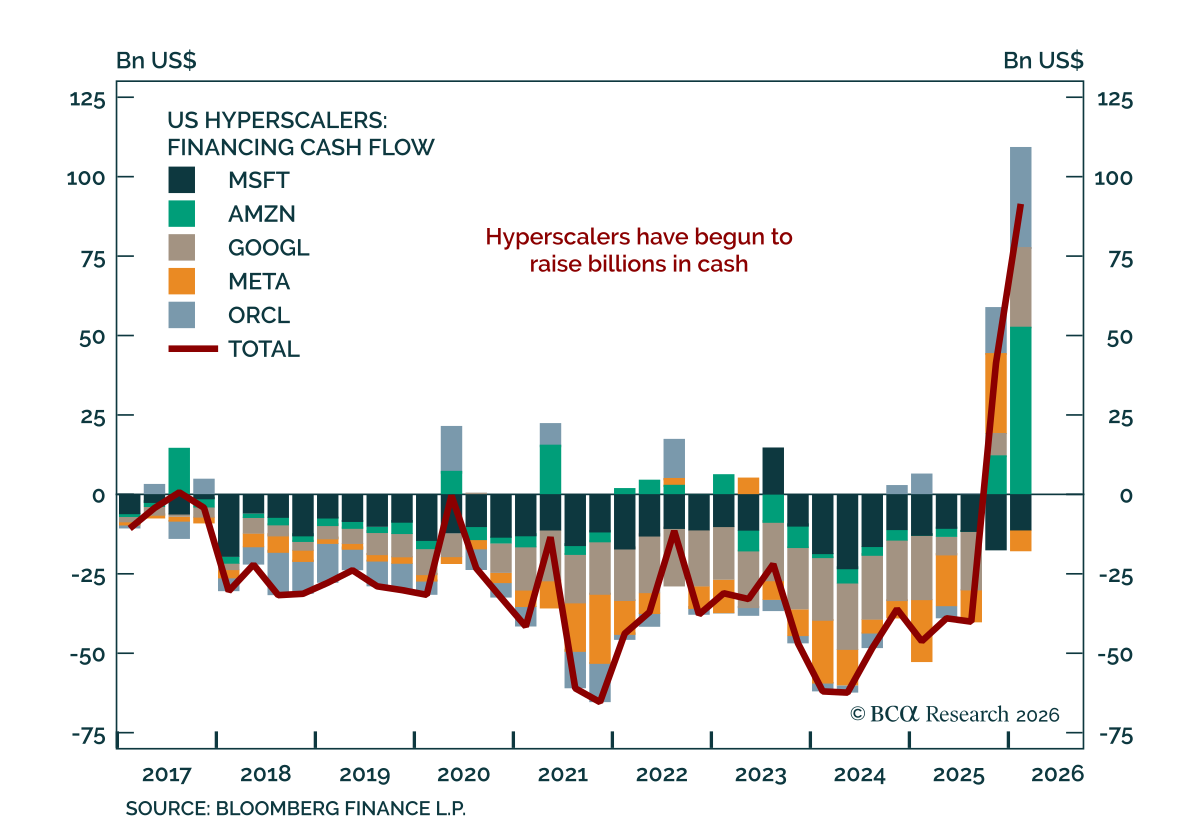

Capex

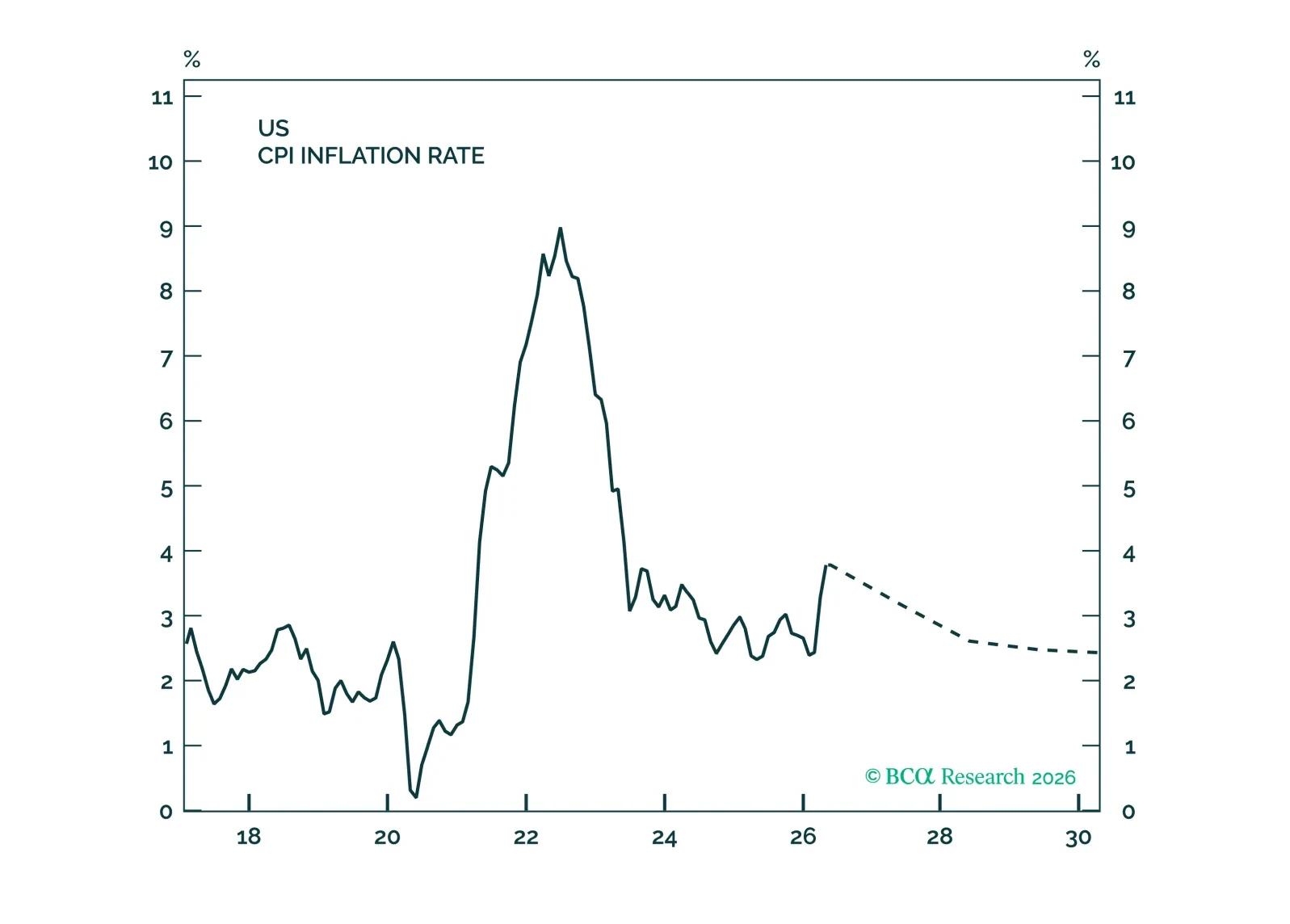

The AI boom will increase inflation in the near term and could also raise it over the long term. The Fed’s reluctance to hike rates is understandable, but it risks amplifying what may already be a brewing stock market bubble.

