Australia

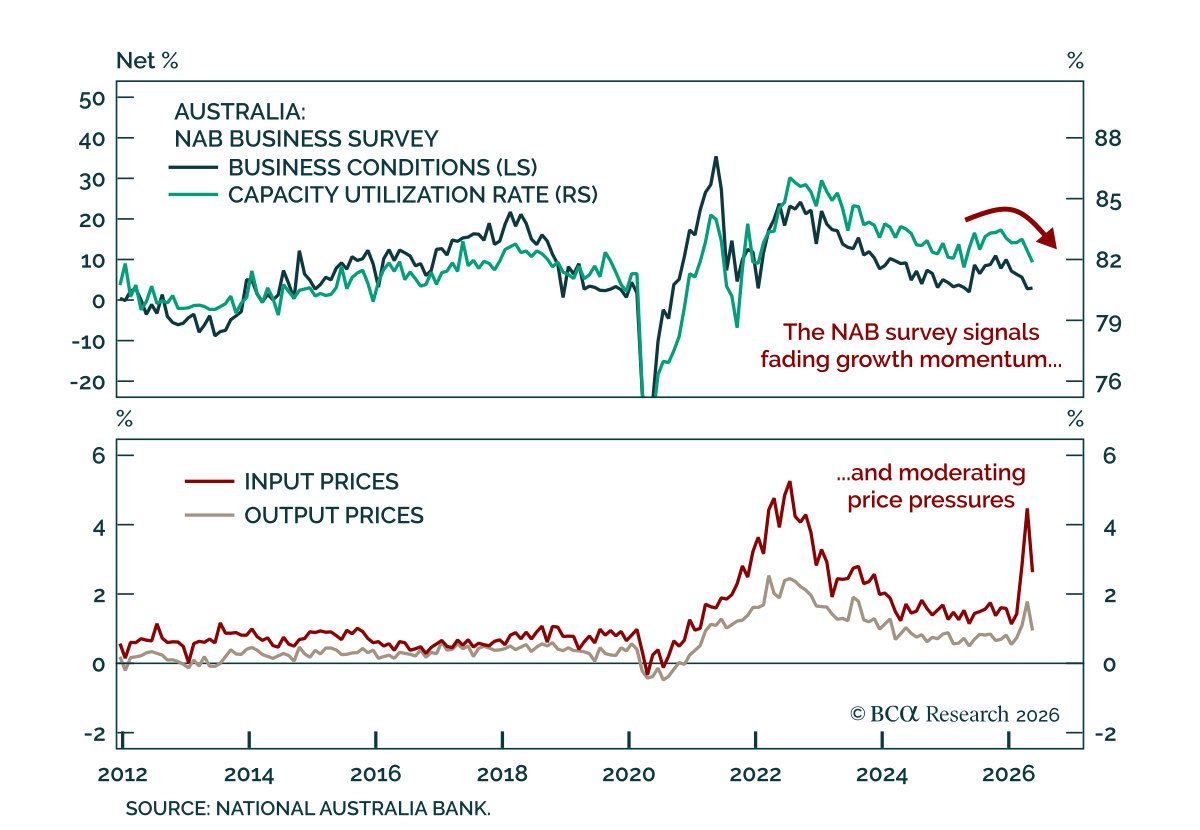

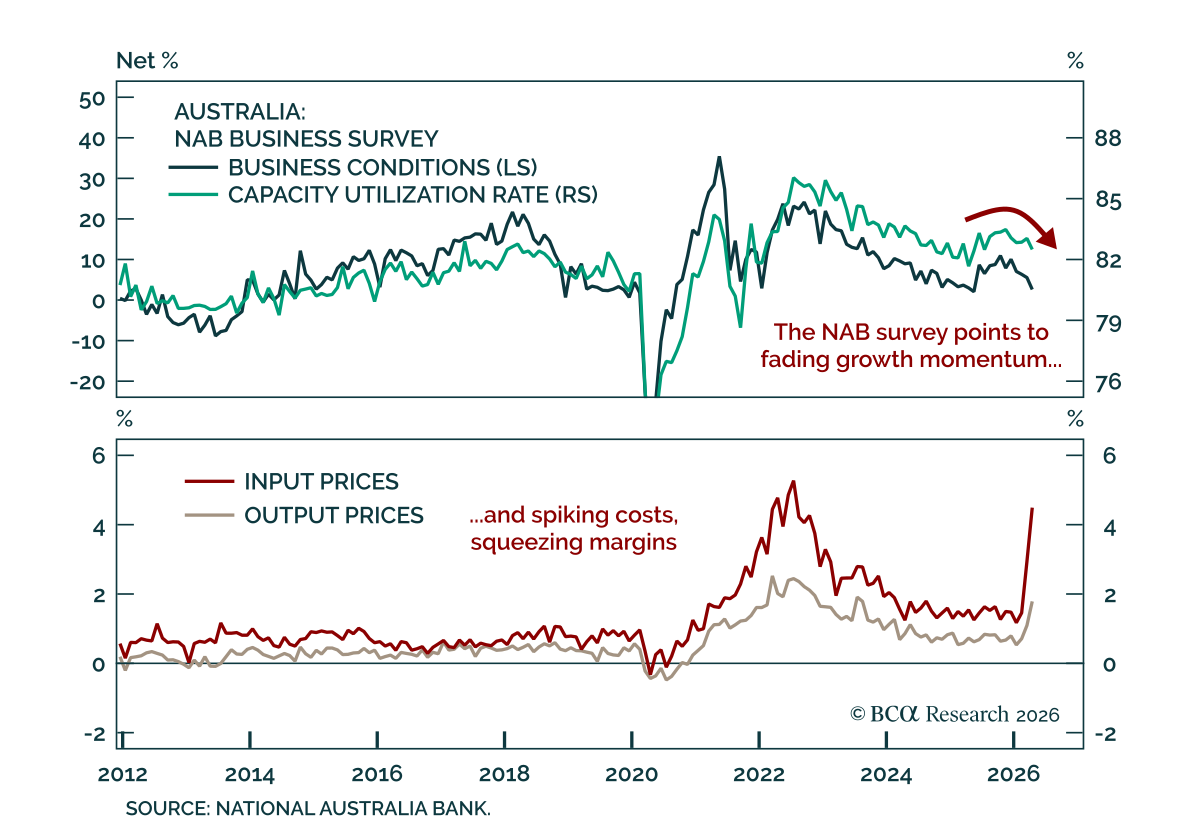

Australia's June NAB Business Survey points to a cooling economy, reinforcing the case for an extended RBA pause. Business conditions held at +3 for a third consecutive month, while business confidence, the more forward-looking measure, rebounded from -14 to…

