Economy

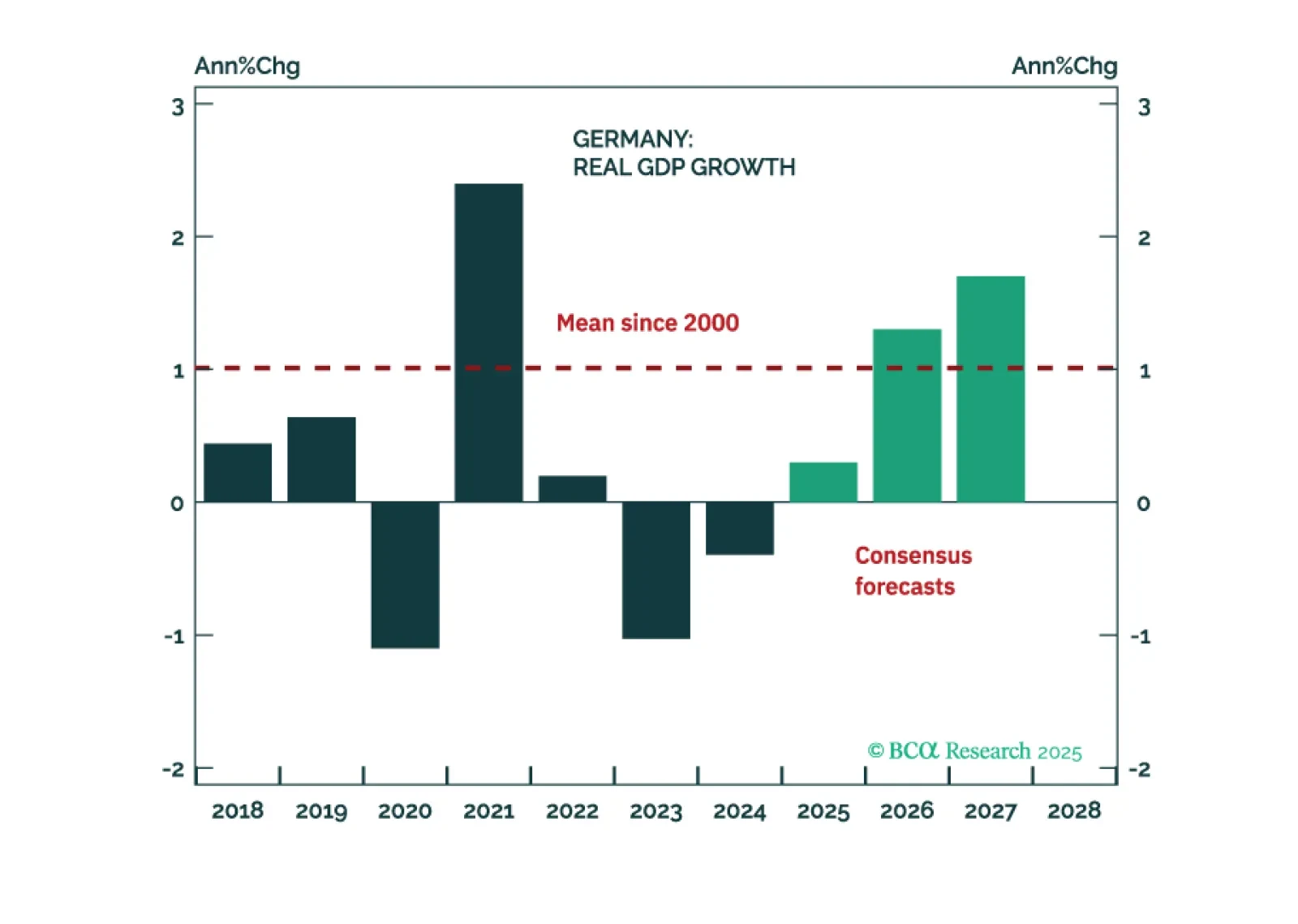

Germany’s economy is regaining momentum after nearly two years of recession. Despite the ongoing cyclical rebound and fiscal stimulus, political gridlock and deep-seated structural challenges threaten to limit the country’s long-term growth potential. Investors should be underweight German Bunds and favor Eurozone equities over German equities.

