UK

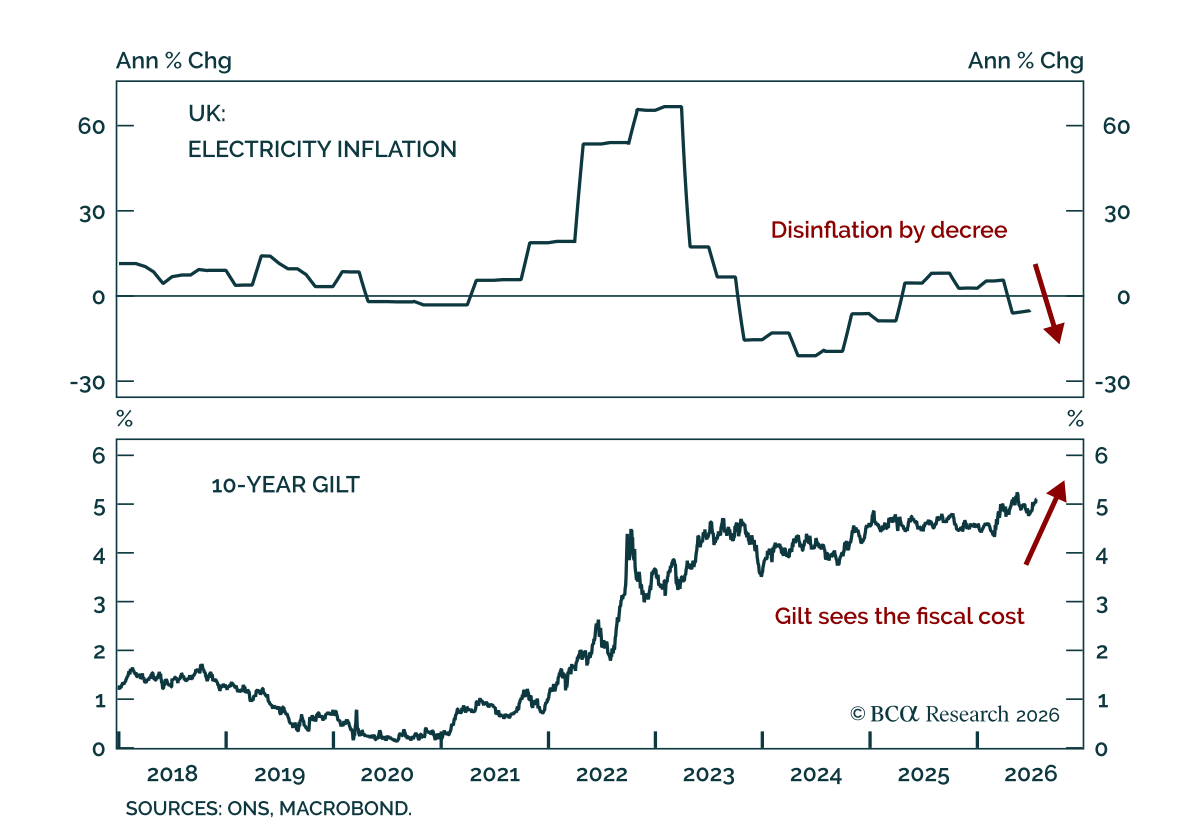

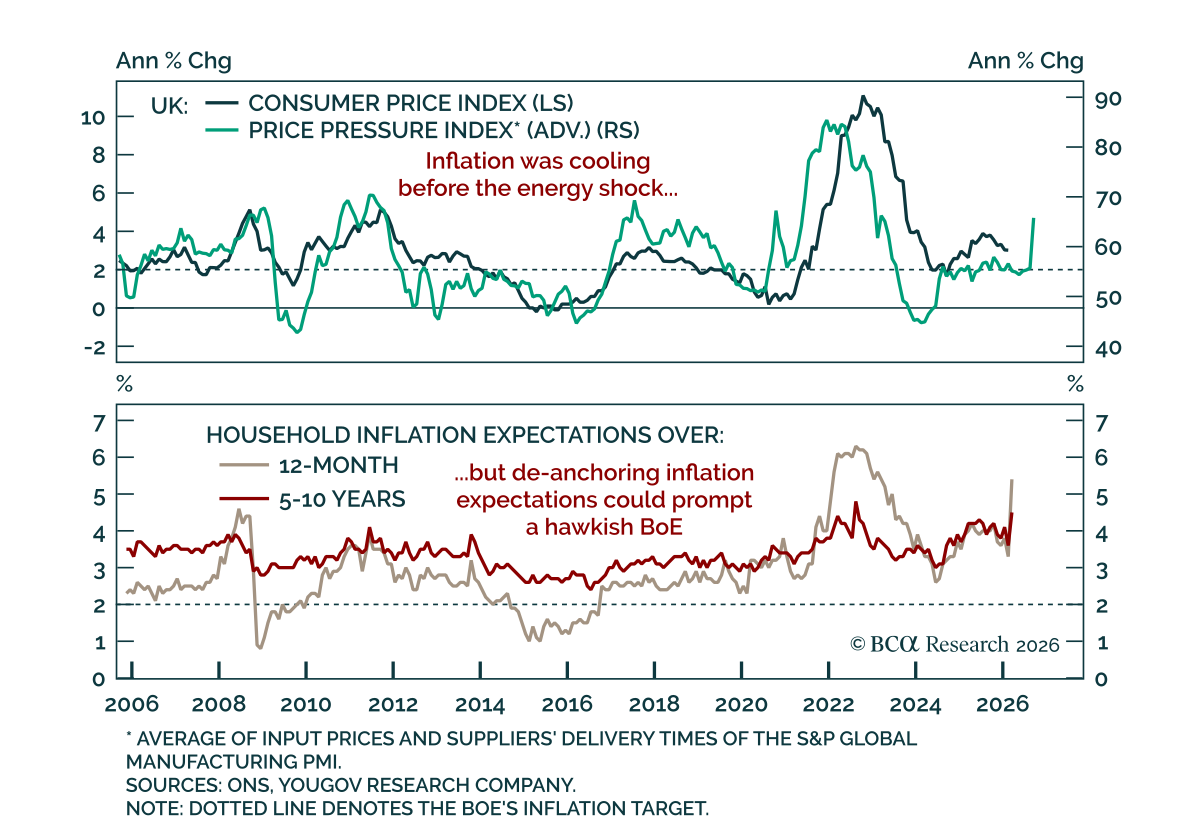

The UK’s latest cost of living relief may lower measured inflation, but it risks worsening concerns about fiscal credibility. June CPI was cooler than expected, falling to a 15-month low at 2.6%. Yet, this is not a clean disinflation story. UK inflation has…

