UK

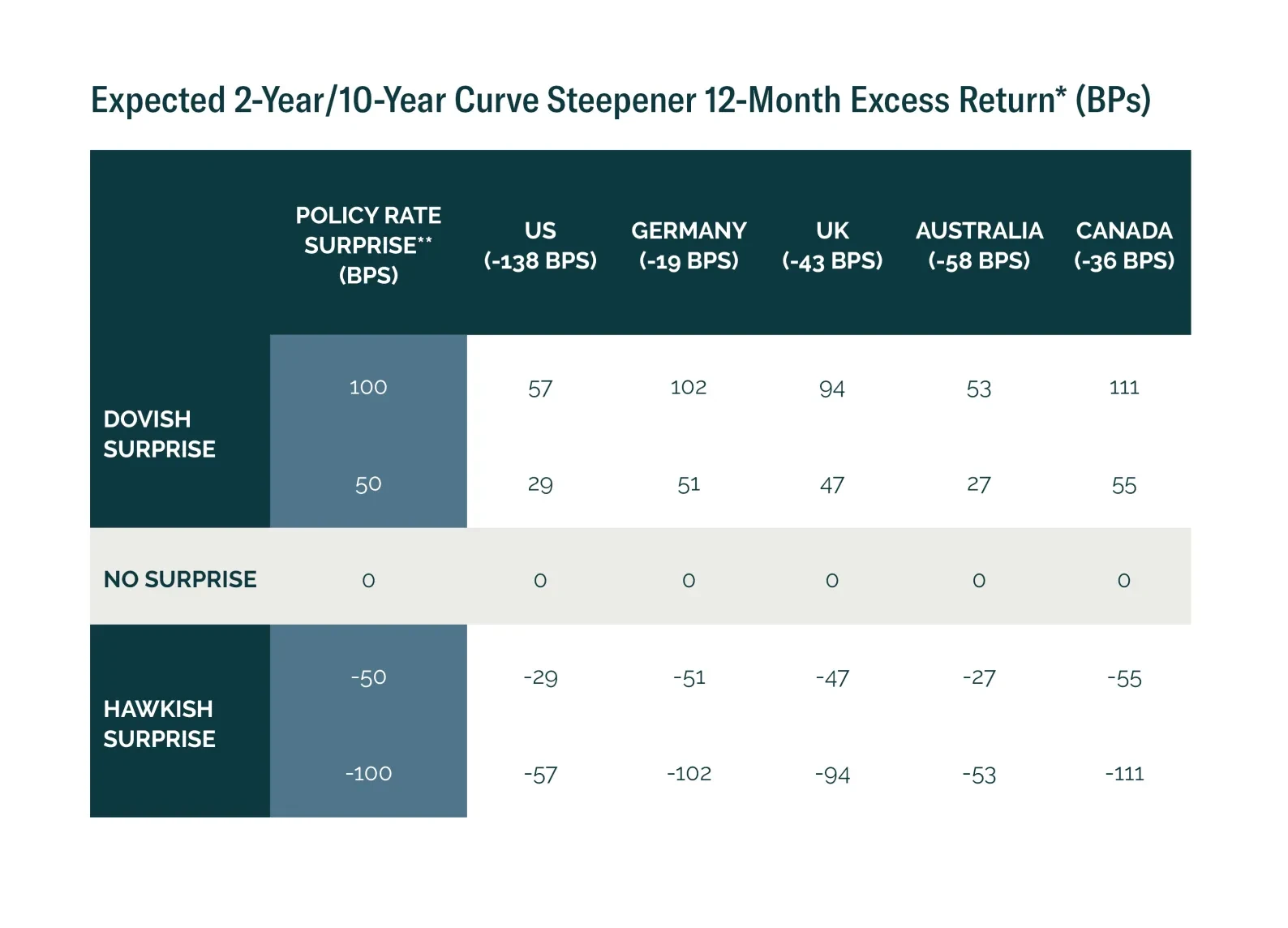

Monetary policy surprises shape curve trade returns. We show where steepeners and flatteners offer the best risk-reward in today’s market.

