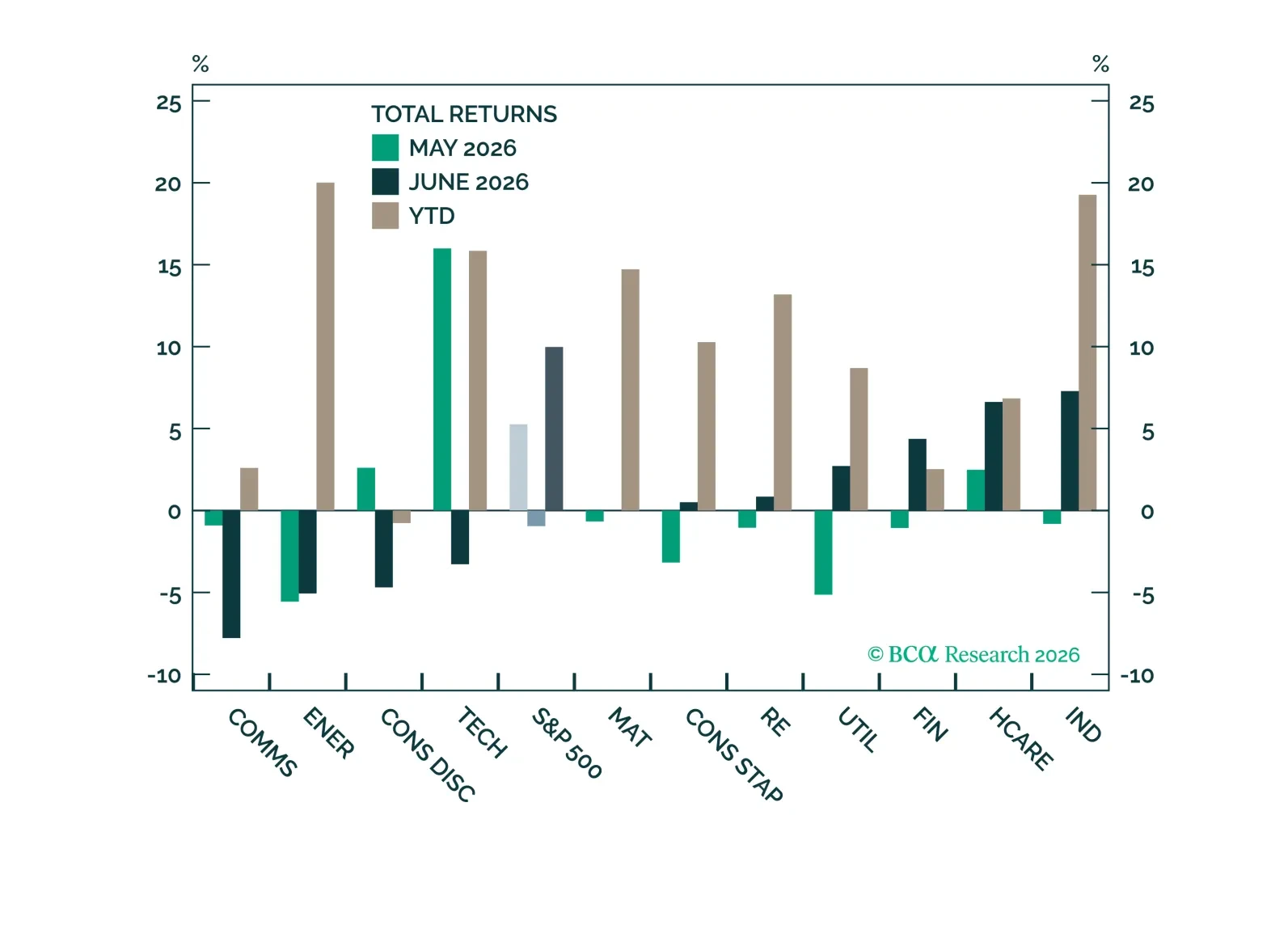

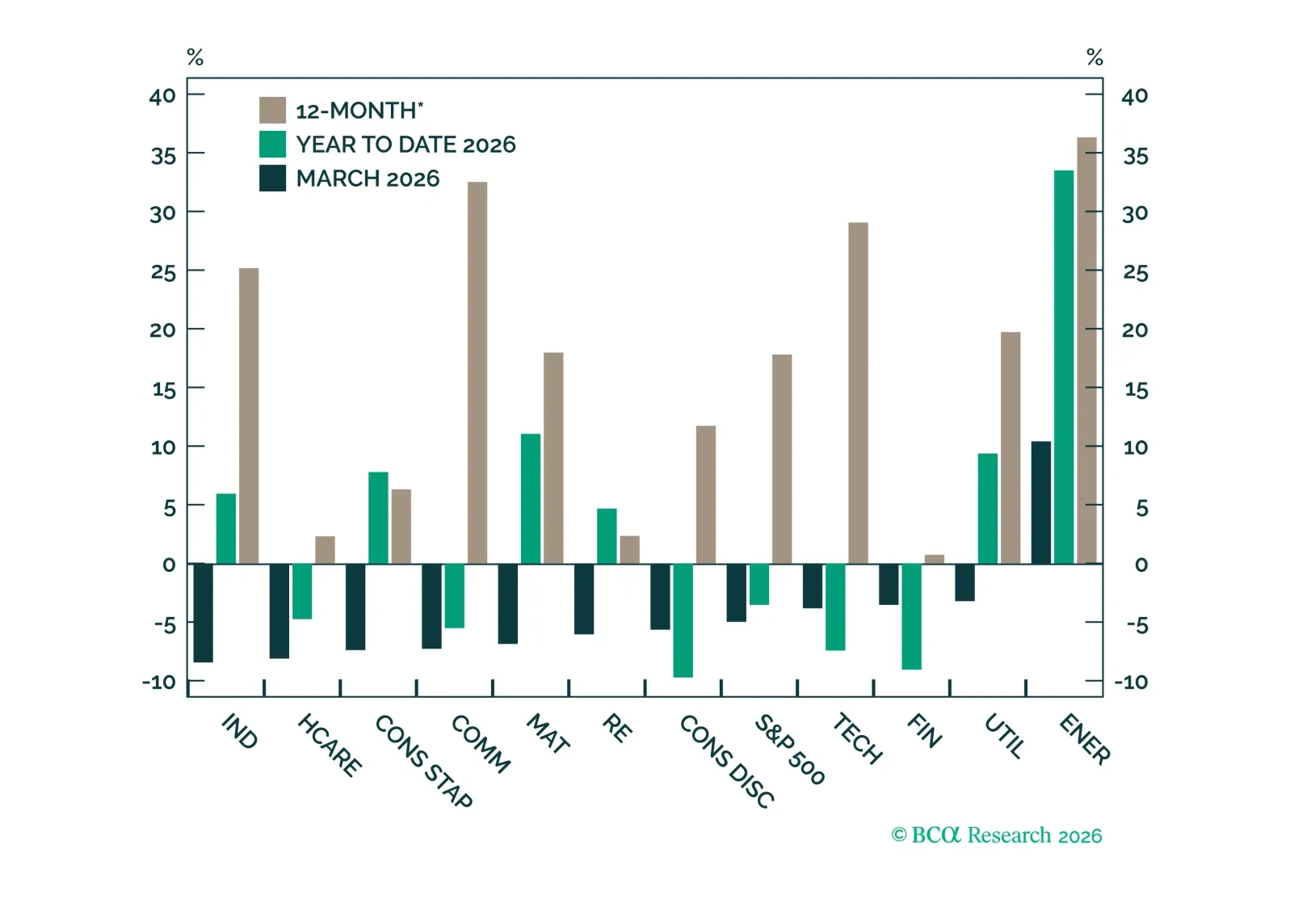

Sectors

S&P 500 performance rotated in June, but fundamental growth remains strong across sectors, with earnings and revenue growth extending well beyond the largest mega-cap companies.

