Economy

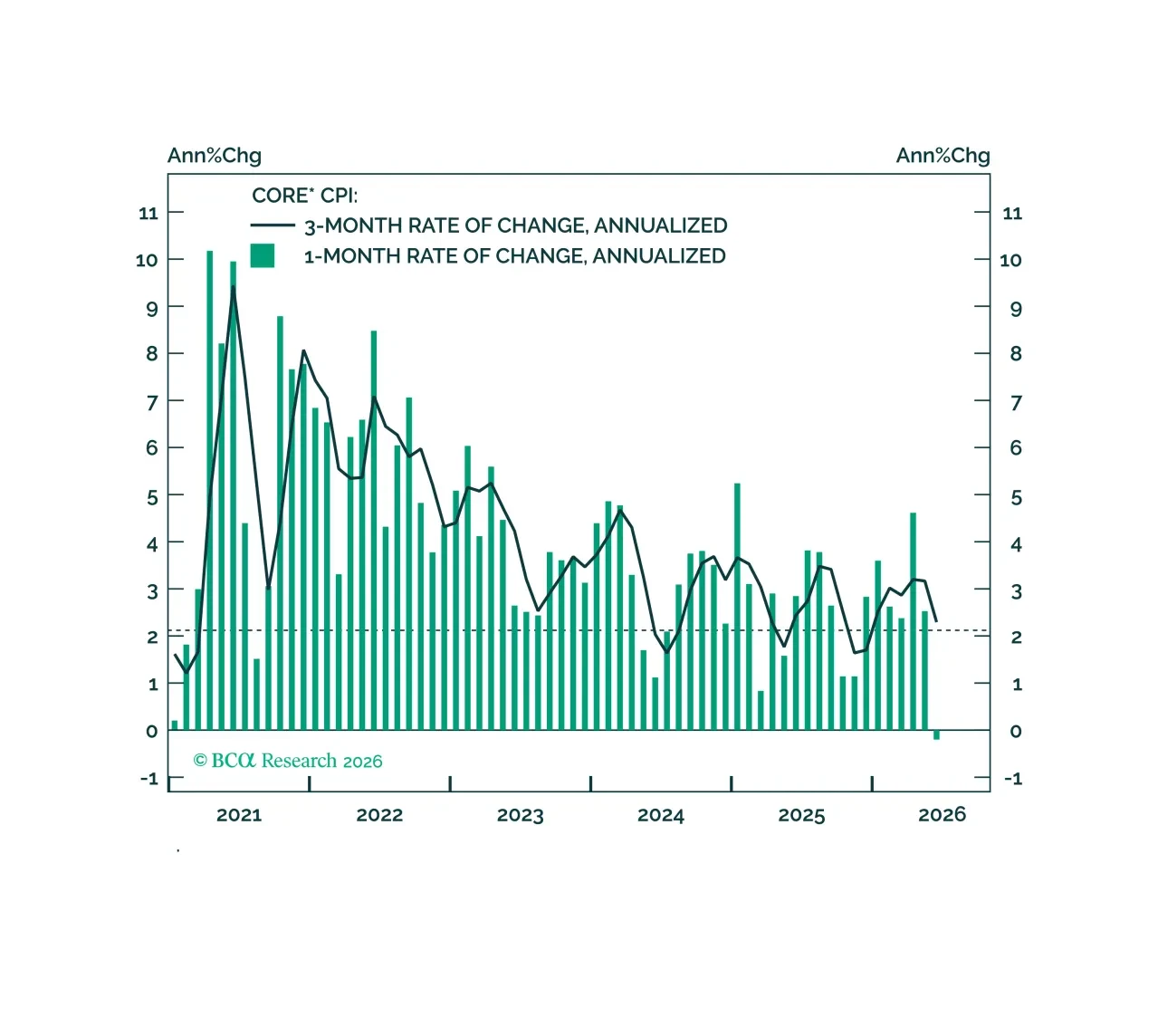

Despite today’s hold, the bar for a rate hike in September remains low and contingent on the next two core CPI reports.