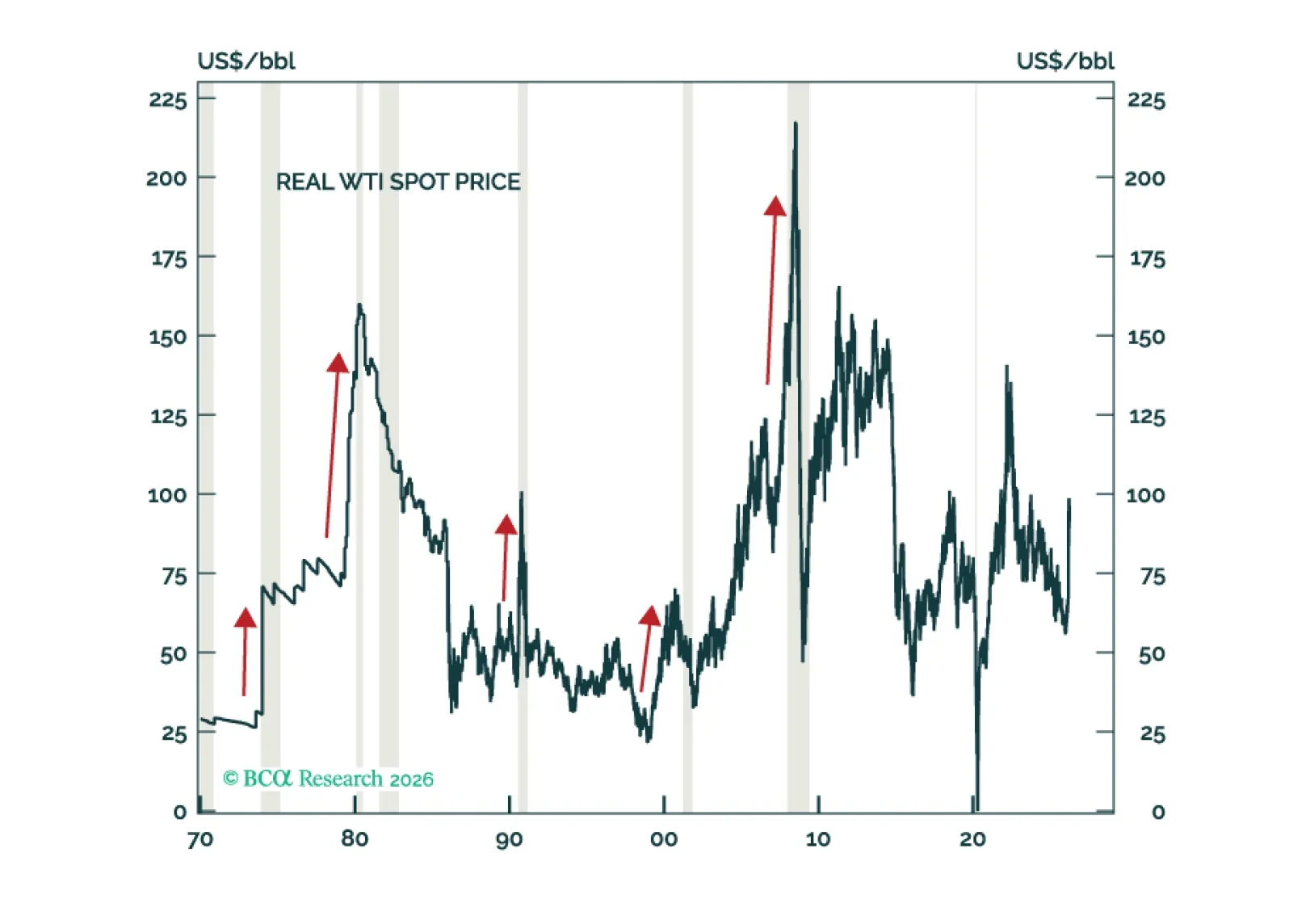

The global economy has weathered the oil shock reasonably well so far. However, the risk of a recession will increase meaningfully if the Strait of Hormuz remains closed into June.