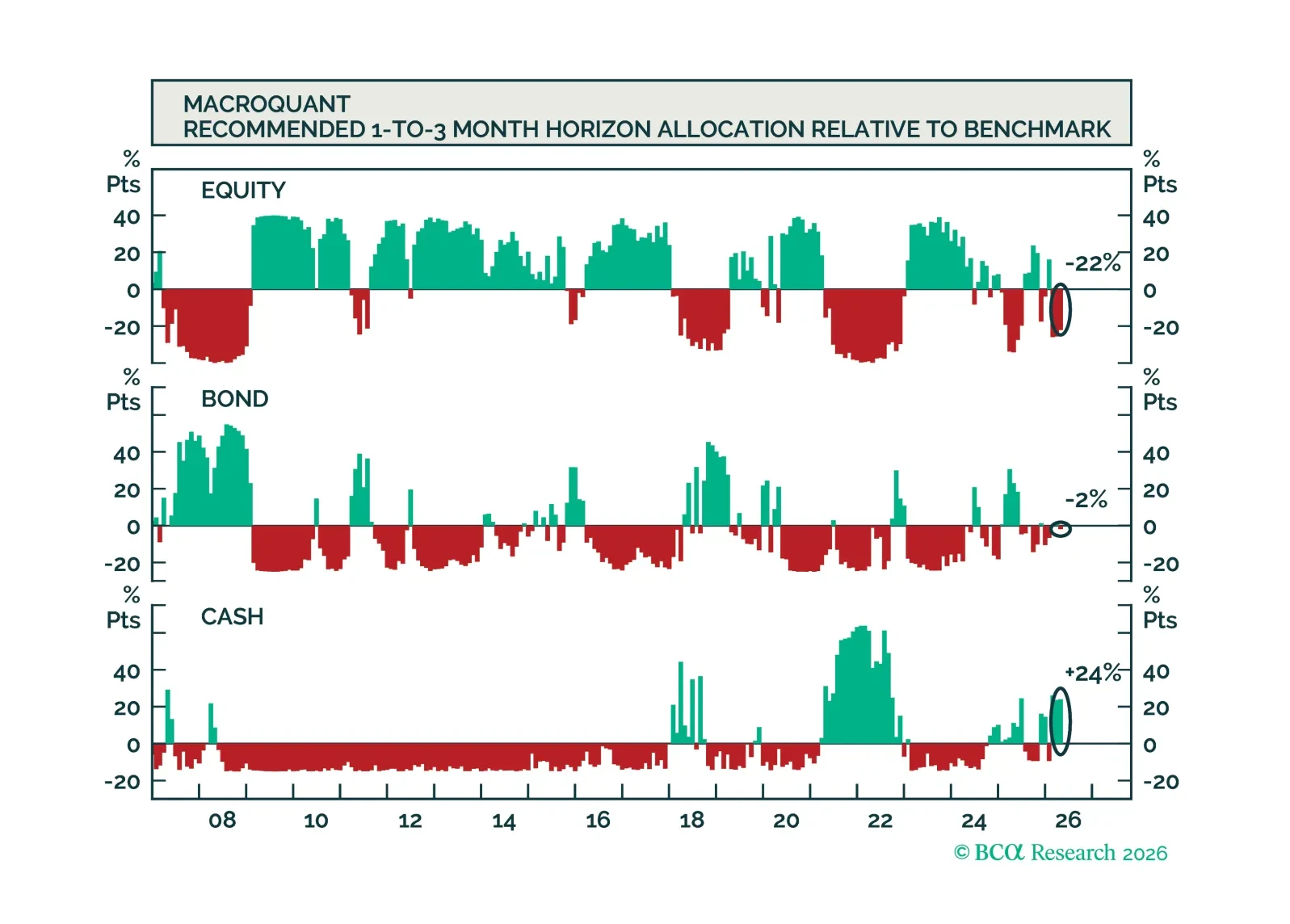

MacroQuant recommends underweighting equities and adopting a benchmark duration stance in fixed-income portfolios. The model is very positive on the US dollar, bearish on gold, neutral on copper, and bullish on oil.