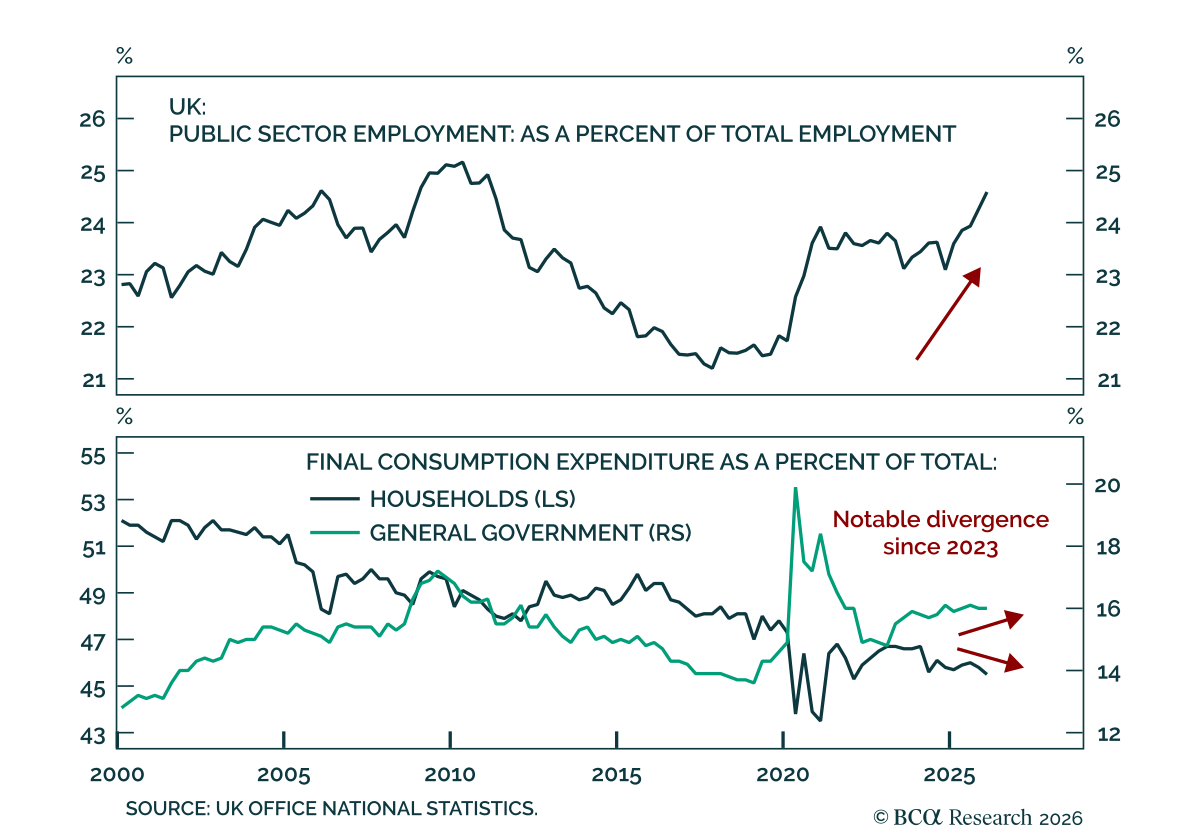

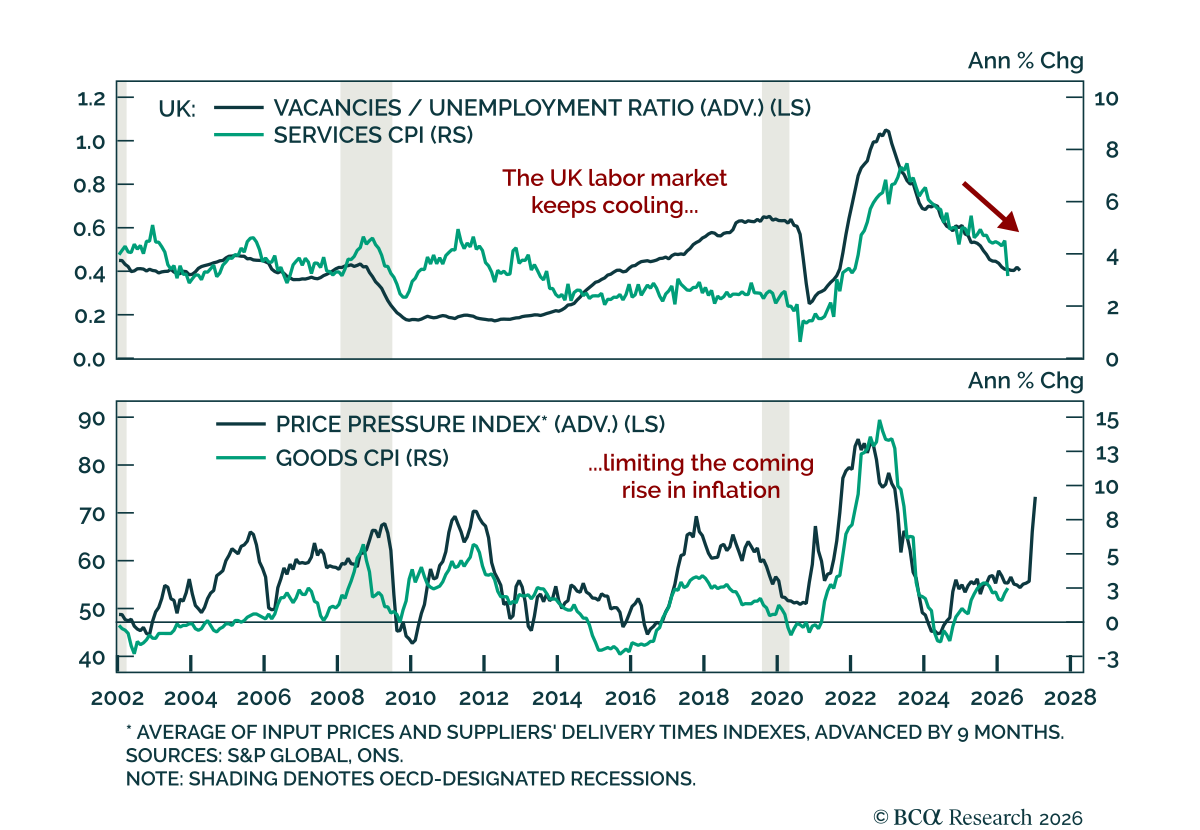

UK May/June employment data came in marginally above consensus, yet only point to a labor market stabilizing at a weak level. Payrolled employees fell by 4k in June, versus expectations for an 8k decline. Job vacancies were broadly flat, as were the…