Most Fed and pundit assessments of inflation expectations are overly narrow, focusing too much on long-term market-based measures. We favor a more qualitative approach that asks whether the inflation outlook is influencing household and business decision making.

As long as the AI boom keeps booming, all other investment considerations will remain on the back burner. However, if the AI trade fizzles, this would expose deep-seated problems within the global economy, which could very well lead to an economic downturn as early as next year.

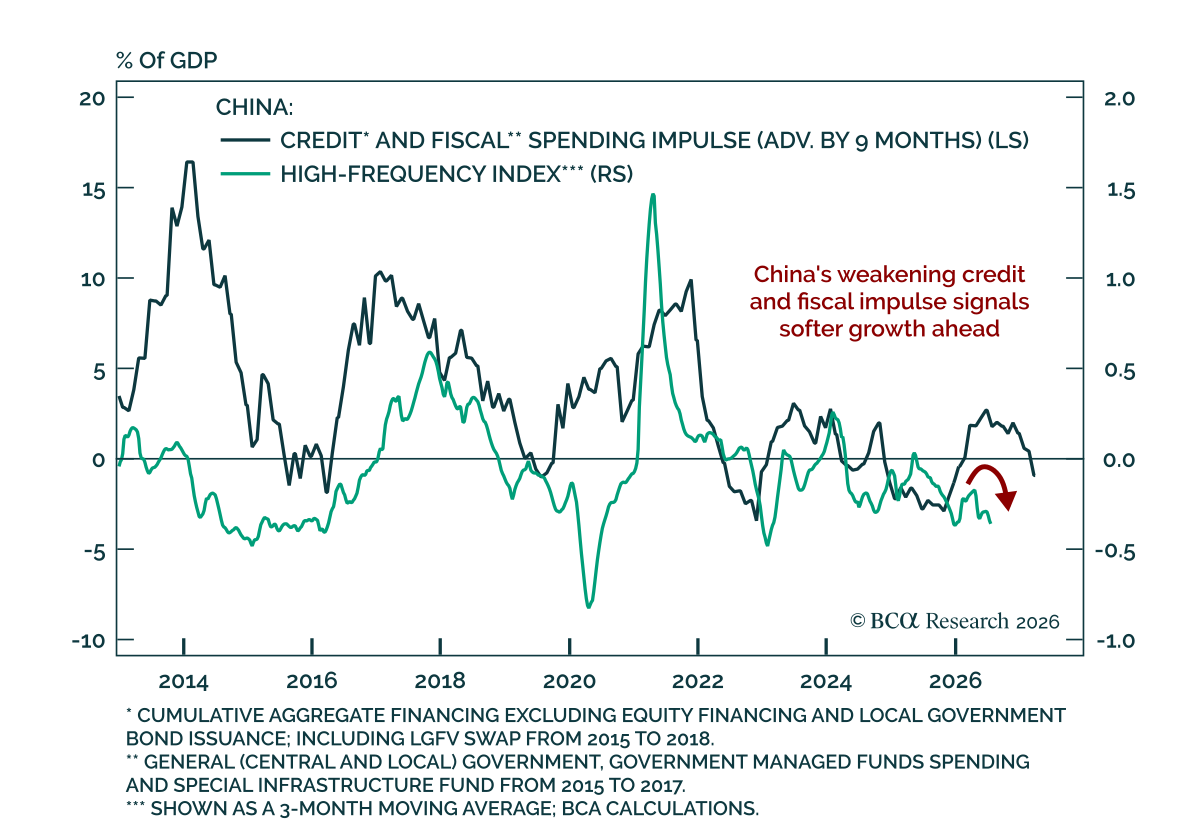

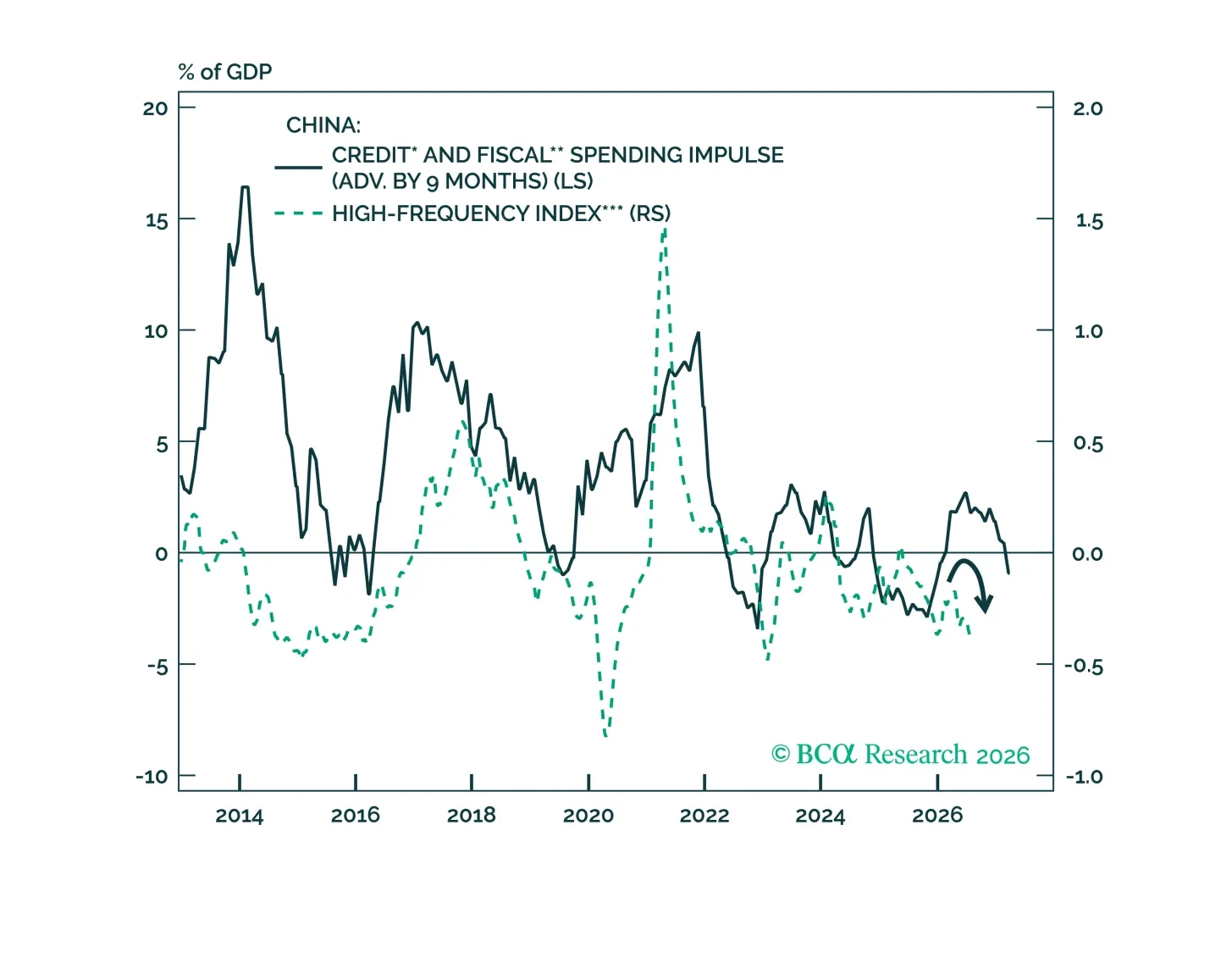

China's economy is slowing, but policymakers are unlikely to launch broad-based stimulus in H2. Meanwhile, the emergence of China's "Kimi moment" underscores Beijing's commitment to technological upgrading and the country's rapidly advancing AI capabilities.

