Insights

Access expert research, timely insights, and exclusive webcasts to help you make confident, data-driven decisions.

Insight

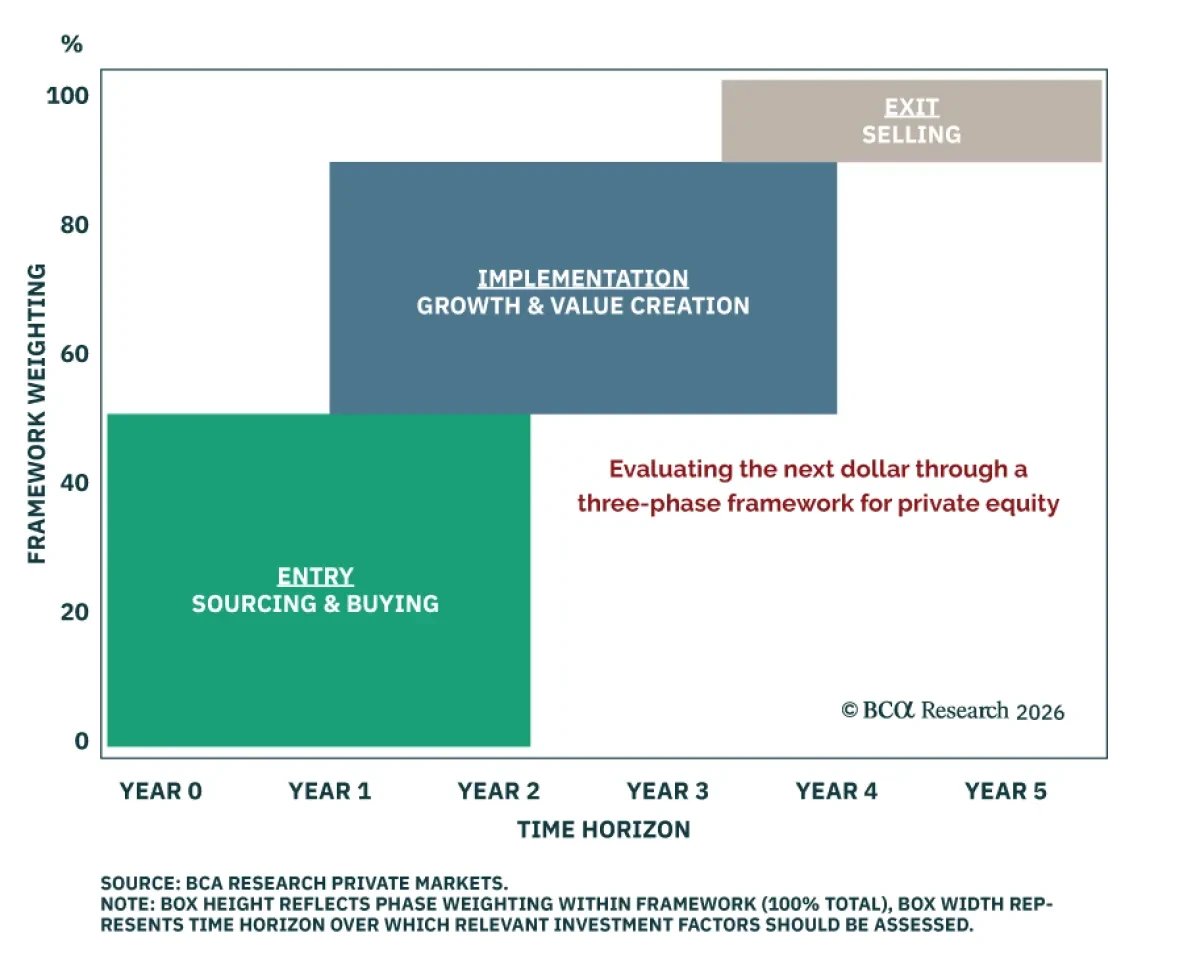

Our Private Markets & Alternatives strategists laid out a framework for evaluating private equity investments. While fund vehicles often last more than ten years, the assets they contain are held for much shorter periods; and it is those shorter periods that drive returns. Closed-end funds can r...

