Energy

As long as the AI boom keeps booming, all other investment considerations will remain on the back burner. However, if the AI trade fizzles, this would expose deep-seated problems within the global economy, which could very well lead to an economic downturn as early as next year.

The UK economy is becoming increasingly fragile, but the investment outlook is improving. Slower growth and a more dovish BoE will support gilts, while UK equities will likely benefit from a favorable sector mix and a weaker pound.

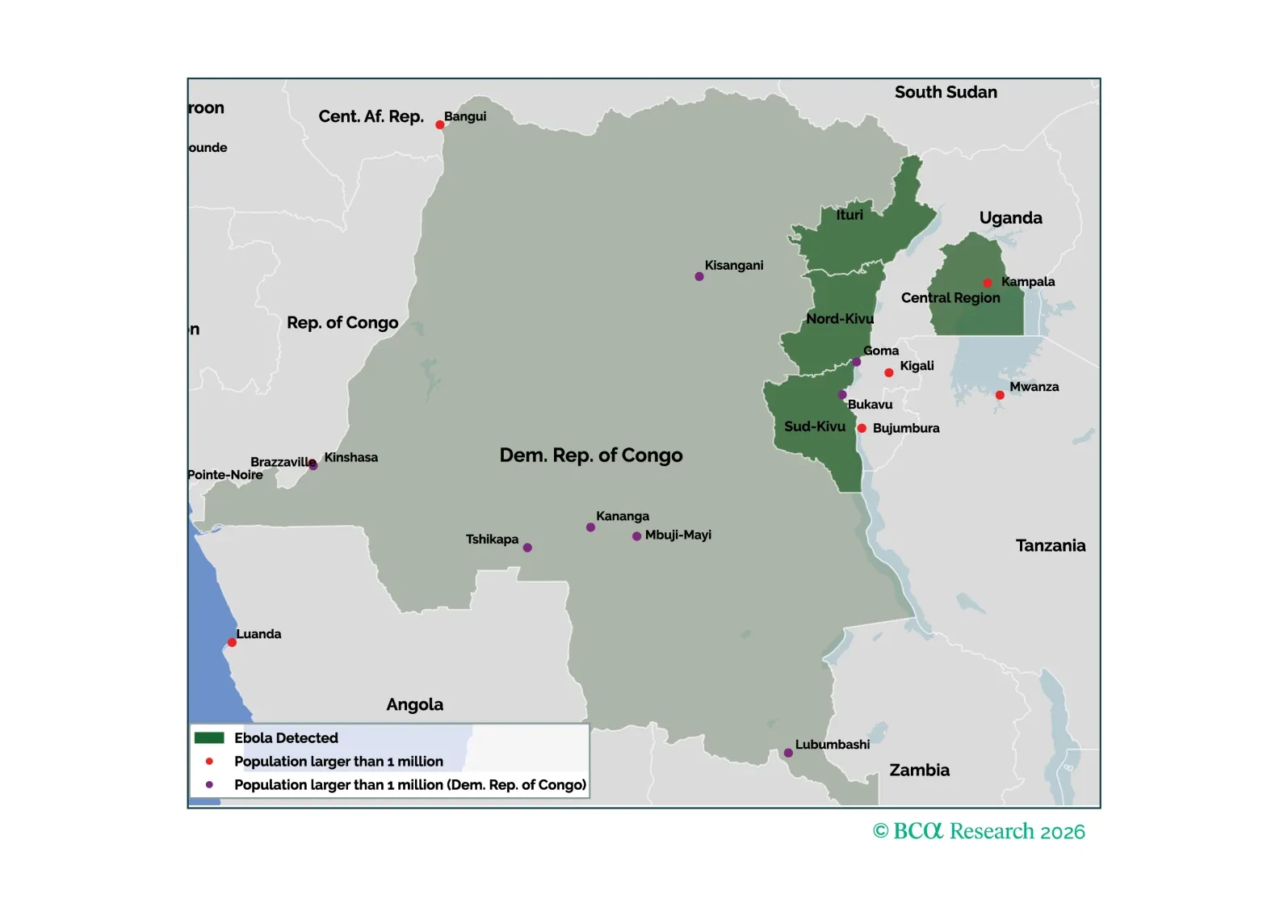

Ebola remains one of the world's deadliest viral diseases, but it is far less transmissible than COVID-19 or influenza. The most likely outcome remains containment rather than a global pandemic.

