessels that were using the US-recommended route closer to Oman. Following US strikes against Iran in retaliation for that incident – with the US military claiming to have struck 140 sites – Iran has retaliated against US military facilities across the Gulf region. According to media reporting and Iranian government sources themselves, Iran attacked Bahrain, Kuwait, Jordan, Qatar and Oman on July 11-12.

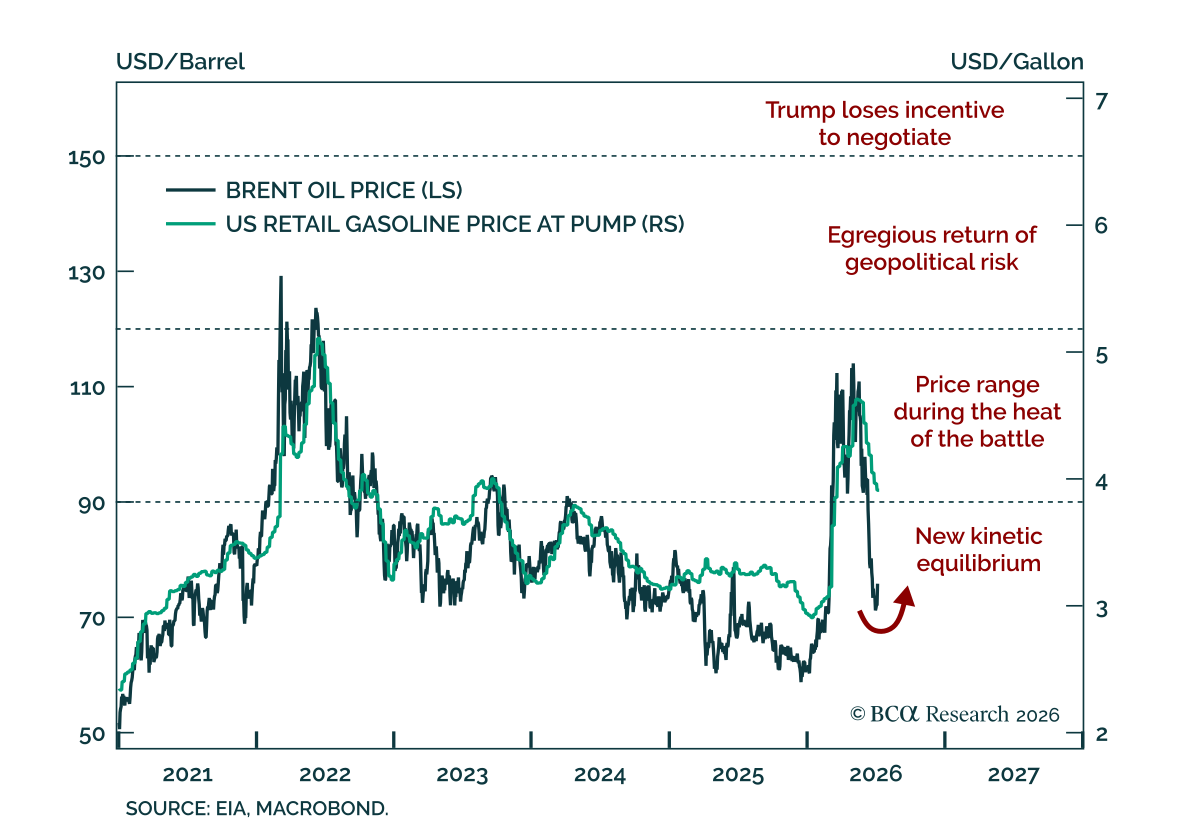

Just as we declared that geopolitical risk has peaked for the year – in yesterday’s Alpha report – President Trump has declared the ceasefire with Iran over after repeated violations via strikes against three tankers in the Strait of Hormuz. That is the life of an investment strategist. But the underlying dynamics continue to play out as we’ve described.

