Latest from BCA Research

Bears will fold like lawn chairs this summer as traffic returns to Hormuz, allowing markets to overcome seasonal malaise. But we are starting to see how the expansion ends. A macro brew of global central bank tightening due to stickier-than-…

The rally in Colombia’s financial markets has a short shelf life. The election will bring a right-wing government, but it cannot fix inflation, fiscal arithmetic, or balance-of-payments vulnerabilities. Use the near-term rally to downgrade…

Copper prices are surging again after a brief pullback in the first quarter. What is driving the renewed strength, and can it persist?

The US economy is moving back toward Expansion, supported by strong investment, improving earnings, and record margins. We are taking profits on our tactical Software long after achieving our target and rotating into Materials, where commodity…

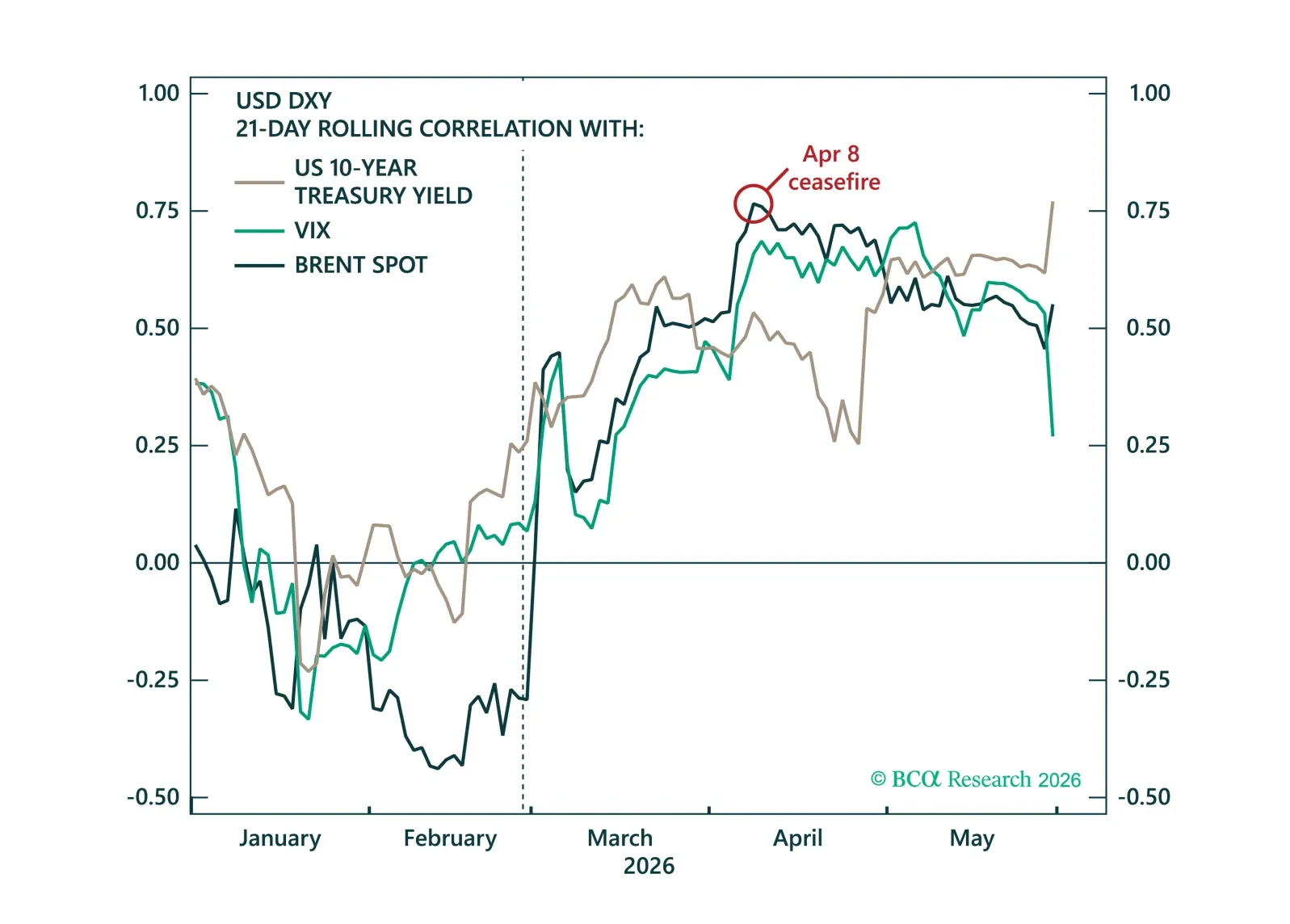

The dollar's muted response to the Iran conflict has led many to question its safe-haven appeal. We argue the opposite – the dollar's defensive properties have returned, while improving growth and rate dynamics should underpin further USD strength…