Read more

Insight

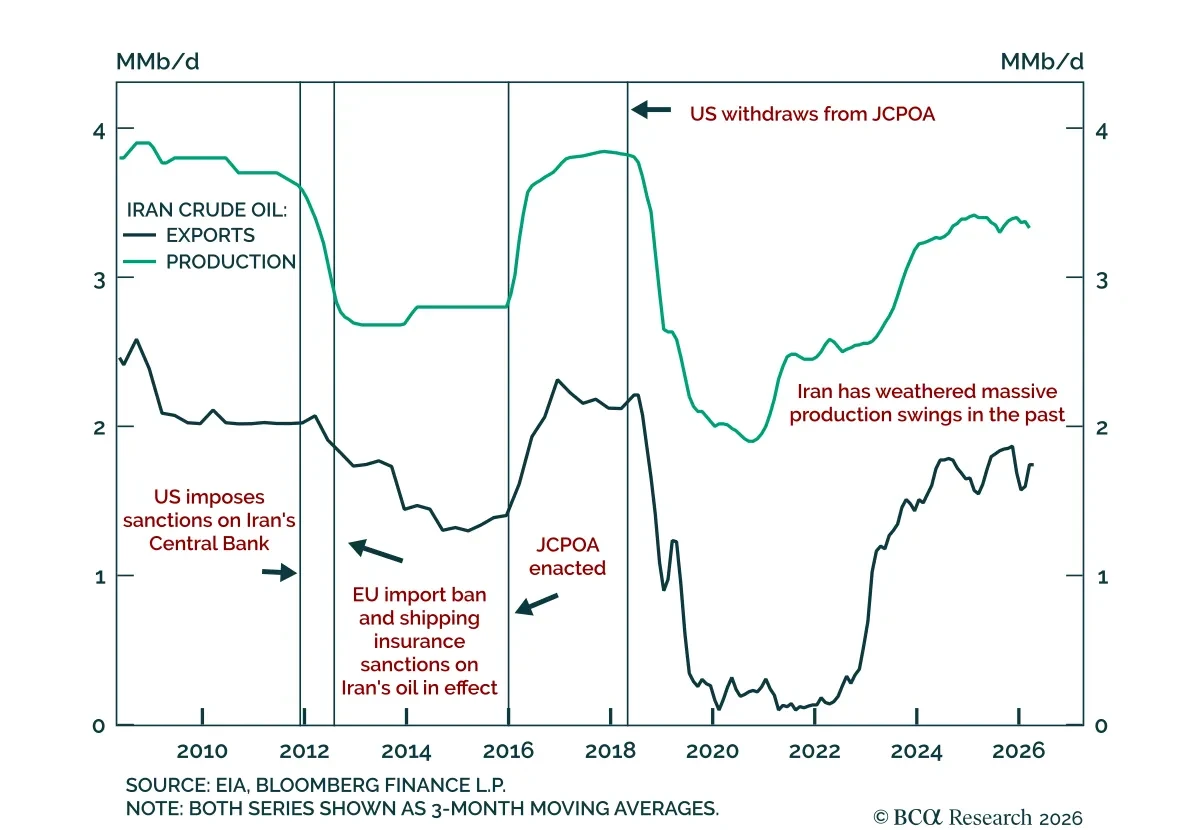

Our Commodity strategists expect oil prices to move higher as de-escalation hopes fade and Strait of Hormuz supply risks reassert themselves. Recent volatility reflect headline-driven uncertainty, with markets swinging between prospects of an imminent Strait reopening and fears of ceasefire breakdow...

