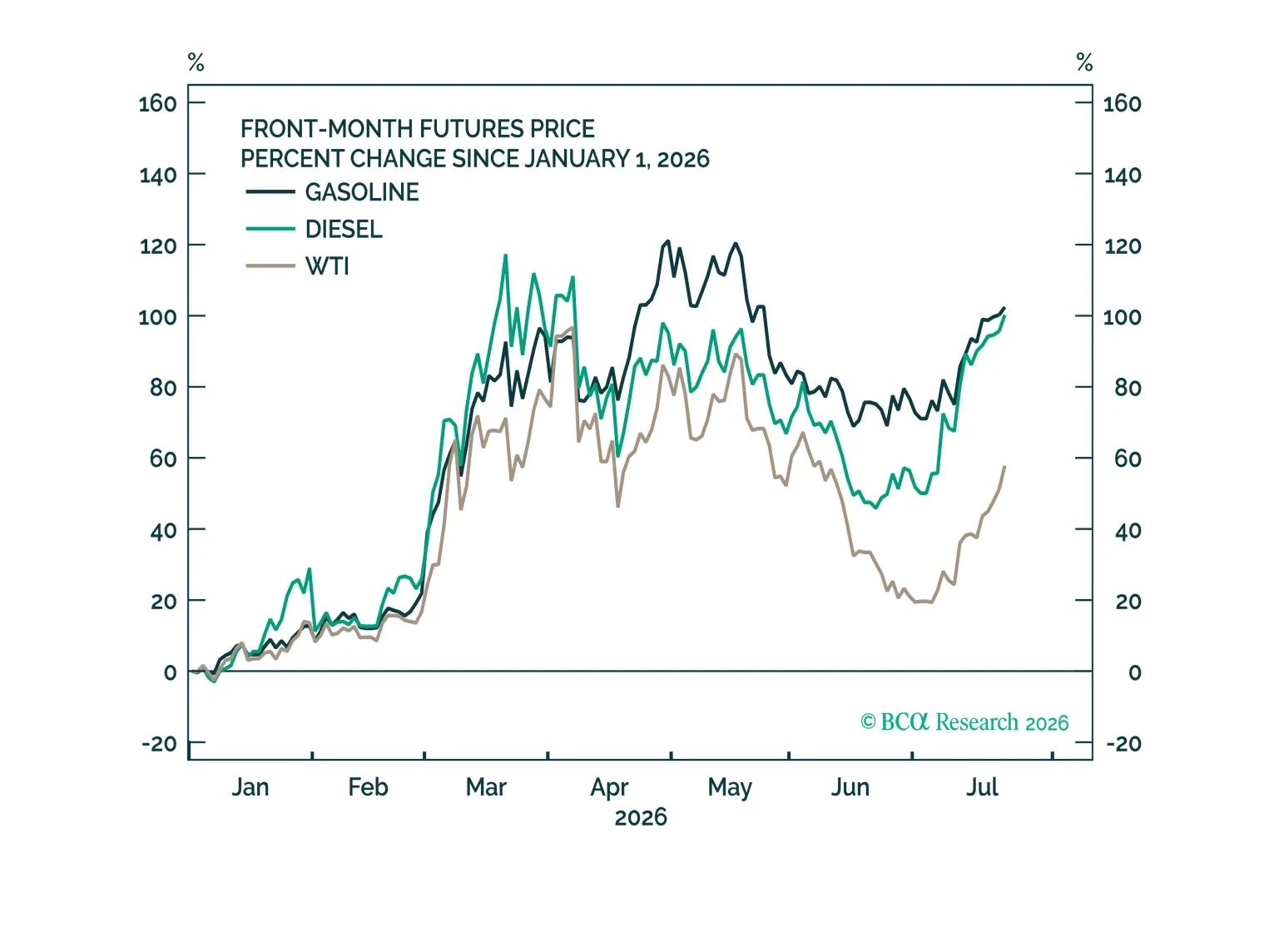

Tariffs

As long as the AI boom keeps booming, all other investment considerations will remain on the back burner. However, if the AI trade fizzles, this would expose deep-seated problems within the global economy, which could very well lead to an economic downturn as early as next year.

