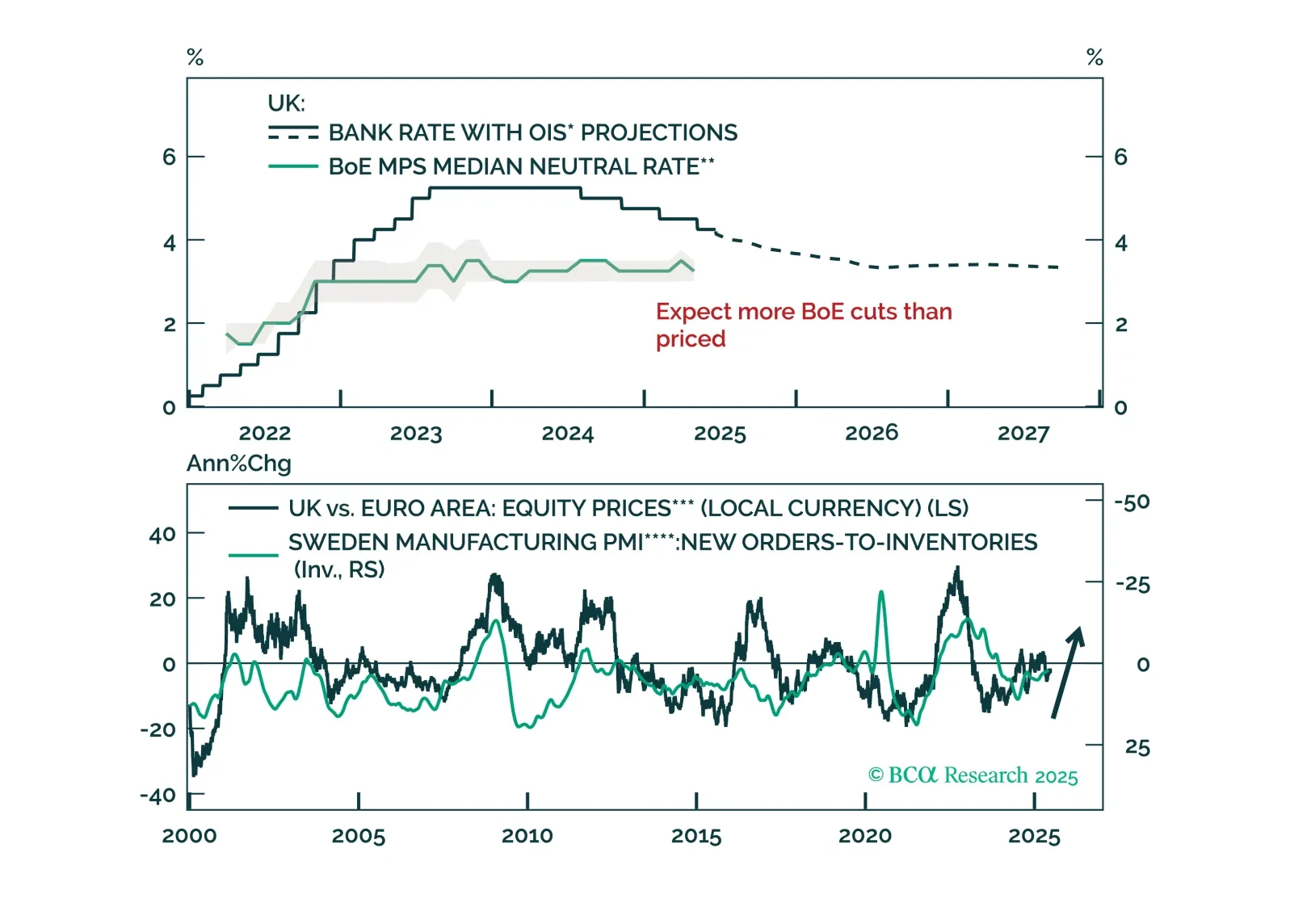

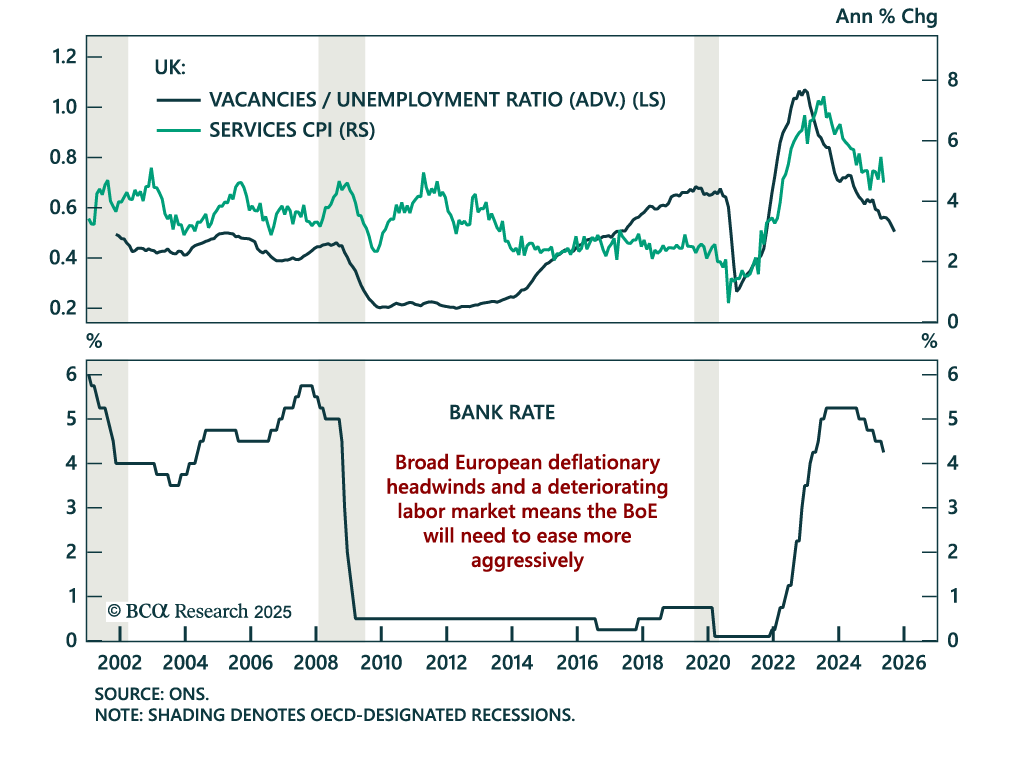

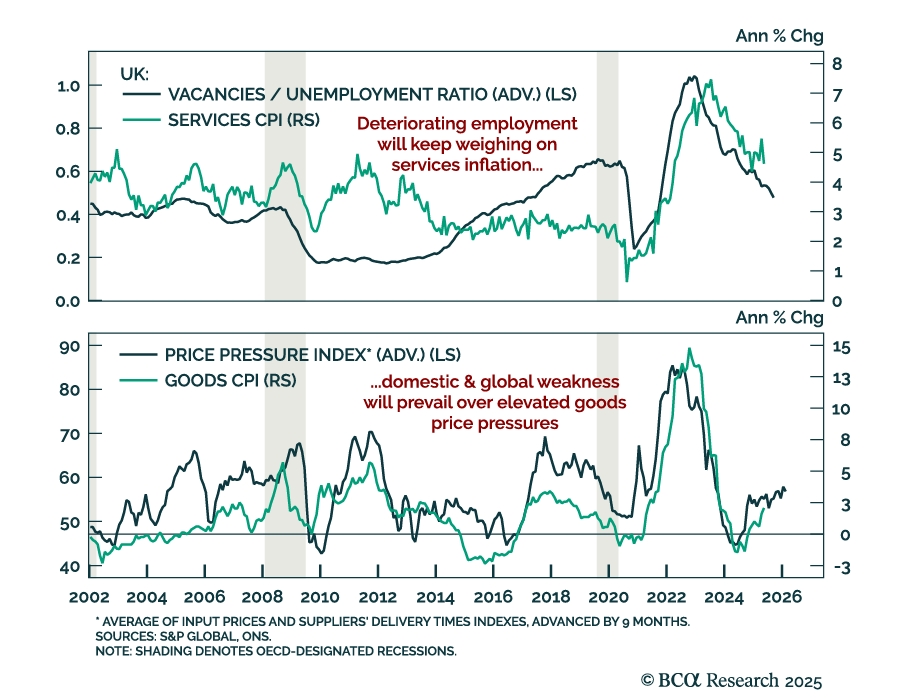