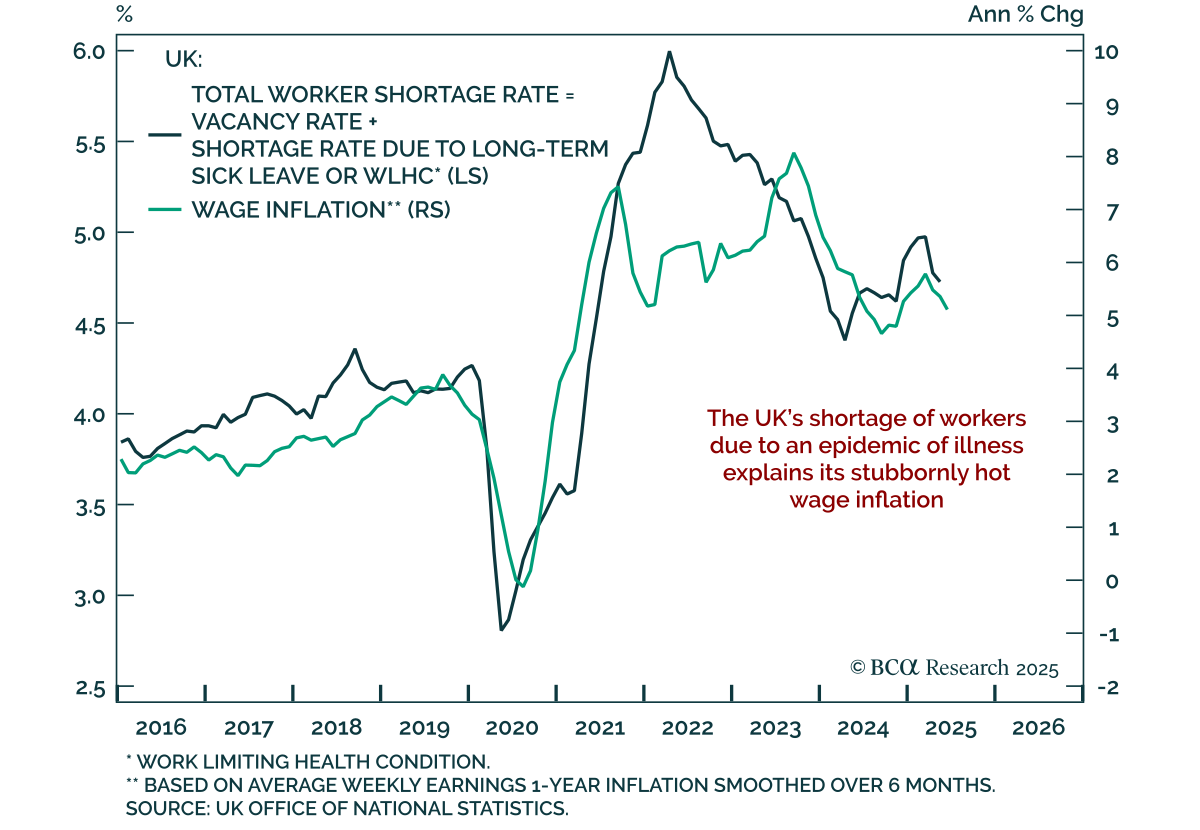

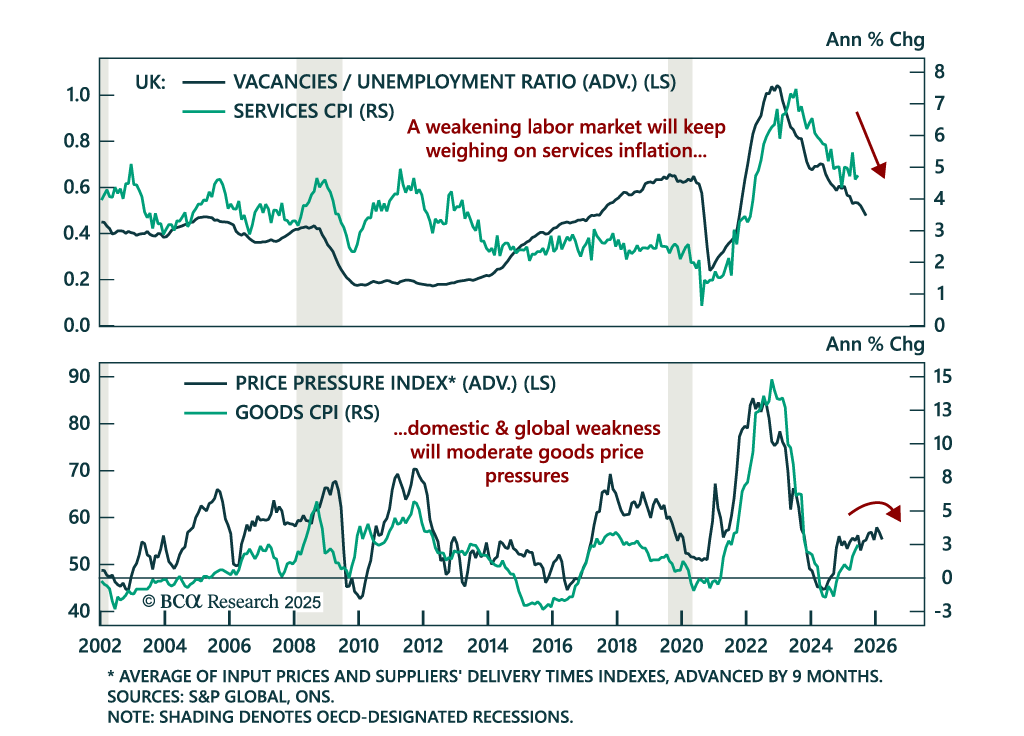

A surge in UK employees on long-term sick leave or with a work limiting