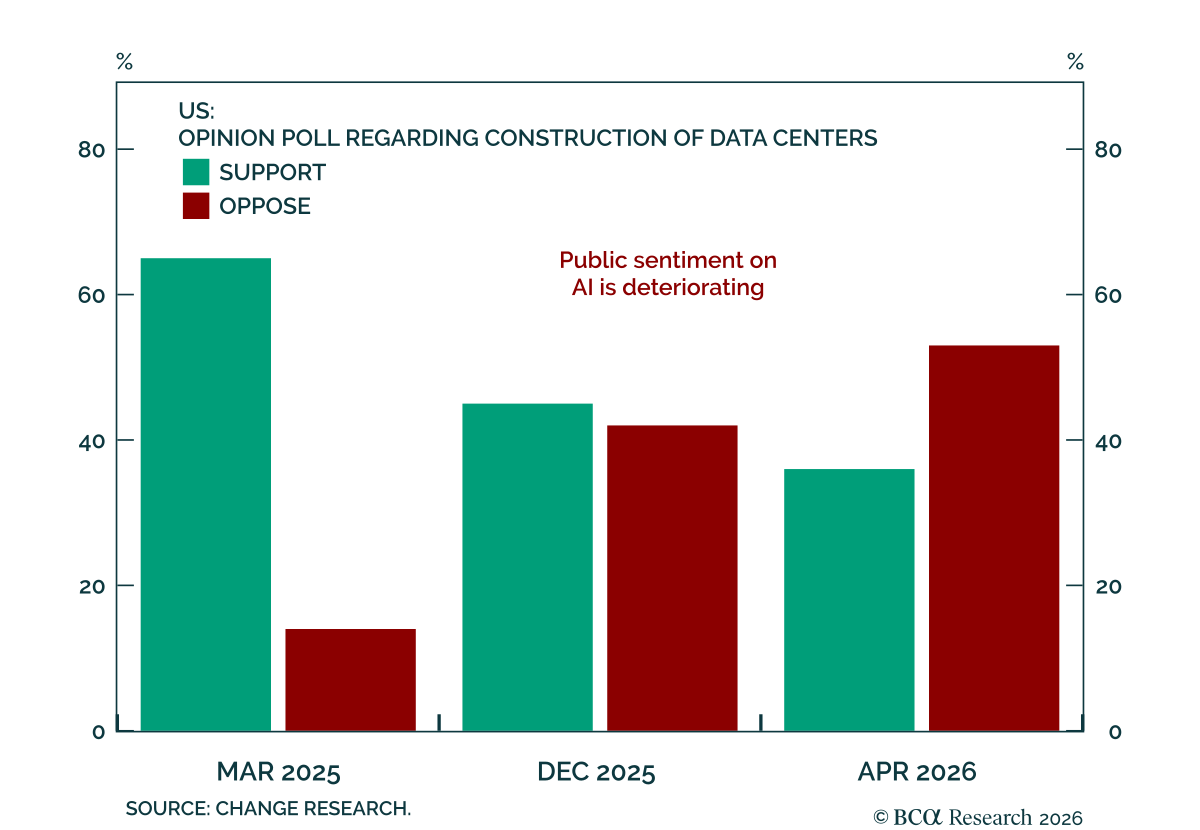

AI

The Goldilocks environment for US profit margins should start to sour next year. Contrary to conventional wisdom, AI could end up eroding margins for both producers and consumers of artificial intelligence.

We remain bullish on risk assets given that the Hormuz war has resolved itself and oil prices have declined by even more than we expected. In addition, the macro fundamentals are not flashing any red signs. That said, we remain skeptical that the AI revolution will continue without any hiccups. In fact, a price war may ensue once all the players realize they’re in the commodity – not tech – space.