UK

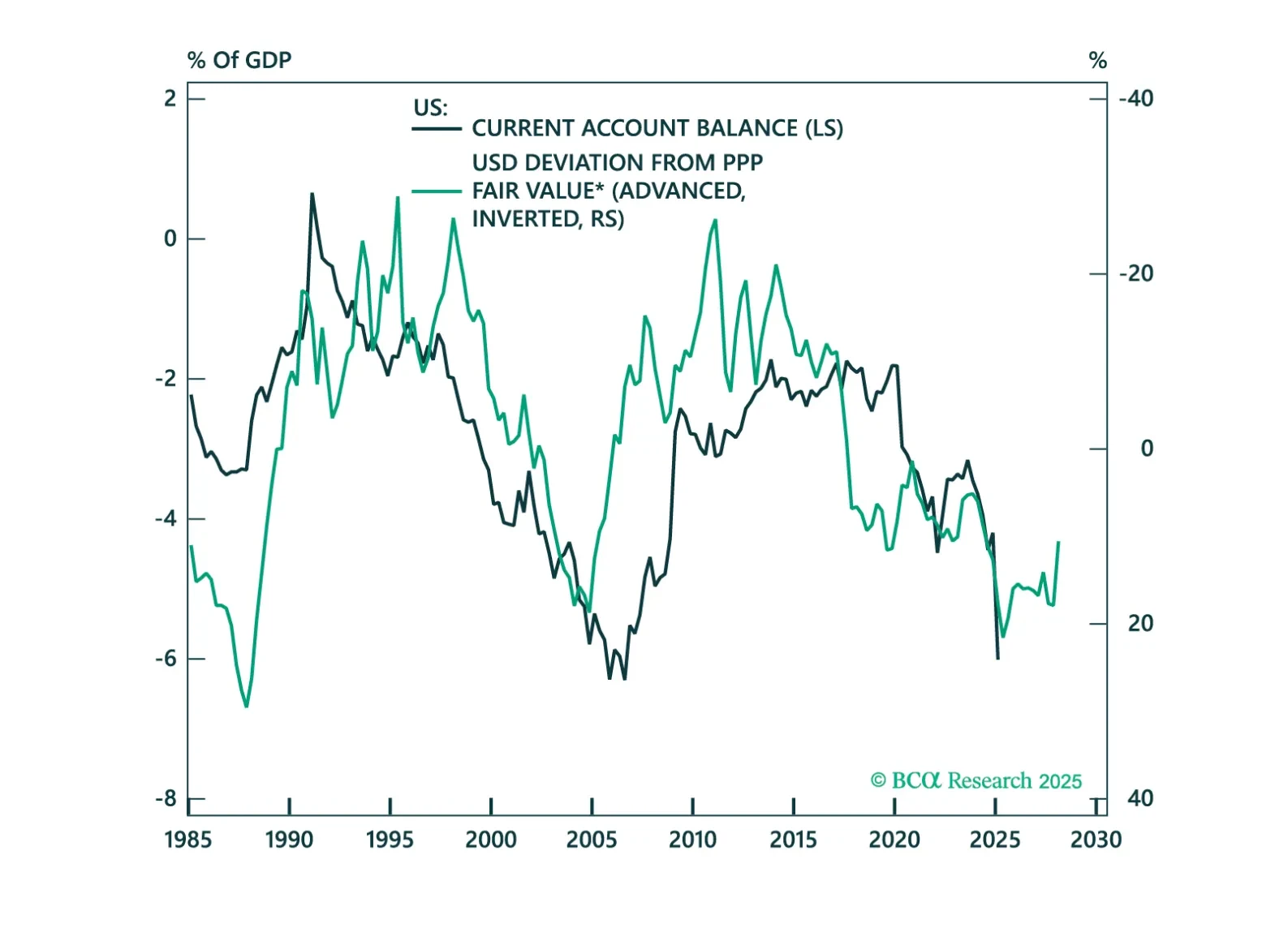

In this chartbook, we look at the balance of payments across DM and EM countries. The US does not fare well, but neither do a few other countries.