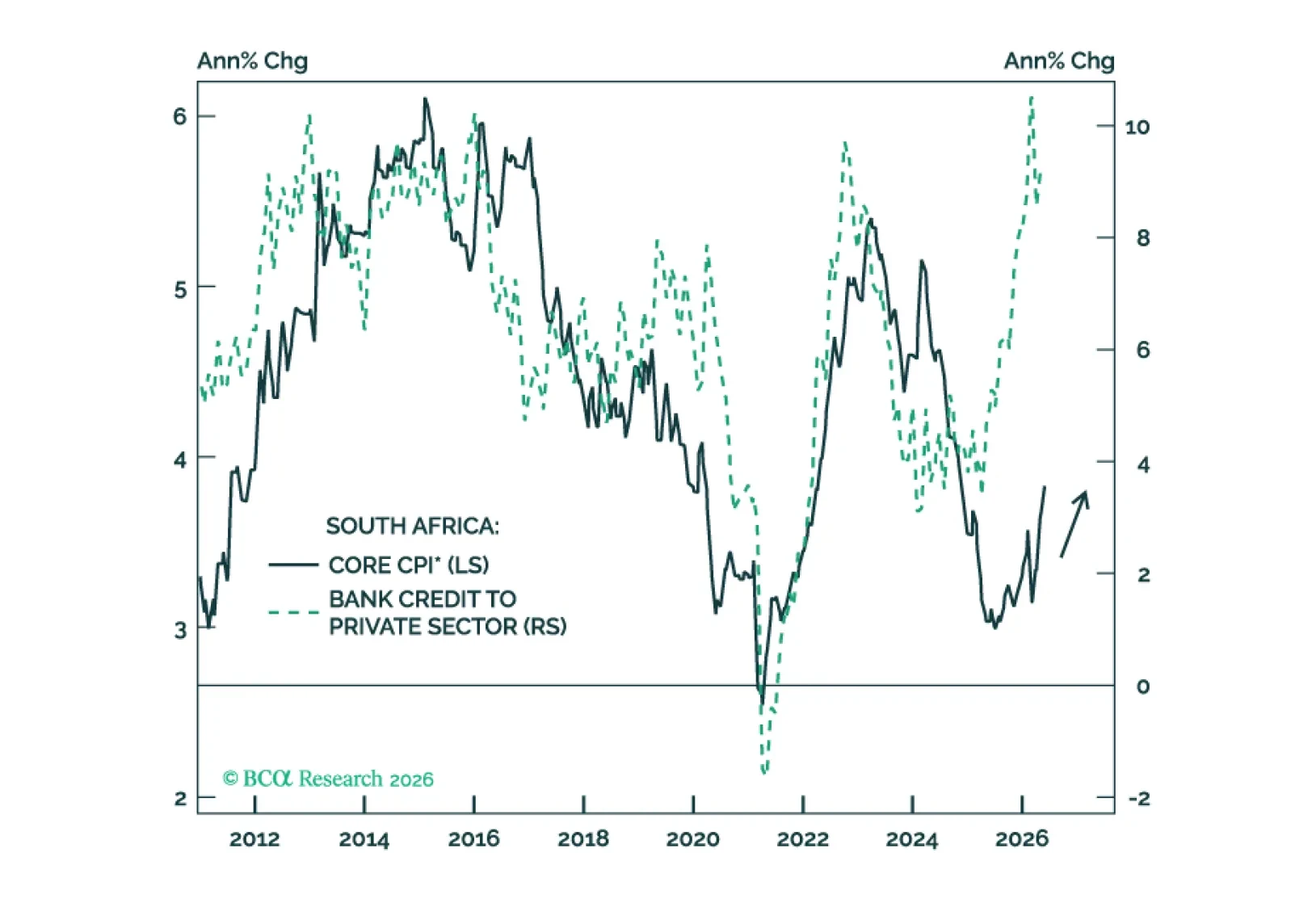

South Africa’s ambitious reform agenda will take time to bear fruit. Meanwhile, the country faces a stagflationary squeeze as inflation rises while growth slows. South African stocks, bonds, and currency are all vulnerable.