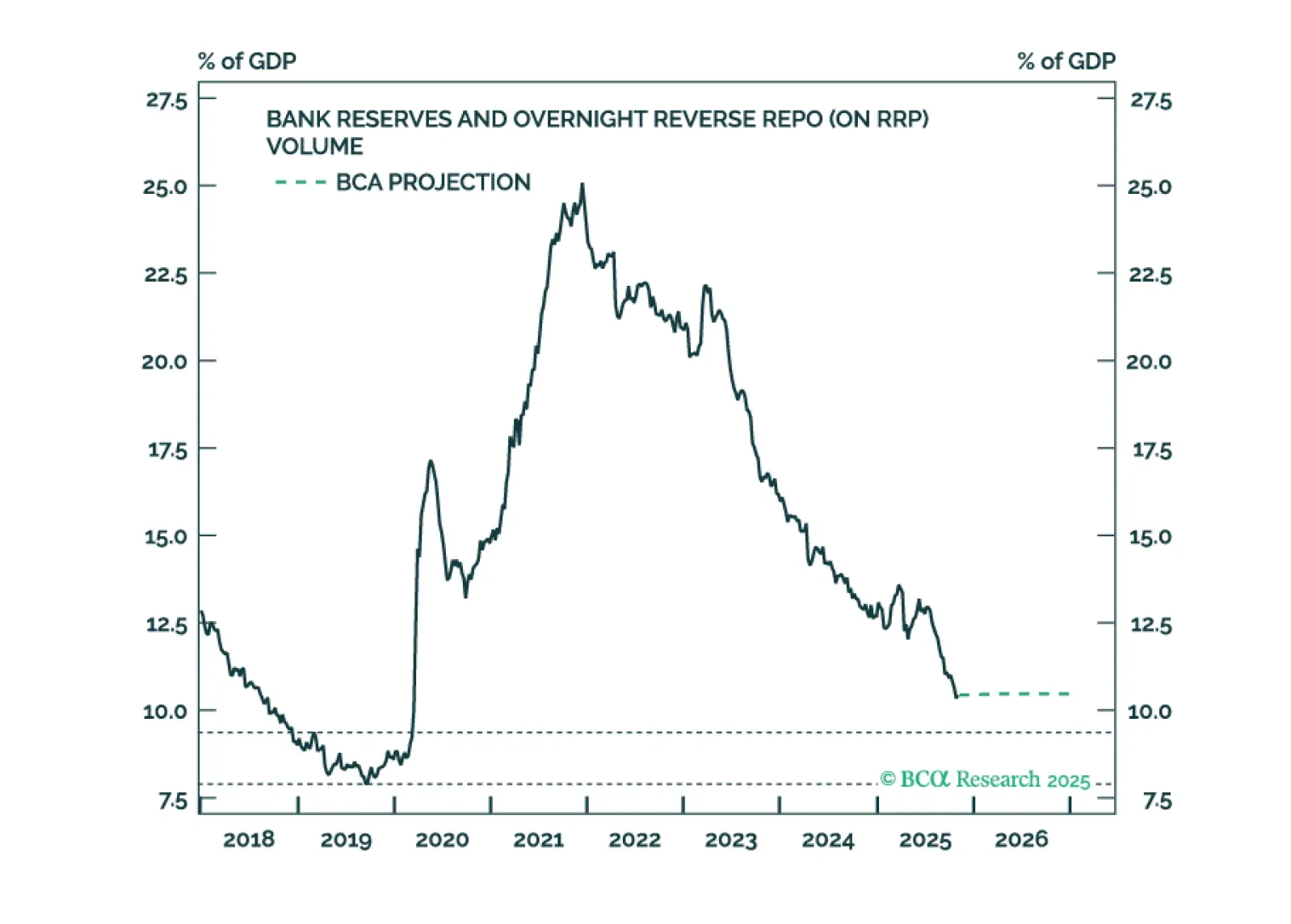

This Special Report outlines the Fed’s balance sheet strategy and the rationale behind it. We also provide updated projections for the major asset and liability line items on the Fed’s balance sheet.