Read more

Insight

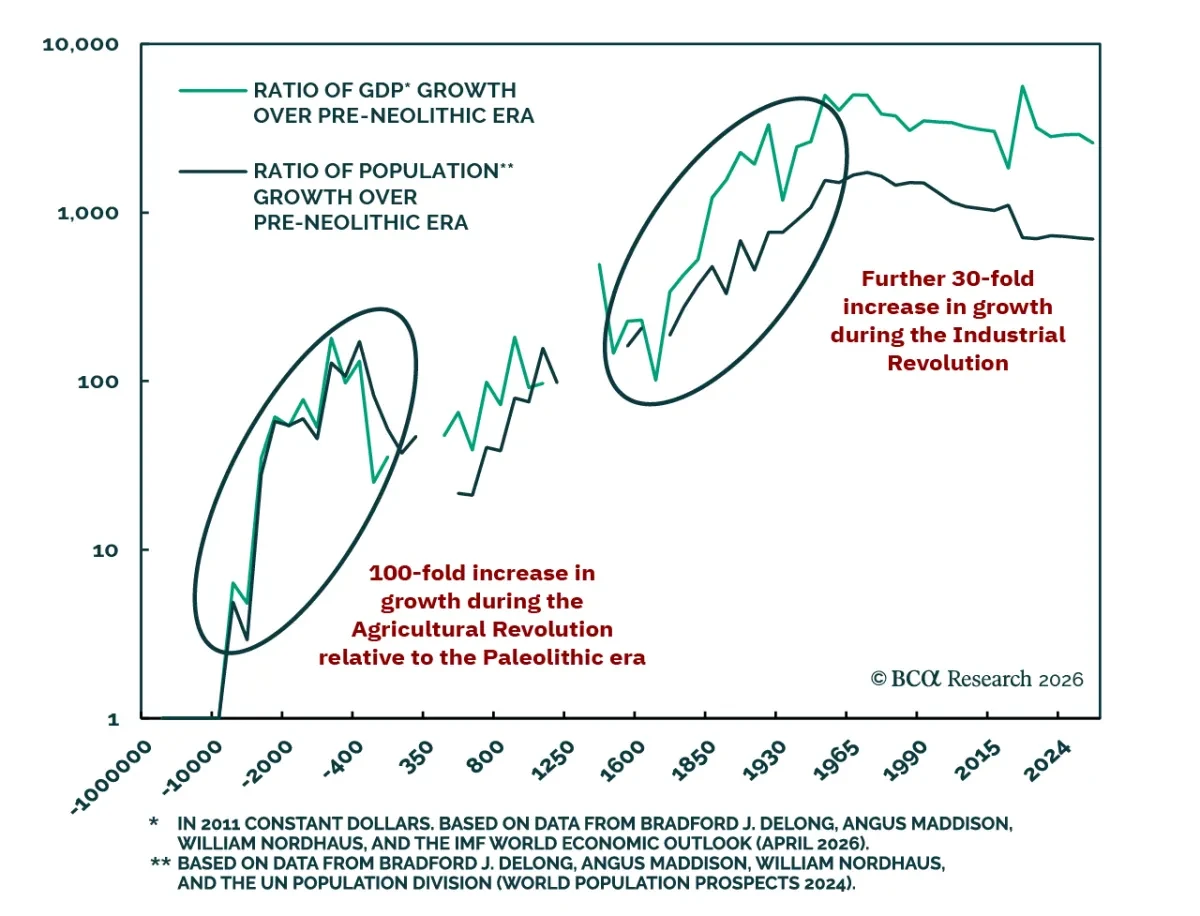

Our Global Investment strategists argue that AI could be as transformative as the Agricultural or Industrial Revolutions, but carries existential medium- to long-term risks. Both prior revolutions lifted GDP growth more than 30-fold versus the preceding epoch, and AI may prove similarly powerful.&nb...