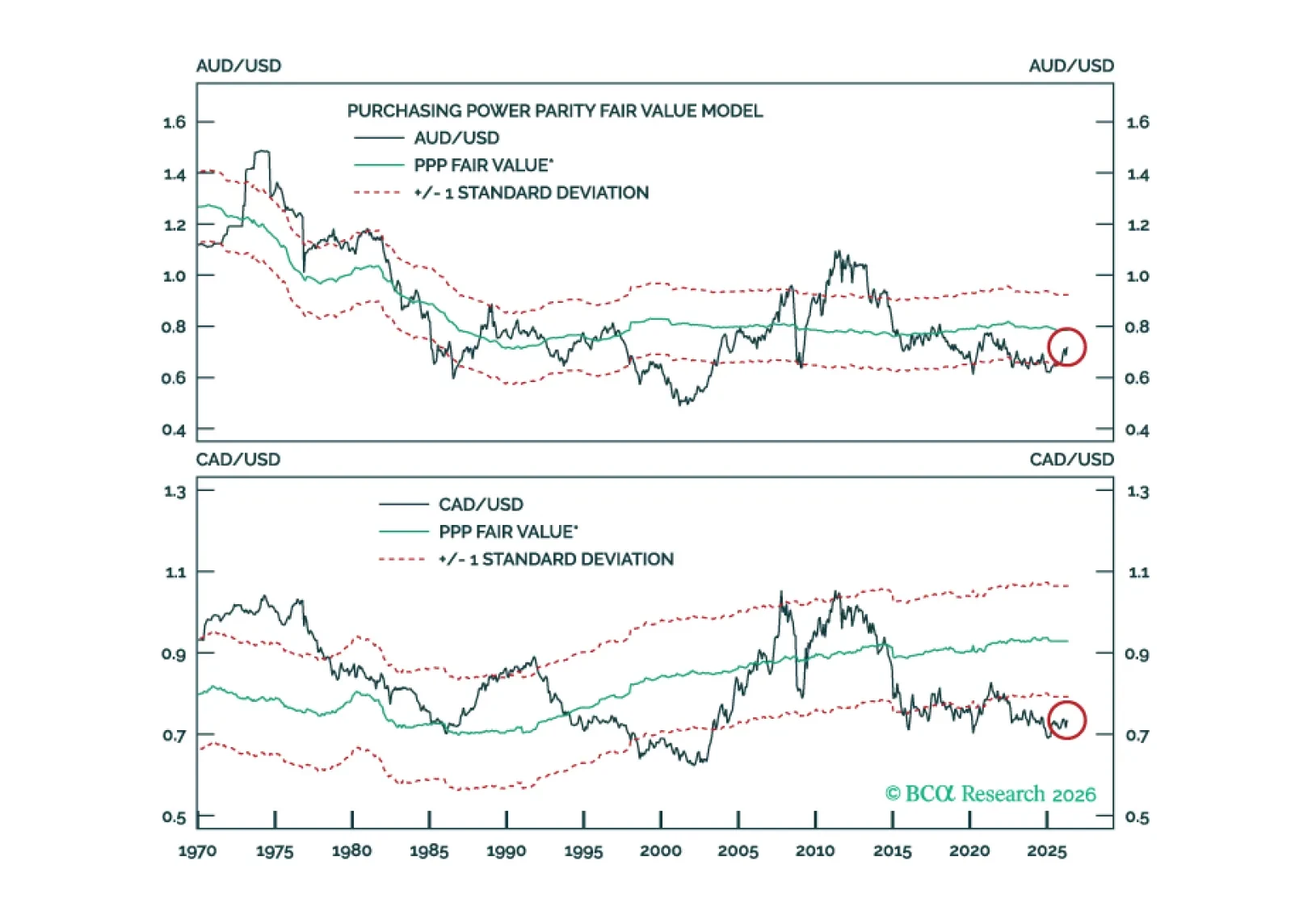

In Section I, Doug compares projected S&P 500 earnings and current capex to past cycles at the same stage of their expansions while also exploring the K-shaped bifurcation in business investment. In Section II, Mathieu argues that Australia and Canada are unloved, undervalued, and on the cusp of a structural re-rating. Long-term investors who wait for the catalysts to become obvious will miss the entry point.

This Special Report argues that Australia and Canada are unloved, undervalued, and on the cusp of a structural re-rating. Long-term investors who wait for the catalysts to become obvious will miss the entry point.

