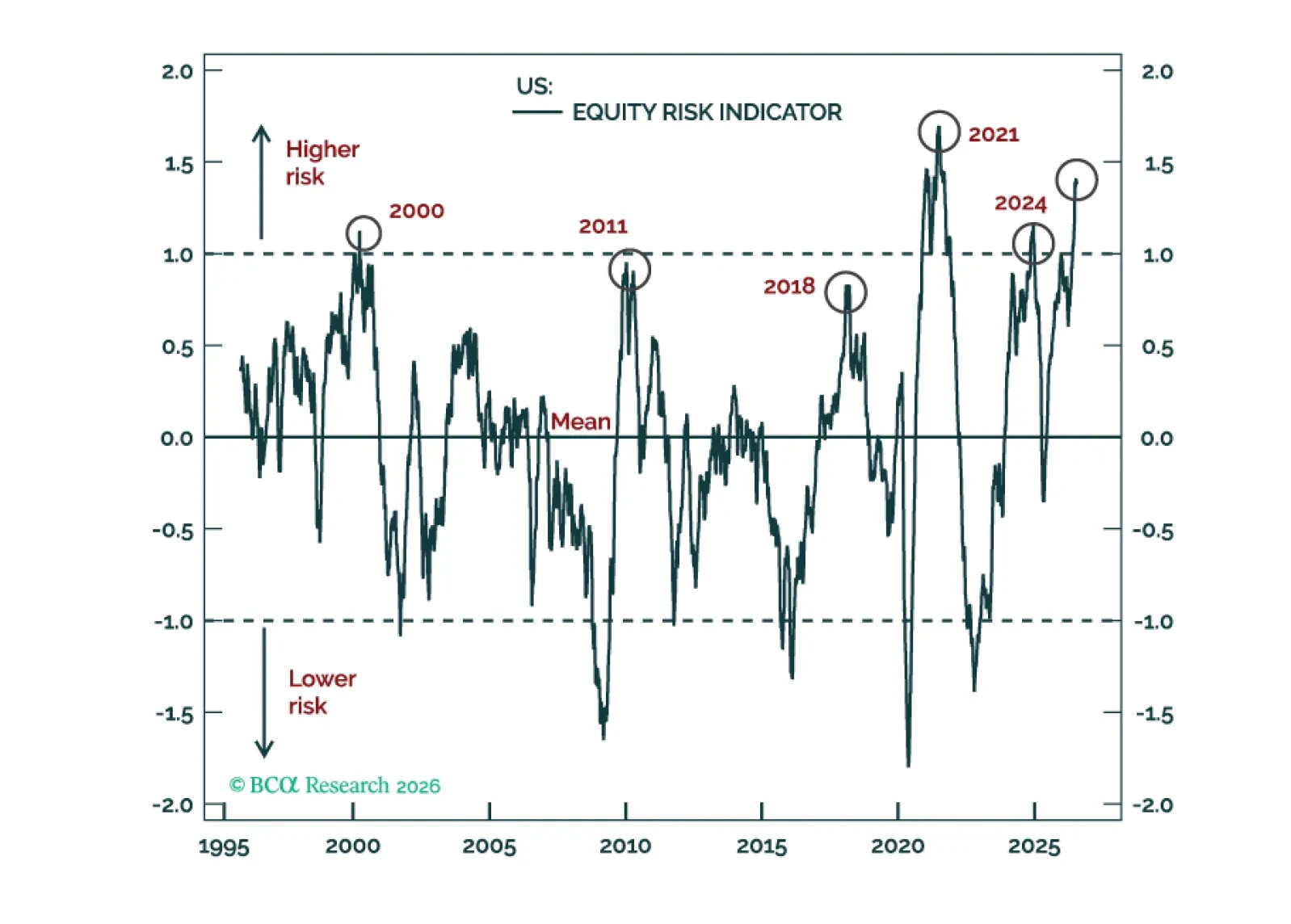

Equities

Global equities have reached extremes on multiple measures, none of which are reliable timing tools. But imbalances in economics and investing can build for far longer than rational analysis would predict - and usually unravel much faster than investors expect.

As long as the AI boom keeps booming, all other investment considerations will remain on the back burner. However, if the AI trade fizzles, this would expose deep-seated problems within the global economy, which could very well lead to an economic downturn as early as next year.