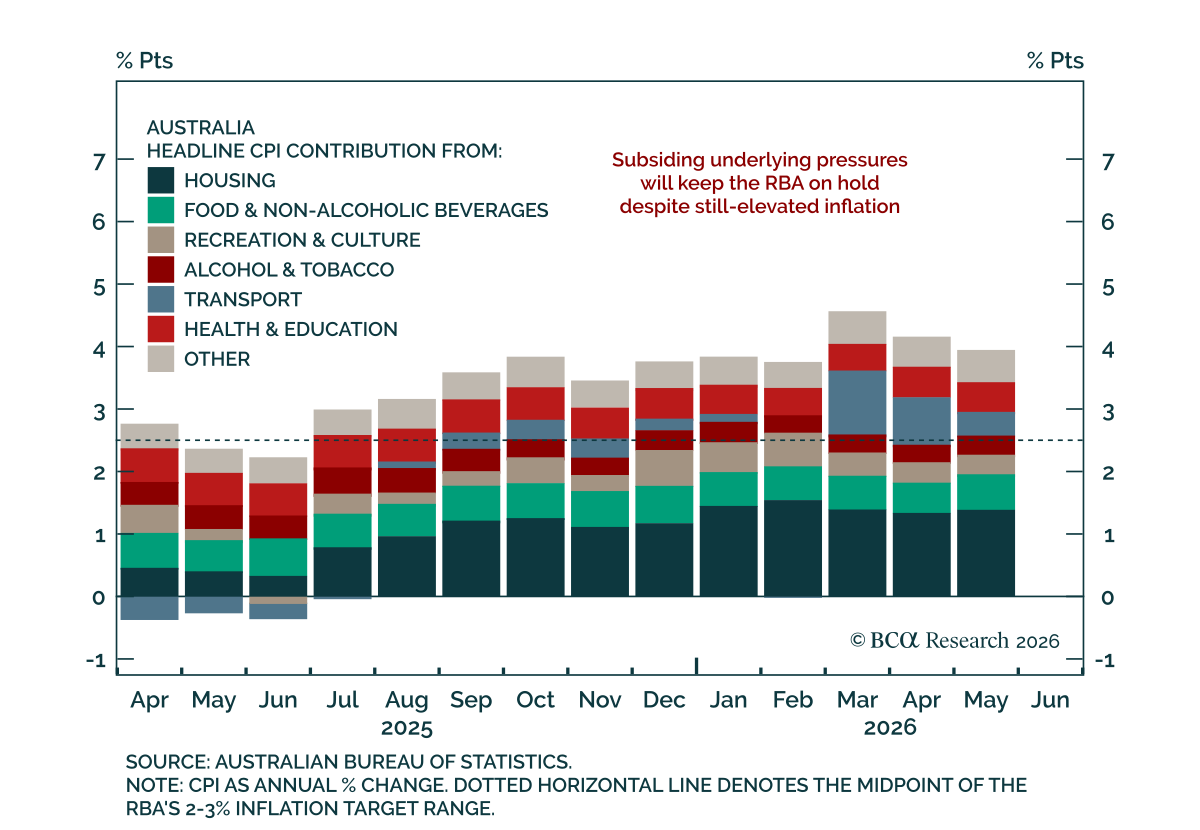

Australia's May data came in firmer than expected, but the RBA will stay on hold. Headline inflation eased to 4% y/y (-0.7% m/m) from 4.2% (0.4%), undershooting estimates. Lower energy prices cooled the print. The trimmed mean, however, climbed to 3.6% y/y…