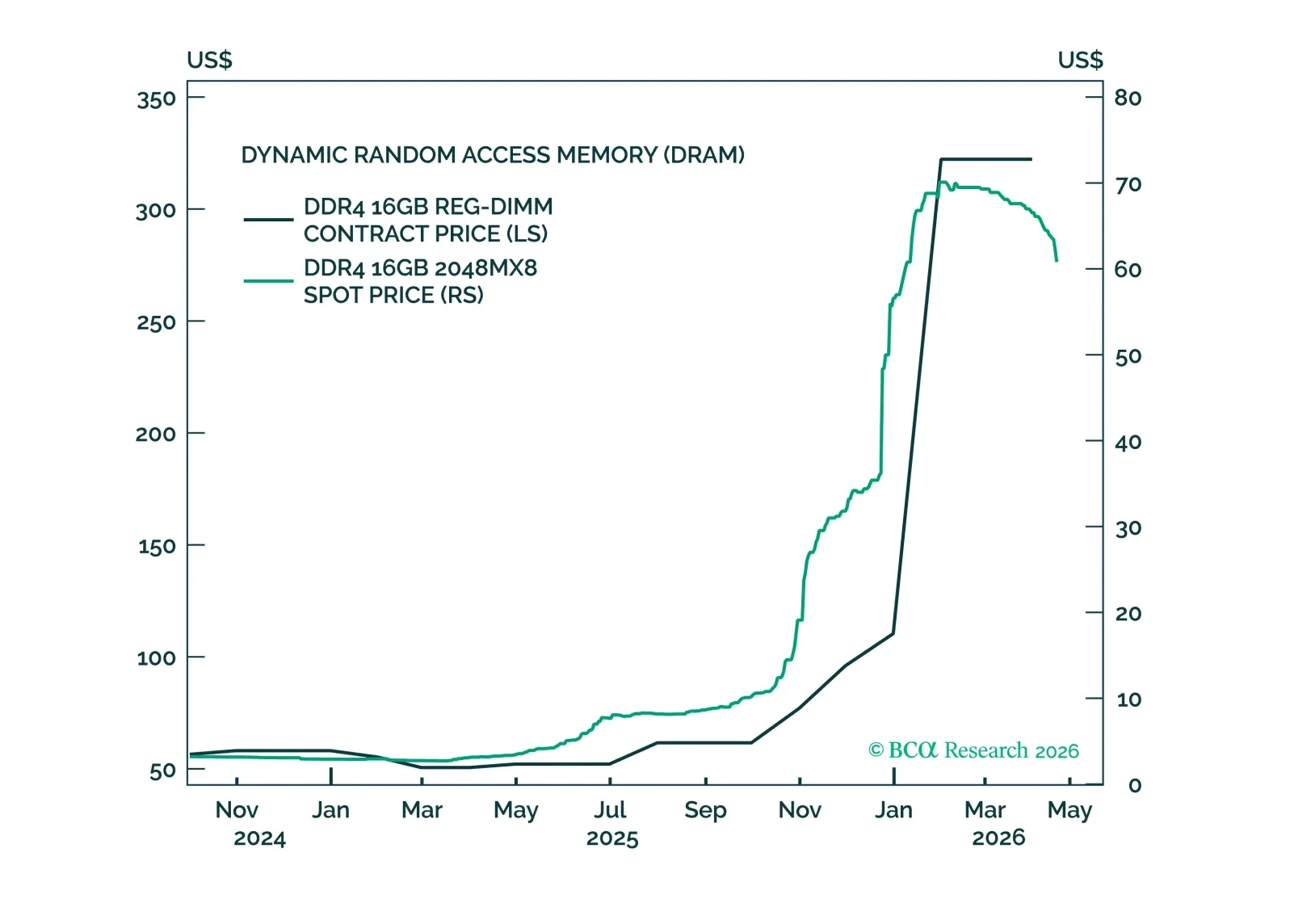

Most of the increase in S&P 500 earnings estimates this year has stemmed from shortages. The oil shortage, which has pushed up estimates for energy companies, will fade once the military conflict is resolved. However, the shortage of semiconductors and other AI paraphernalia could persist for a while longer. As such, we are moving our recommended 12-month equity allocation from a slight underweight to neutral. We are already neutral on a 3-month horizon.

The current macro environment is a toxic brew of many of the same vulnerabilities that haunted the global economy in the lead-up to past recessions: Rising oil prices, an unsustainable tech capex boom, elevated equity valuations, excessively high homes prices, and brewing stresses in private credit and other parts of the financial system. While global equities look increasingly oversold in the very near term, they will still finish the year below current levels.