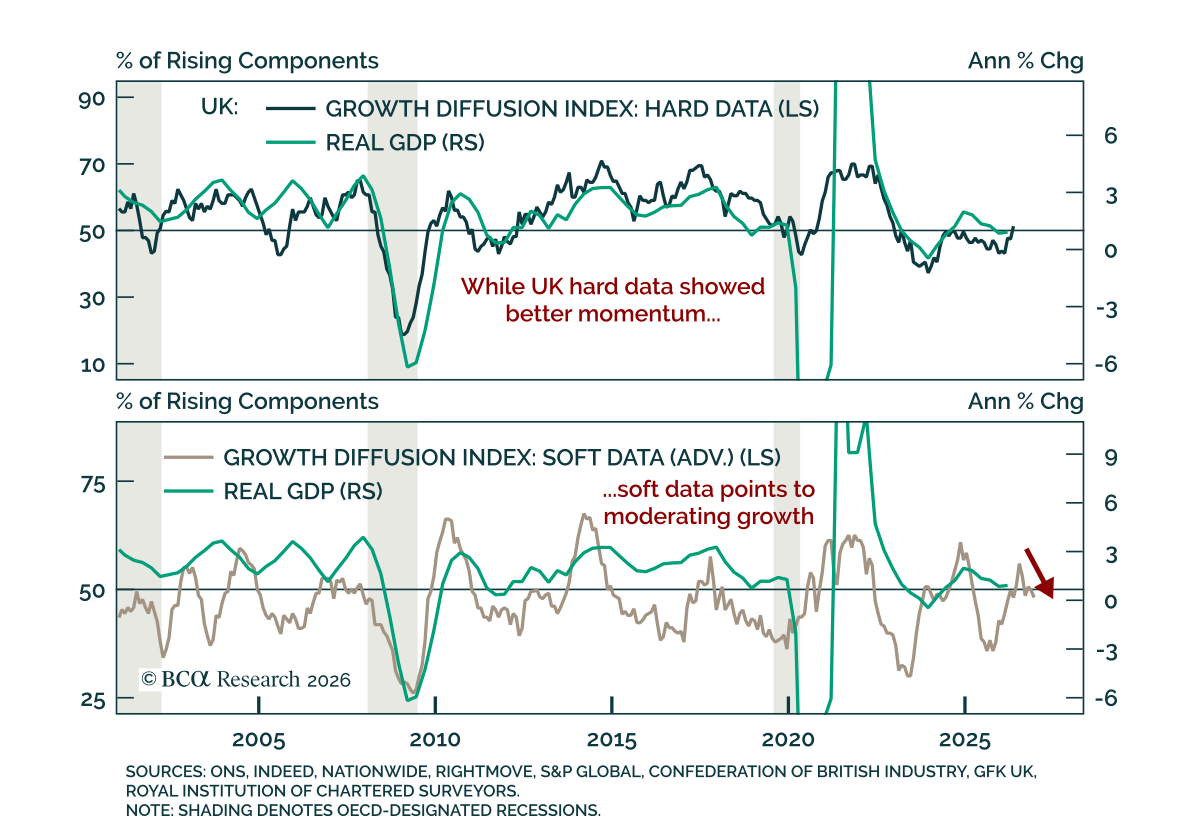

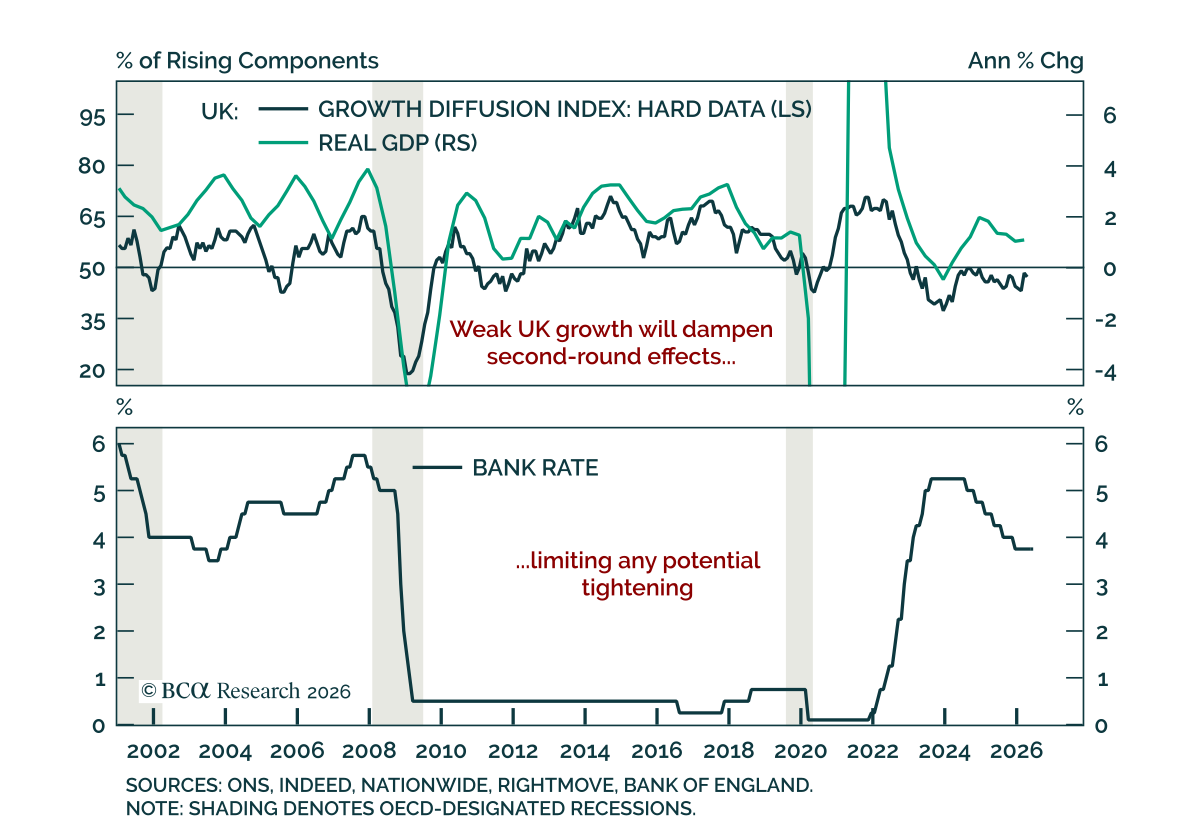

UK May hard data surprised to the upside, but still pointed to weak growth and limited scope for further BoE tightening. Hard data refers to directly measurable activity such as production, employment, and spending. Monthly GDP rose 0.1% m/m after contracting…