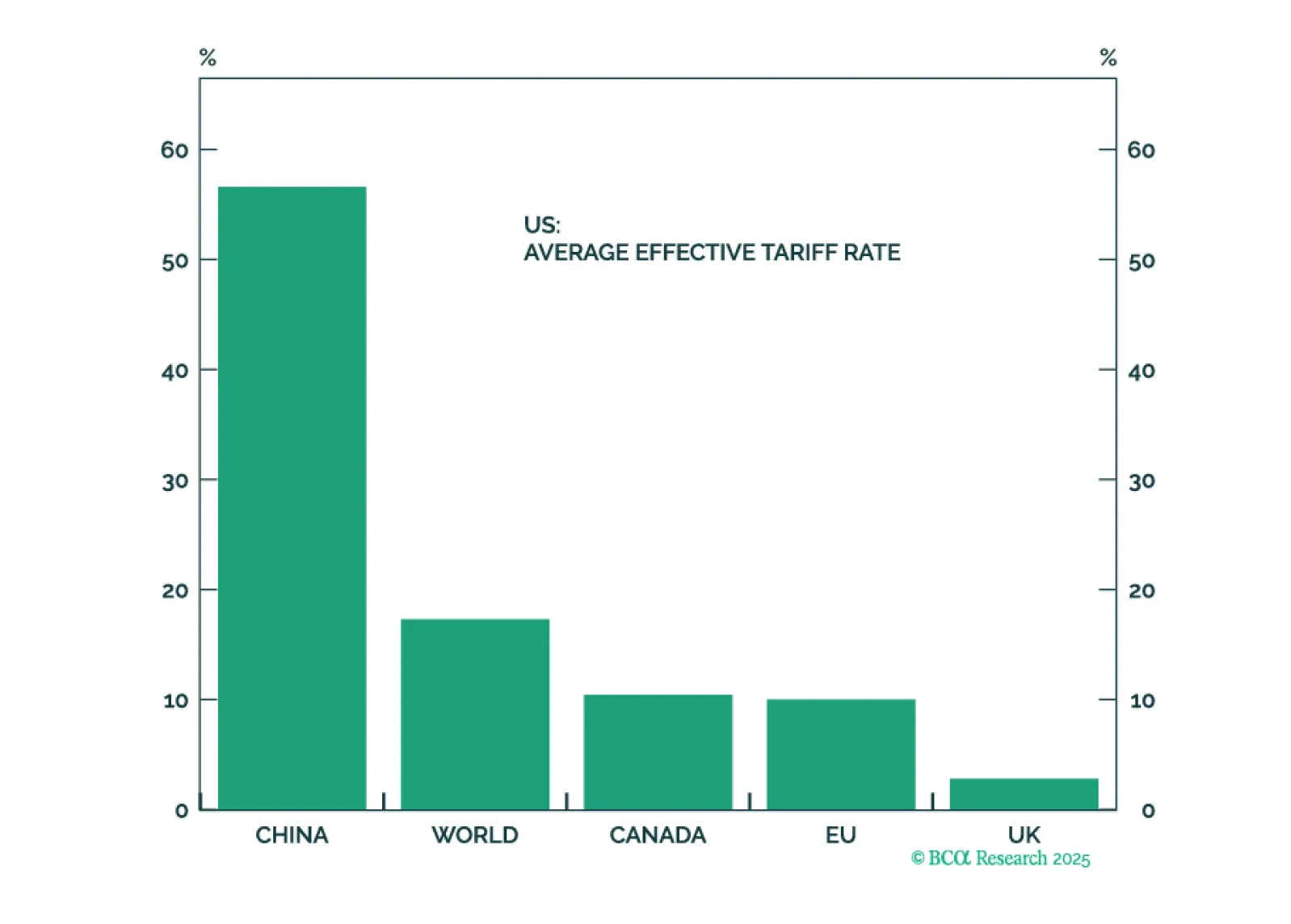

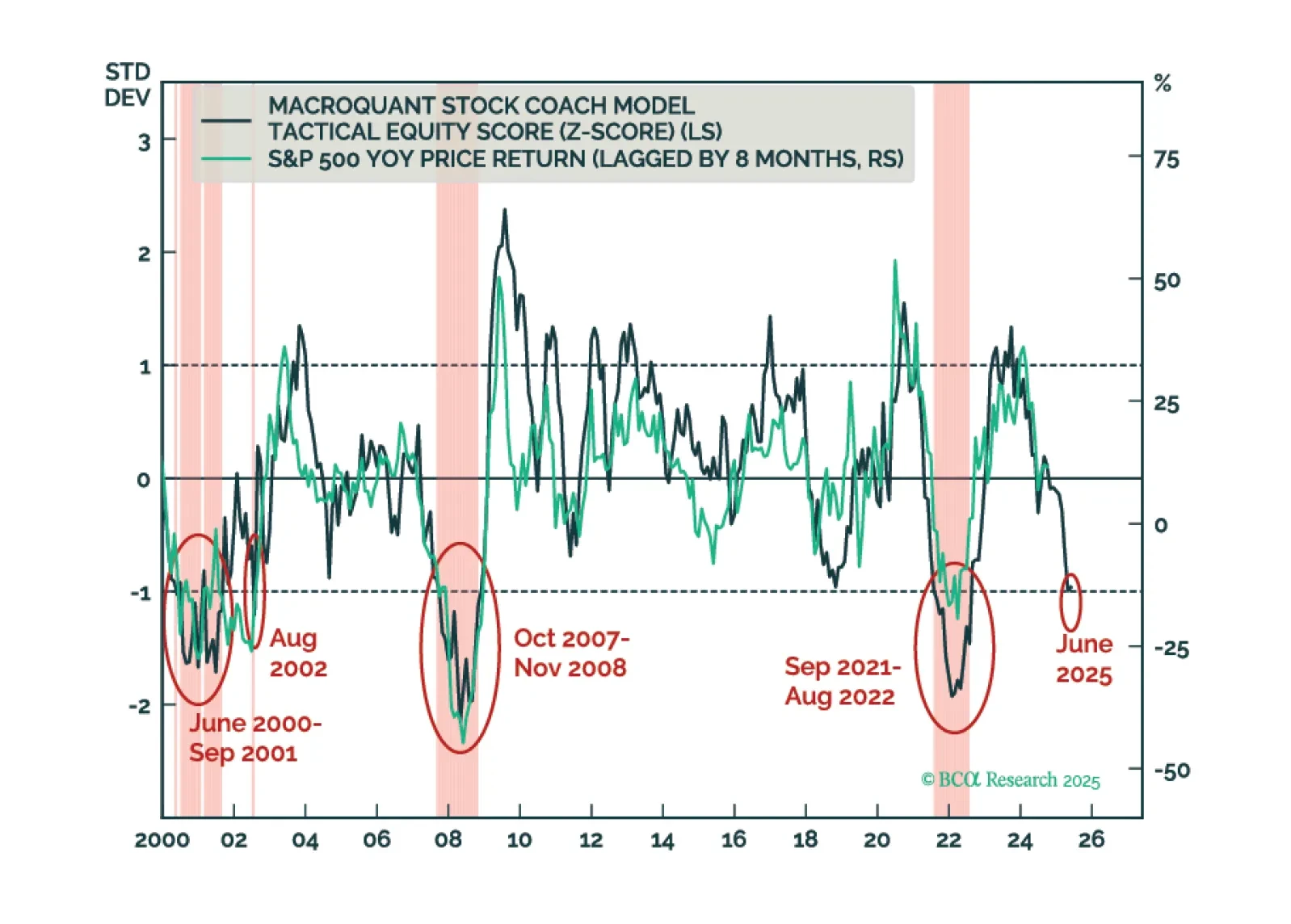

Acute geopolitical risks, like a massive oil shock, may be abating. But structural geopolitical risk remains high and could upset a blithe market. Cyclical economic risks are underrated as the US slows down and China continues to stumble. Investors should book some profits in anticipation of tariff implementation and a downturn in hard economic data.