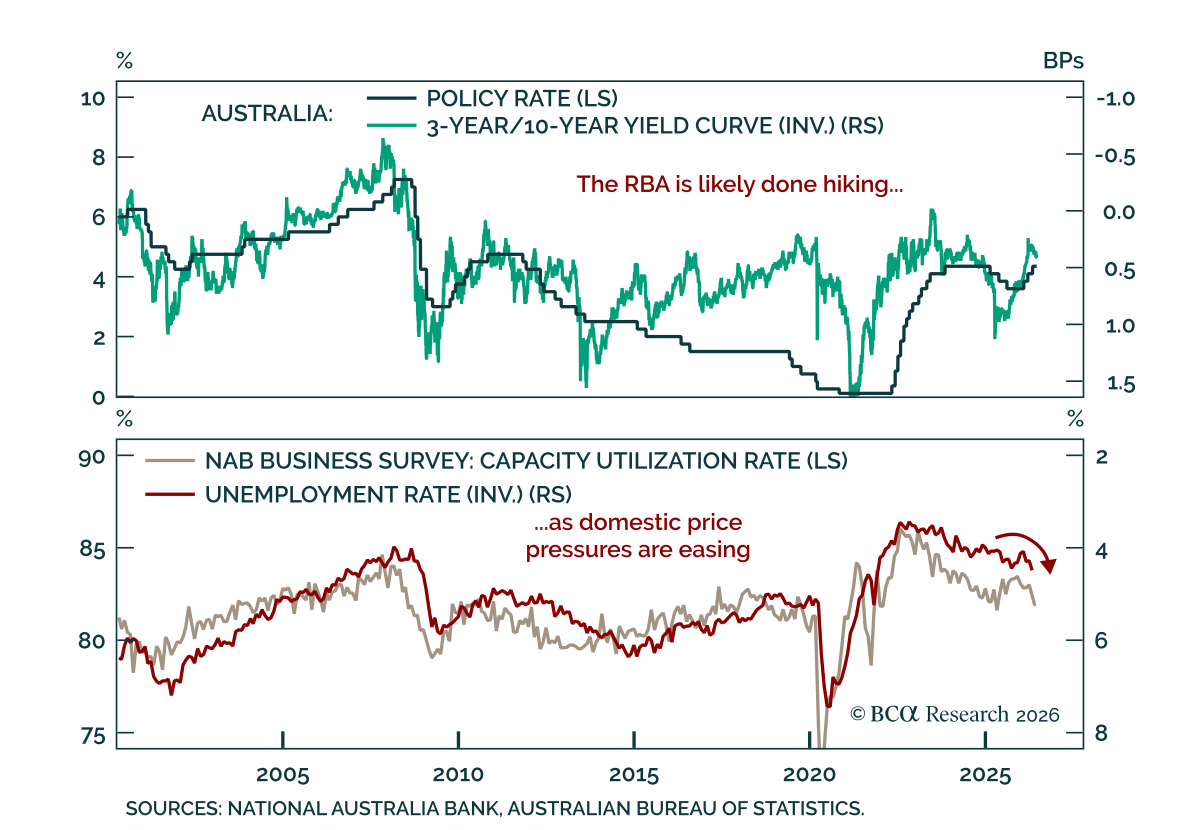

The RBA held rates, and further tightening looks unlikely despite the hawkish rhetoric. The policy rate was left unchanged, as expected, after three consecutive hikes totaling 75 bps. The decision was unanimous. Still, Governor Bullock declined to rule out…