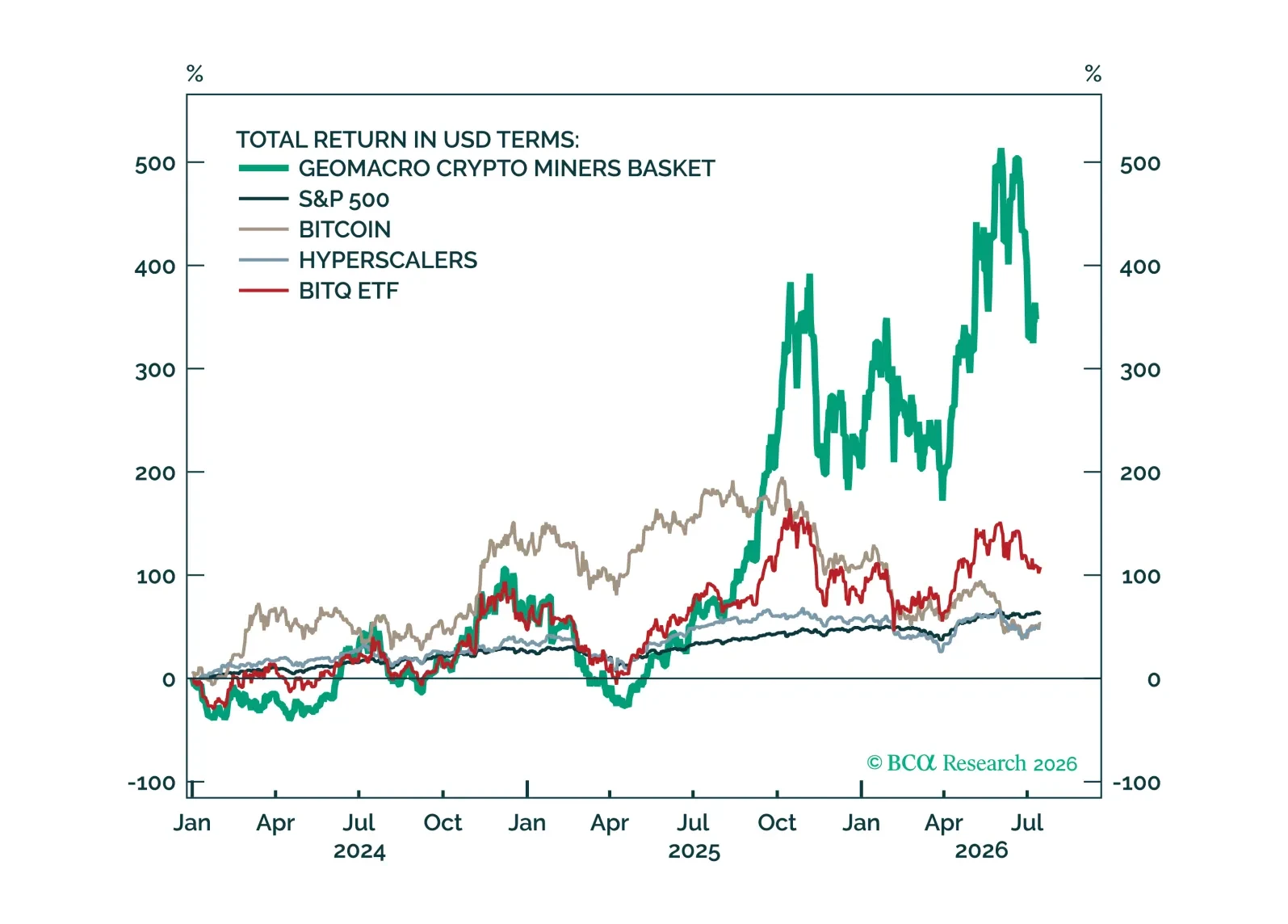

Bitcoin miners are transitioning from a pure crypto play to AI infrastructure landlords, offering investors exposure to both a crypto recovery and the surge in secular power demand driven by the AI capex buildout.