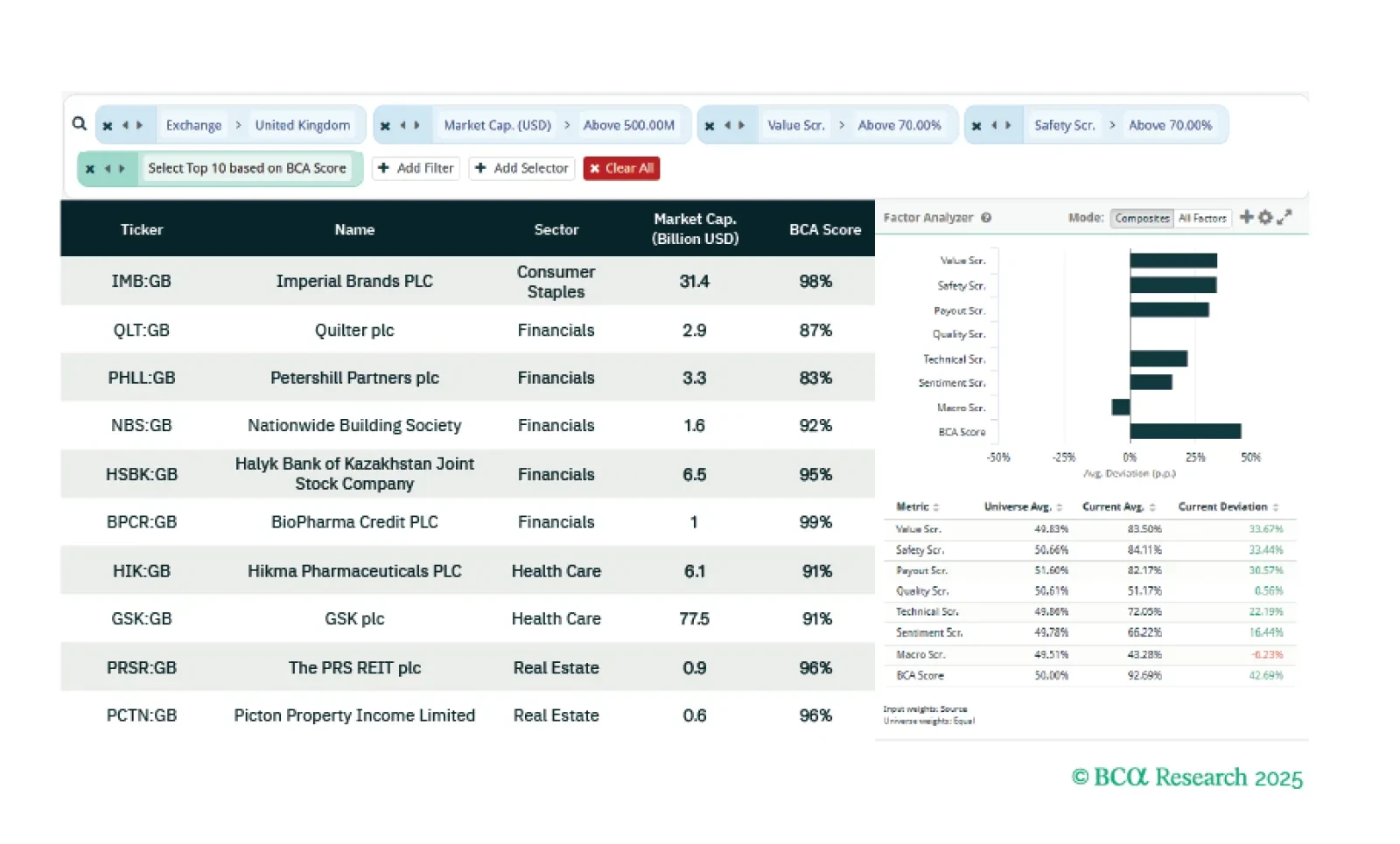

This week our three screeners explore: UK stocks that are cheap and offer a geopolitical hedge; French stocks that are sensitive to China; and US Value and dividend paying stocks.

Investors should modestly underweight equities in their portfolios and look to turn more aggressively defensive once the whites of the recession’s eyes are visible. We think that will happen within the next few months.