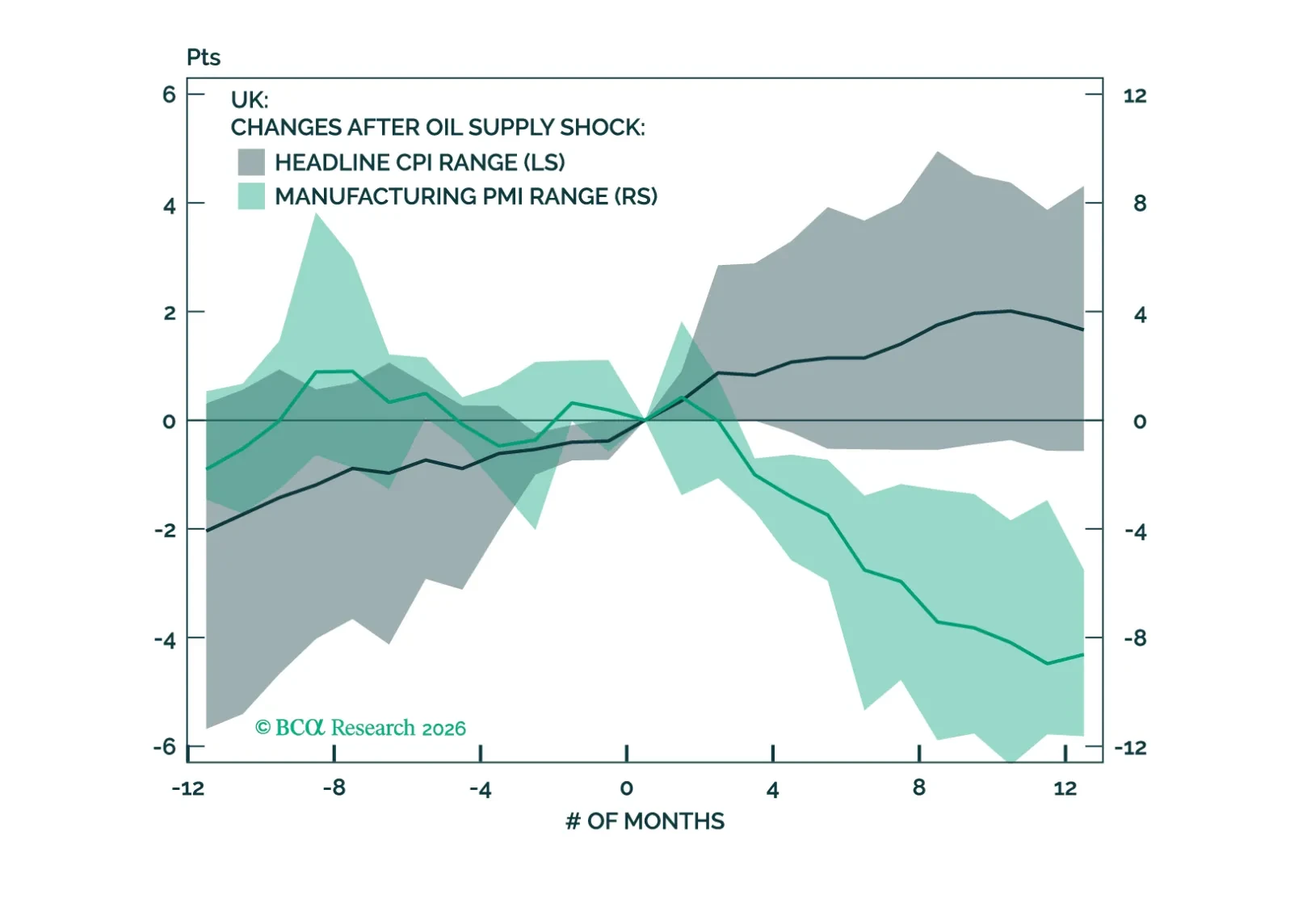

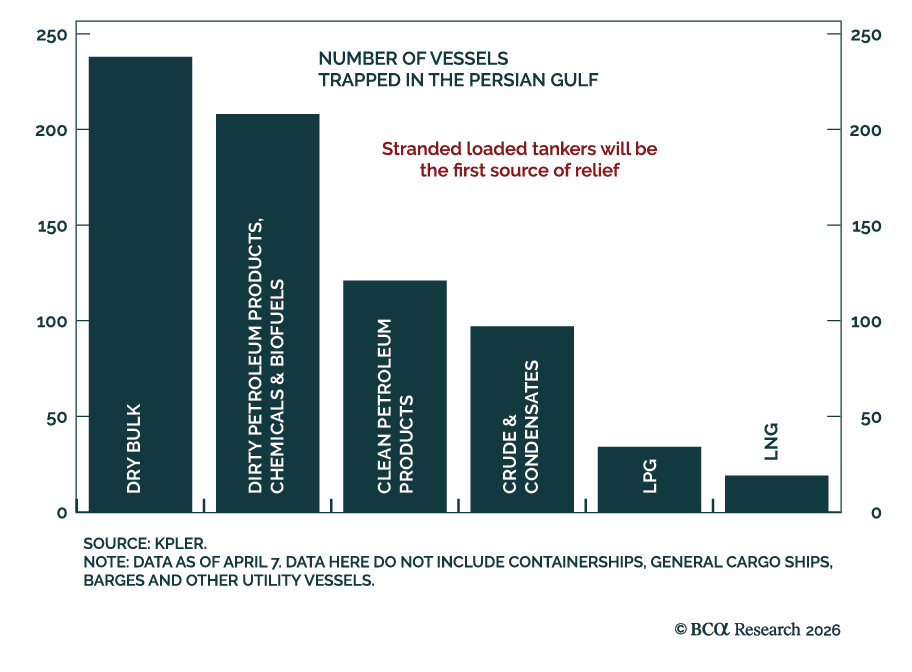

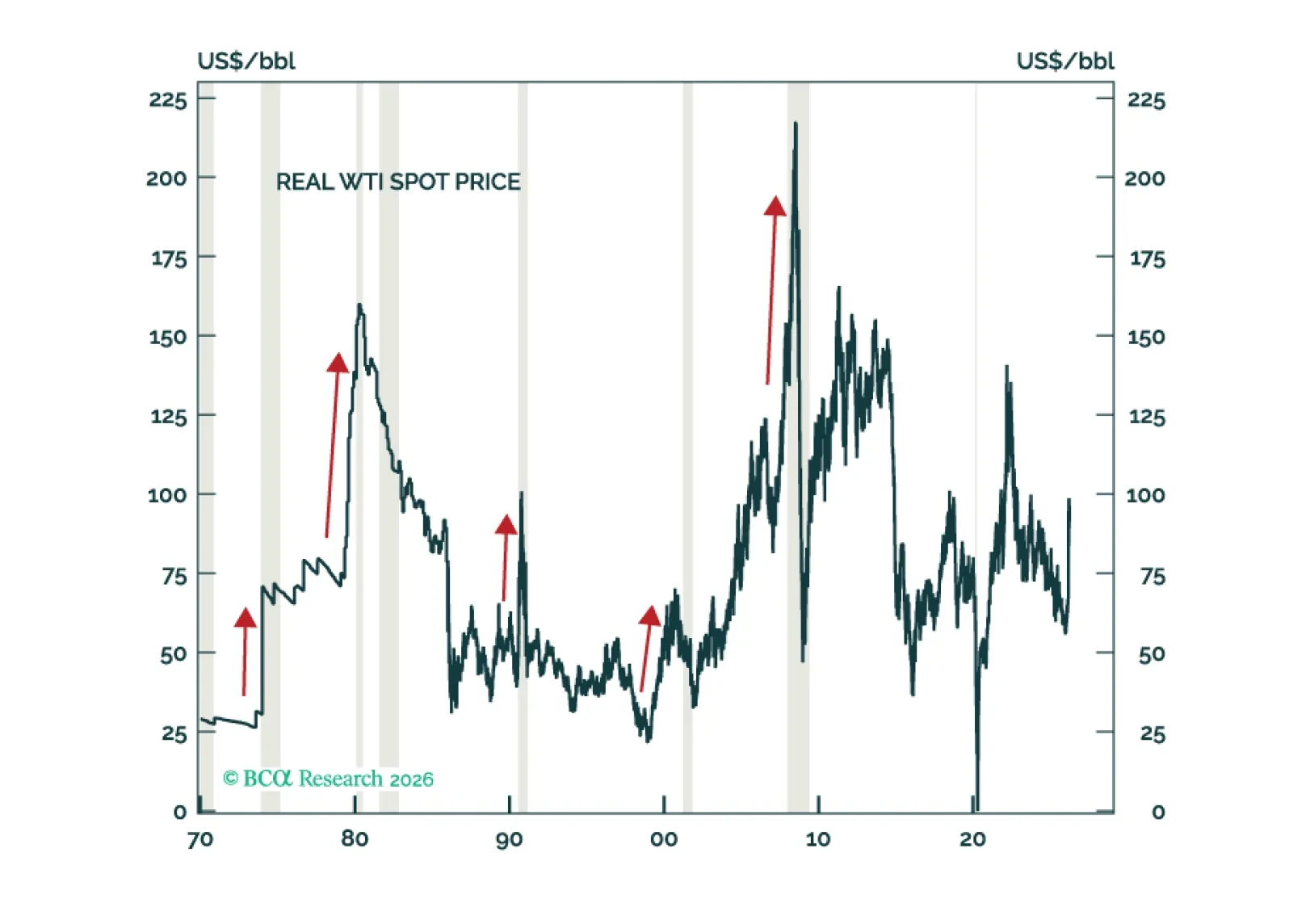

Volatility is high, but the path for yields is clearer than it looks. Across three oil scenarios, we show how policy responses shape fixed income markets and why the balance of risks still points to lower yields.