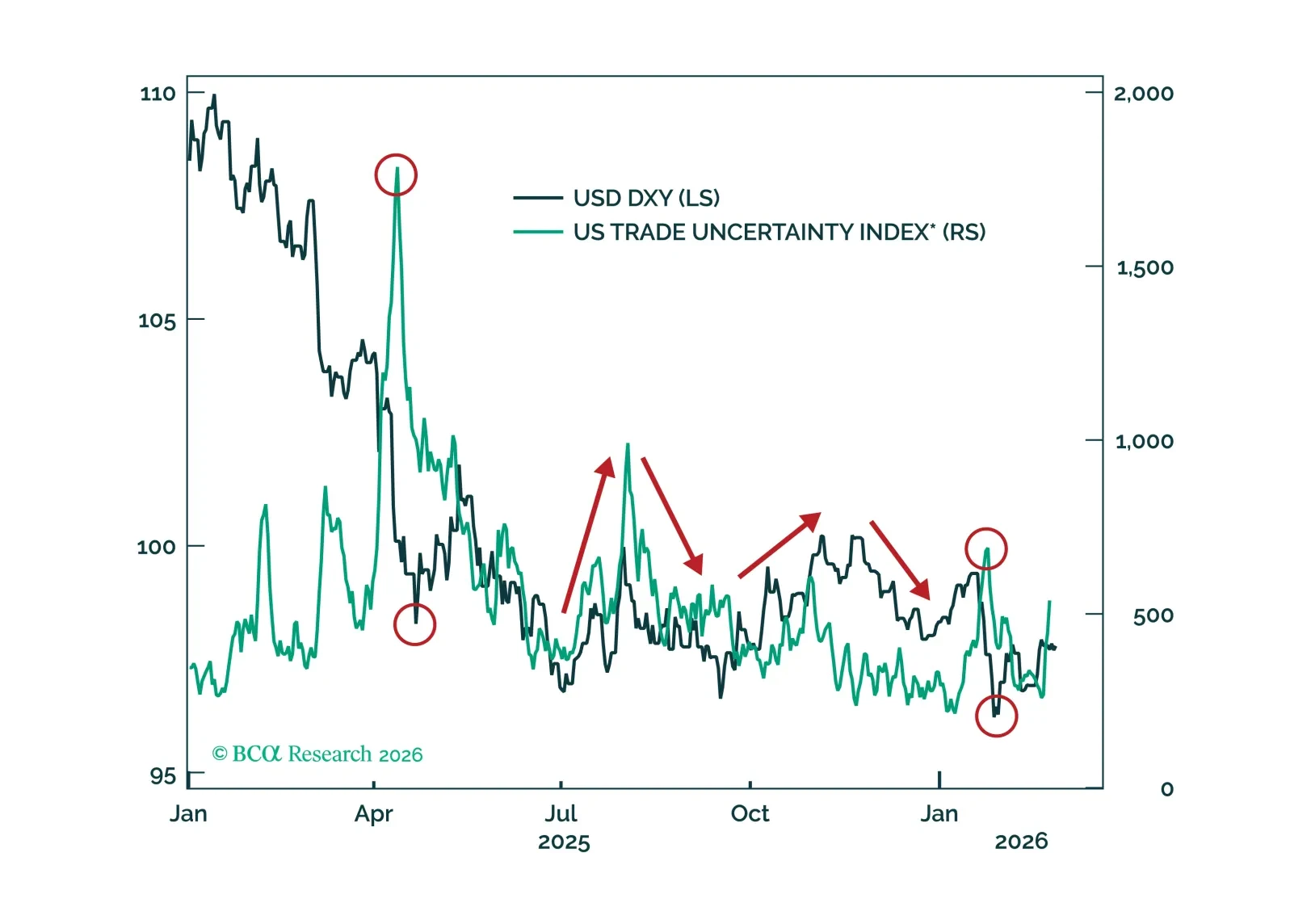

Policy risks are set to fade just as markets underestimate hawkish Fed repricing and crowd into short-USD positions, setting the stage for a tactical dollar rebound into the election cycle. Go long USD/CHF to capture the rate differential and receding policy uncertainty.