health condition explains stubbornly high UK wage inflation. This leaves the Bank of England and the UK government with some tough choices to make in the months ahead. Plus, a new tactical trade is short CSI 300.

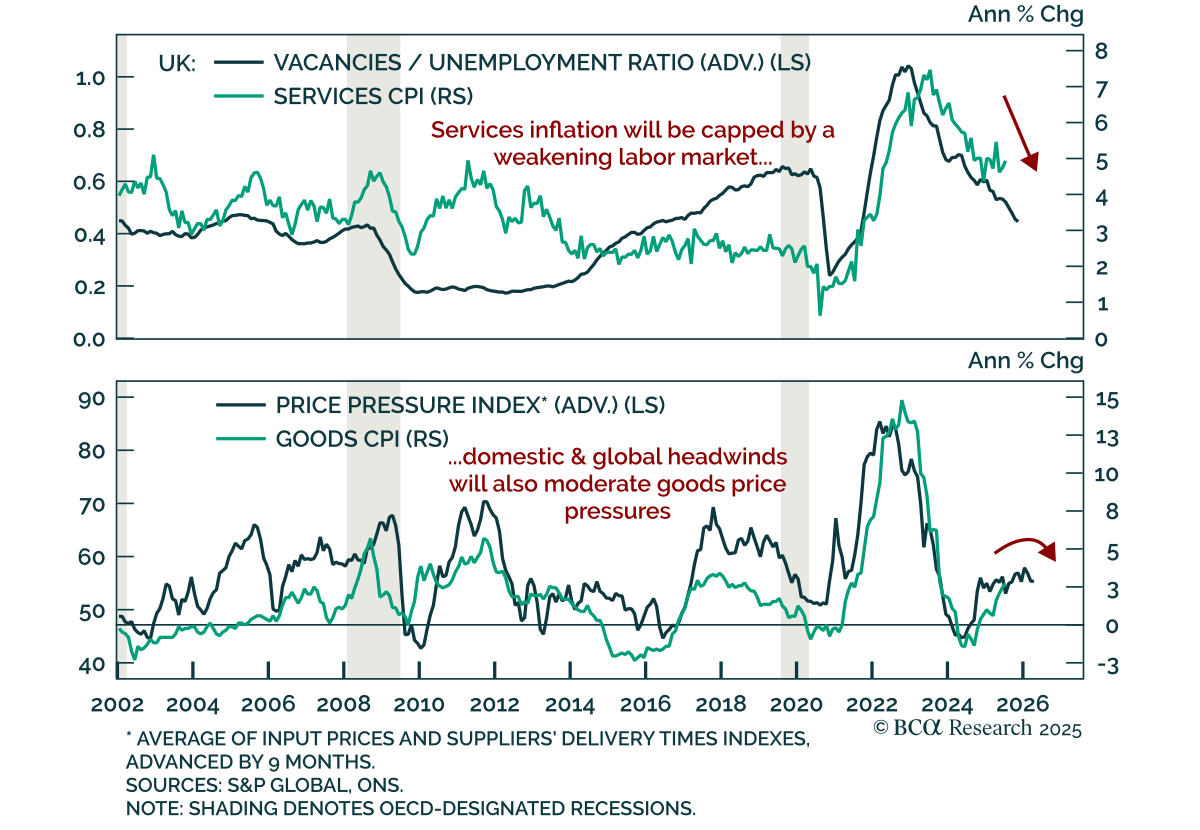

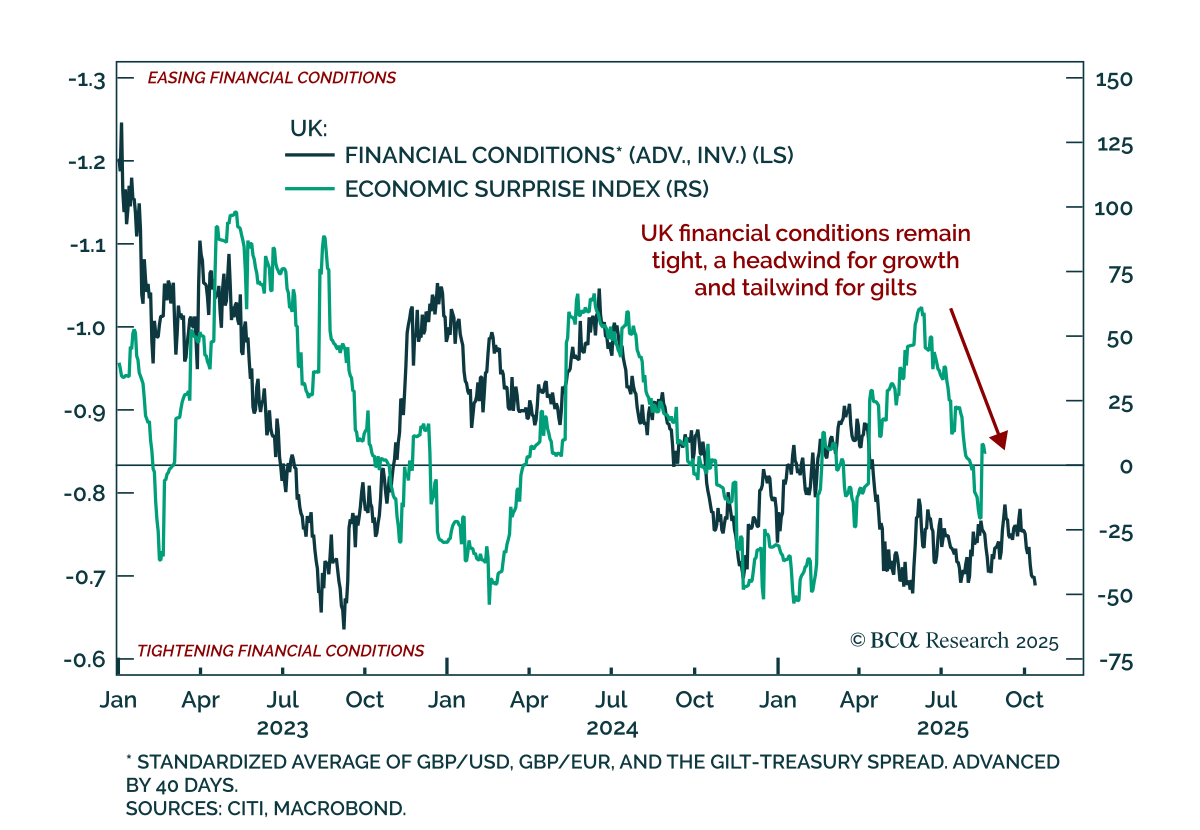