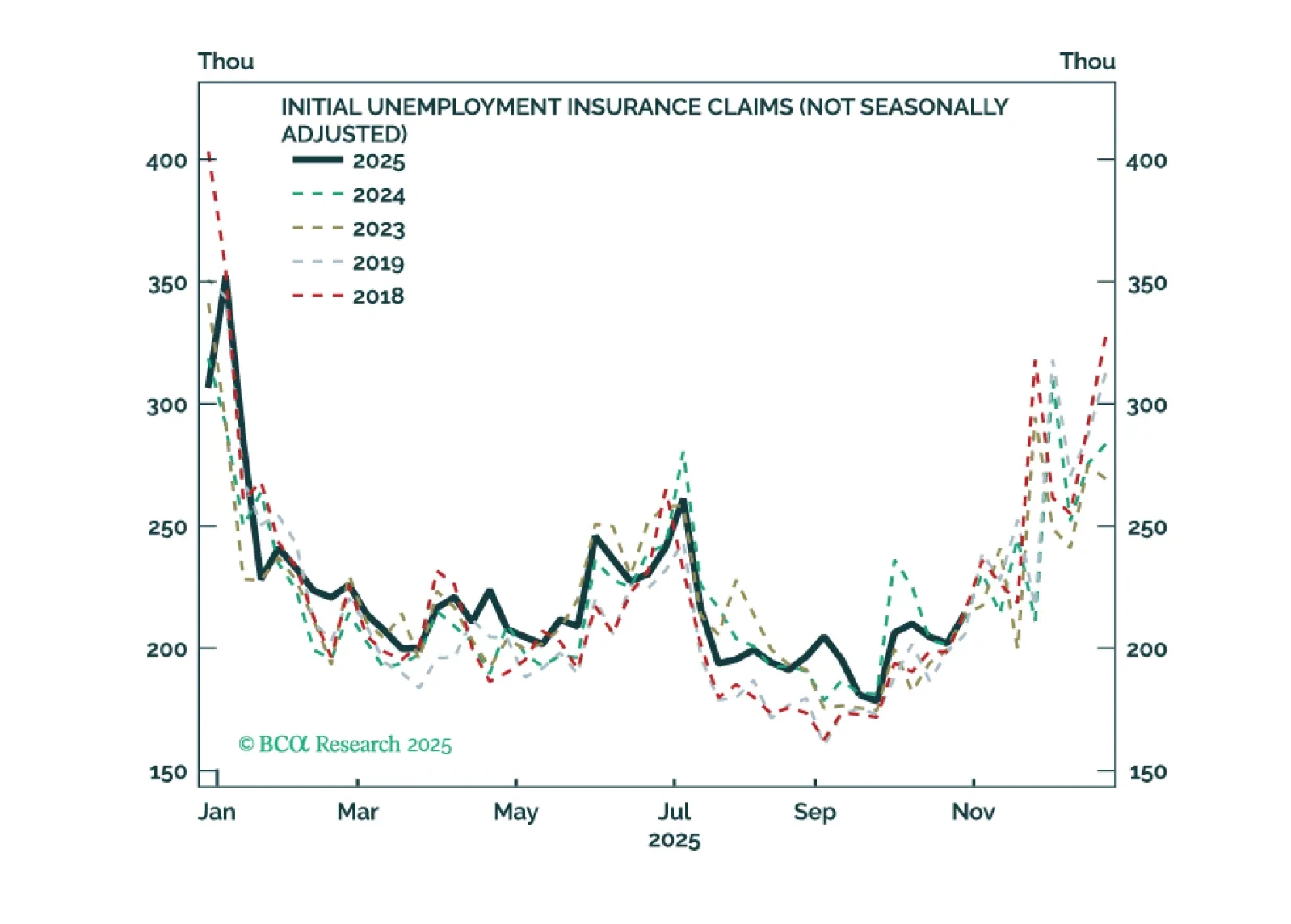

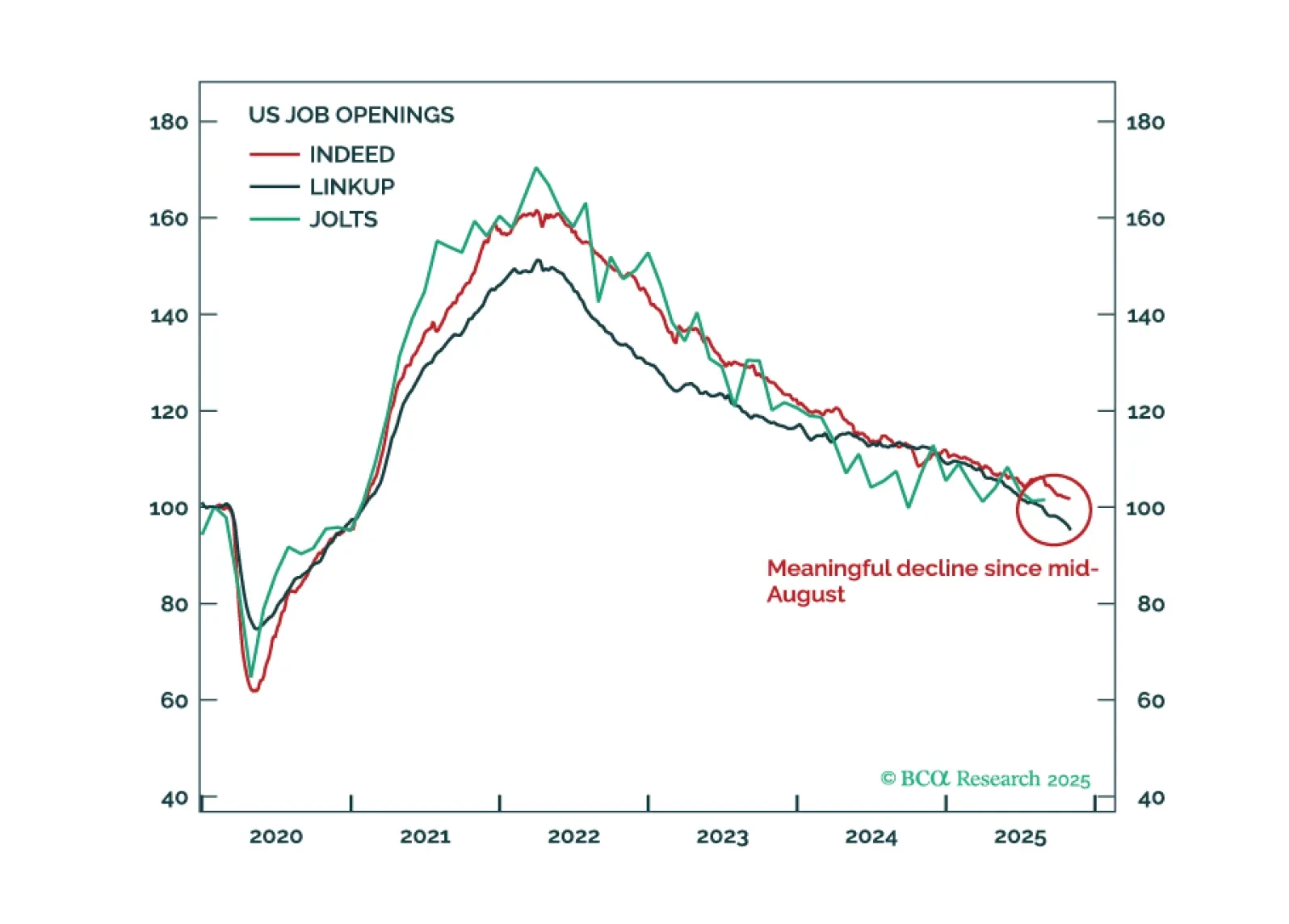

In the absence of official government data, investors are turning to alternative sources to gauge the direction of the US economy. Our analysis of this data suggests that the economy has continued to expand at a moderate pace over the past two months. If the Supreme Court were to strike down the tariffs, this would reduce the near-term odds of a recession while raising the odds of overheating.