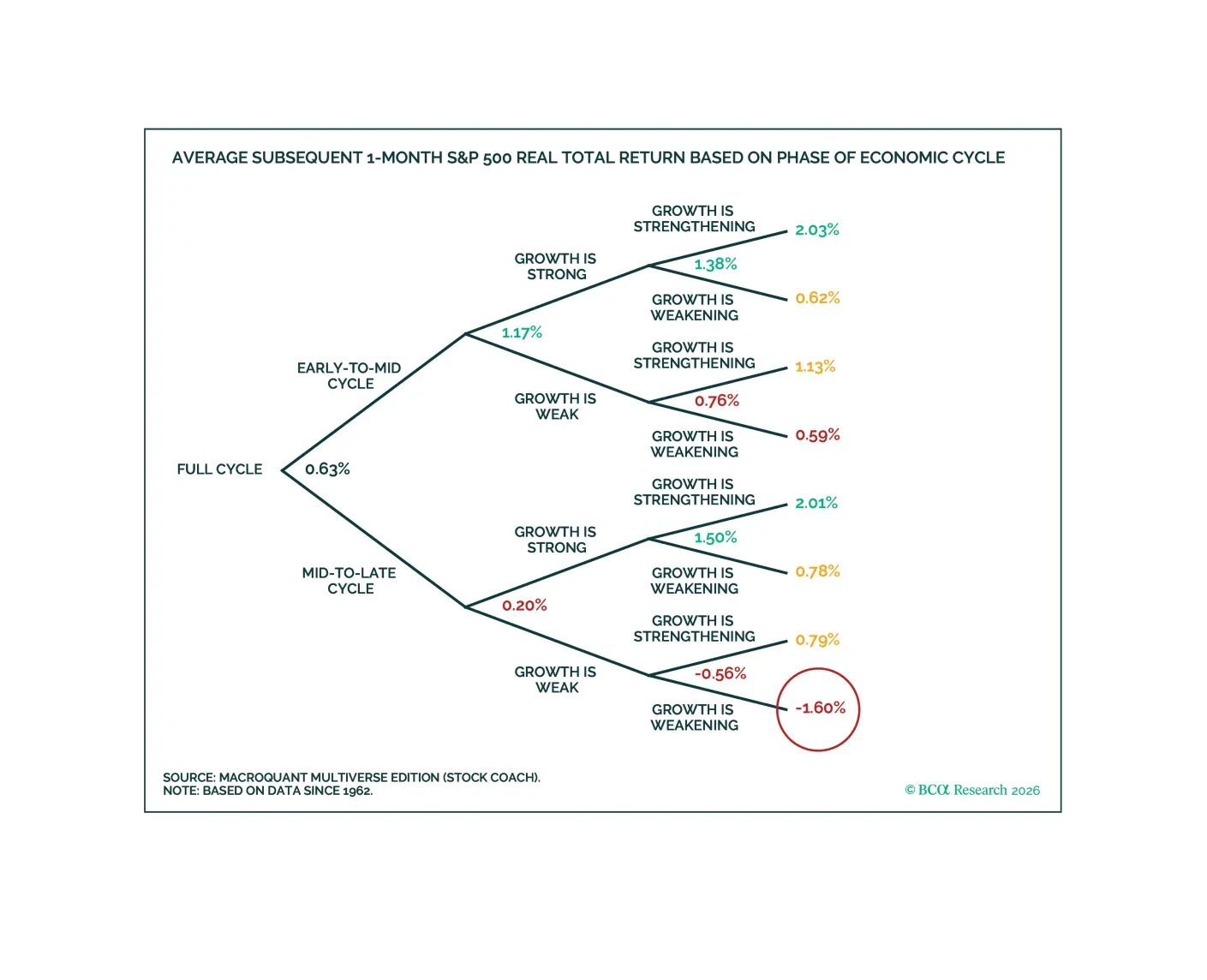

MacroQuant recommends underweighting equities and adopting a benchmark duration stance in fixed-income portfolios. The model is very positive on the US dollar, bearish on gold, neutral on copper, and bullish on oil.