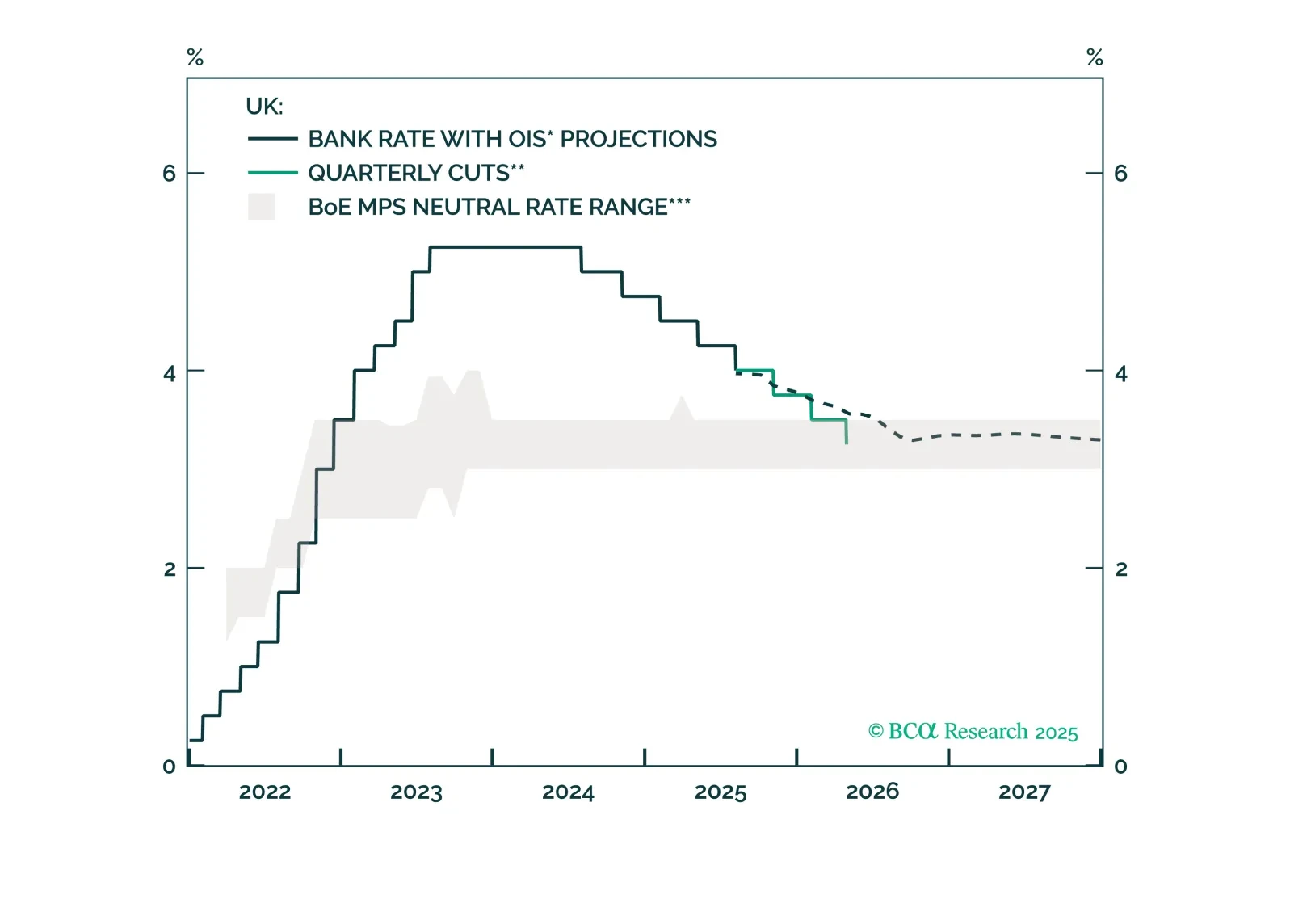

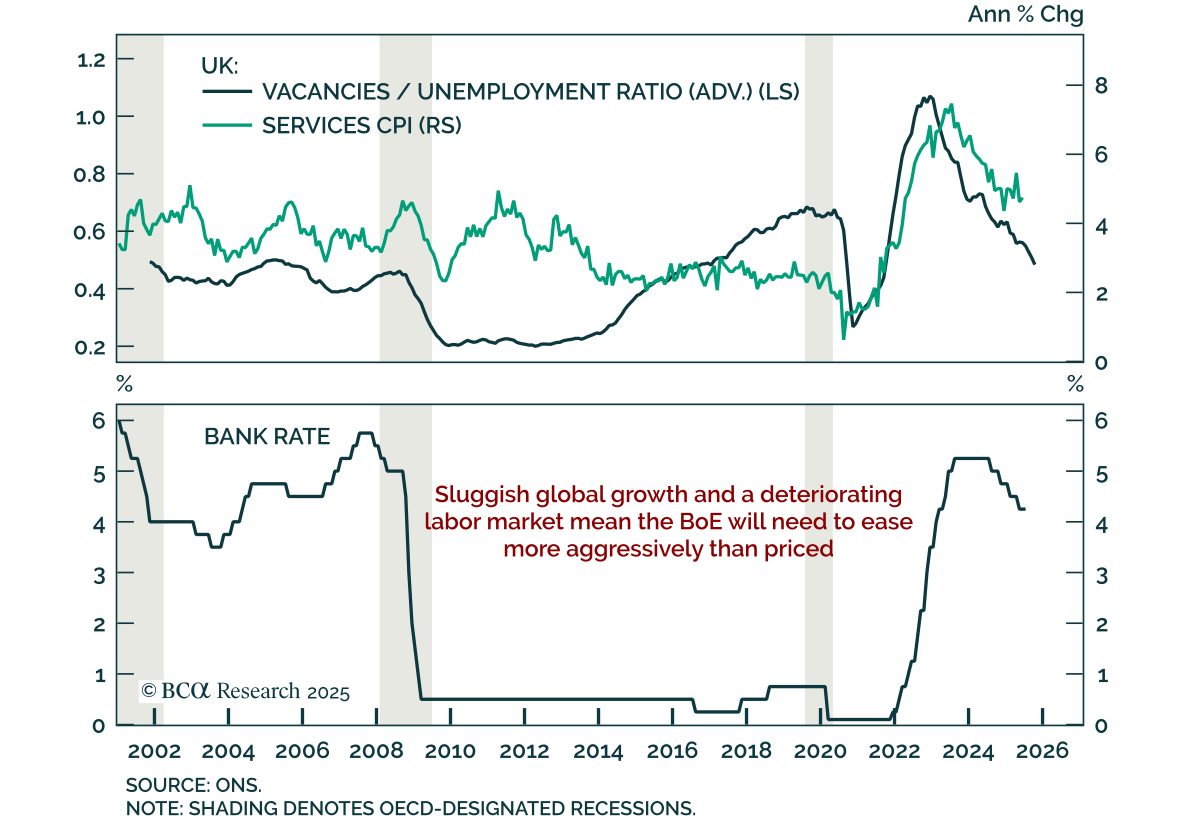

The BoE is easing, but risks falling behind. Labor and growth cracks are starting to emerge, and the Bank may soon be forced to move more decisively. This report outlines why gilts remain a buy and sterling’s path is diverging vs. USD and EUR.