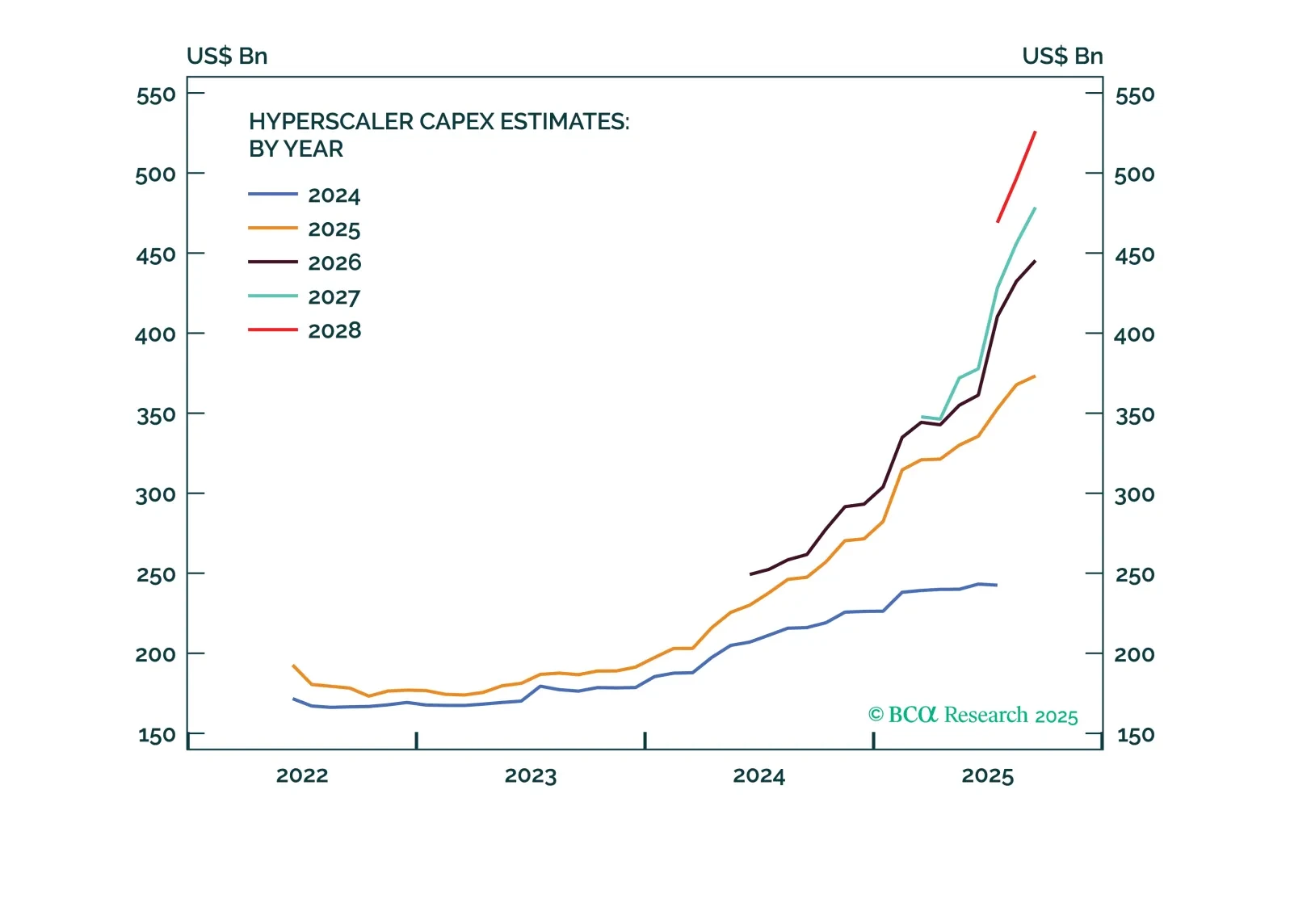

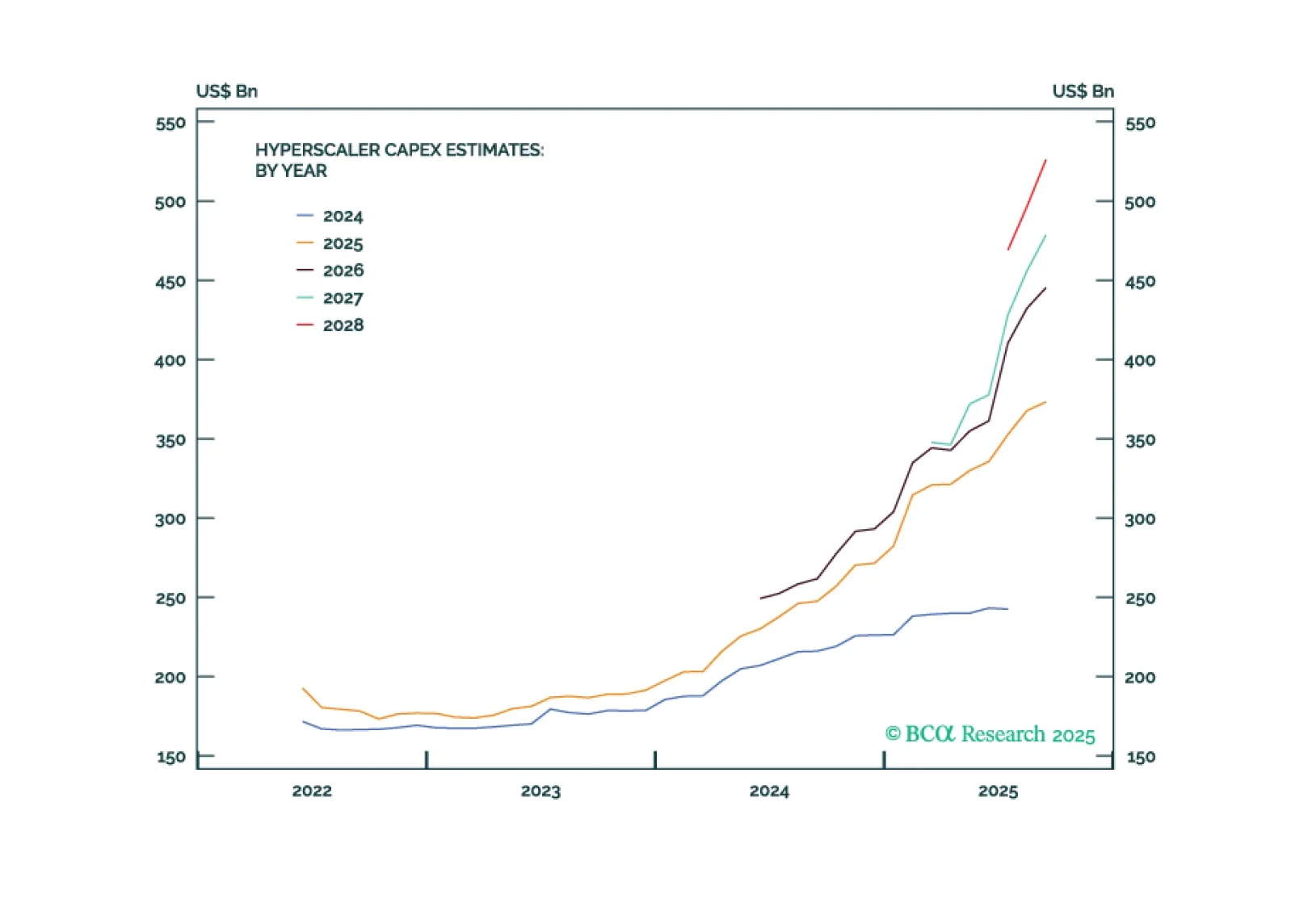

Fresh off a month of boning up on all things AI, we walk through a high-level Q&A discussing AI capex and how much the AI investing boom is really contributing to US growth.