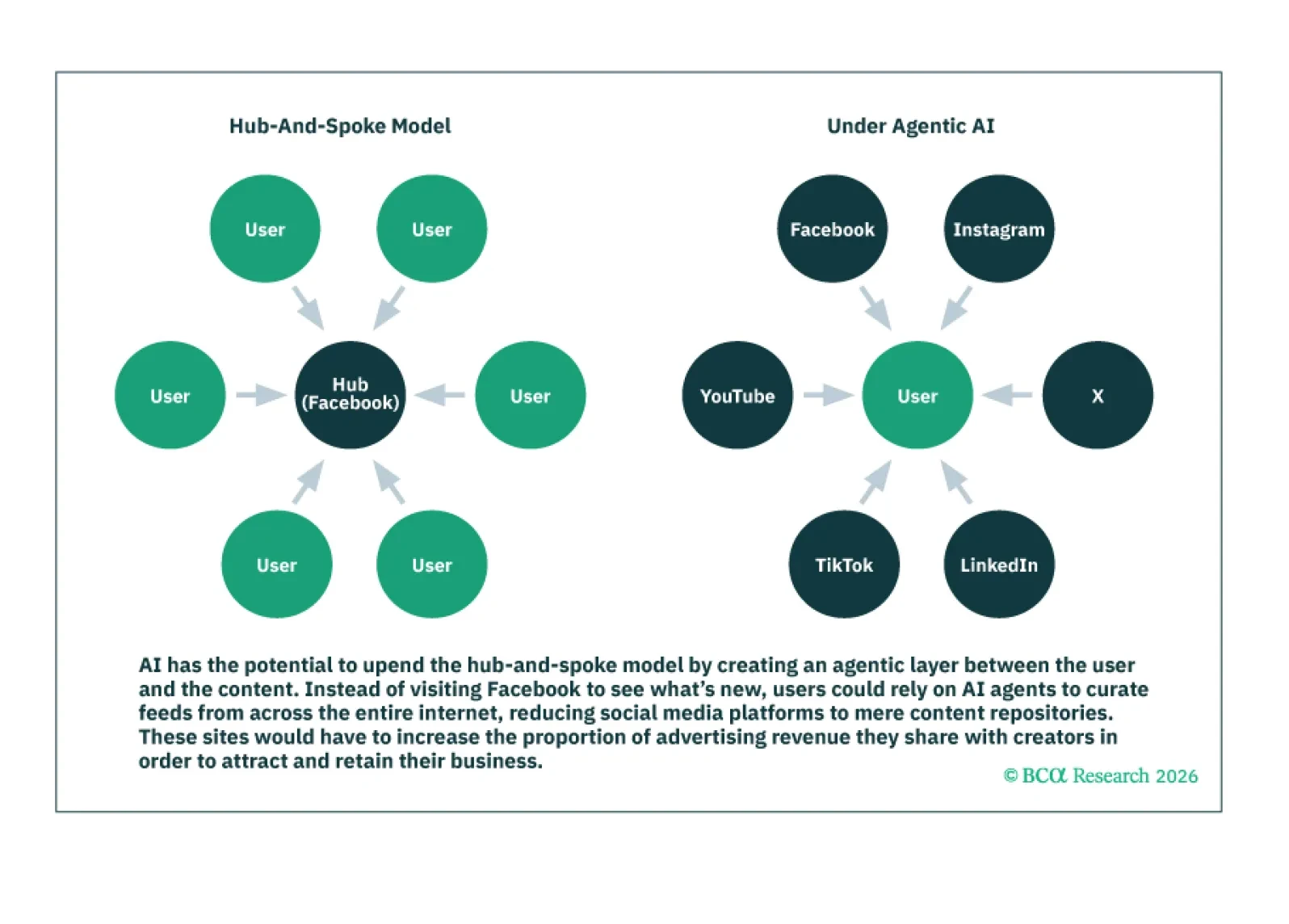

Tech companies have historically generated profits from three main sources: 1) economies of scale; 2) network effects; and 3) proprietary technologies. AI threatens to undercut all three sources.

