Insights

Access expert research, timely insights, and exclusive webcasts to help you make confident, data-driven decisions.

Macro headlines may have shifted attention away from Private Markets, but the underlying risks remain. We revisit the Private Credit-Software cracks we flagged early and explain why, despite the noise, the structural story is just getting started.

- How did we get here?

- Is Software making or breaking Private Credit's diversification case?

- Systemic risk or a normal credit cycle?

- How are our 2024 calls on Distressed versus Buyouts playing out?

- Where are the most overlooked opportunities across Private (and Public) Markets right now?

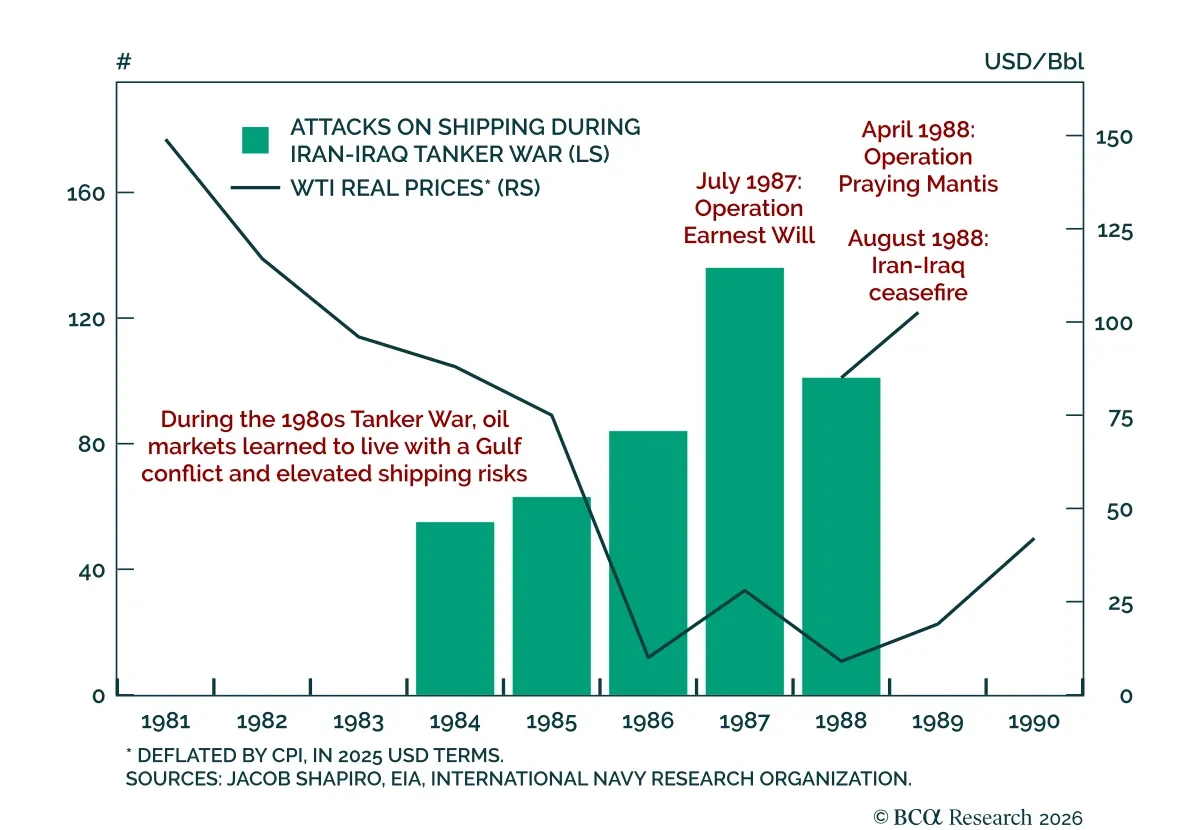

Marko Papic, Matt Gertken, and Roukaya Ibrahim look at the latest developments in the Strait of Hormuz and the implications for global financial markets.

Topics discussed:

- Will the US-Iran ceasefire hold? What should investors monitor to determine whether it is failing?

- How long will it take for energy flows and shipping to improve significantly? What would cause a relapse?

- Will the disconnect between financial markets and the real economic impact prove lasting or significant?

- How should investors position for the future evolution of commodity markets and commodity-linked assets?

- What other market dynamics will emerge and will Hormuz remain the central global focus?

Juan discussed:

- What are the consequences of the current oil shock to the global economy?

- How will policy makers respond to this shock?

- What indicators should investors be looking for a resolution?

- What indicators should investors look for to get more positive on equities?

- What are the long term consequences of the war?

BCA美国政治与地缘政治副主编马语书的中文网络直播:《地缘政治与美国政治二季度展望》。

- 伊朗冲突接下来将如何演变?当前的暂时停火能持续多久?

- 特朗普的约束与承受阈值在哪里?

- 中期选举将如何影响美国的外交政策决策?

- 中东的地缘政治紧张局势是否可能进一步扩散?对其他地区有何影响?

- 持续的地缘政治风险和政策不确定性,对投资有何启示?

In this webcast, BCA Research Chief Strategists, Mathieu Savary, Robert Timper, Jeremie Peloso and Artem Sakhbiev discussed the following:

- Oil: Temporary buffers are masking a looming oil deficit that could trigger a global recession.

- Inflation: The shock is stagflationary, but weaker labor markets limit second-round inflation risks.

- Policy: Central banks are likely to look through inflation short term, then pivot to growth concerns.

- FX: Terms-of-trade dynamics favor USD and commodity exporters over energy importers.

- Markets: Bonds offer asymmetric upside; equities and FX remain driven by energy exposure and policy repricing.

US Equity Strategy Webcast Series: Noah Holds Barred - Episode 1

Noah and Jason discussed:

- The foundations of our constructive outlook and 7700 year-end S&P 500 target

- The capex outlook and its implications

- Do valuations represent a meaningful constraint?

- Tensions and opportunities between market pricing and the state of the cycle

- What a US recession could mean for equities

- Middle East tensions: potential paths to resolution and market implications

- Sector positioning for 2026