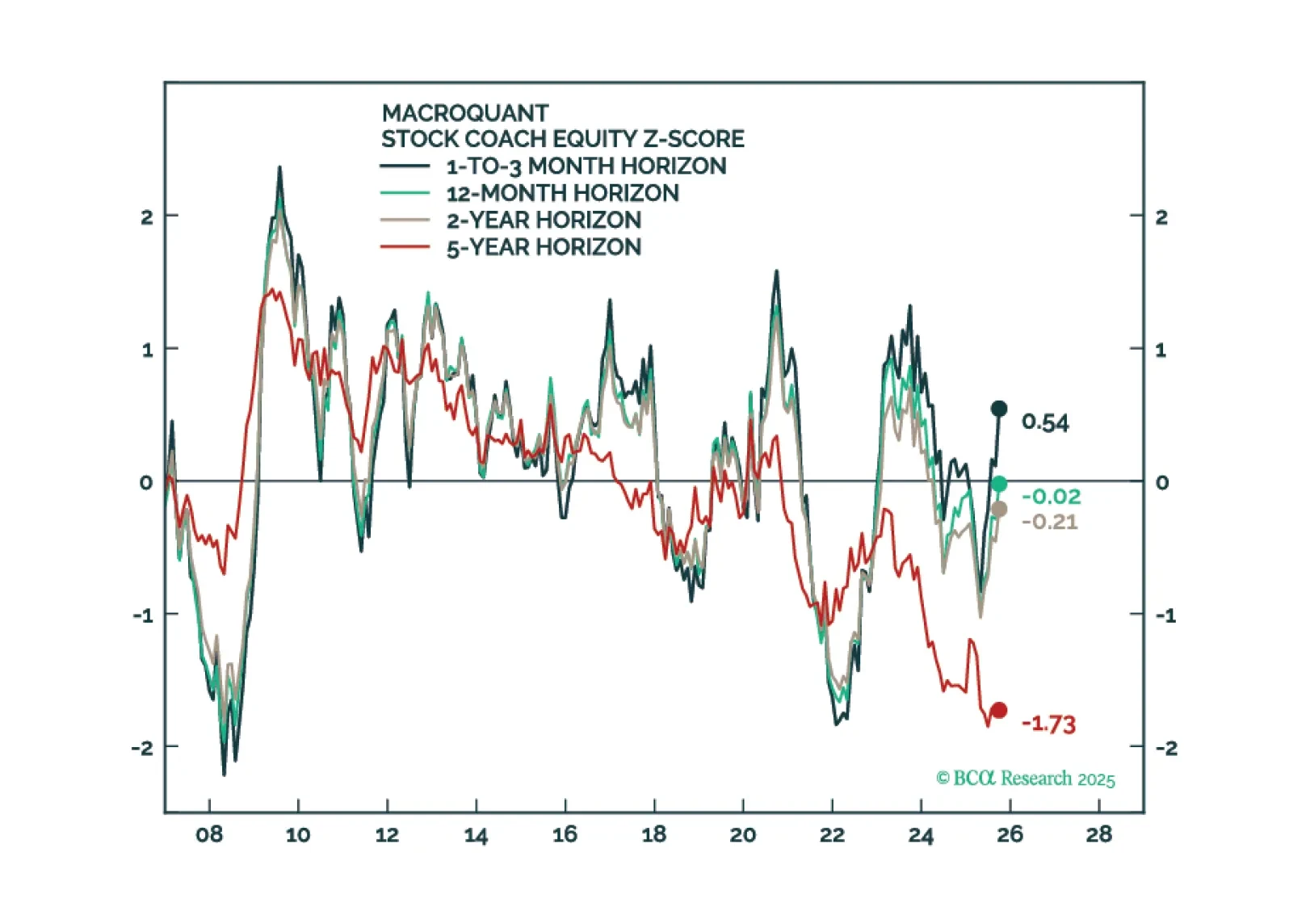

MacroQuant is tactically overweight equities, favors an above-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is bullish on gold and copper.

In Section II, Doug and Global Investment Strategy’s Miroslav Aradski consider the implications of the AI investment boom.