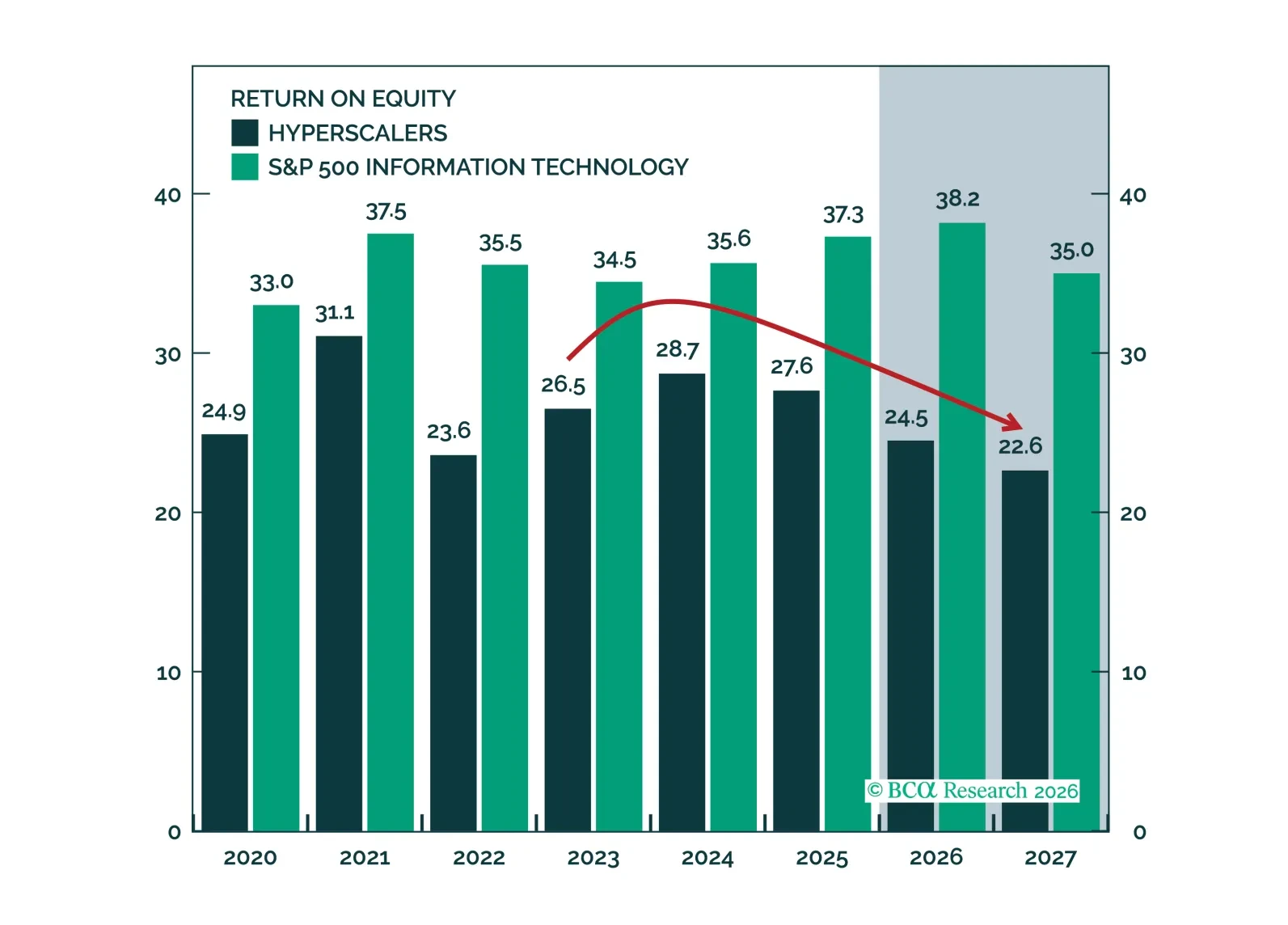

The capex debate is better framed not as boom versus bubble, but as around capacity, leverage, and cash conversion. ROEs have compressed, but revenue growth and margin expansion offer a credible path back. Spenders likely have time to make good on their investments, though the market’s leash may be shorter than anticipated.