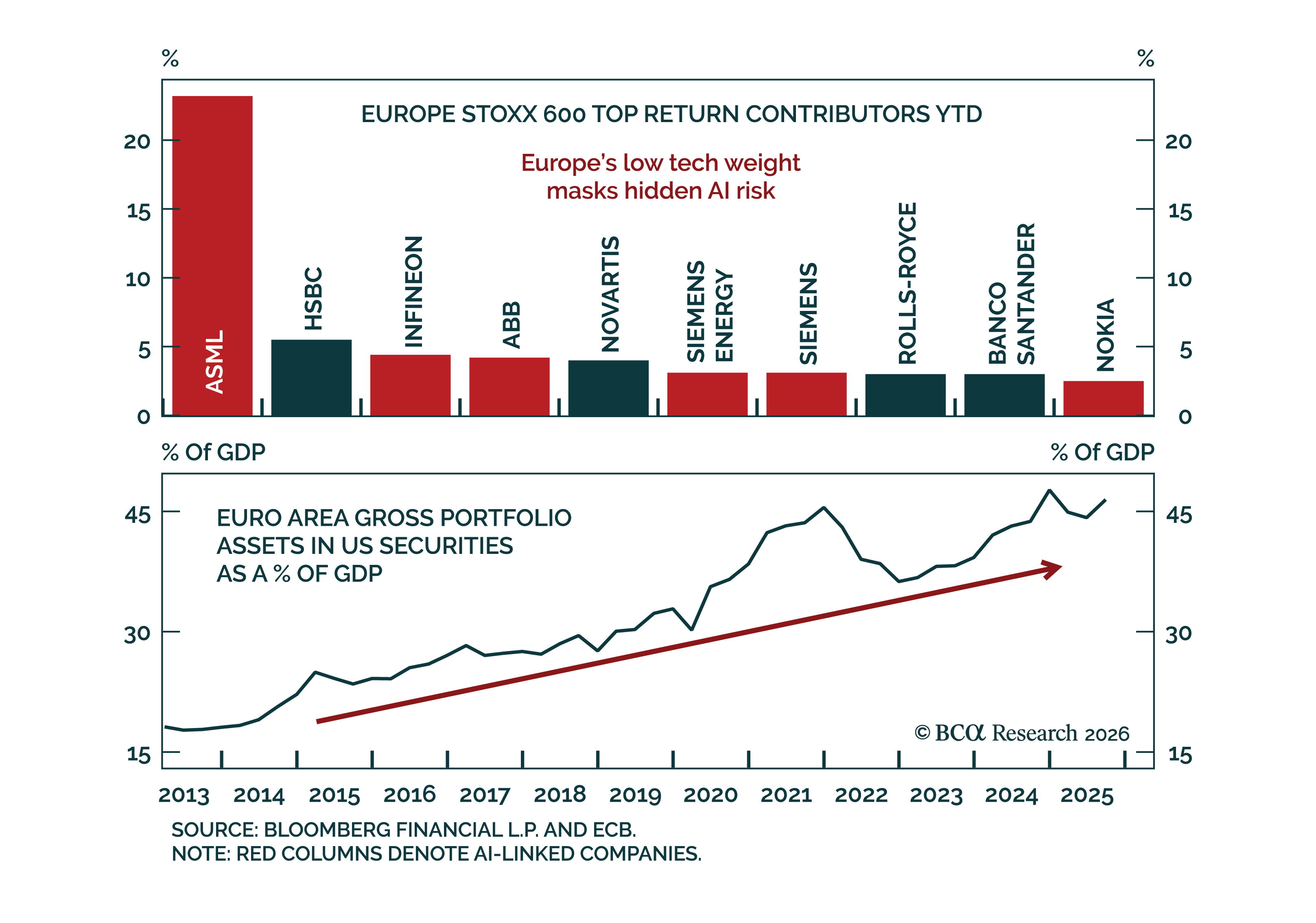

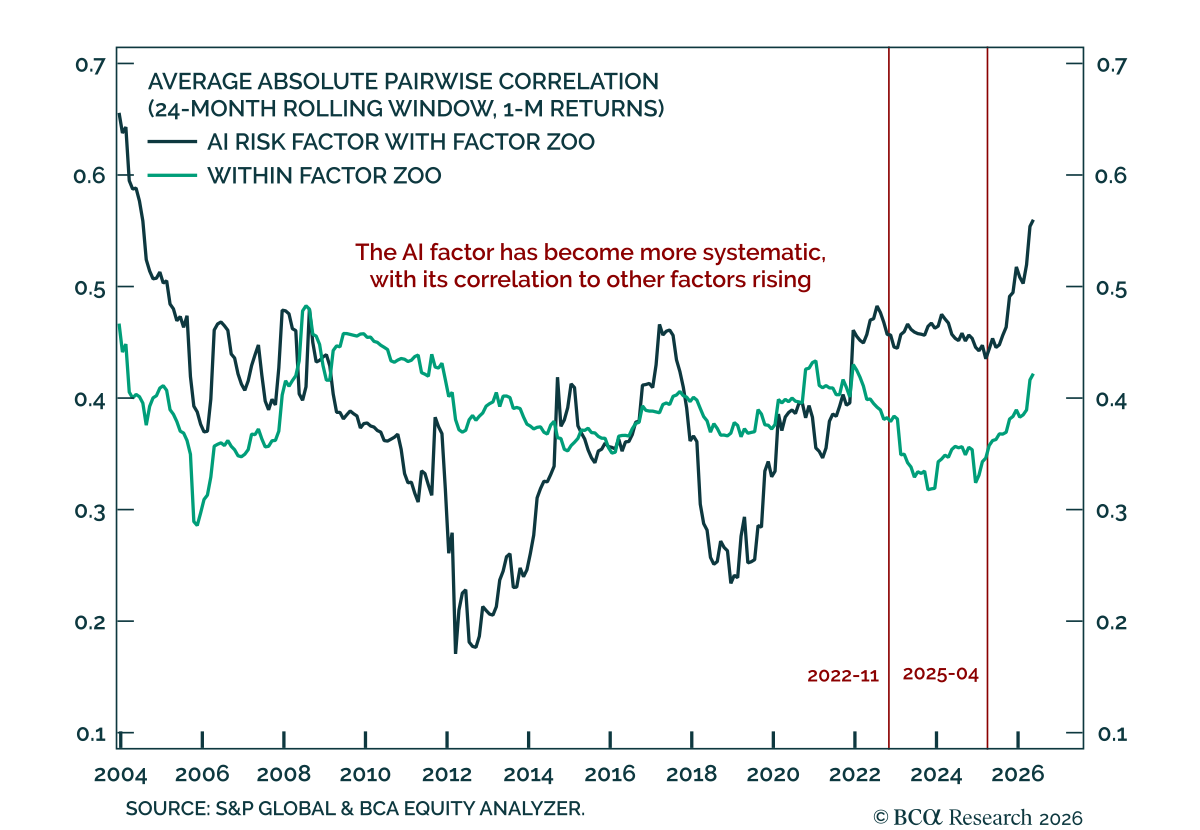

The S&P 500 has become increasingly concentrated. We know that. But the critical question is not how many stocks are driving the market; it is how many factors are driving stocks. We define an AI risk factor to test whether AI has become the dominant common exposure throughout much of the factor zoo.