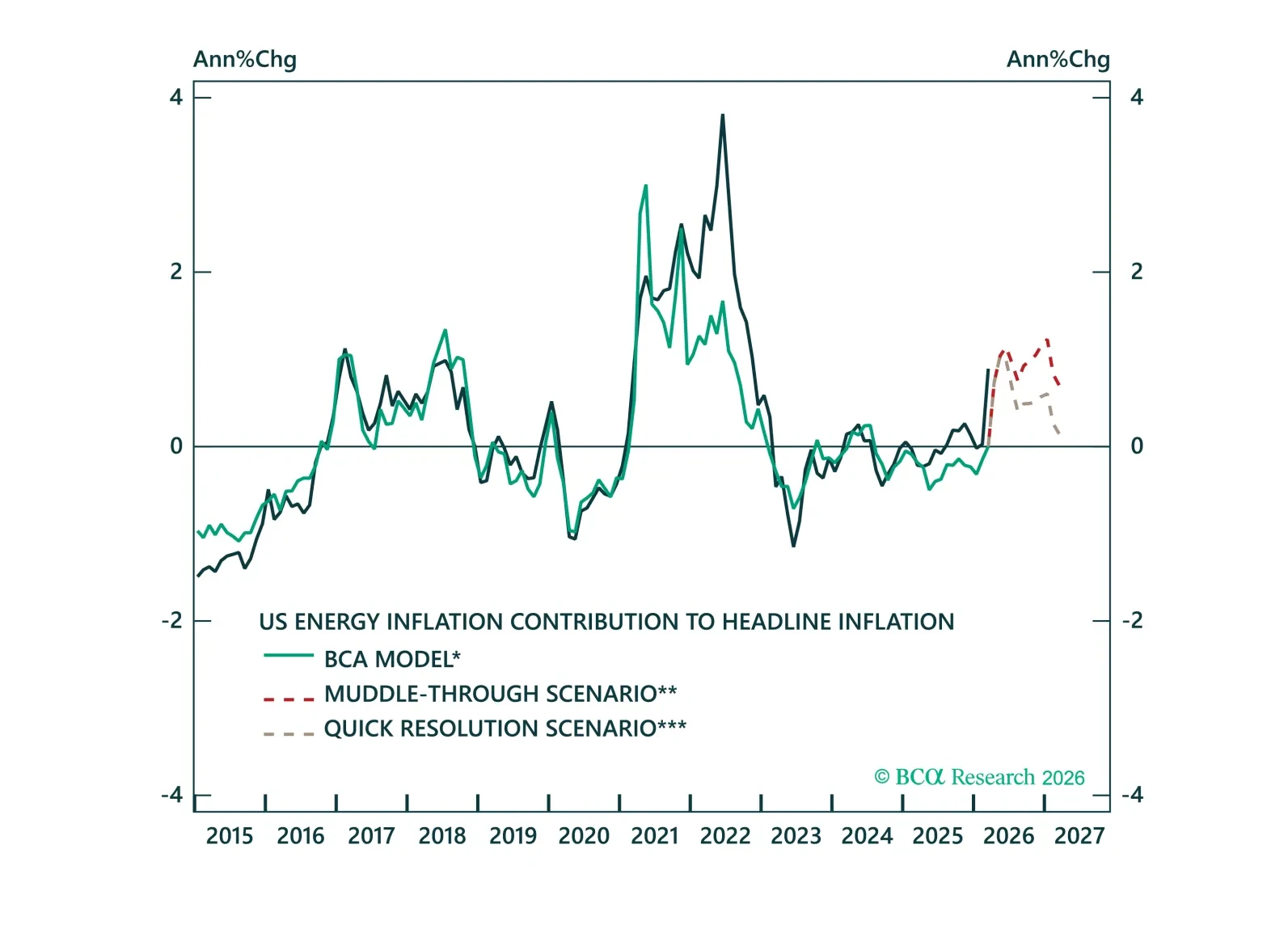

The UK economy entered the latest energy shock with recessionary signals already flashing red. While the rise in energy prices is unlikely to rival the 2022 crisis, it could still have a disproportionate impact on growth as the economy was already weak.…