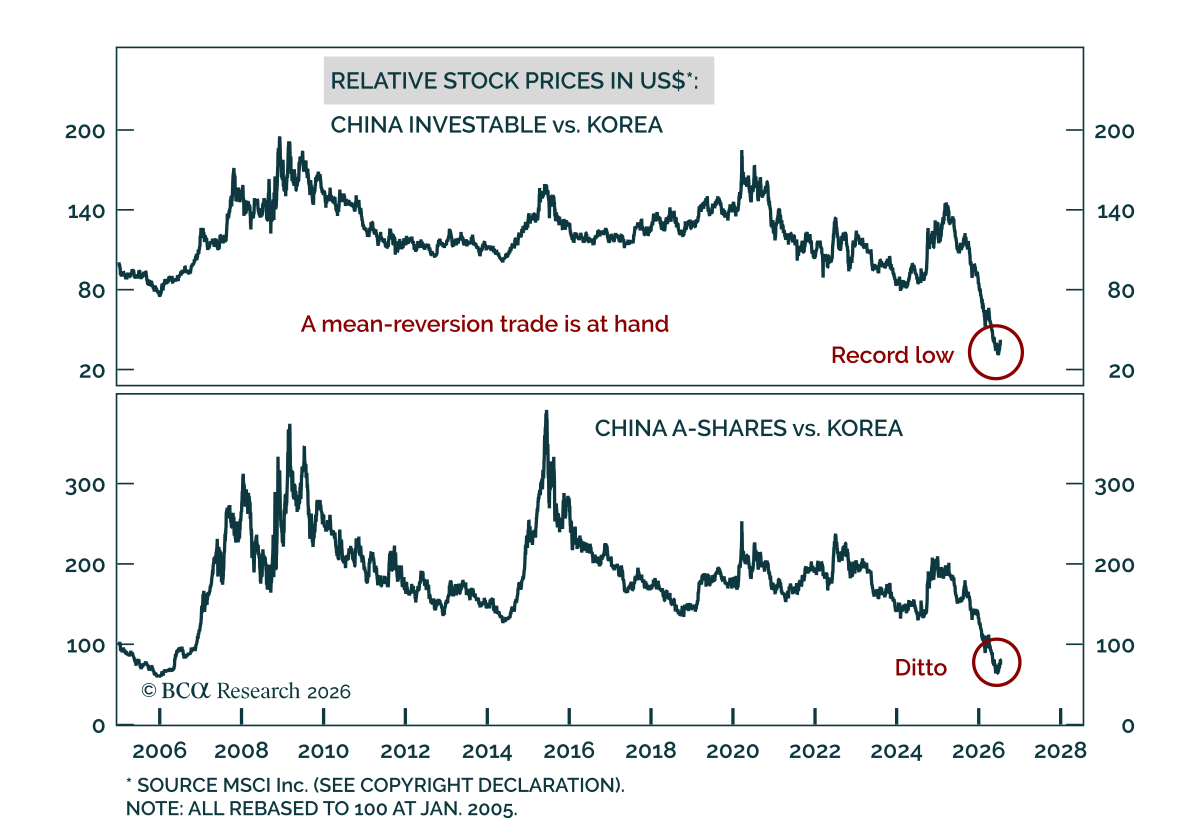

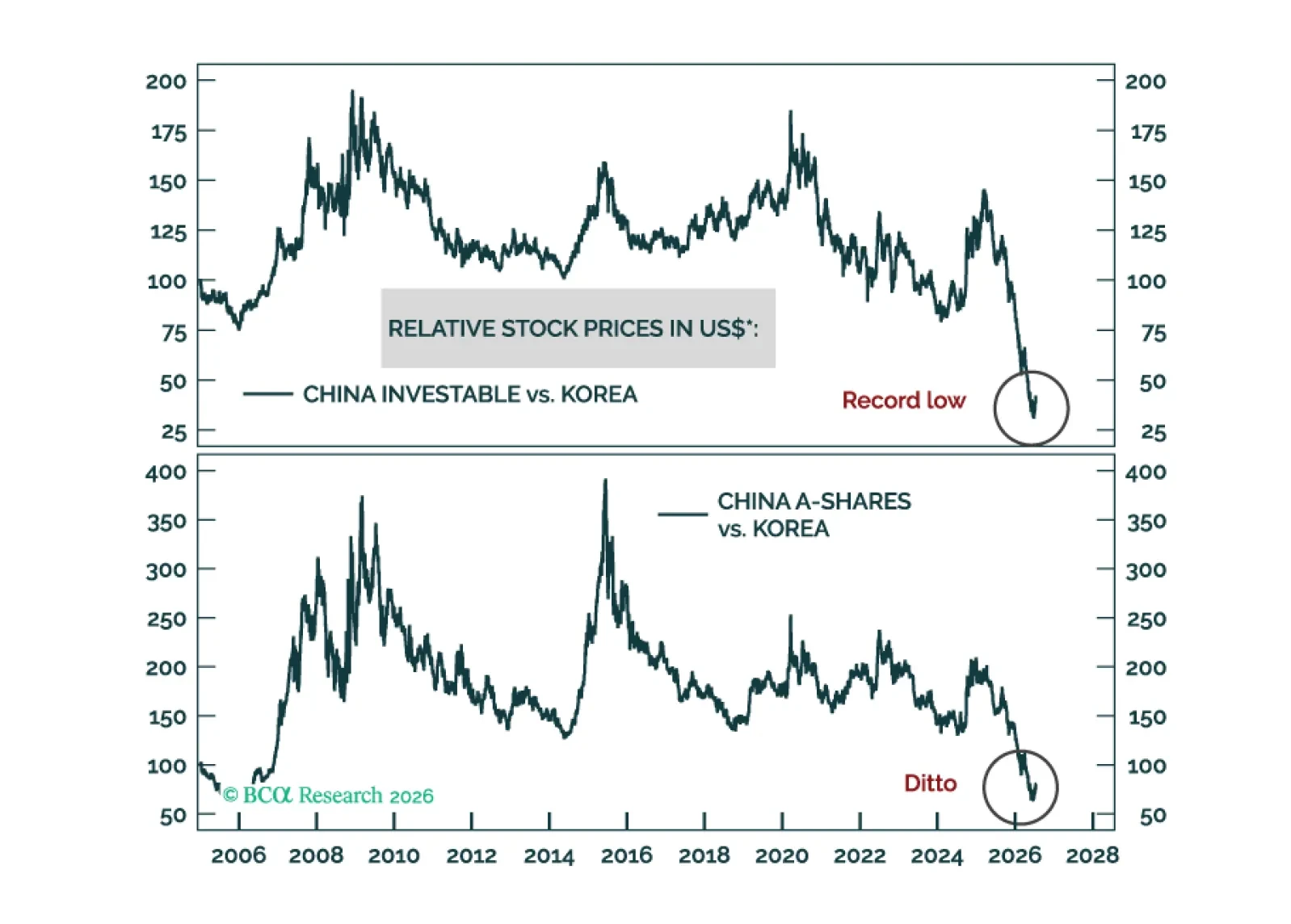

As a short-term (0-3 months) trade, go long an equal-weighted basket of Chinese Investable and A-shares / short the KOSPI. This is a bet on mean reversion. We do not recommend that medium- and long-term investors implement this strategy.