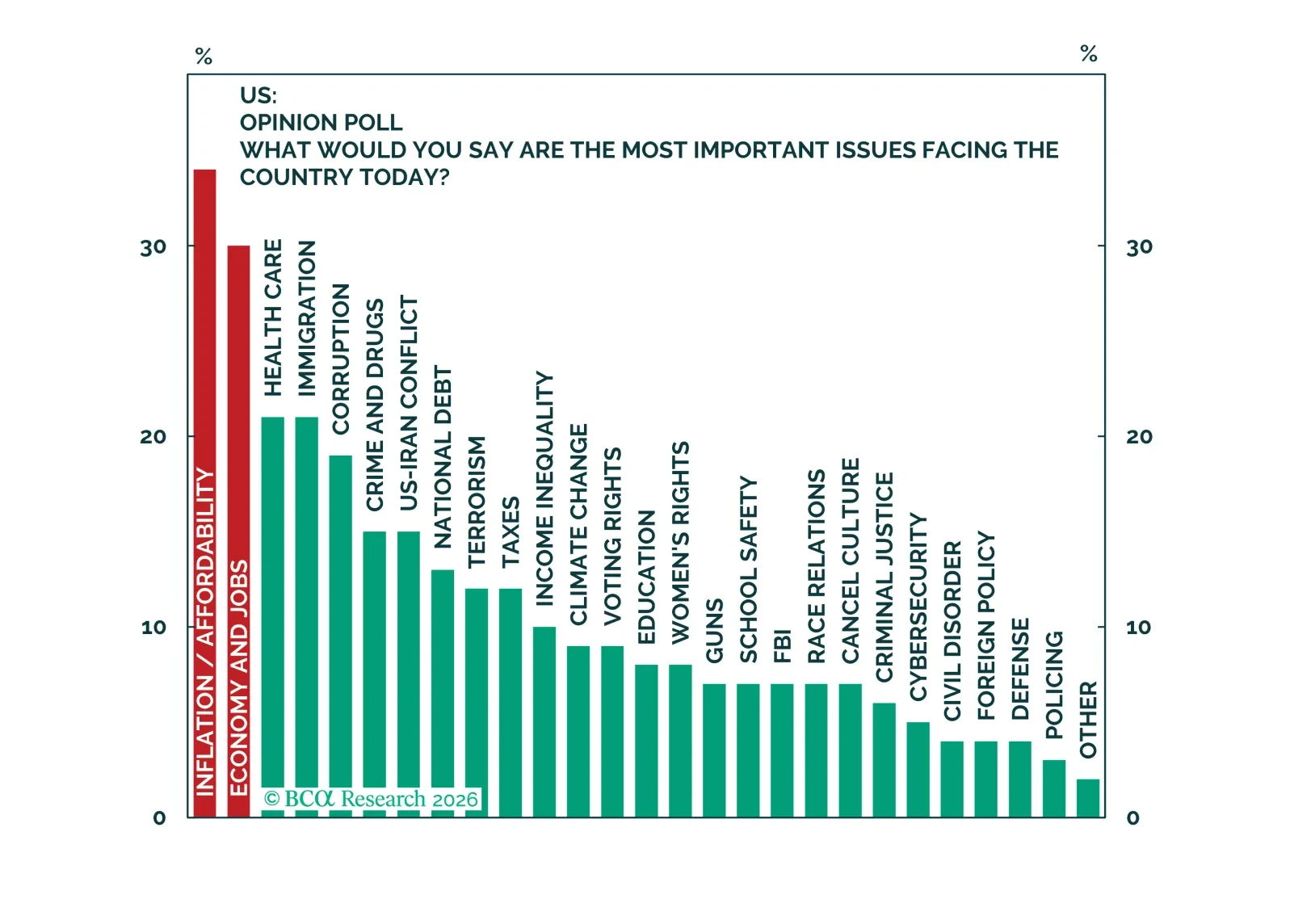

News flash: Young urban professionals are not gasping under the weight of an impossible rent burden. Investors should not be led astray by lightly examined popular narratives.

June’s low CPI reading rules out a July rate hike, but September is still on the table.