So far most of the value in the AI supply chain has been captured by hardware companies. However, as model providers shift to usage-based pricing, value will begin to accrue to models and applications. Communications Services and Software should…

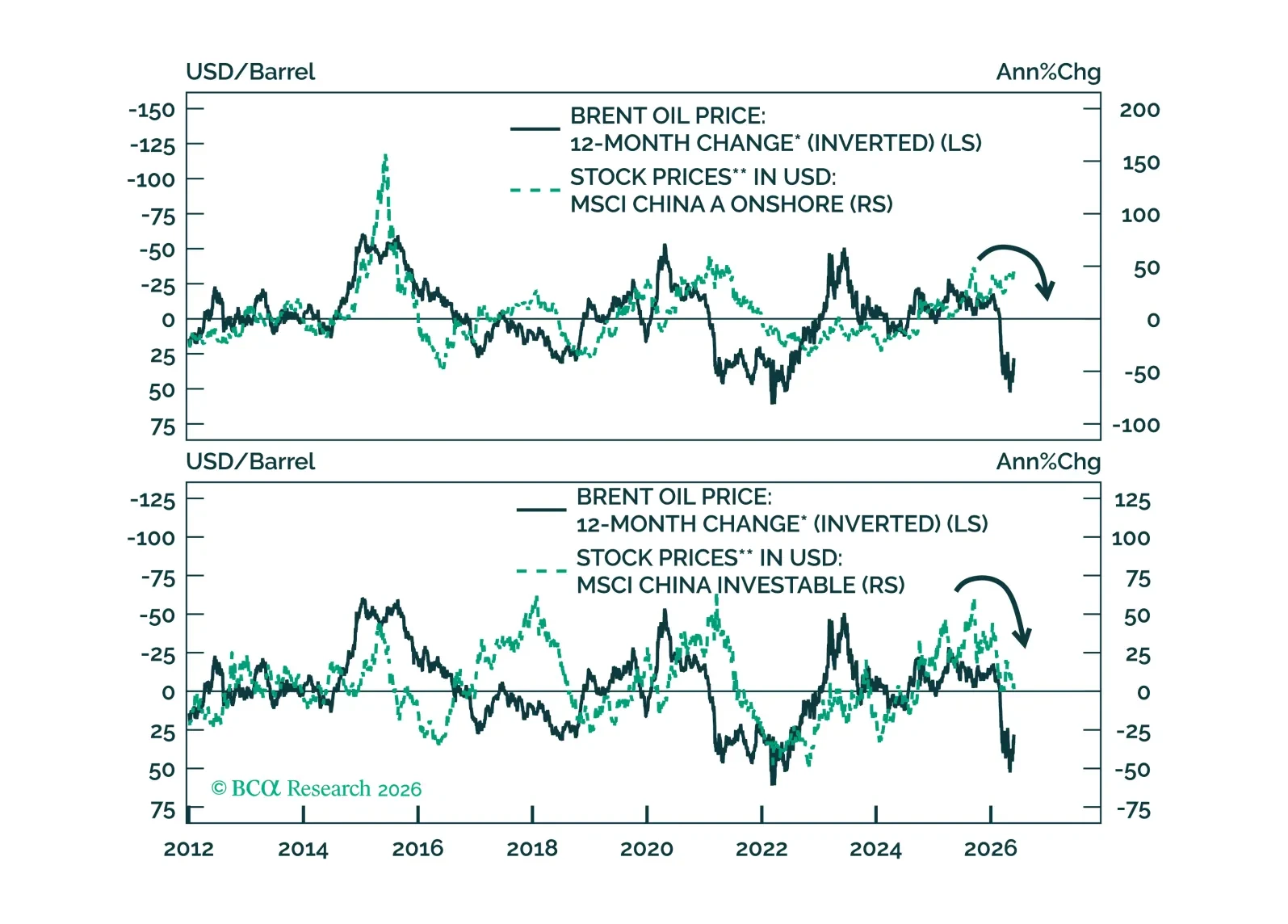

Oil shocks hit economies with a lag. China will feel the delayed pain of surging oil prices, pushing Beijing toward infrastructure spending as its main tool to prop up growth.