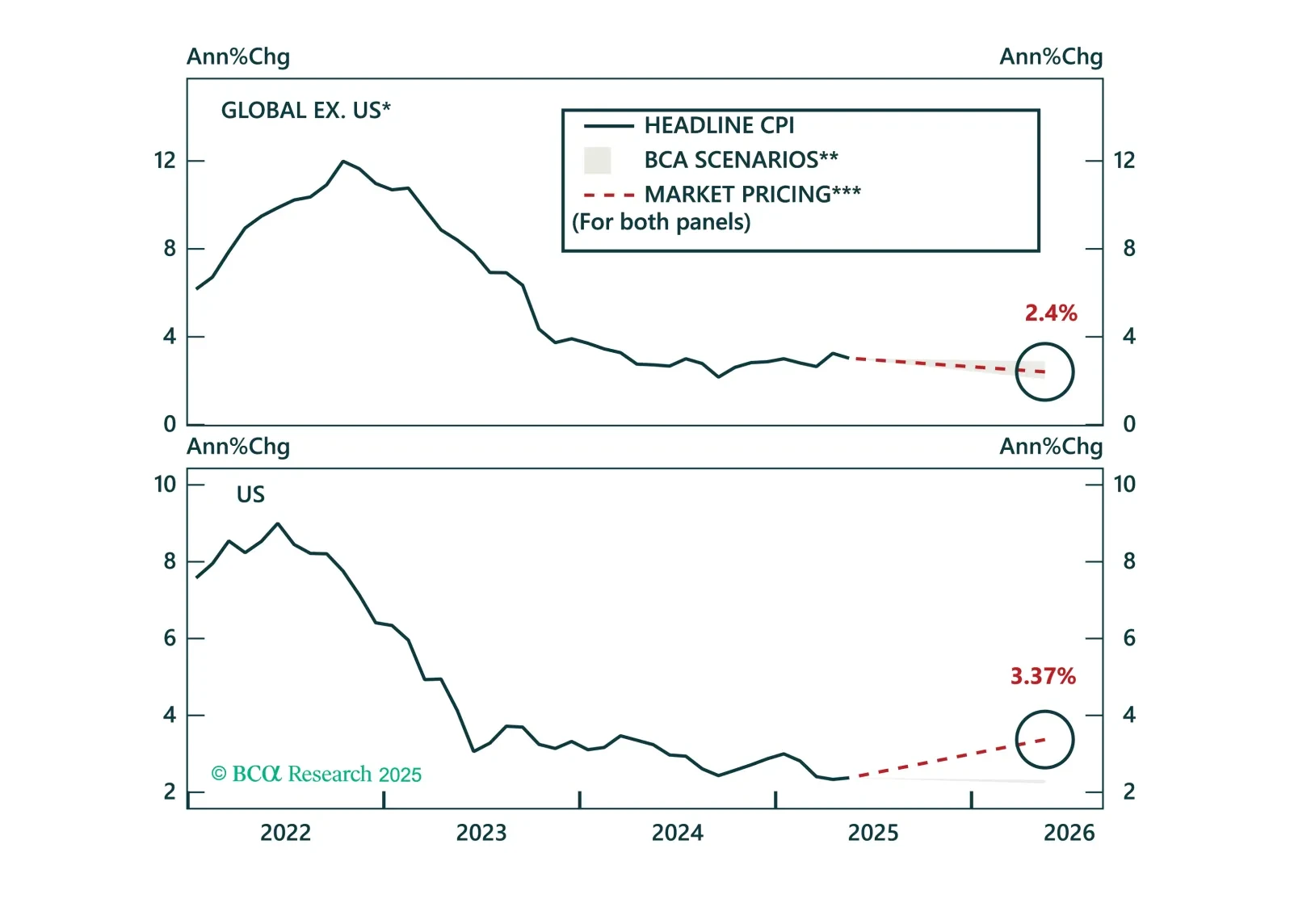

Disinflation continues to unfold globally, and markets are finally catching up. Inflation expectations have broadly realigned with fundamentals, prompting us to shift our global ILB allocation to neutral. While tariff risks are inflating US expectations, pricing in the UK, Japan, and Australia has adjusted sharply. Today’s Strategy Report reviews these developments and updates our country-level ILB positioning.