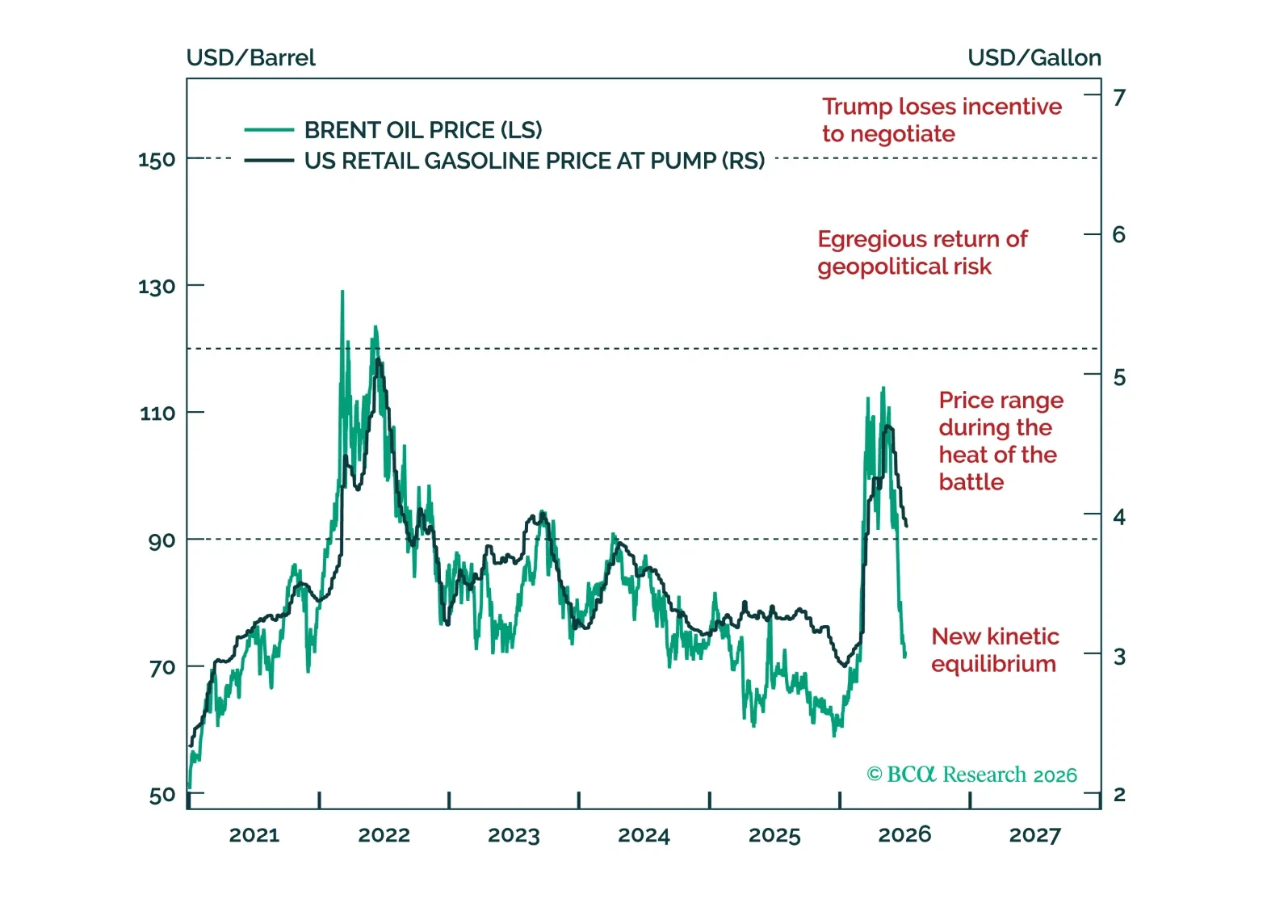

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

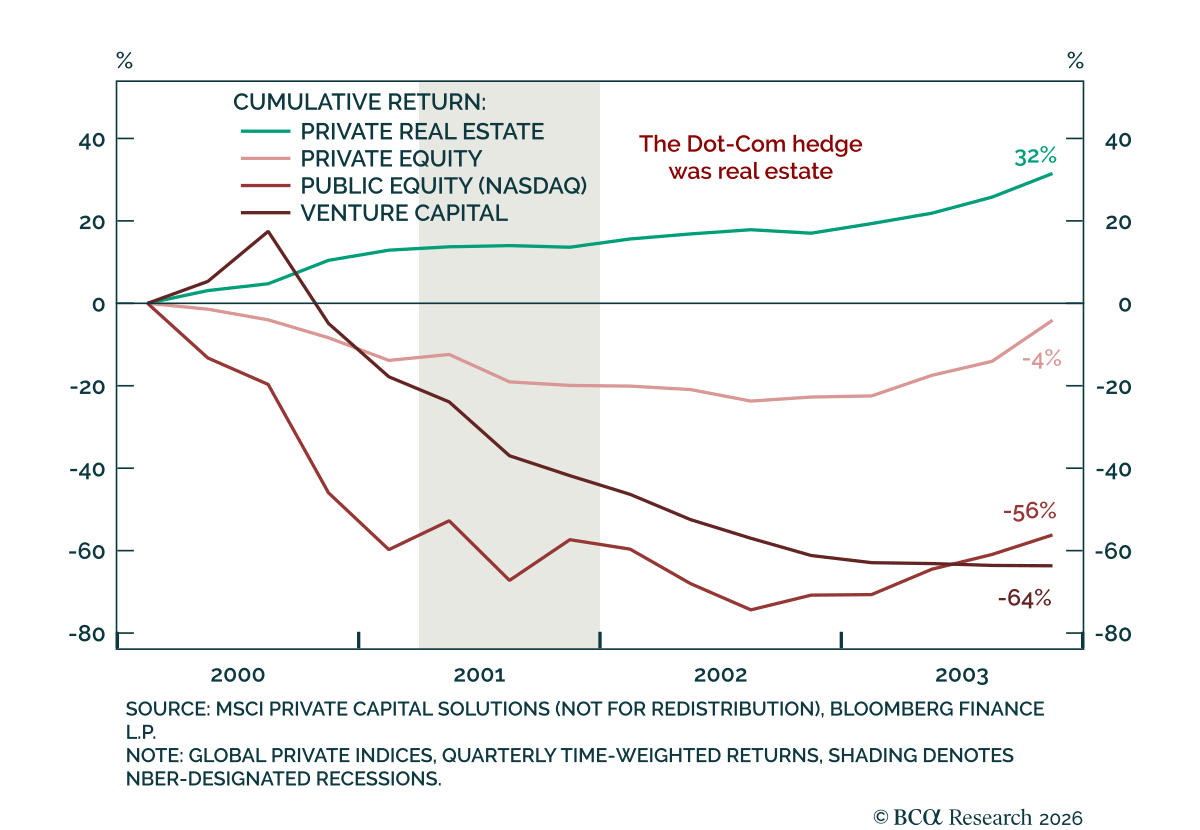

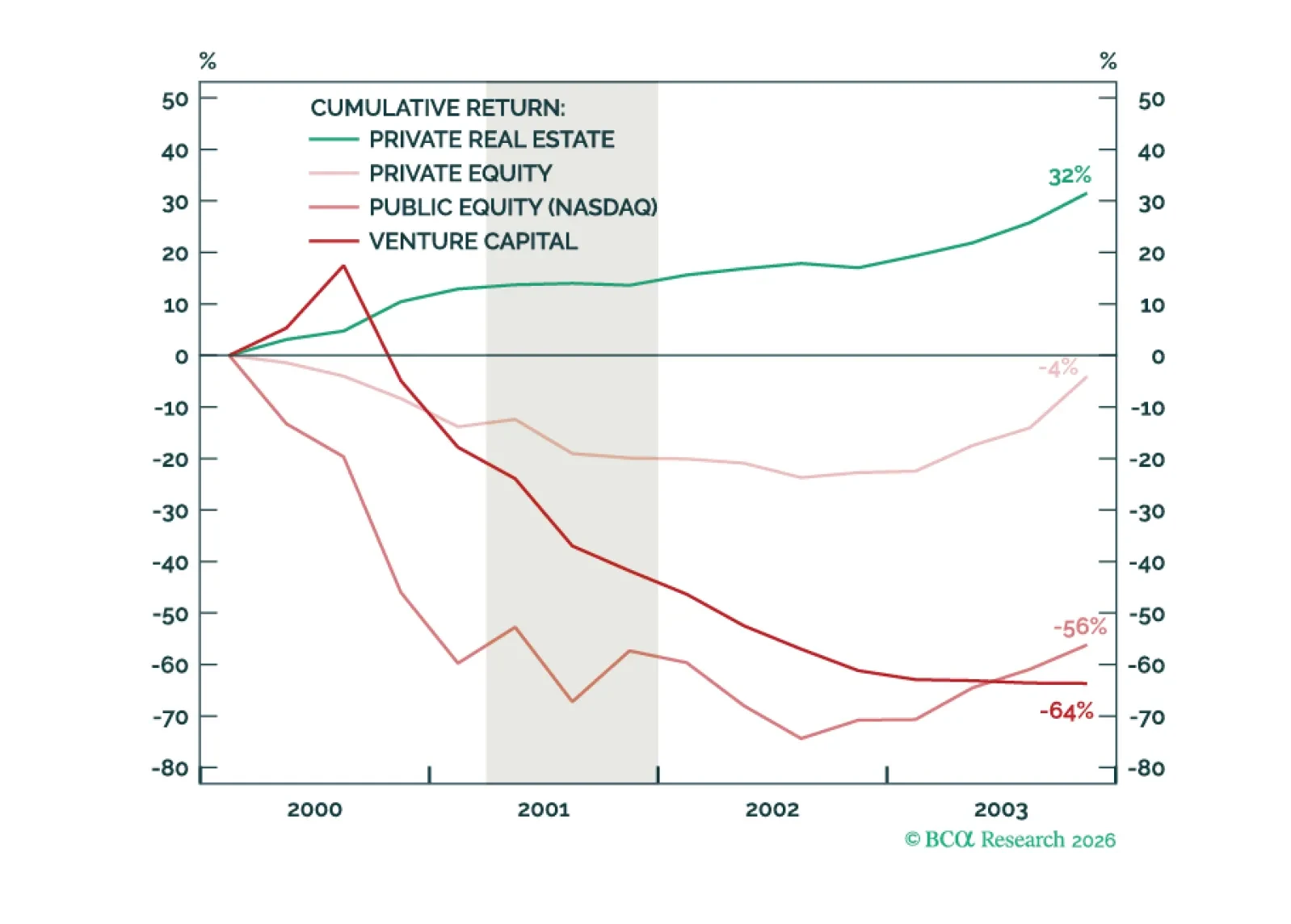

AI dominates markets, but concentration is risk. Real Estate is the diversifier. It outperformed during the Dot-Com bust and will do so again if the AI trade unwinds. Even Office, the sector arguably most exposed to AI disruption, will prove more resilient than bears expect.