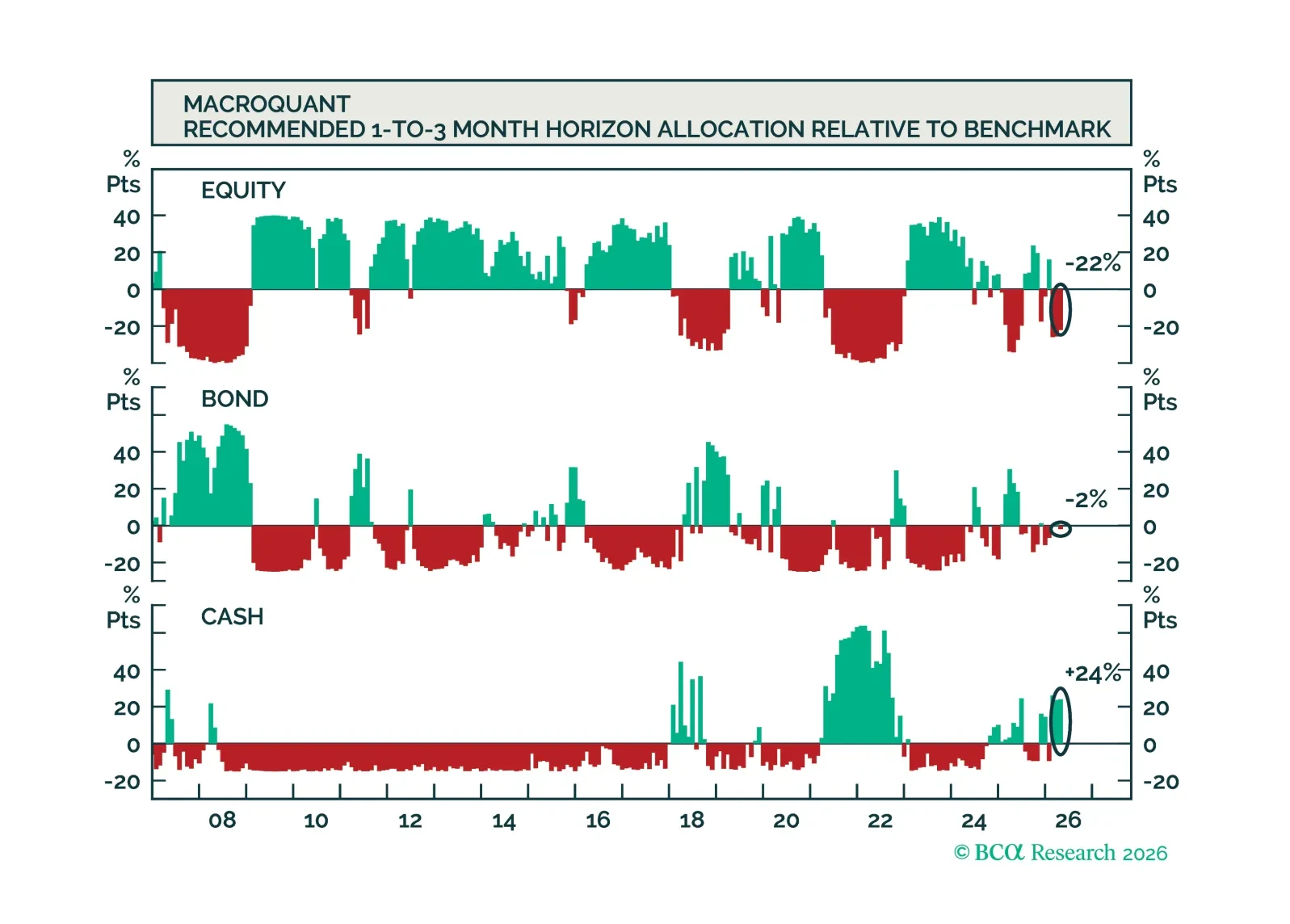

MacroQuant recommends a slight underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is very positive on the US dollar, downgrades gold to underweight, upgrades copper to overweight, and remains…