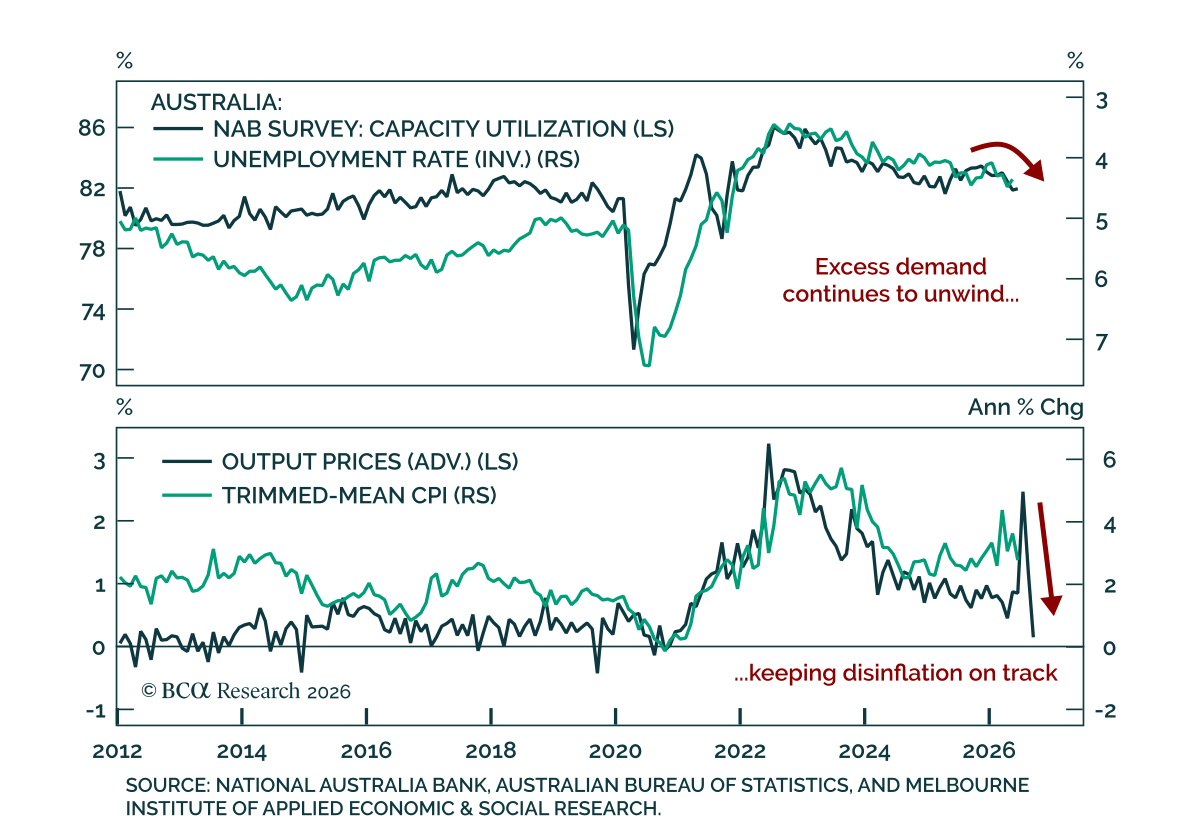

Australia's May NAB survey pointed to softer growth, with moderating price pressures reinforcing the case that the RBA's tightening cycle is over. Business conditions held steady at +3, firmly below the long-term average, after falling every month this year.…

In this screener report, we explore opportunities in: US copper beneficiaries; Australian Materials, Energy, and Industrial stocks; and US reinvestment-led Tech stocks.