Read more

Insight

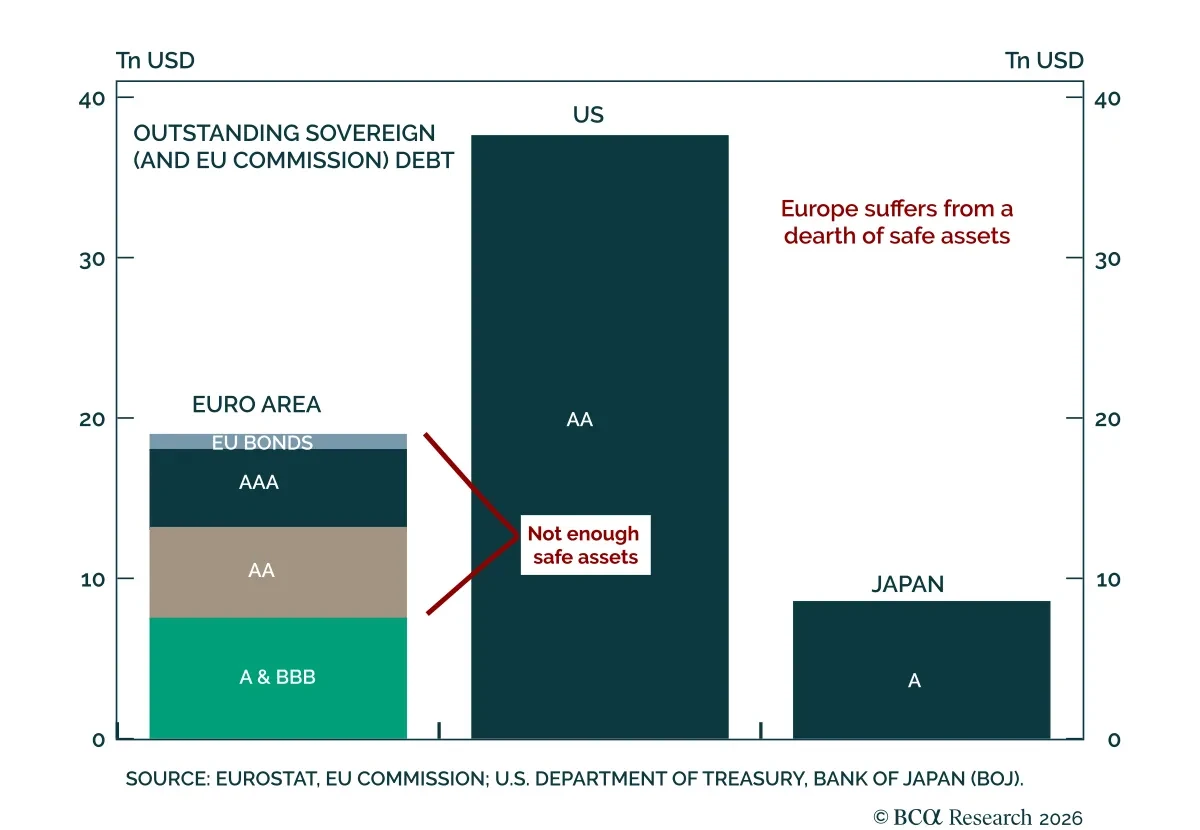

Our DM ex-US strategists make the case for the Eurobond as a structural necessity. The ECB has expanded EUREP (its global euro liquidity facility) to lay the groundwork for currency internationalization, but liquidity infrastructure without a deep pool of risk-free collateral achieves little. Euro-d...