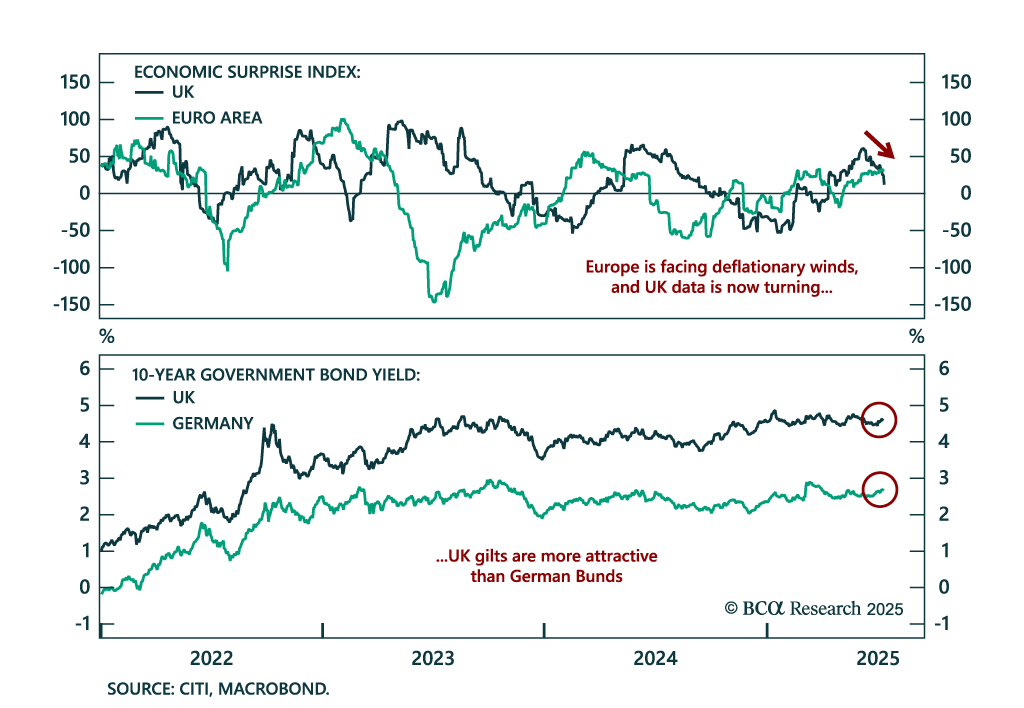

UK inflation risks are falling on the back of a weakening labor market. Read why Gilts and UK stocks are poised to outperform as BoE easing resumes.

In this Insight, we highlight our strong conviction trades based on the central bank meetings held by the Bank of England, the Norges Bank, the Swiss National Bank and the Riksbank.