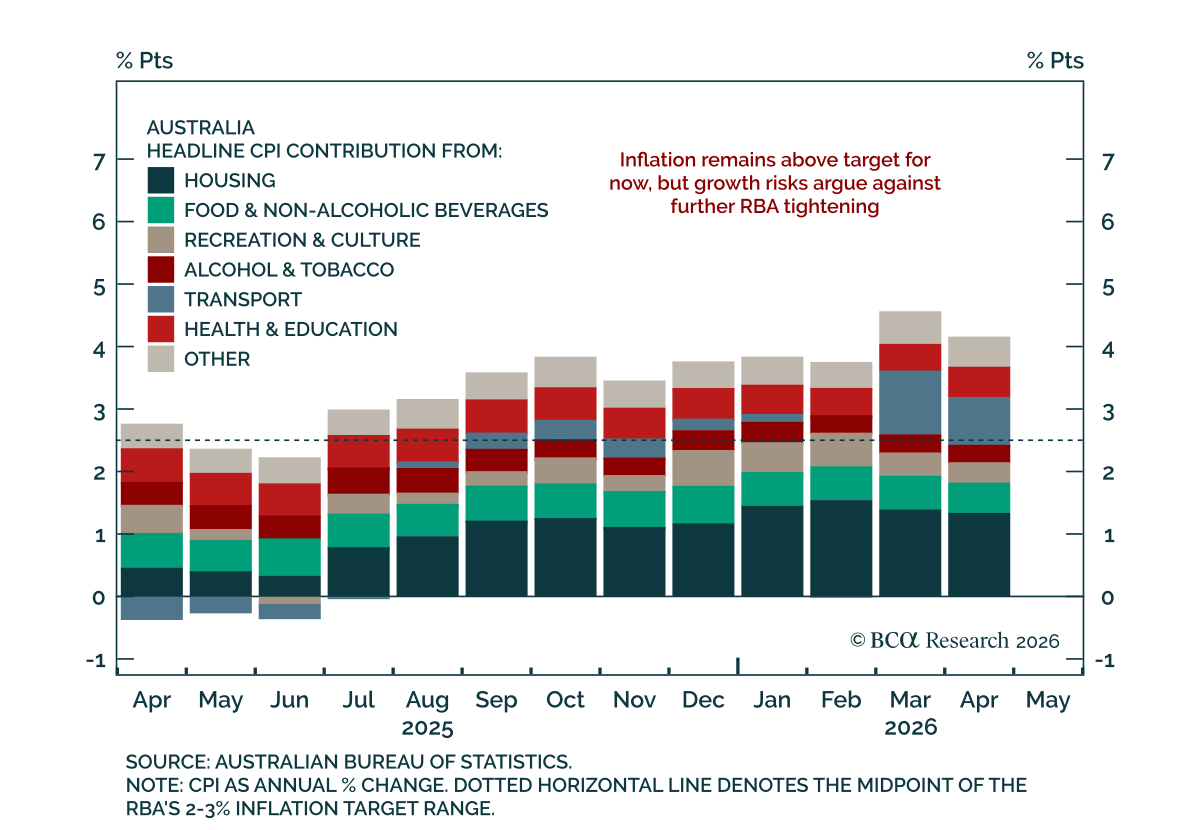

Australian CPI remains hot, but growth risks will limit further RBA tightening. April headline inflation decelerated more than expected to 4.2% y/y (0.4% m/m) from 4.6% (1.1%), partly reflecting a government fuel tax cut. The trimmed mean ticked up to 3.4%…