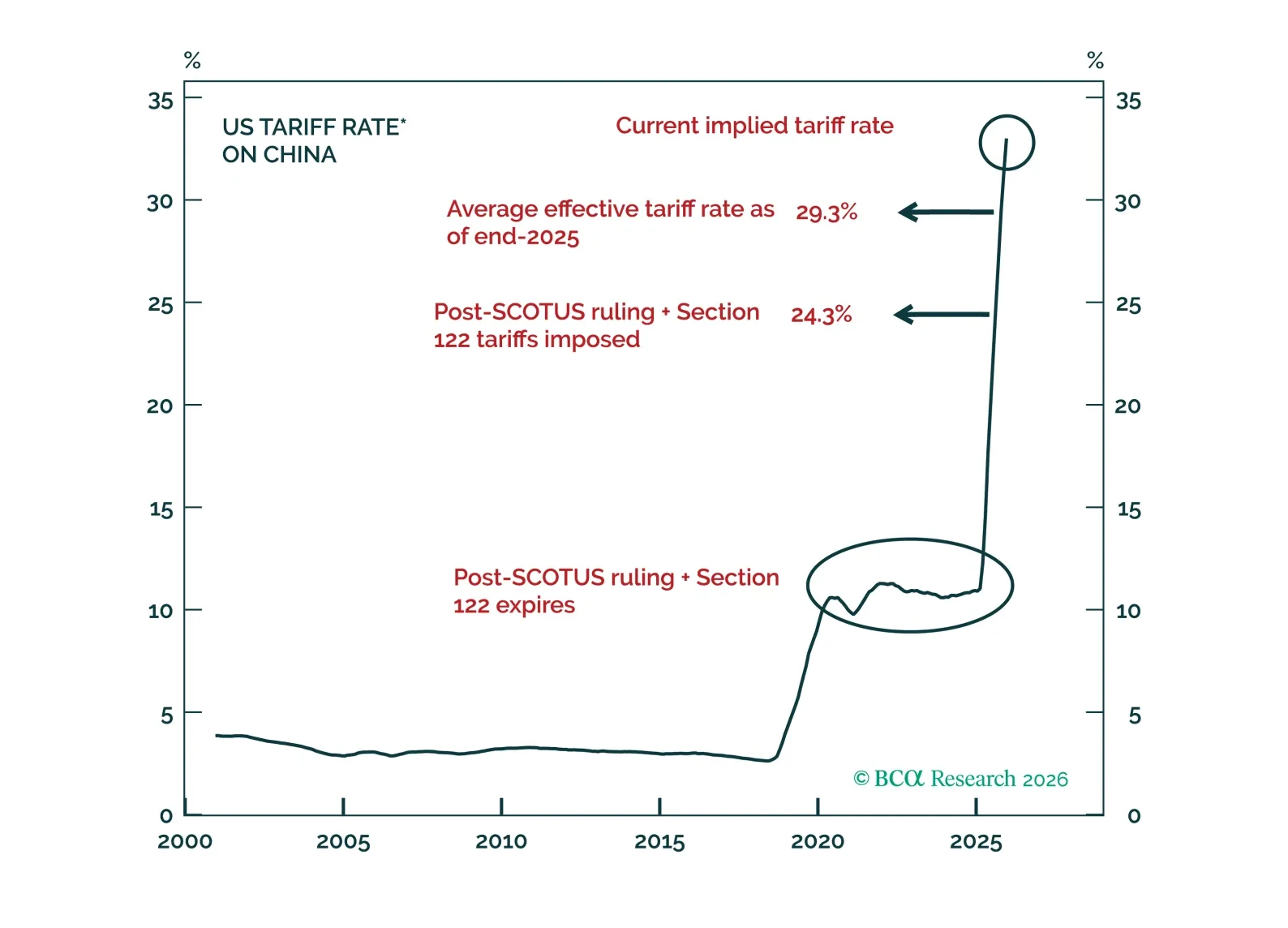

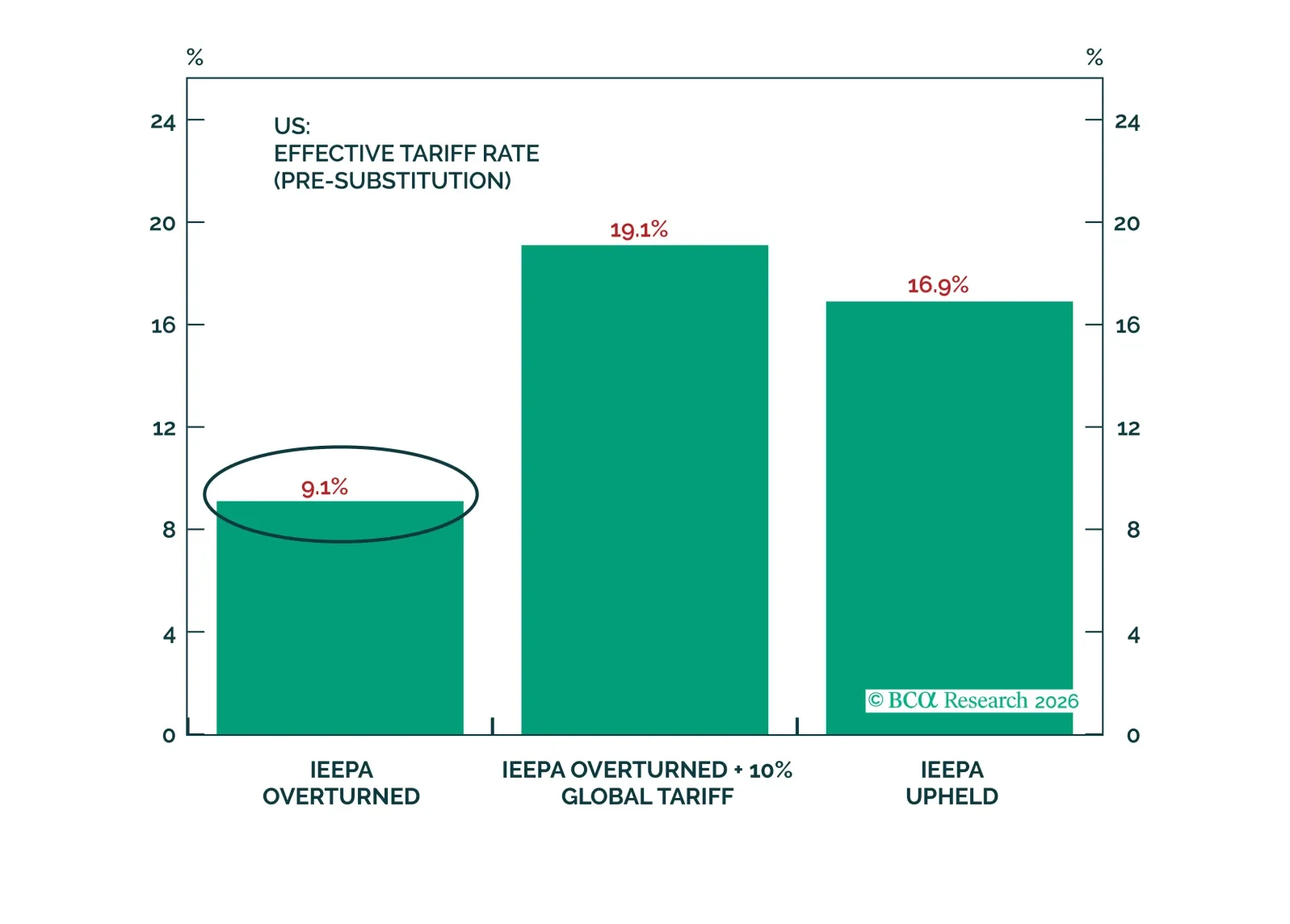

This report examines the implications for Chinese exports and global trade in light of the US Supreme Court’s ruling on tariffs.