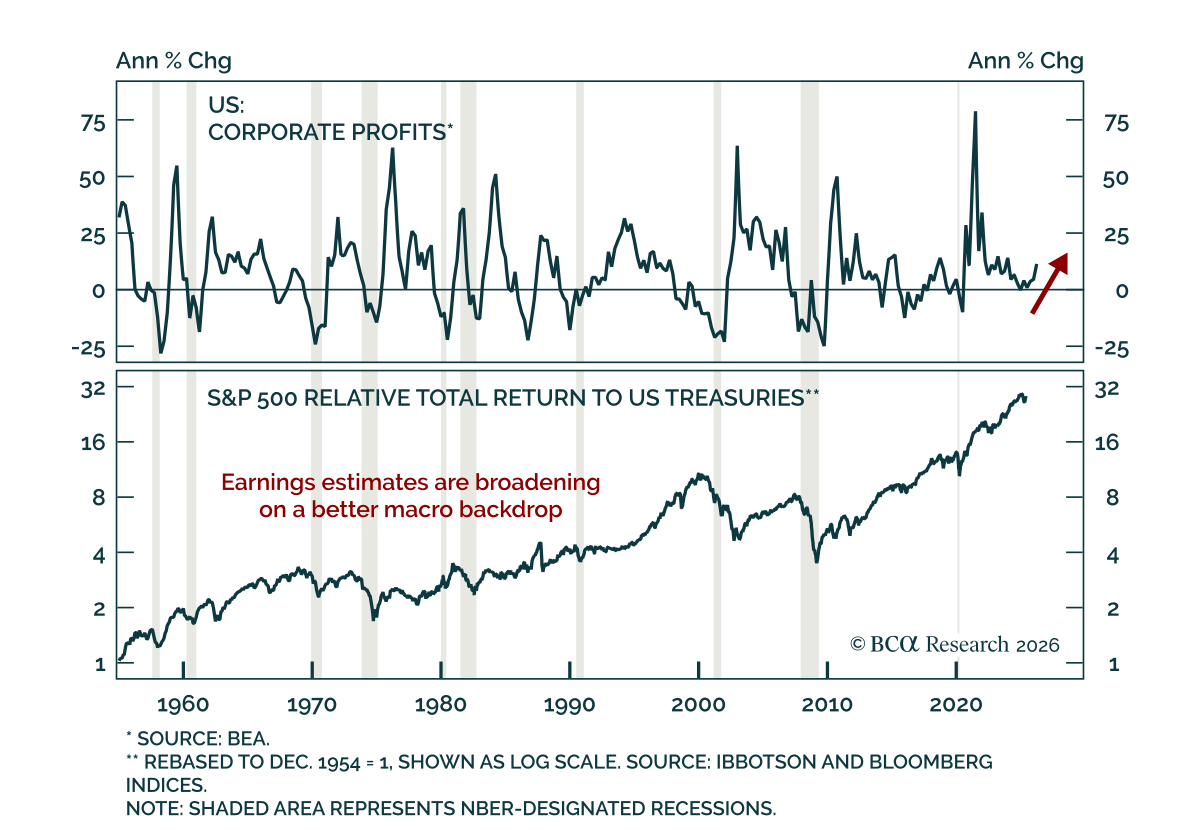

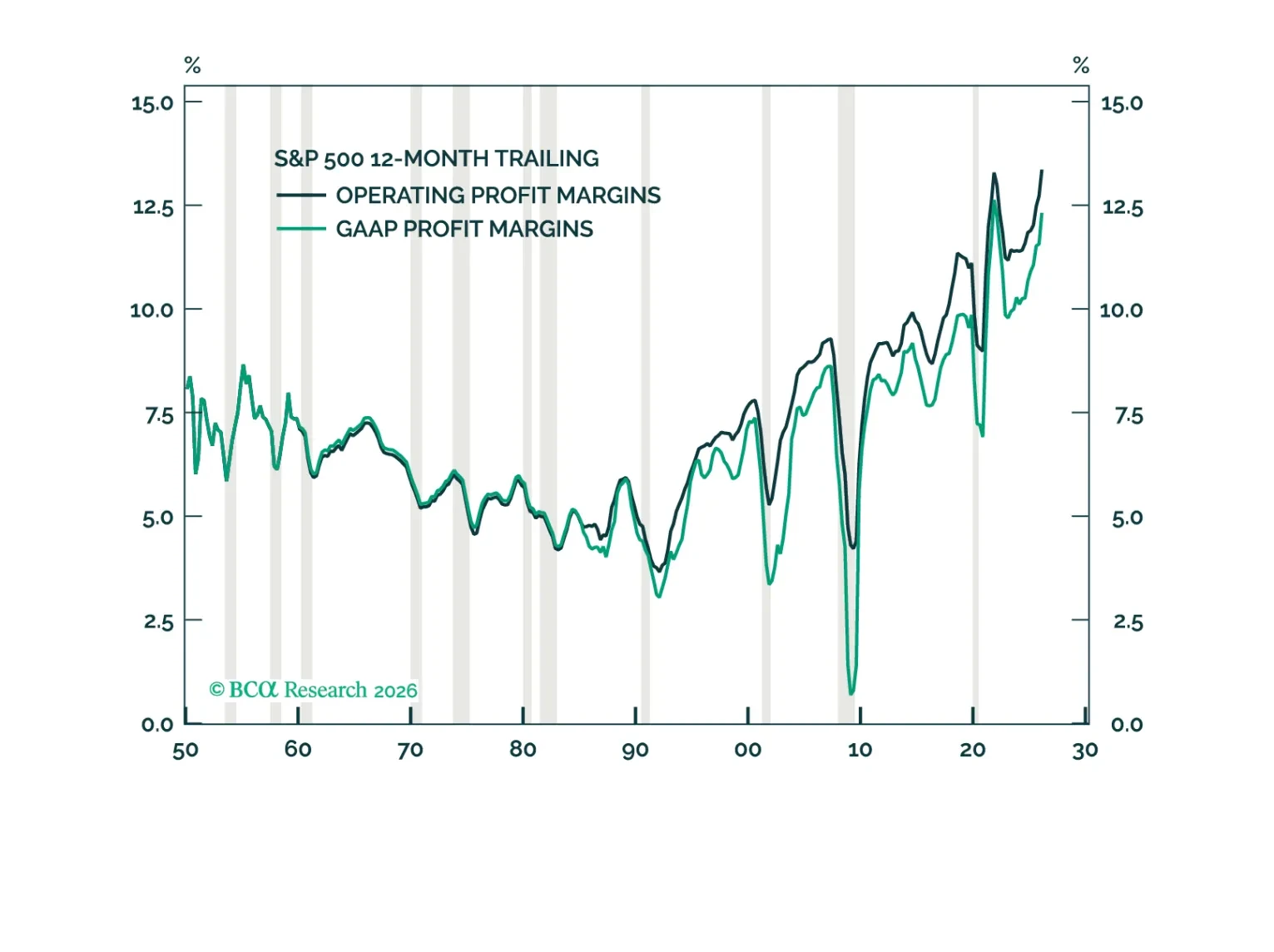

The Goldilocks environment for US profit margins should start to sour next year. Contrary to conventional wisdom, AI could end up eroding margins for both producers and consumers of artificial intelligence.