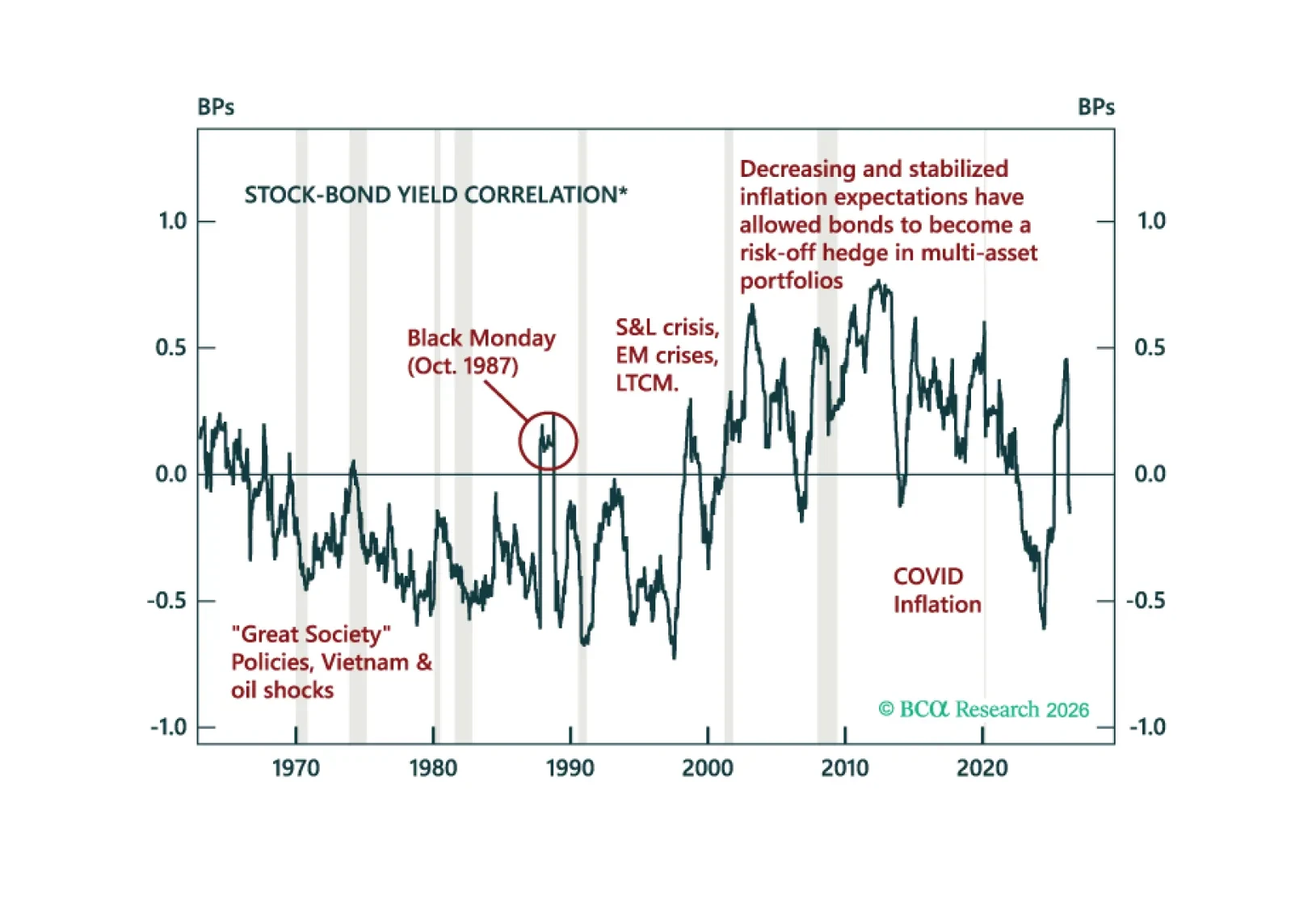

Every market cycle belongs to a longer history. The charts in the BCA Chartbook of Economic & Financial History trace the forces that have shaped economies, markets, and investment regimes across decades. That long view has guided BCA’s work…

The AI bubble is a different type of bubble. It is primarily an earnings bubble rather than a valuation bubble. Like all bubbles, the AI bubble will burst. For now, however, our AI demand indicators do not suggest that this is imminent.