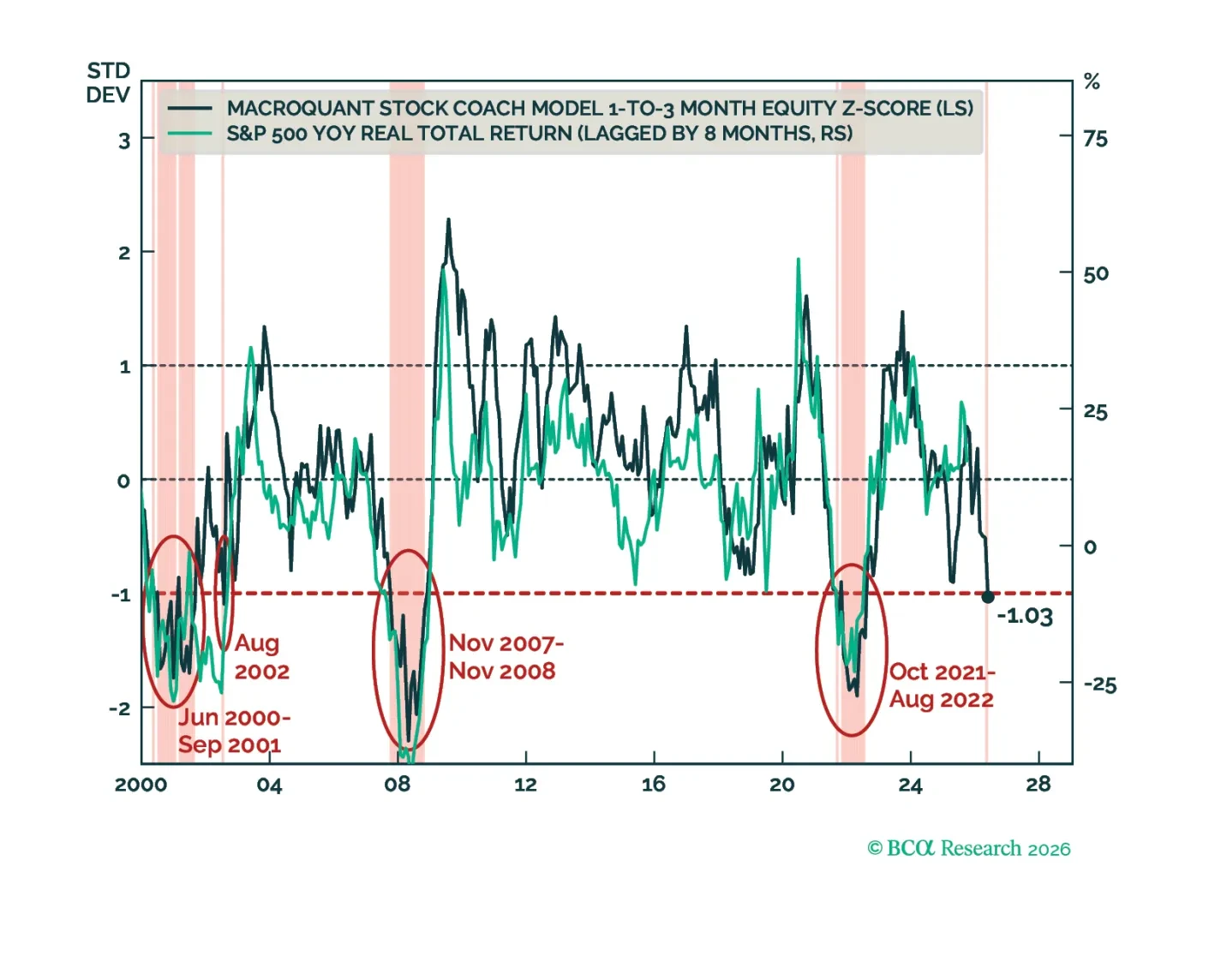

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

Stay overweight gilts despite renewed political turmoil in the UK.