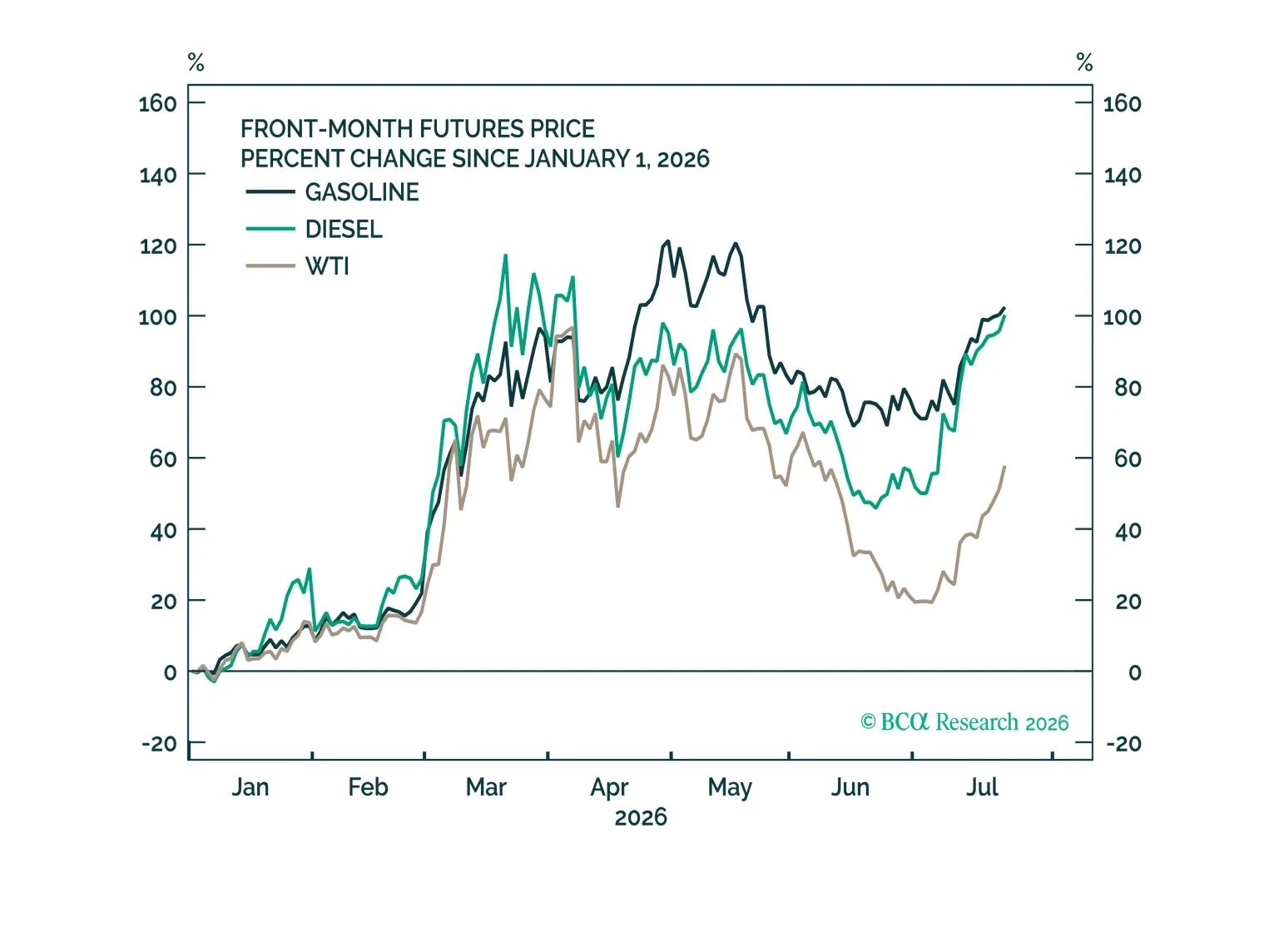

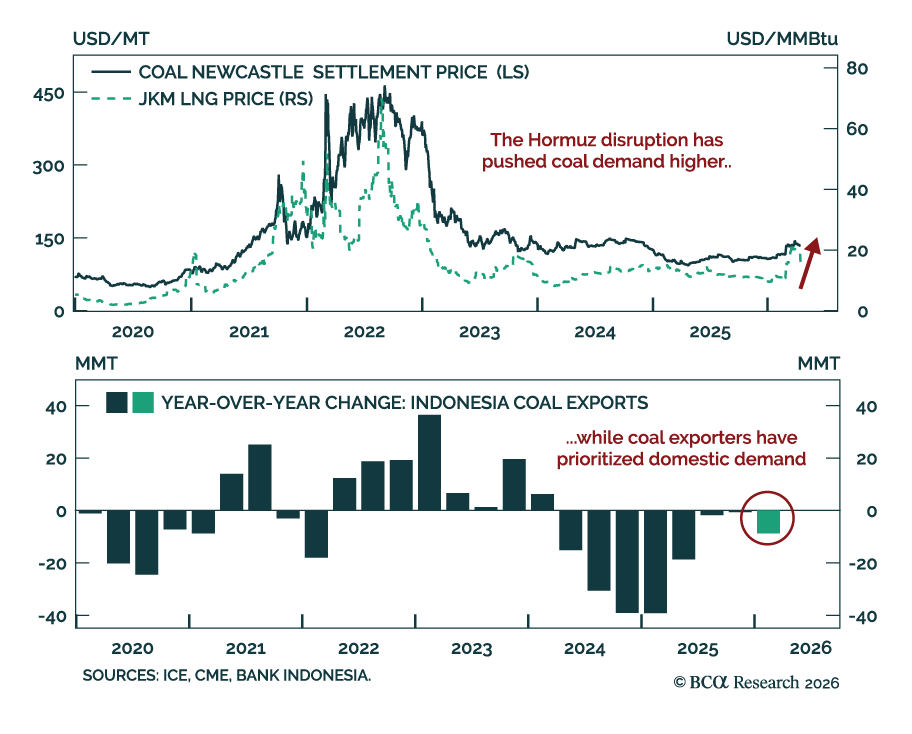