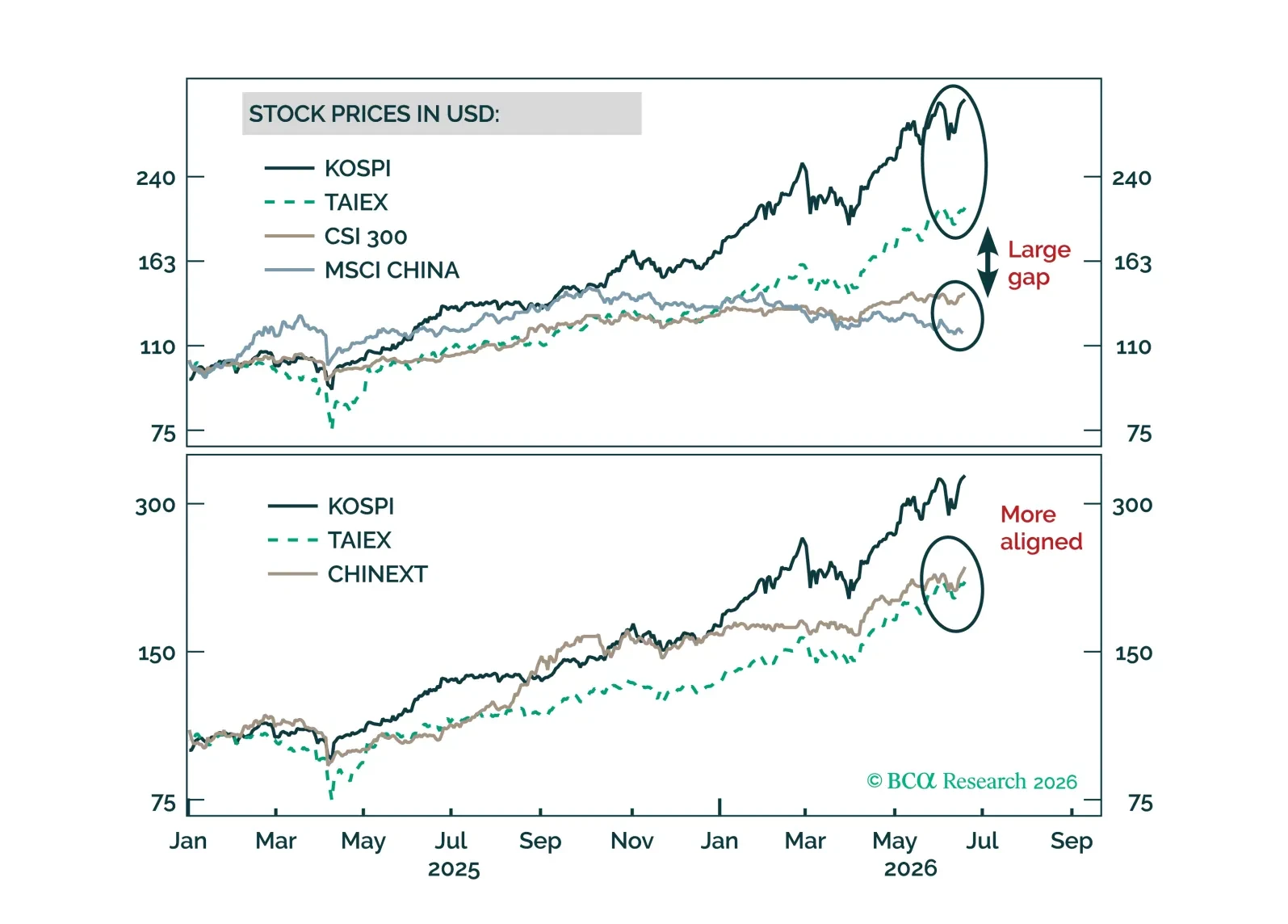

This report addresses five frequently asked questions from our Greater China clients over the past few months.