Trump is saving face with new tariffs but will avoid any major new tariff shock until 2027. For now, Iran risk will overshadow tariff volatility.

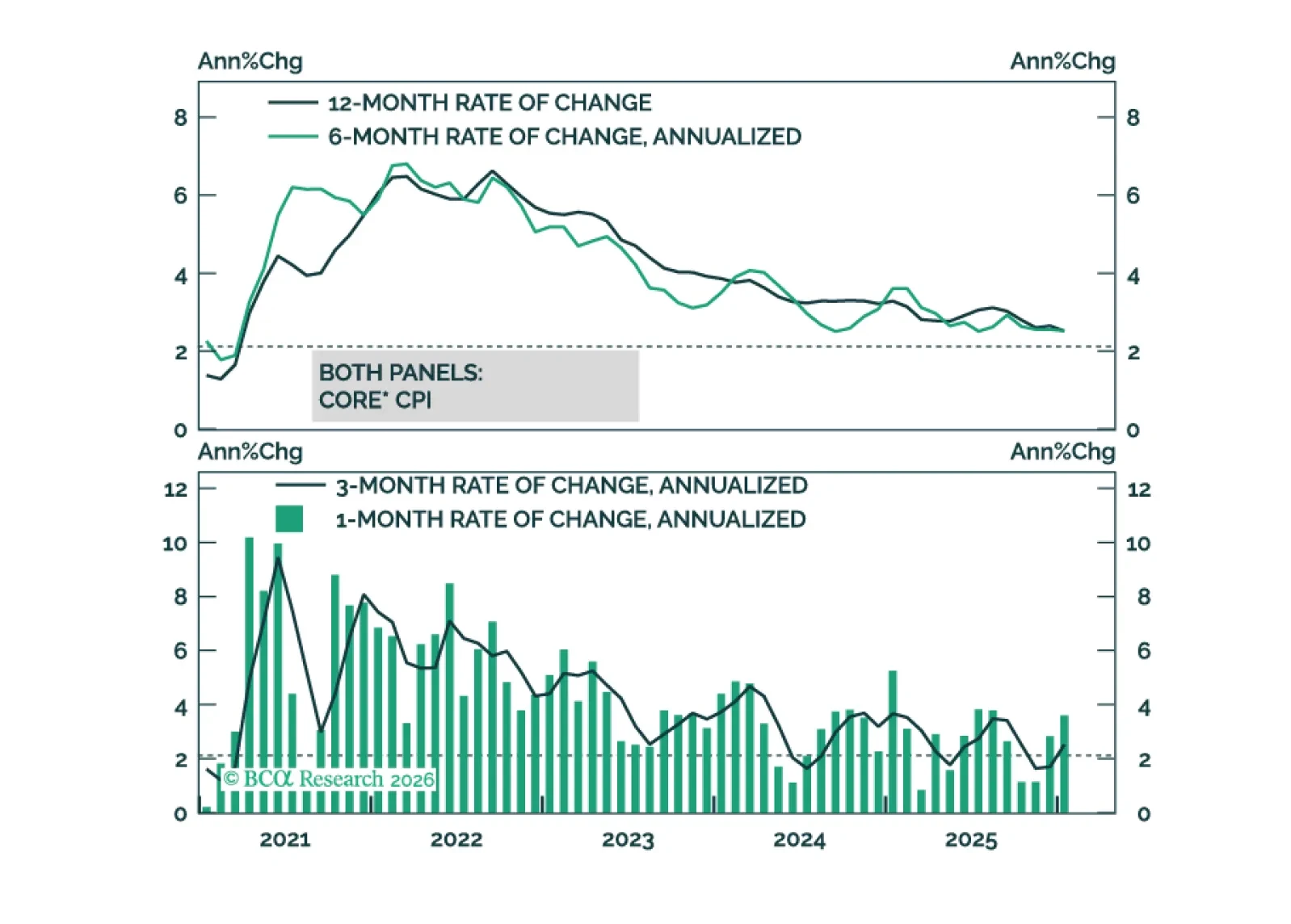

Core inflation will get close to the Fed’s 2% target by the end of this year.