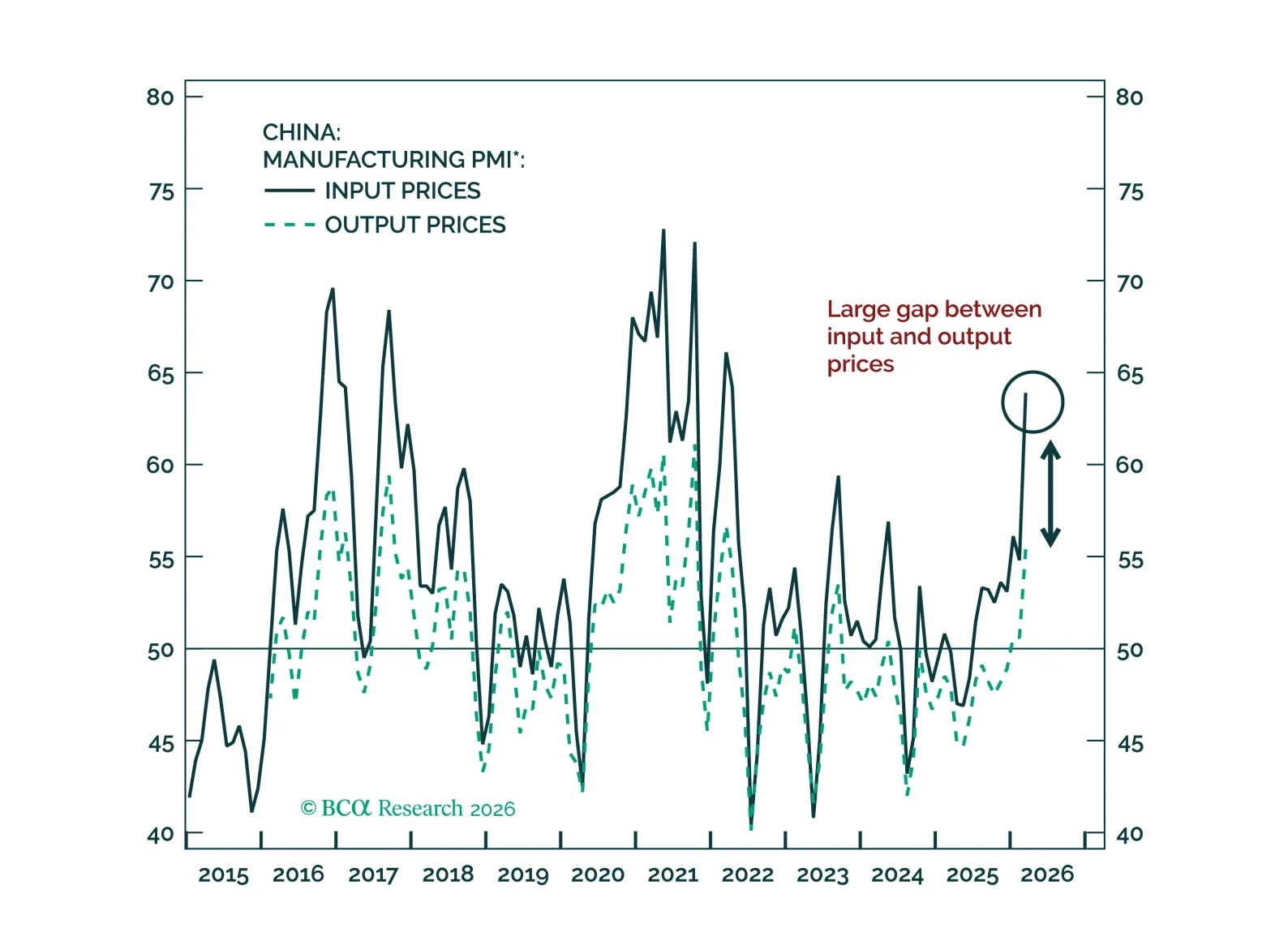

The ceasefire announced on Tuesday may signal peak intensity in the Middle East crisis, but sustained energy price pressures will continue to challenge Chinese corporate profitability.