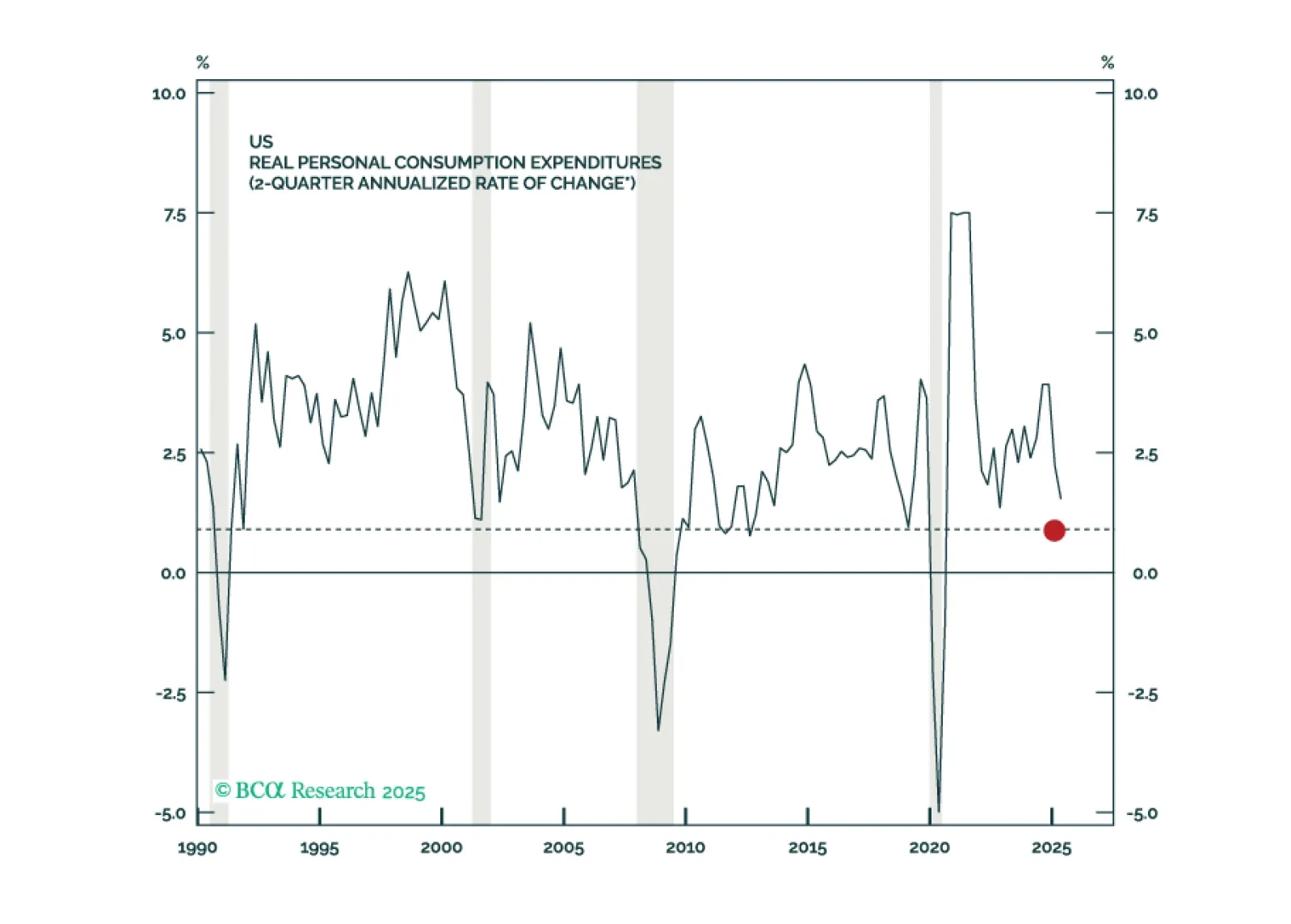

In Section I, Doug explains how the sharp upward revision to second-quarter consumption in the final GDP estimate has reduced our recession conviction and could lead us to abandon our recession call altogether. The situation is fluid, though, as typified by the striking weakness of stocks in consumer-facing and cyclically exposed subindustries. In Section II, Doug and Global Investment Strategy’s Miroslav Aradski consider the implications of the AI investment boom.