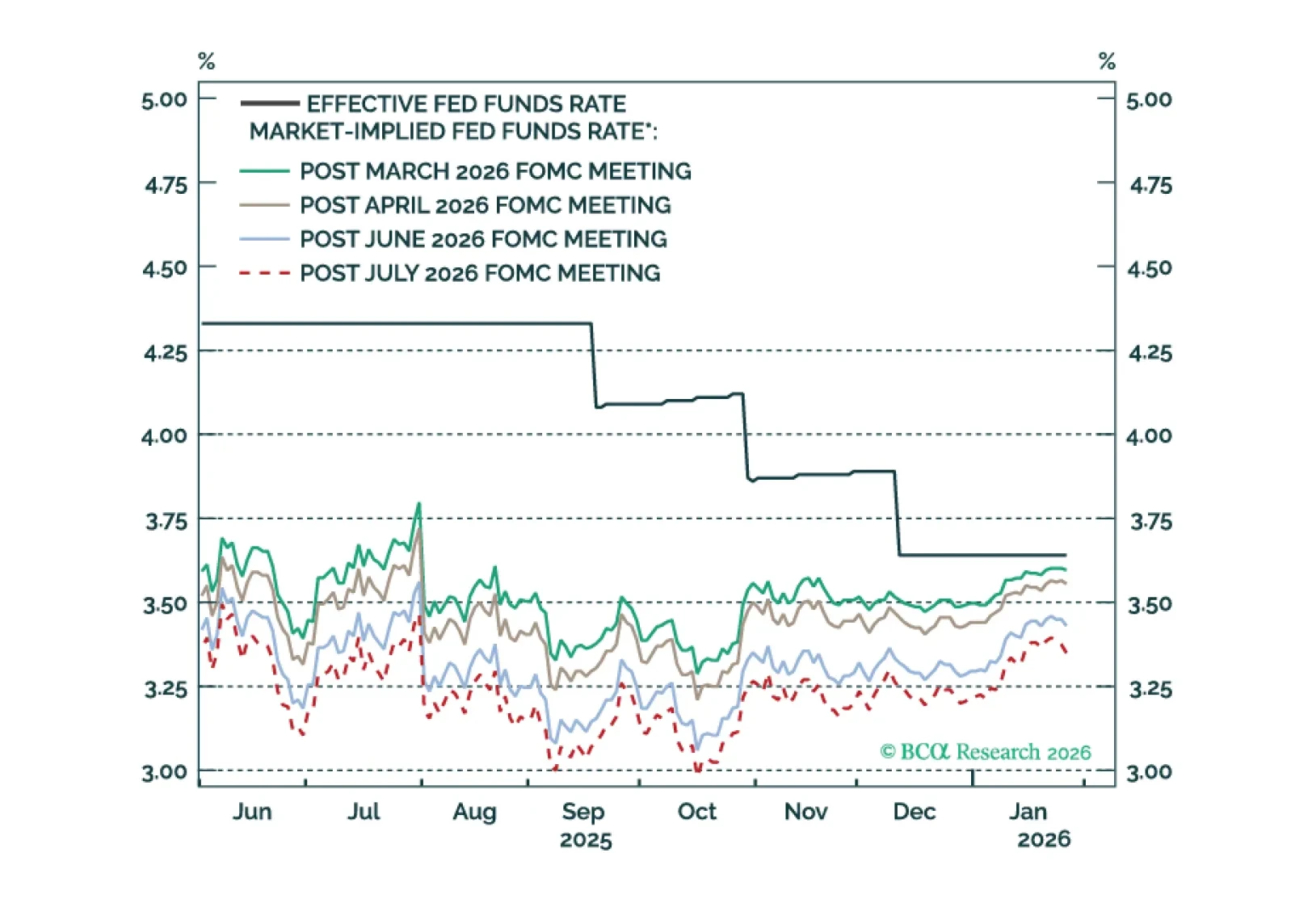

The Fed will keep rates on hold in H1 2026, but dovish policy surprises are likely in the second half of the year.