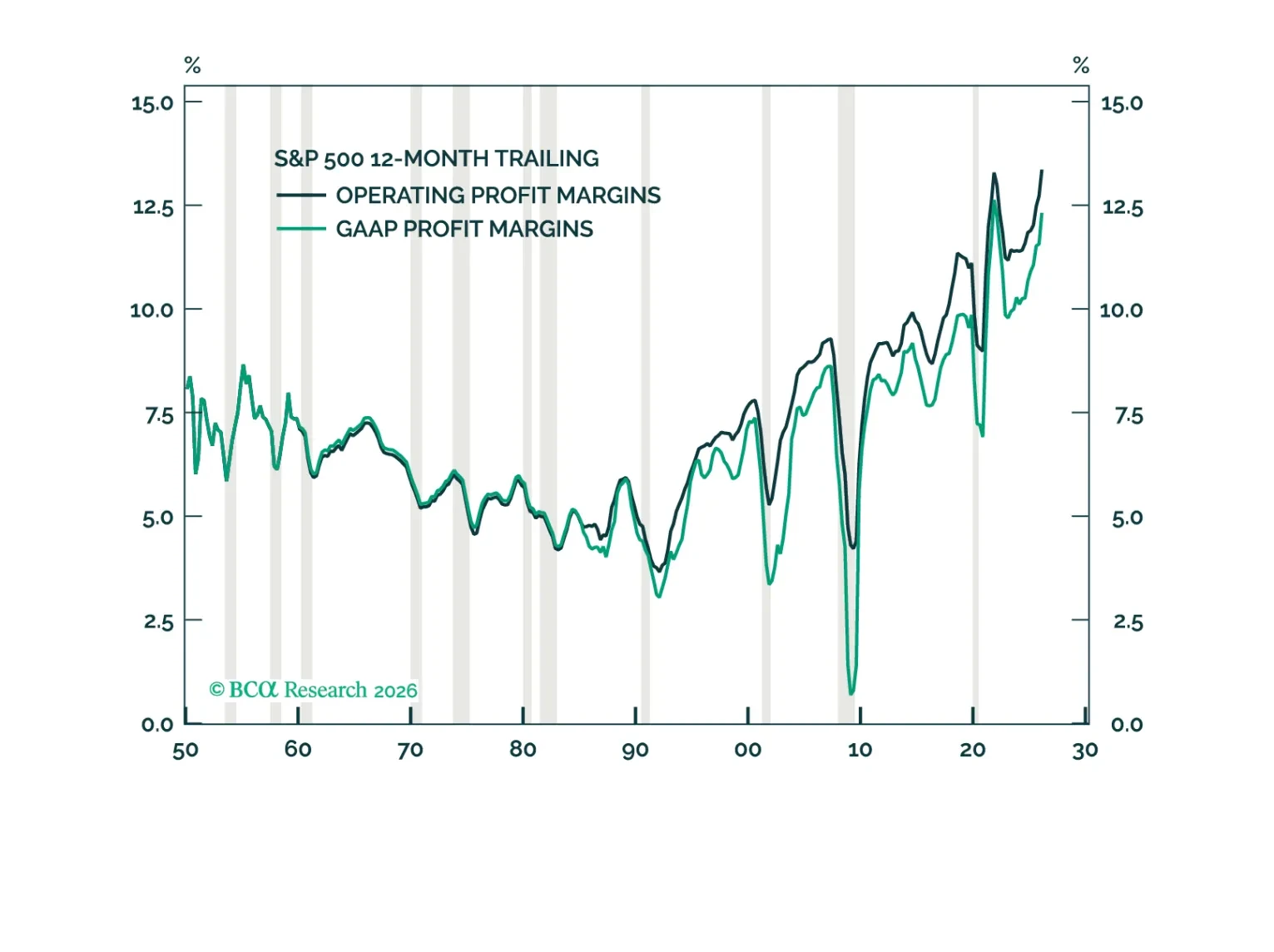

The Goldilocks environment for US profit margins should start to sour next year. Contrary to conventional wisdom, AI could end up eroding margins for both producers and consumers of artificial intelligence.