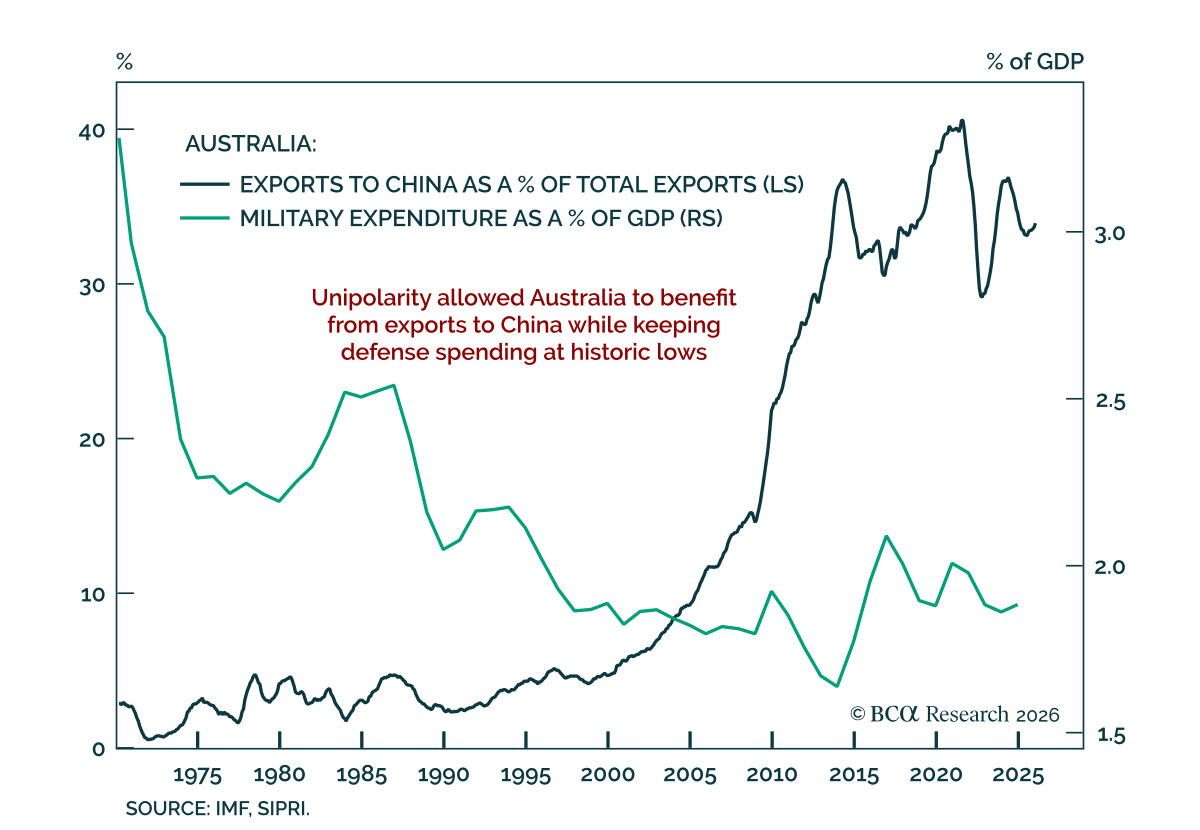

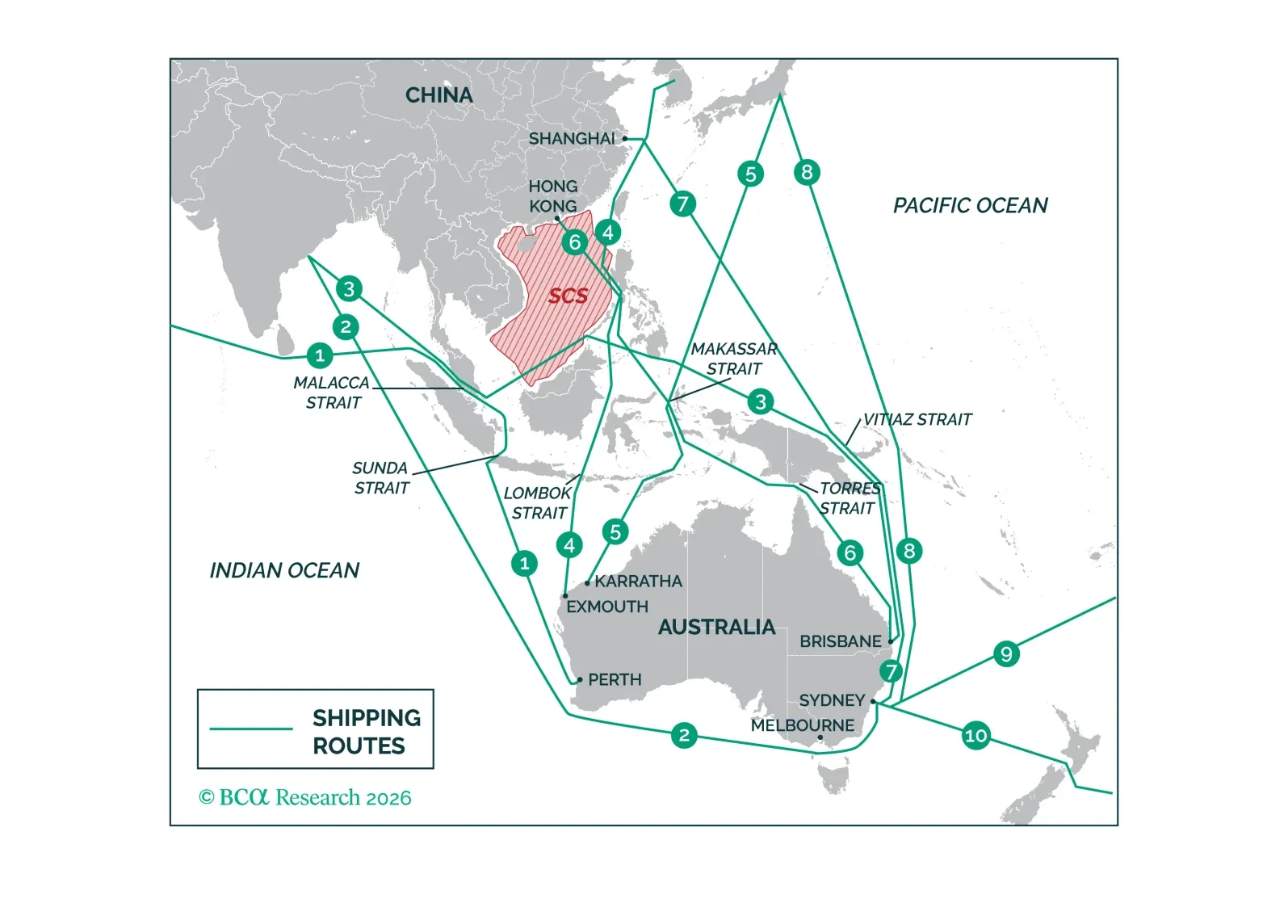

Our GeoMacro strategists see Australia as the most geopolitically conflicted major economy in the world. Its security depends on the US, its export revenues on China, and its trade routes run through waters both powers contest. How that triple exposure…