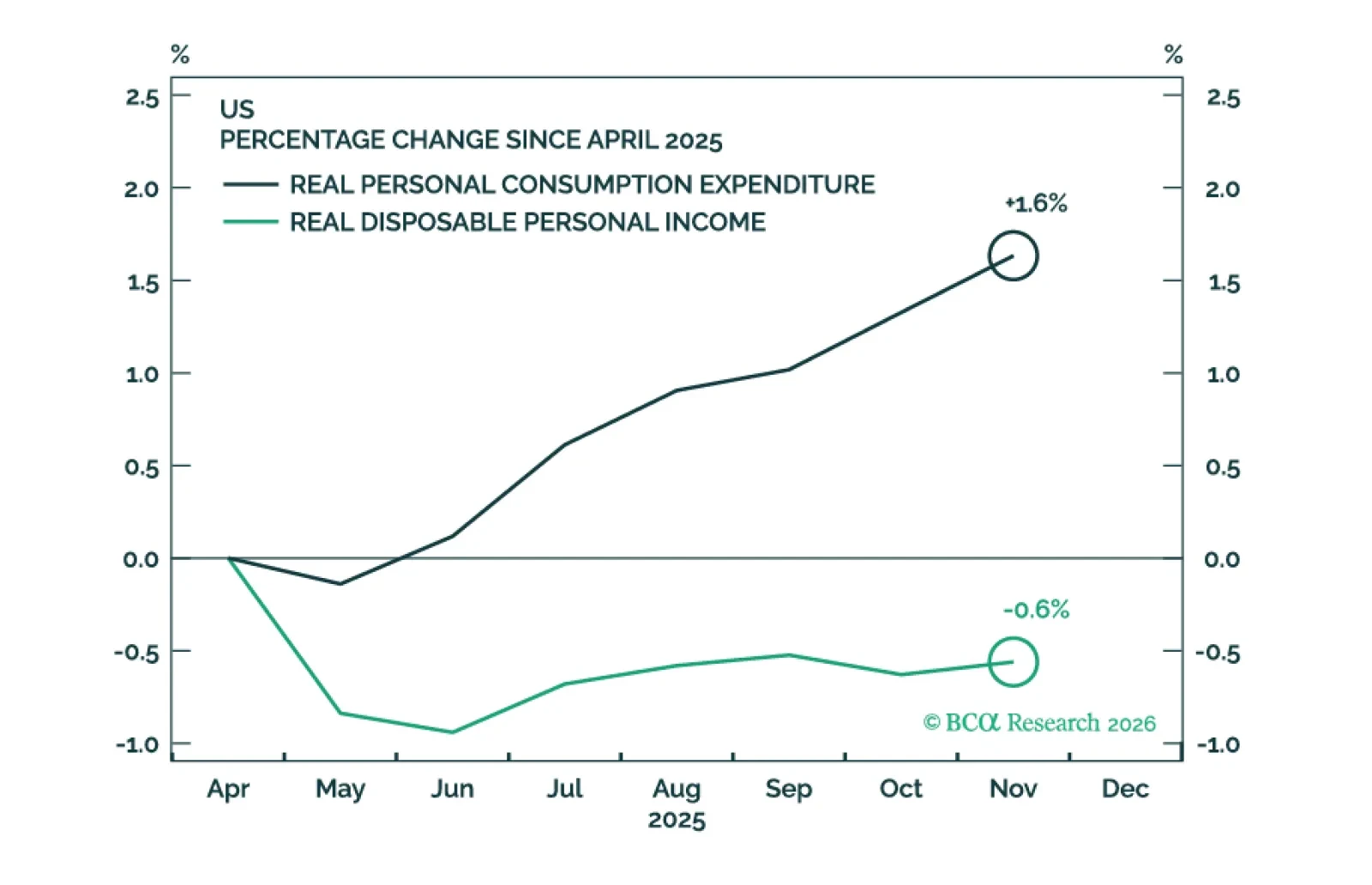

Recent economic data have been reasonably firm. We will cut our 12-month US recession probability to 40% from 50% if the Supreme Court strikes down President Trump’s tariffs. This would take our scenario-weighted year-end 2026 price target for the S&P 500 to 6375 from 6200.