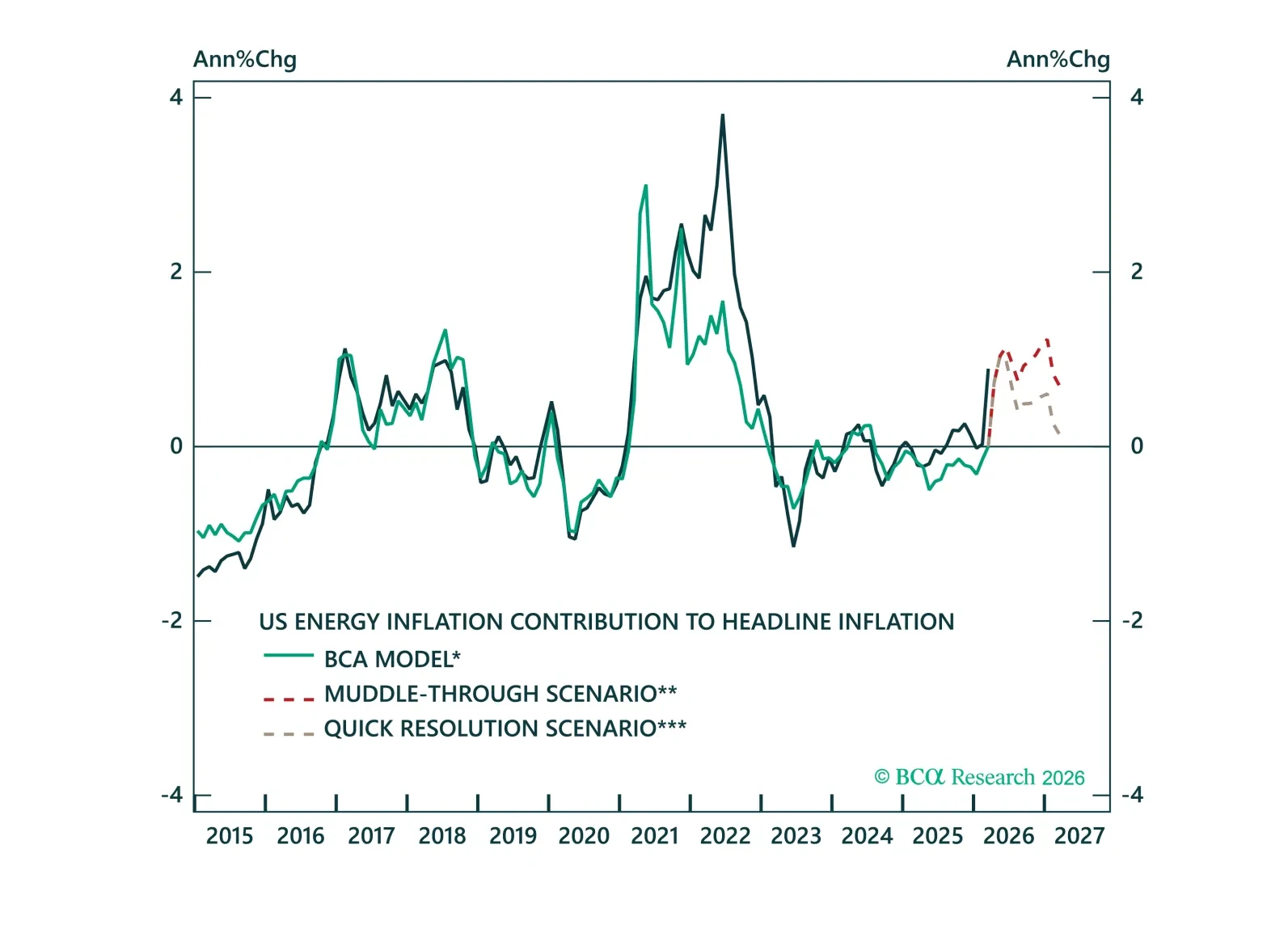

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.