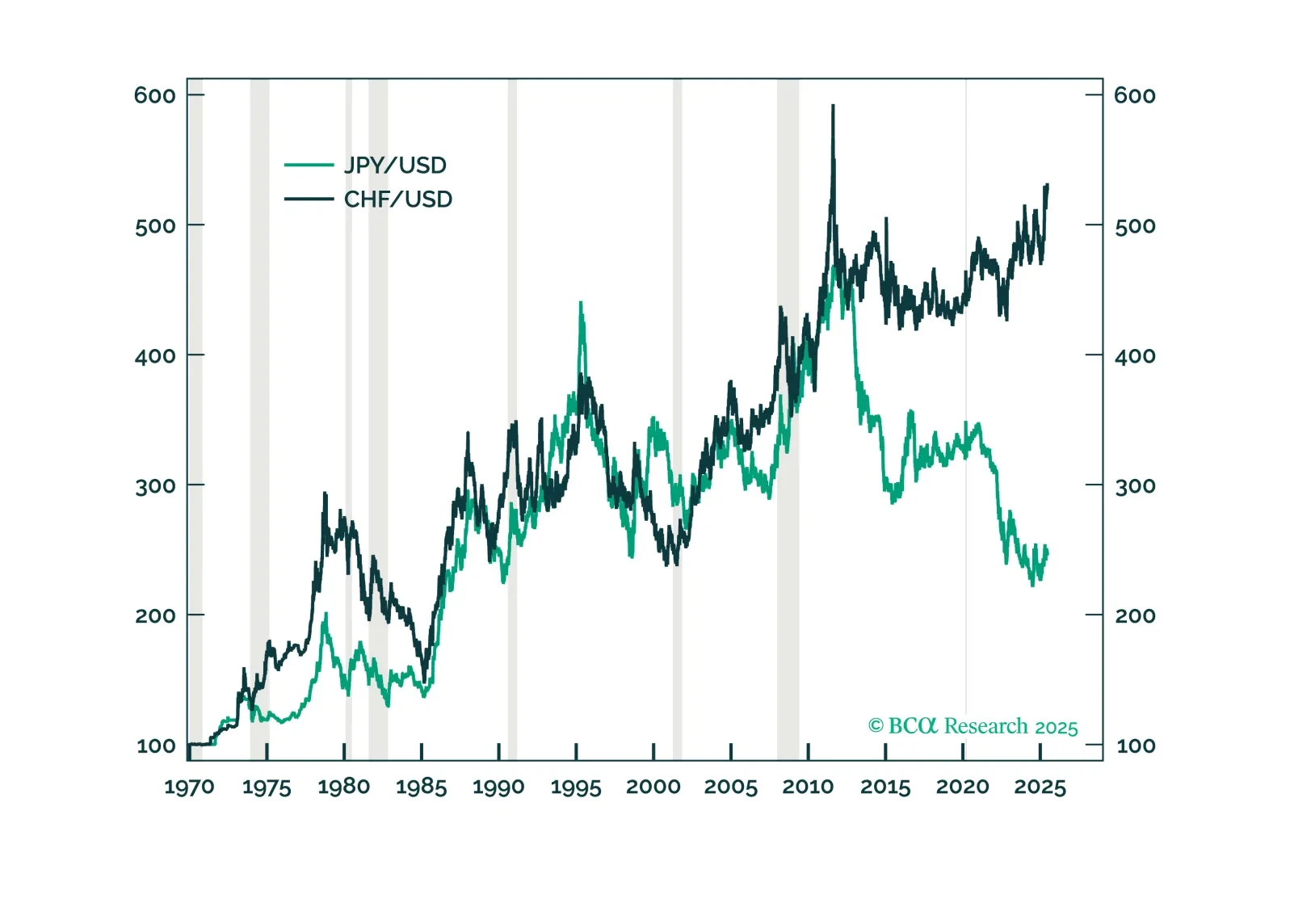

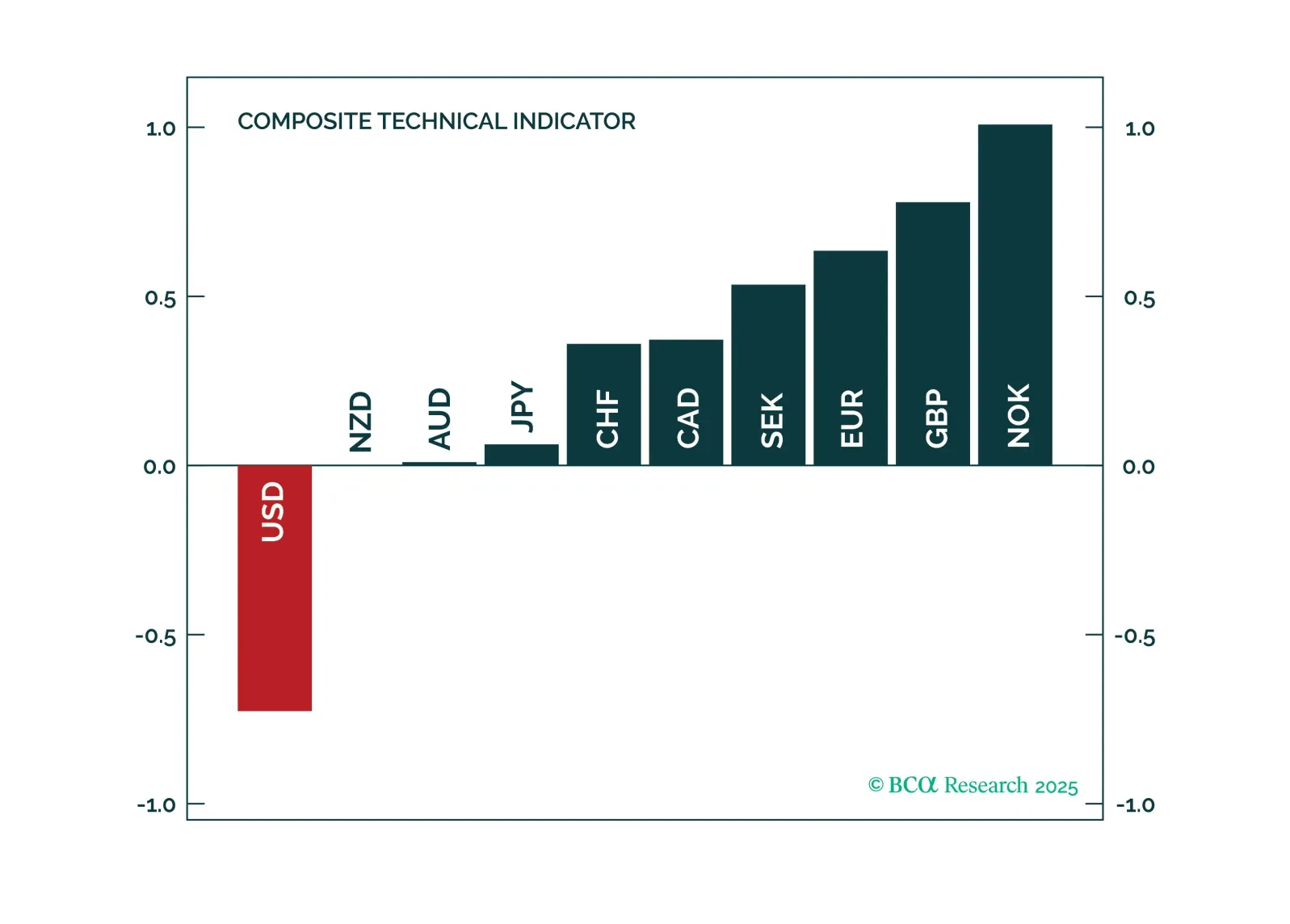

In this FX note, we provide a rationale for why it is important to pay attention to technical indicators, while still keeping your eyeball on the structural factors that drive currencies. This report answers the following questions: 1. Should you buy or sell the USD over a three-to-six month period from the pure lens of our proven technical indicators and 2. What are the best tactical cross trades among currencies.