Trade

As long as the AI boom keeps booming, all other investment considerations will remain on the back burner. However, if the AI trade fizzles, this would expose deep-seated problems within the global economy, which could very well lead to an economic downturn as early as next year.

We do not expect the oil shock to have a lasting effect on inflation. Looking further out, a variety of structural forces will influence inflation, including fiscal policy, globalization, demographics, and AI.

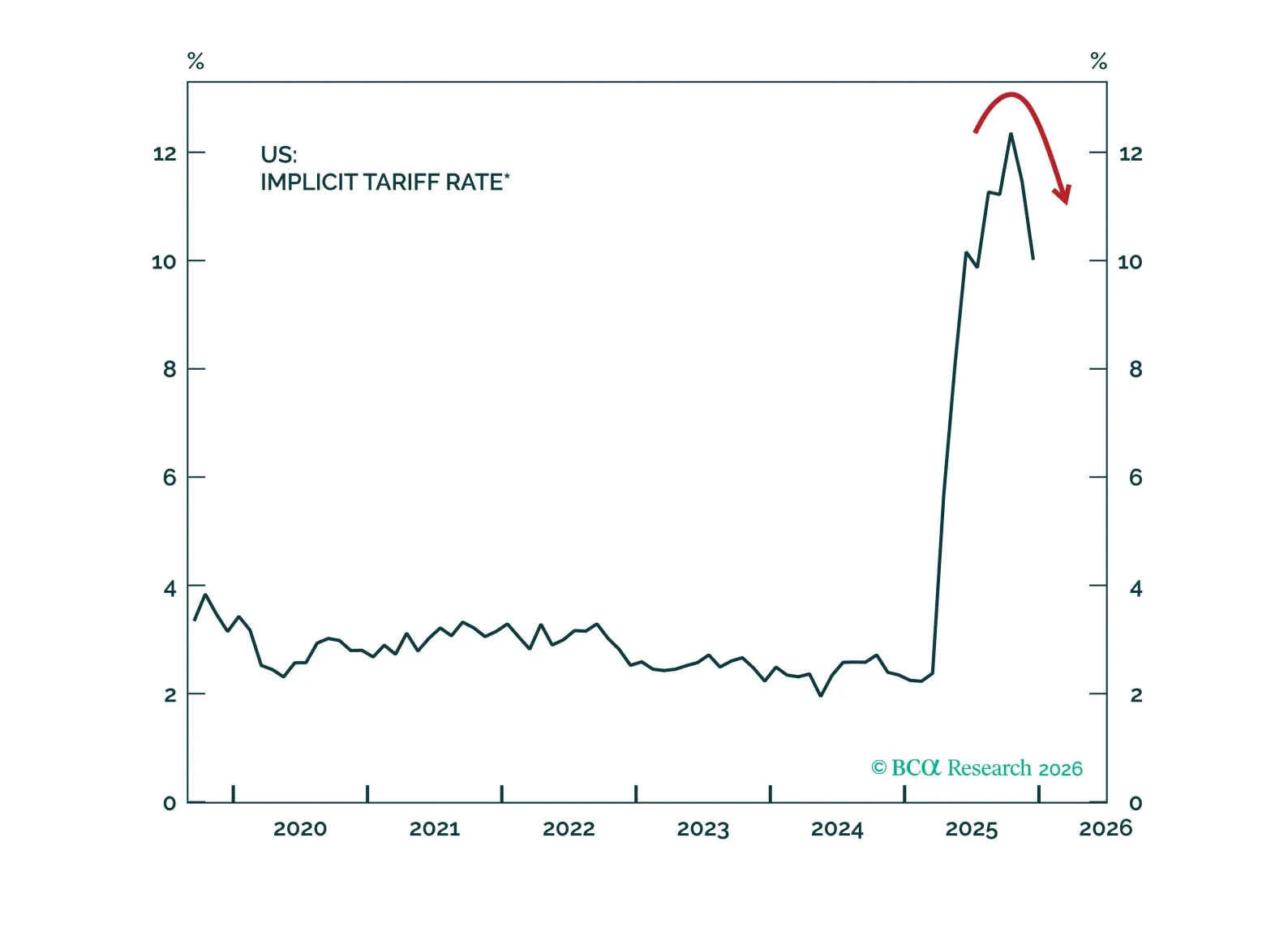

The Section 122 tariffs under the US Trade Act of 1974 are more favorable to Europe; the trade-weighted tariff rate falls to 10.45%, from 11.74% pre-ruling. This positive development does not change our overall views on Europe, as we expected lower tariffs ahead of the US midterms.