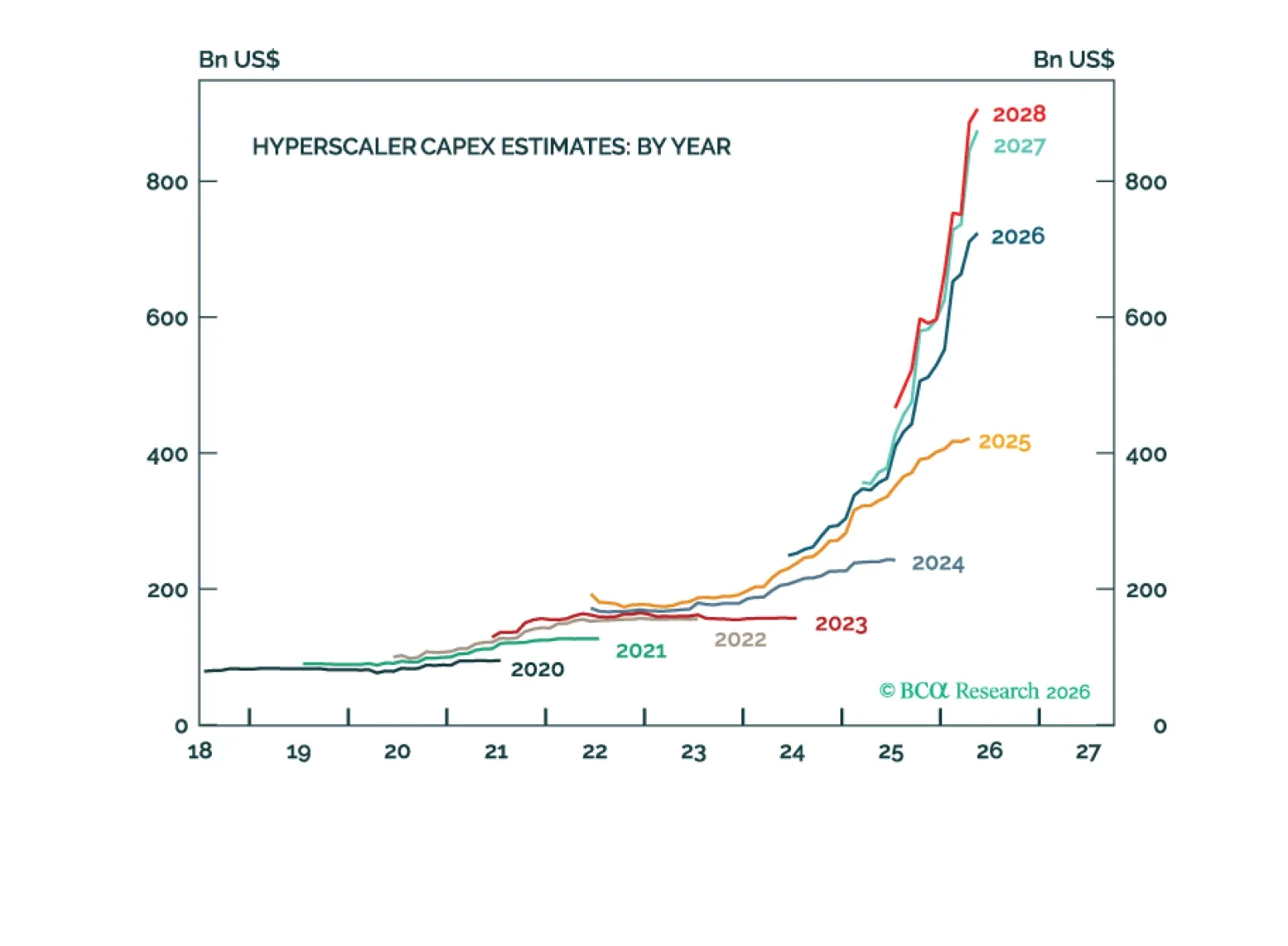

A surefire way to make money is to buy stocks in industries experiencing shortages. AI supply-chain bottlenecks will persist for the next few years but markets will price in relief before then.