Read more

Insight

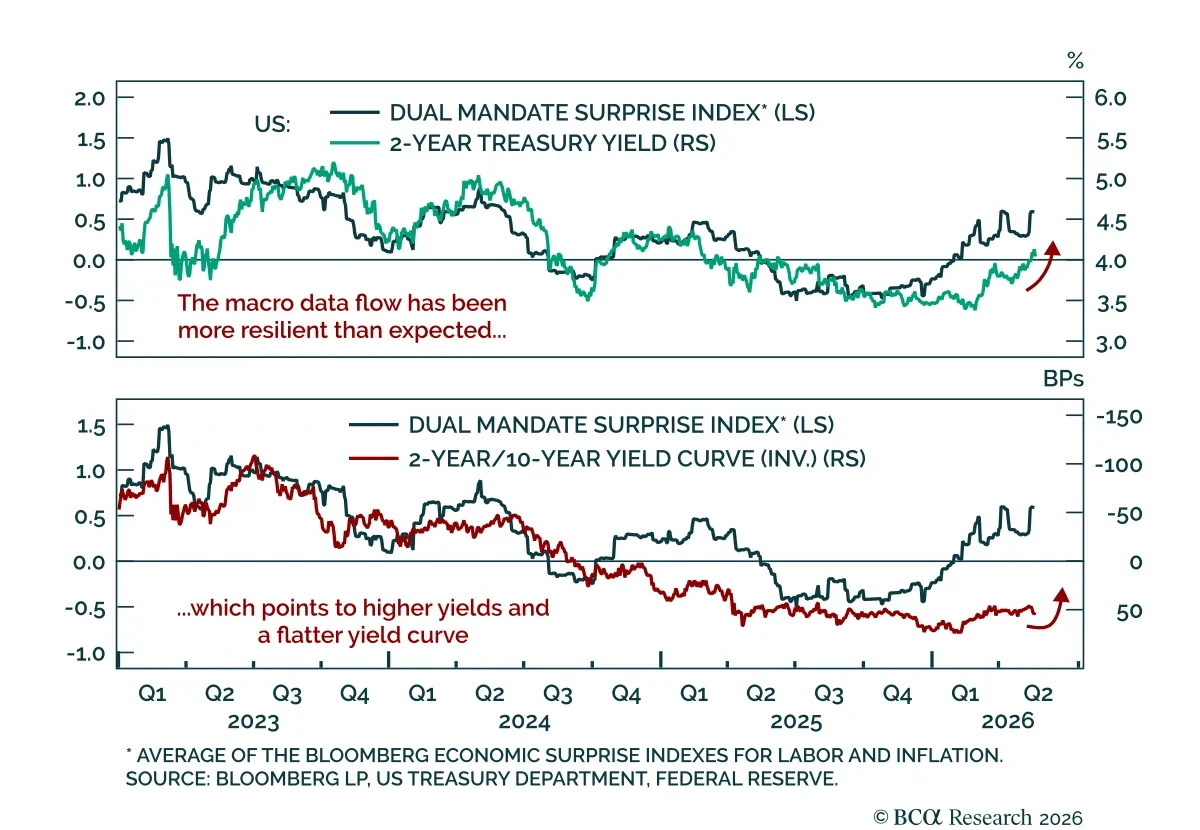

The April FOMC minutes clarified the hawkish shift that marked the meeting. The Fed held at its last meeting, but there were four dissents. While Governor Miran favored a 25 bps cut, regional presidents Hammack, Kashkari, and Logan supported a hold but voted against the easing bias in the statement....

Read more

Webcast Replay

Chief Strategists Matt Gertken and Roukaya Ibrahim and Jesse Kuri discussed:

- Presidents Trump and Xi Jinping agreed to expand their trade truce, as both face challenges, not least in the Strait of Hormuz.

- But China is not yet willing to apply pressure on Iran to enable shipping to resume in the strait. Only the US and Iran have the physical power necessary to resume shipping.

- Trump's attempt to negotiate a quick deal with Iran has not borne fruit, though negotiations are not yet dead.

- Faltering diplomacy implies a new round of hostilities over the coming days and weeks.

- Hormuz is likely to remain shut and attacks will likely increase over the coming month.

- In late June the world will start to hit constraints from physical oil inventory drawdowns.

- The global economy will increasingly see demand destruction as a result of elevated commodity prices.

- Global financial markets are increasingly disconnected from the underlying threat to the economy.

Webcast Replay

Jeremie and Robert discussed:

- Has the energy shock caused irreversible damage to the European economy?

- Central banks so far refrained from hiking. Will they continue to stay put?

- How is the energy shock affecting Europe relative to the US? What are the equity, fixed income, and currency implications?

Webcast Replay

In this webcast Ryan discussed the outlook for US inflation and consider whether rising consumer prices will force the Fed to hike rates in the coming months. The Webcast addressed the following questions:

- Will the oil price shock have only a temporary impact on US inflation, or will it send consumer prices sustainably higher?

- Is the US labor market heating up or cooling off?

- What economic scenarios would push the Fed toward rate hikes or rate cuts?

- Which US fixed income sectors stand to profit from an extended period of on-hold Fed policy?

Webcast Replay

Chief Strategists Marko Papic, Matt Gertken and Roukaya Ibrahim discussed:

- President Trump heads to China this week for critical talks with Xi Jinping that will focus on the war in Iran and global stability.

- If the US cannot offer significant strategic concessions for China's sphere of influence, then China may not join the pressure campaign against Iran.

- Meanwhile the "kinetic equilibrium" in the Persian Gulf faces renewed threats as the US and Iran trade barbs over how to restart shipping.

- The good news is that both sides are trading proposals — and the number of attacks has tended to decline since the April ceasefire.

- The bad news is that Iran remains unwilling to abandon its nuclear program, the US maintains its blockade, and Iran will attack US naval escorts of commercial ships.

- What will come of the US-China talks? Will Iran and the US manage to restart shipping? Can global financial markets continue to weather the Hormuz shock?

Webcast Replay

Please join BCA Research Strategists, Matt Gertken, Yushu Ma and Jesse Kuri for a Webcast on the US Midterms.

Wednesday, May 13

10:30 AM EDT | 3:30 PM BST |4:30 PM CEST

- Midterm elections occur every four years and thus constitute a normal risk, not significant uncertainty.

- But the midterms matter this year because they constrain the Trump administration's foreign policy, which threatens the global economy.

- The midterms will also act as a barometer on US public opinion and the likelihood of another massive reversal of national policy in 2028.

- We revised our quantitative election models to give a read on what range of outcomes to expect for the House and Senate.

- With this information, investors can begin to envision the next twists and turns in market-relevant US policy.

- We will also discuss President Trump's "lame duck" status after the midterms and the investment implications.