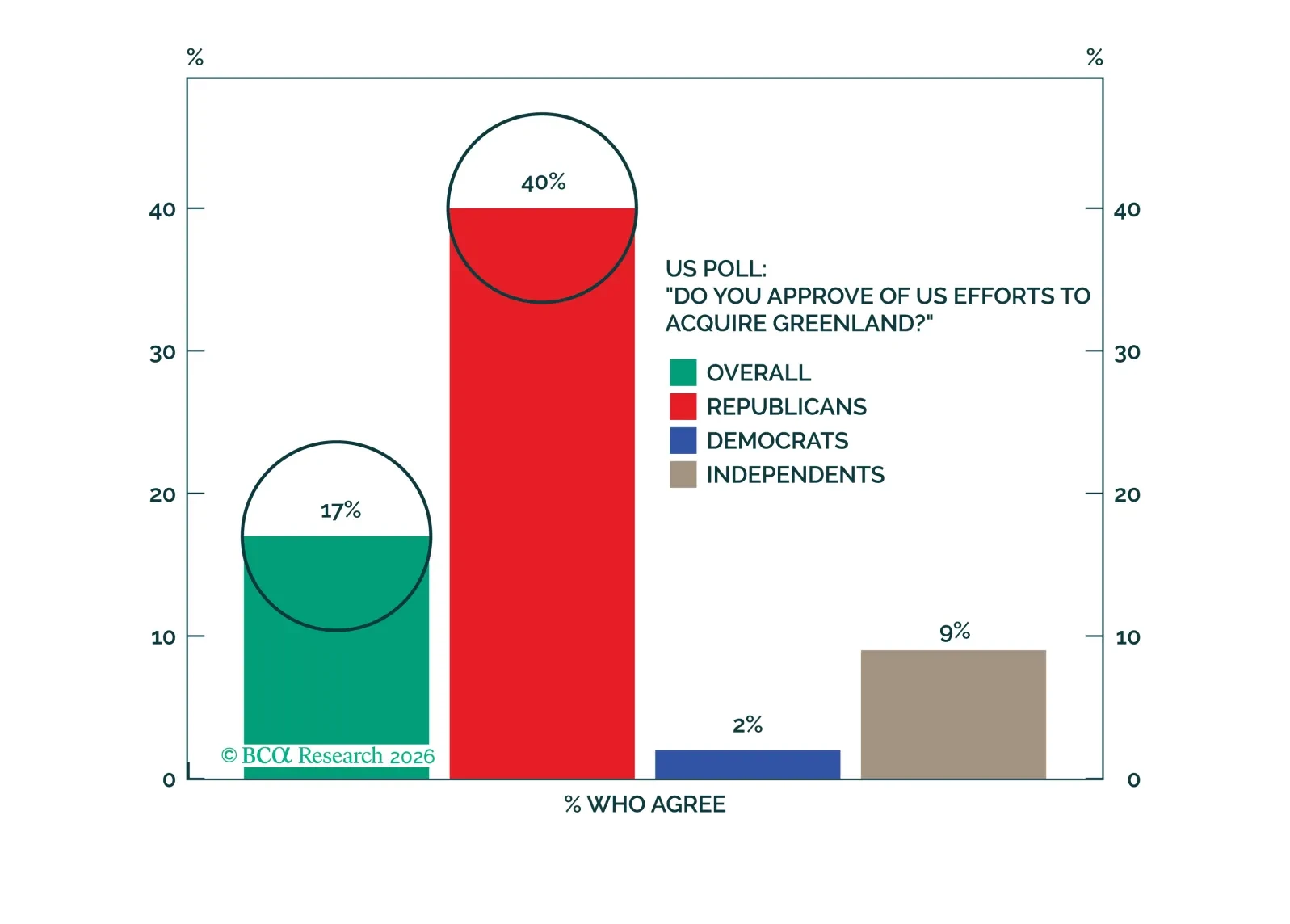

Investors should bet against the US seizing Greenland by force and collapsing NATO. But stay tactically defensive anyway.