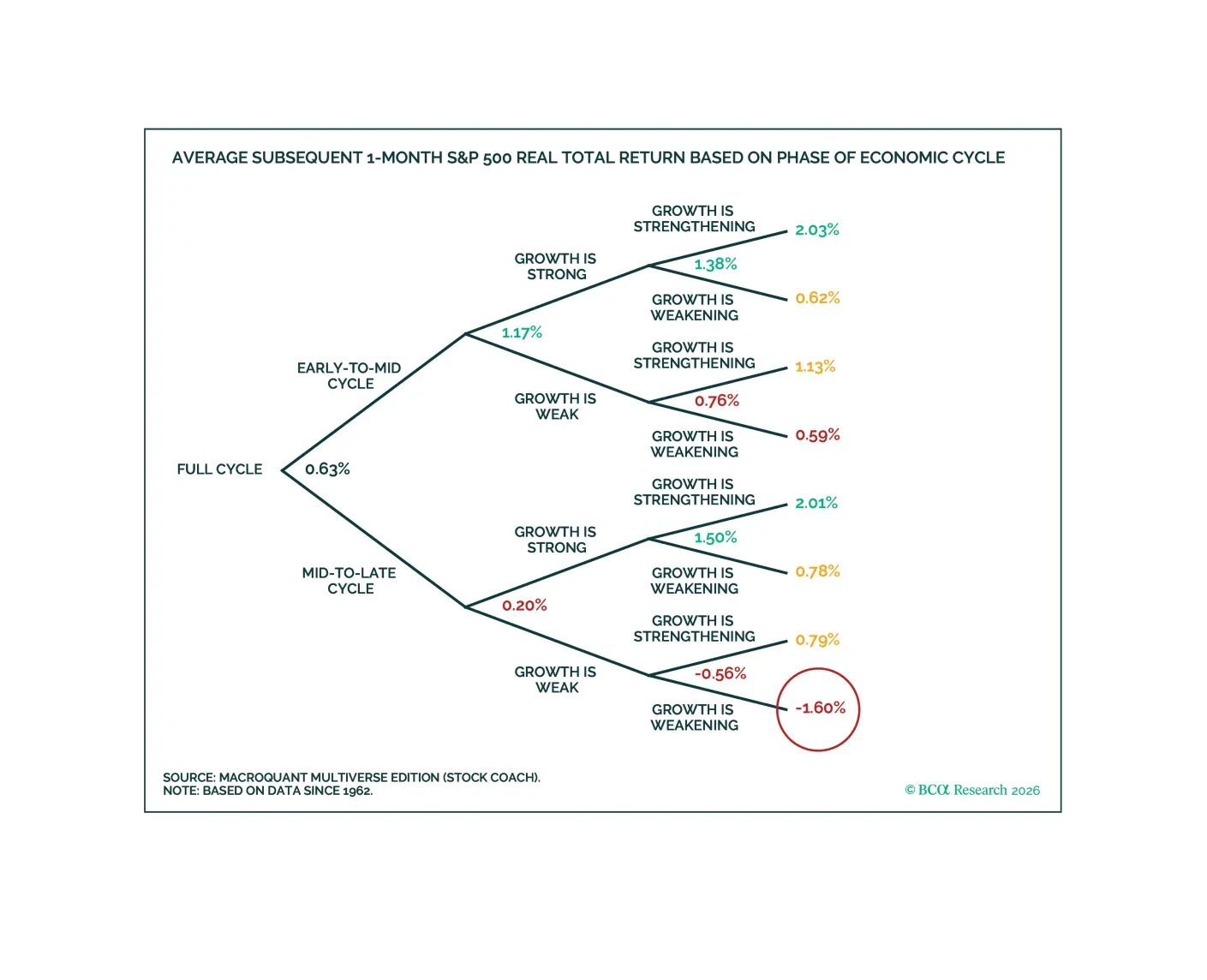

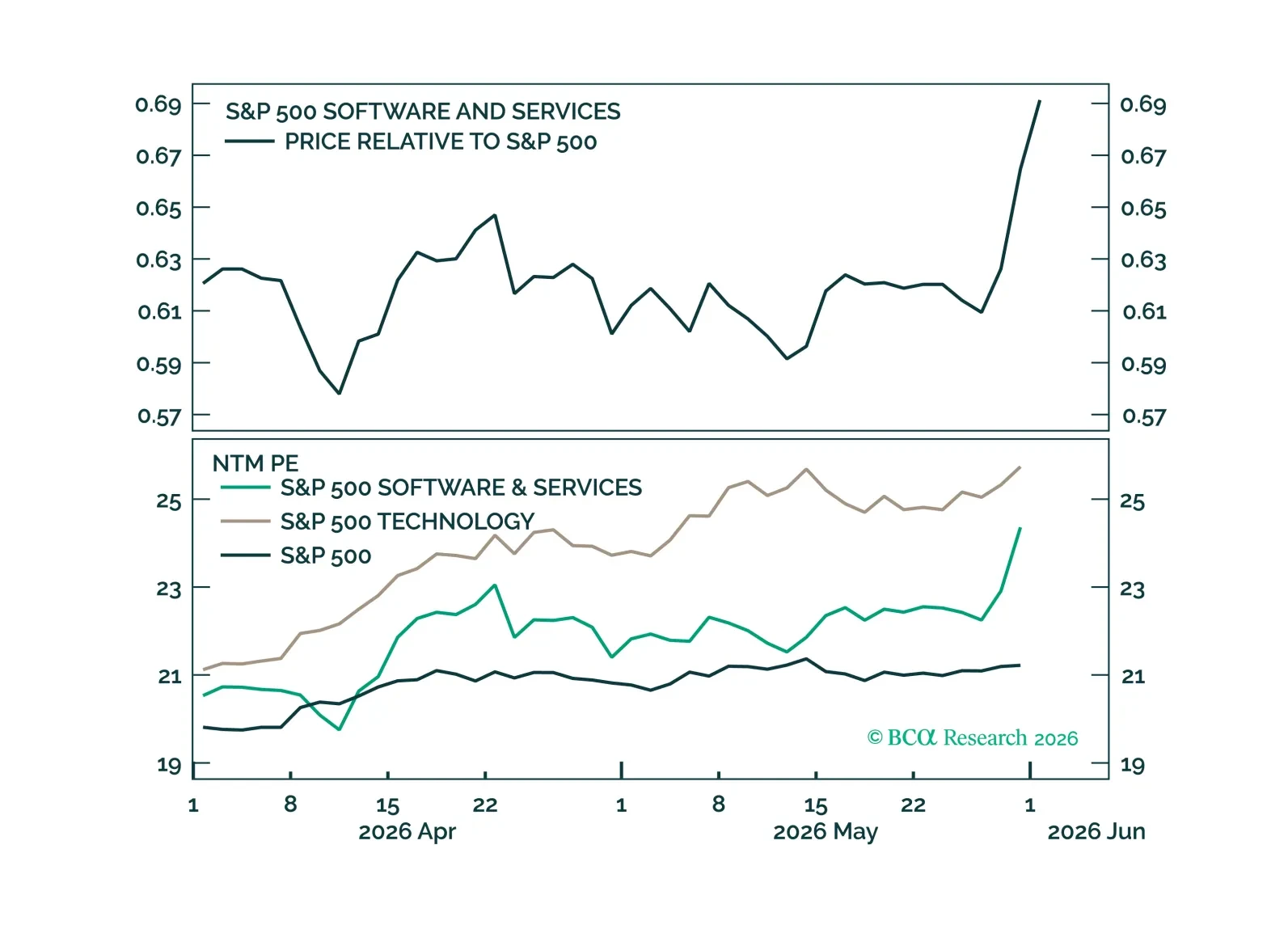

The US economy is moving back toward Expansion, supported by strong investment, improving earnings, and record margins. We are taking profits on our tactical Software long after achieving our target and rotating into Materials, where commodity strength and earnings momentum continue to support the sector.

MacroQuant recommends a slight underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is very positive on the US dollar, downgrades gold to underweight, upgrades copper to overweight, and remains very bullish on oil.

Leadership has rotated toward investment-driven sectors, reflected in both EPS growth and price performance. Expanding margins suggest the cycle may have longer to run, as productivity gains start to work their way through fundamentals. We continue to see upside for the S&P 500, with no change to our sector outlook.

MacroQuant recommends an underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is neutral-to-slightly positive on the US dollar, remains neutral on gold, upgrades copper to neutral, and is very bullish on oil.

Chinese onshore equities are riding the global “scarcity trade,” powered by tight semi supply and surging alternative-energy demand. How should investors position in this environment?

The long-run rise in S&P 500 margins reflects more than a shift toward higher-margin sectors. Most of the increase has come from higher profitability within sectors, supported by favorable mix of macro forces. Looking ahead, many of those tailwinds are likely to fade, with AI-driven productivity gains as a potential offsetting upside driver of margins.

We expect the S&P 500 to deliver $308 of EPS in 2026, with a year-end target of 7700. Revenue growth drives upside, with little margin or multiple expansion. With economic growth tilted toward investment, we are overweight Technology, Industrials, and Materials, market-weight Financials, Energy, Health Care, Communication Services, and Real Estate, and underweight Consumer Staples, Consumer Discretionary, and Utilities.