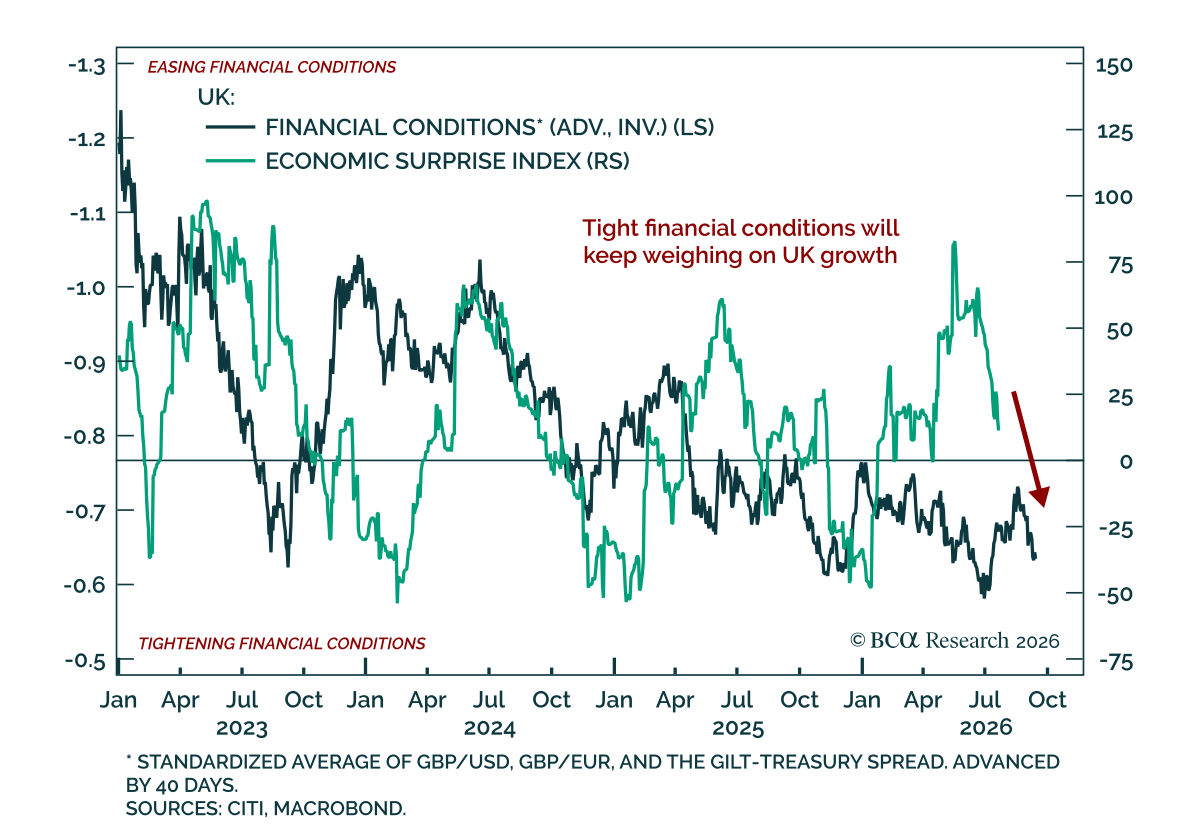

The Bank of England held rates at 3.75%, as expected; we remain overweight UK gilts on a 12-month horizon. The hold was a 7-2 decision, with the two dissenters favoring a hike. Those MPC members were concerned about second-round effects and pointed to…

The latest UK employment and inflation data came in cooler than expected, reinforcing the case for weaker growth ahead. Payrolls fell by 100k in April after a 28k decline in March. The unemployment rate also rose 0.1pp to 5.0%. Average weekly earnings ticked…

Volatility is high, but the path for yields is clearer than it looks. Across three oil scenarios, we show how policy responses shape fixed income markets and why the balance of risks still points to lower yields.

UK February inflation was broadly in line with expectations, but the report is already stale in the face of the energy shock. Headline CPI was unchanged at 3.0% y/y, while core CPI rose slightly to 3.2% from 3.1%. Services inflation ticked down to 4.3% from…