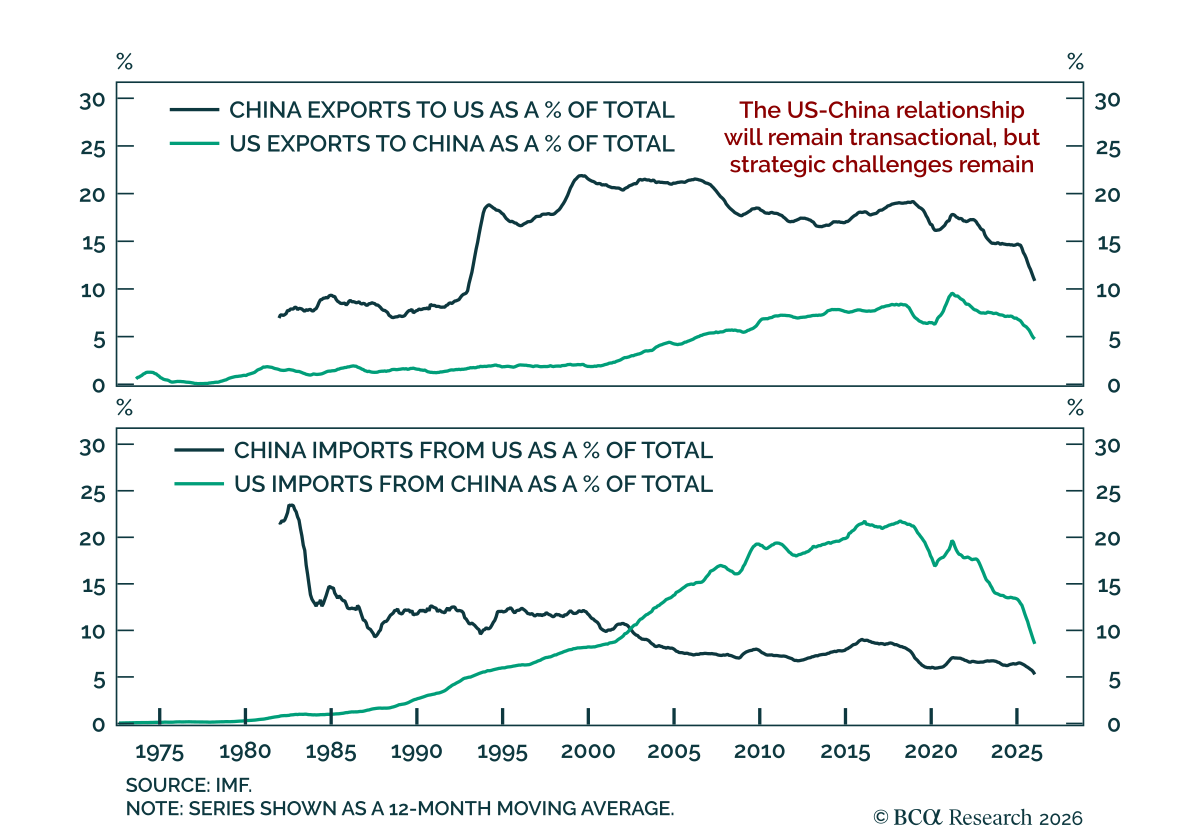

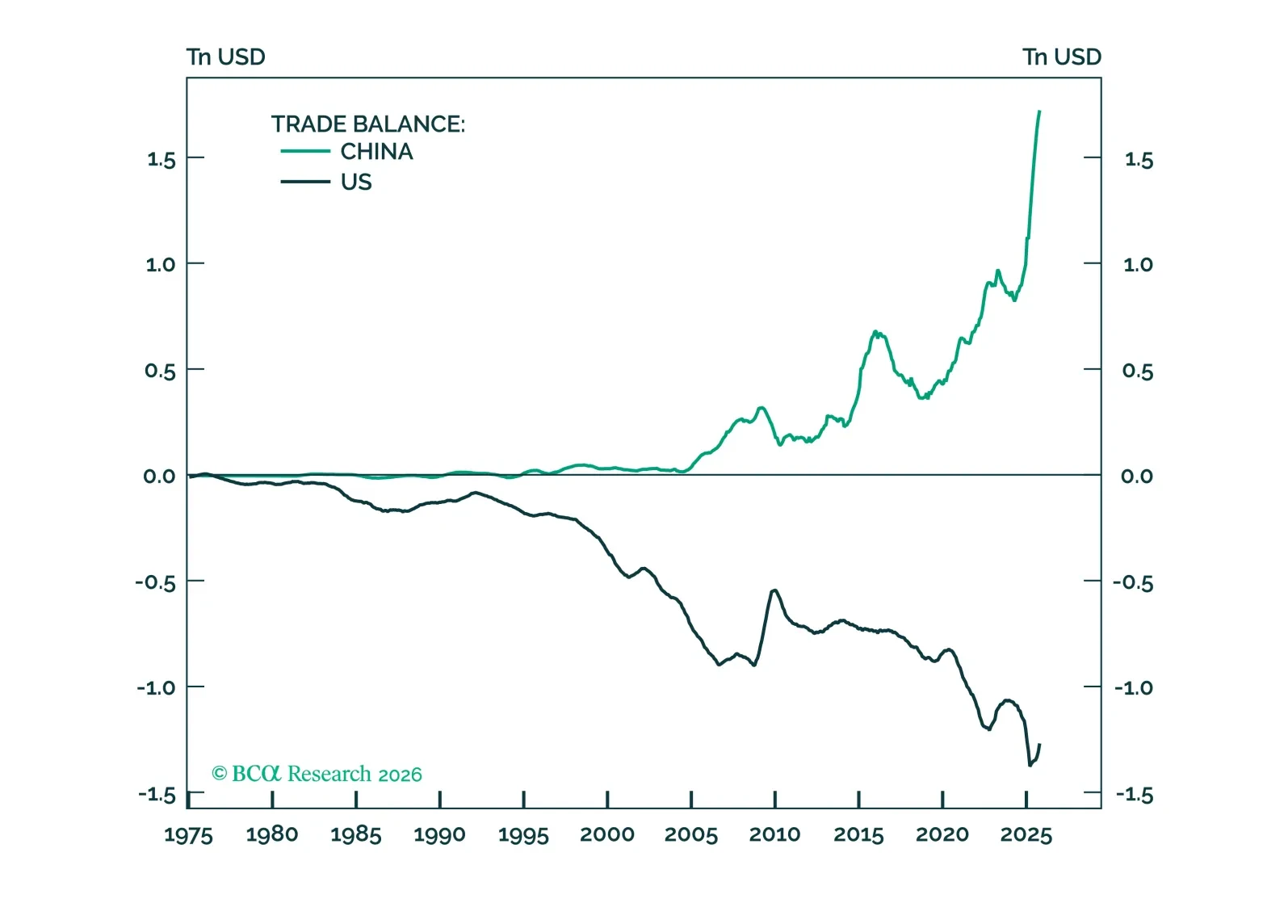

The CNY is undervalued and highly competitive. This gives China room to let the currency appreciate while remaining an export-driven powerhouse, gradually shifting from export intensity toward stronger domestic consumption. This achieves two objectives. First, it narrows the capital account deficit and strengthens the CNY’s role as a global anchor. Second, it enhances Beijing’s geopolitical autonomy by reducing reliance on foreign final demand.