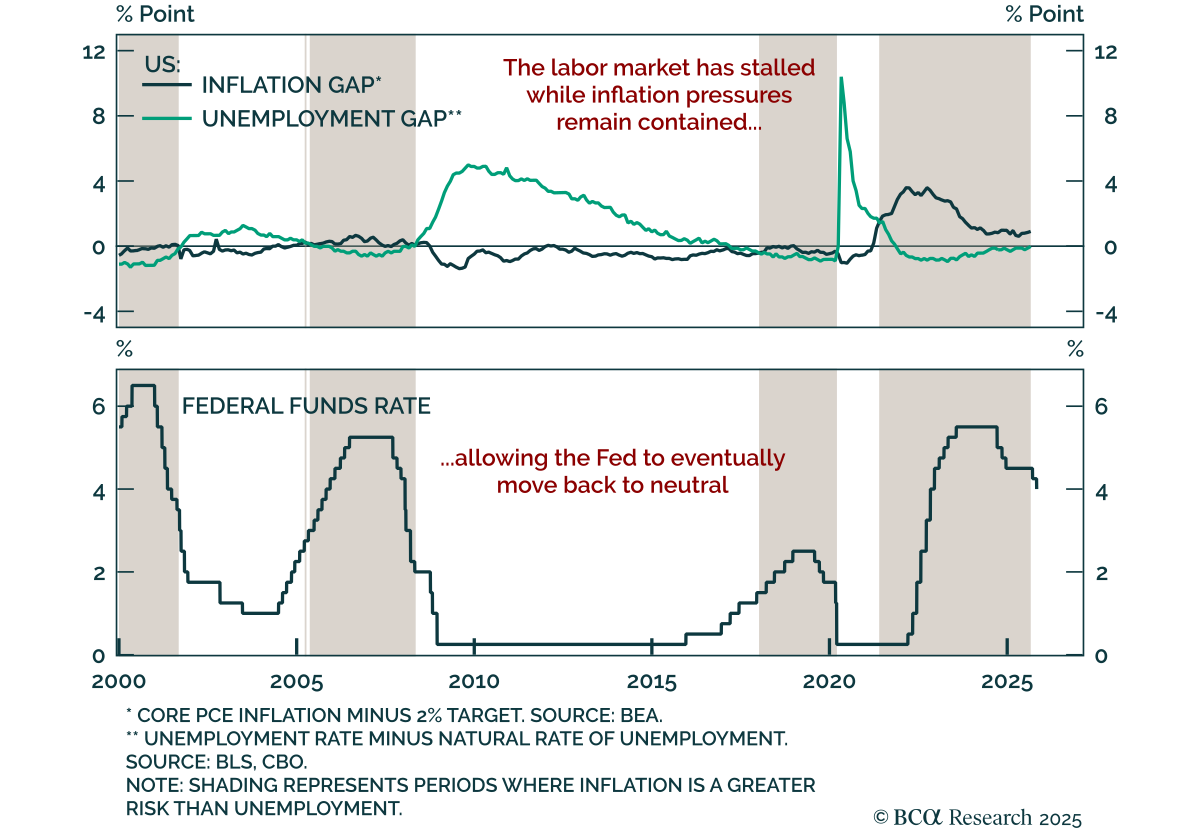

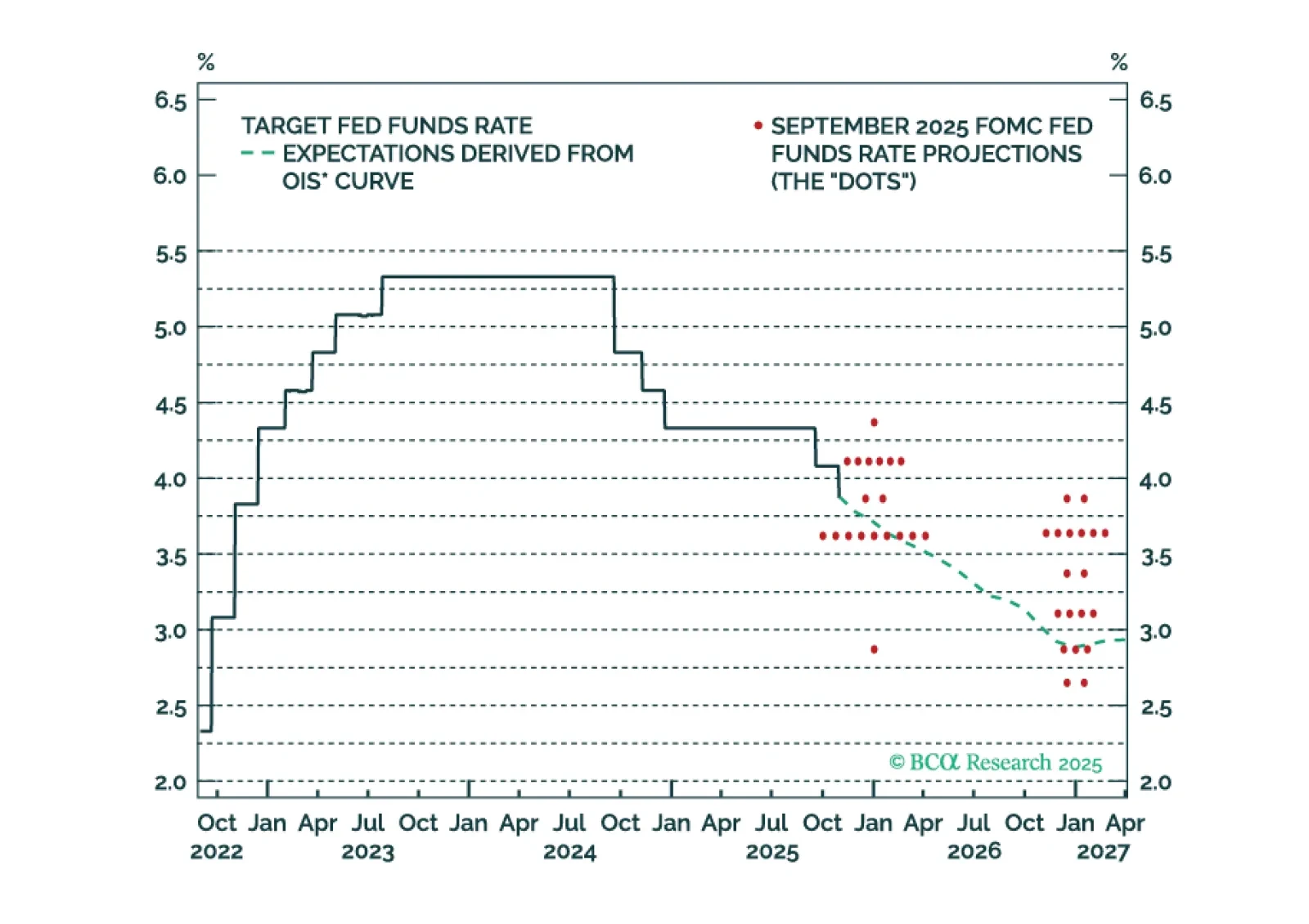

The Fed cut rates today, but a follow-up rate cut in December is uncertain. It will depend, in large part, on who wins a debate about the neutral rate of interest.