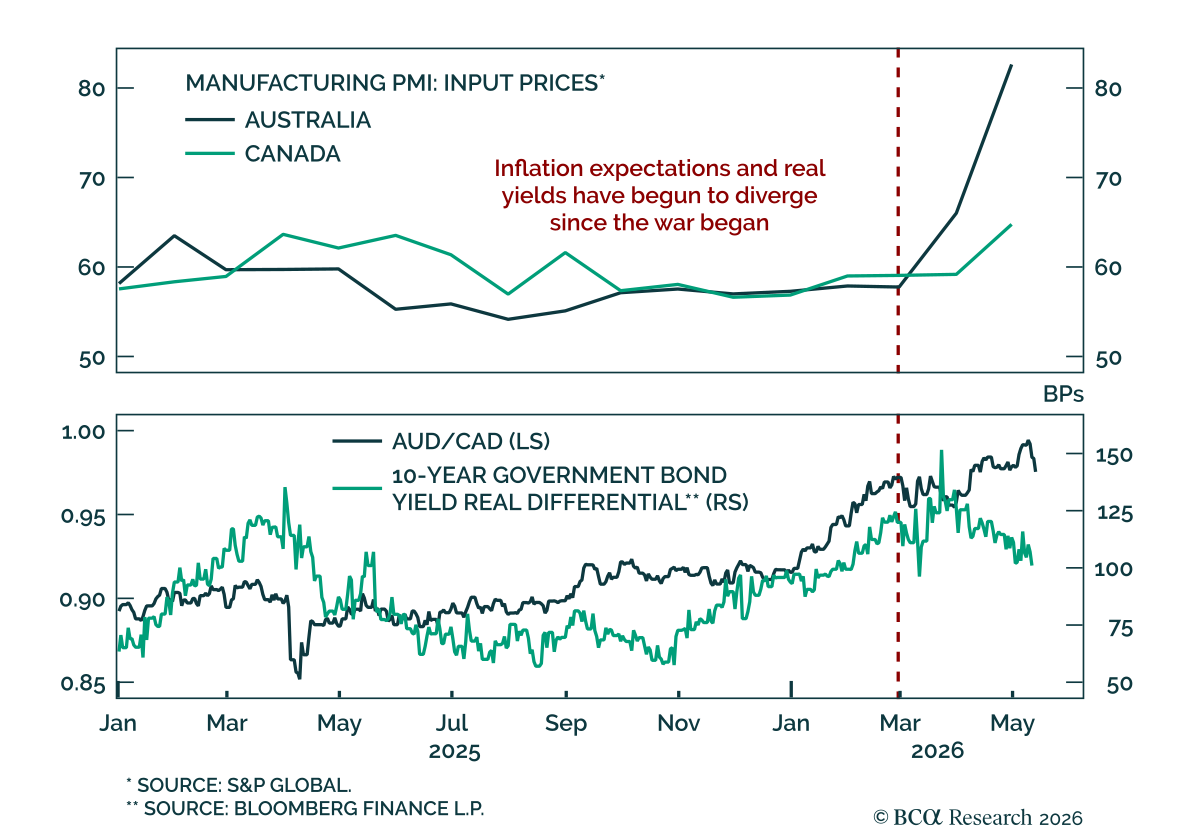

The Hormuz shock has pushed rate expectations higher in both Australia and Canada, but the inflation and growth transmission is already diverging. Canada’s status as a net energy exporter helps cushion the domestic growth impact from higher oil prices, while…

In this month’s Beta Report, we assess what that structural tension means for investors under two distinct scenarios. In our base case – a multipolar world order – Australia's position turns out to be more advantageous than it appears. The great power capital expenditure race generates demand for precisely what Australia produces. In the tail risk – a hard bipolar rupture – the calculus inverts, and the same commodity dependencies that long appeared as structural strengths begin to look like structural liabilities.

The April NAB survey points to a worsening growth-inflation mix in Australia. Business conditions moderated to +3 from +6, a fourth consecutive decline that left the index firmly below its long-term average. Business confidence, the more forward-looking…