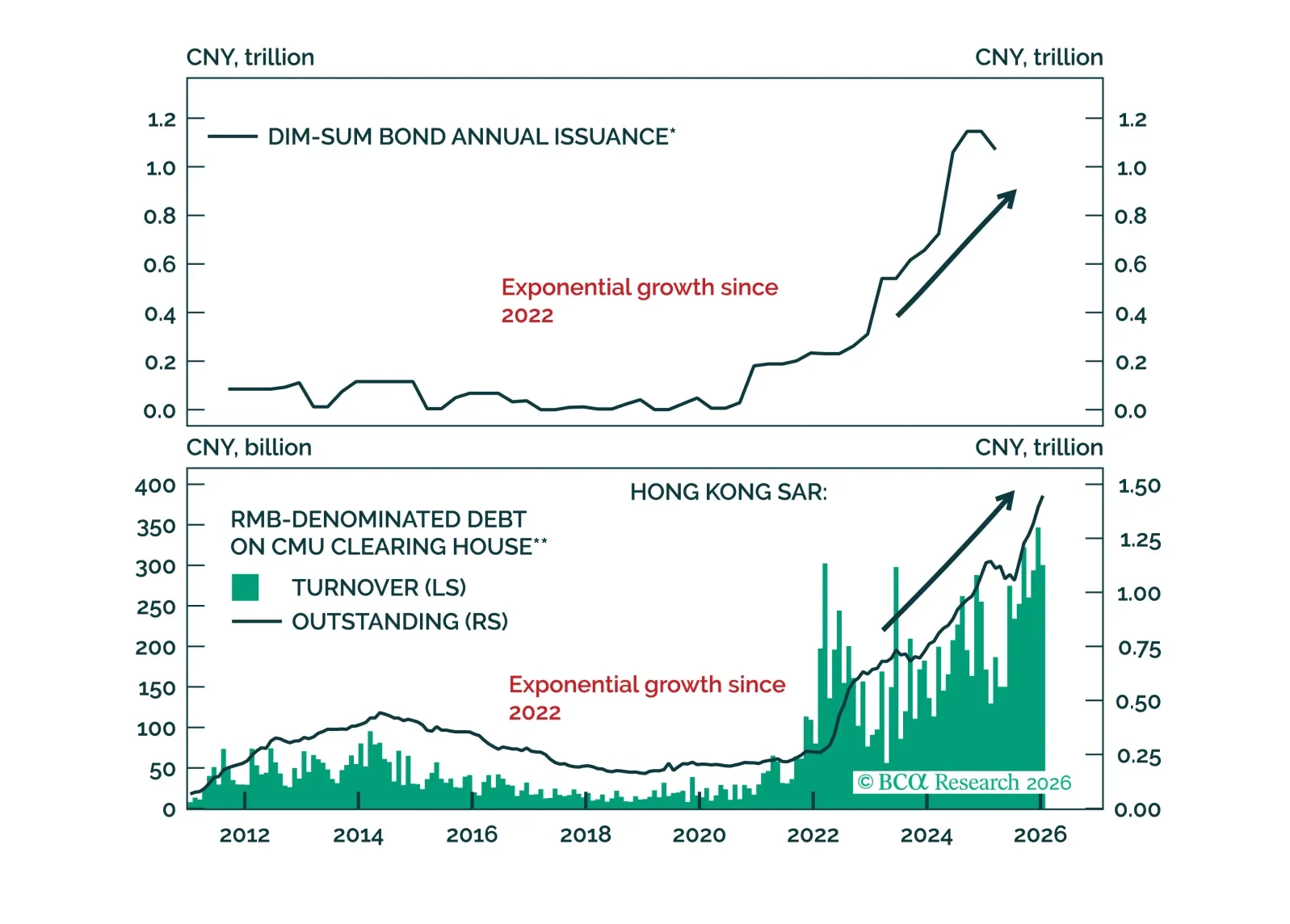

This Special Report assesses evidence of RMB’s involvement in global carry trades, examines its structural characteristics, and identifies key indicators of a potential unwind.