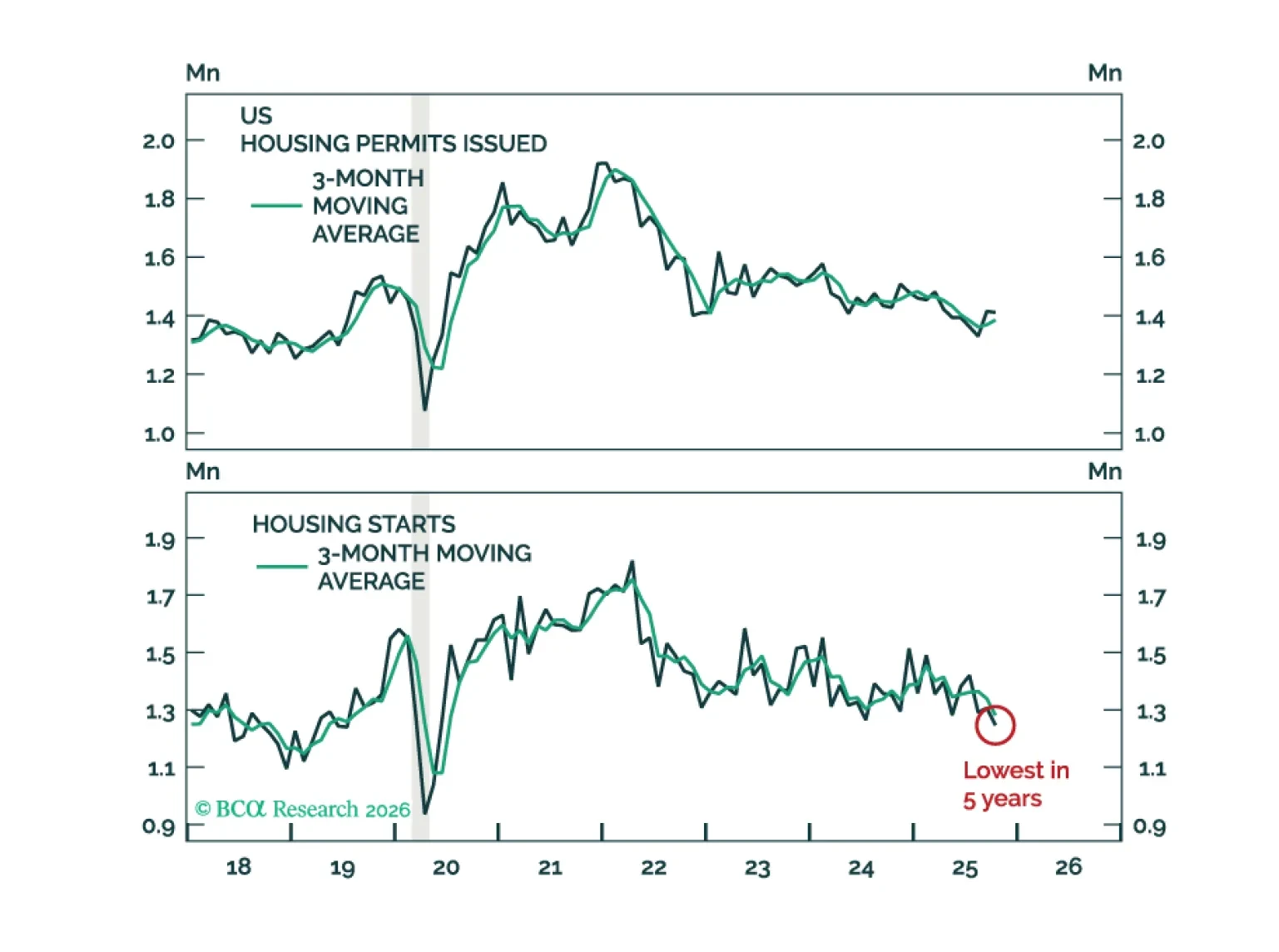

The US residential real estate market remains soft. While the decline in mortgage rates is a positive, it is too early to bet on housing becoming the engine of growth for the US economy this year.