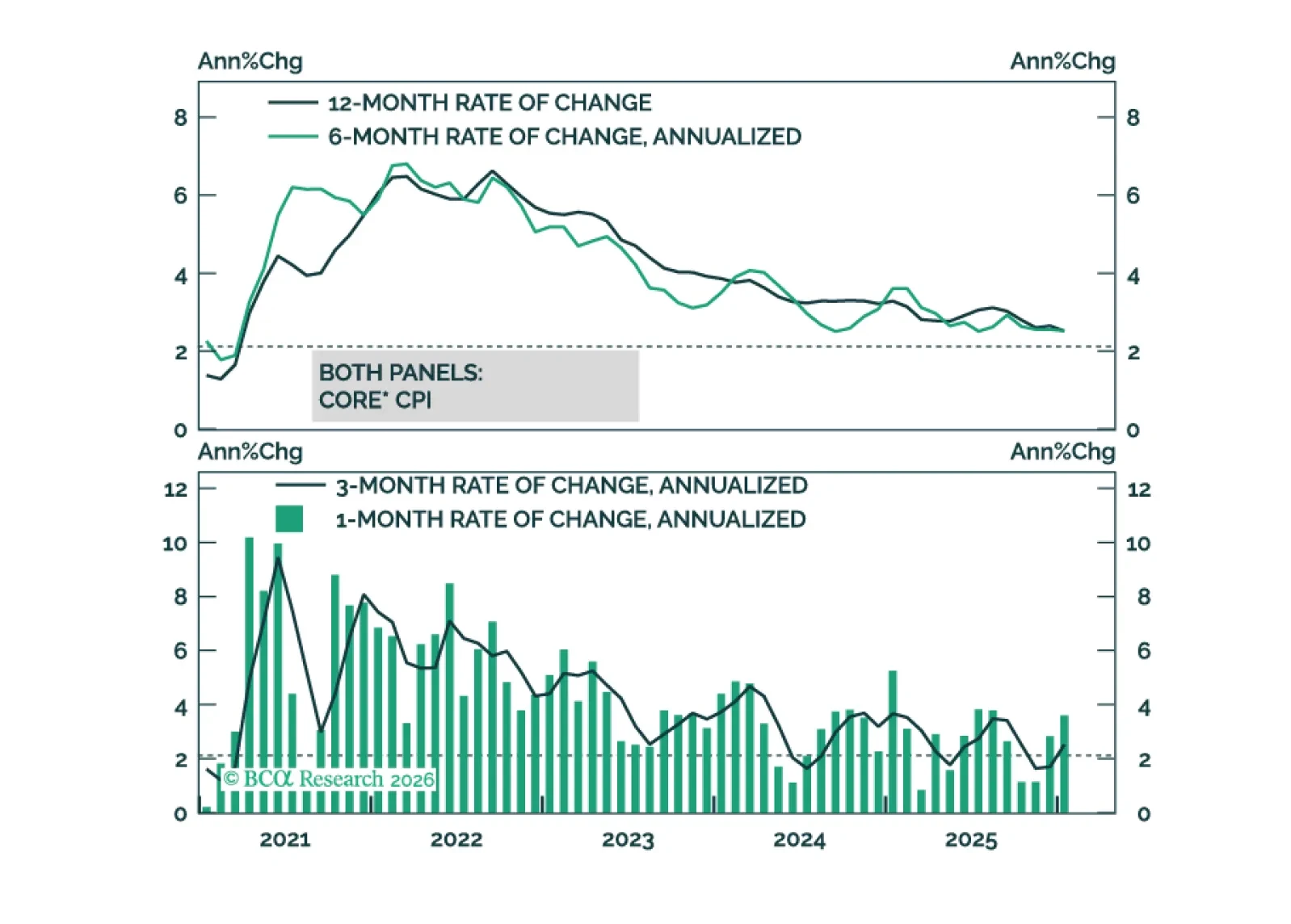

Core inflation will get close to the Fed’s 2% target by the end of this year.