Developed Countries

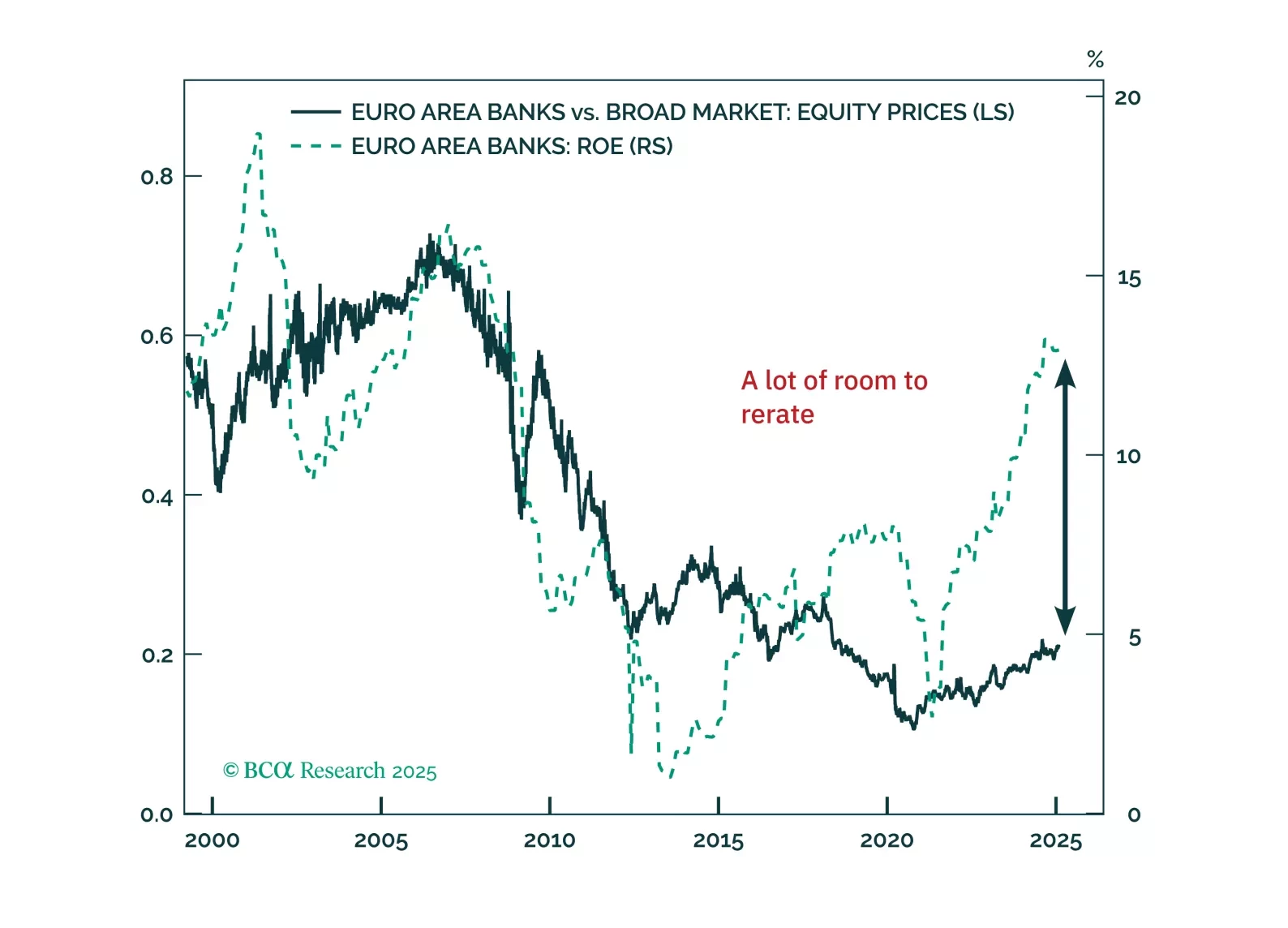

Eurozone banks have quietly outpaced the Magnificent 7—can they keep winning? With strong balance sheets, rising profitability, and structural tailwinds, European lenders still offer value despite short-term risks. Meanwhile, German equities continue to defy expectations, but is a near-term pullback on the horizon?

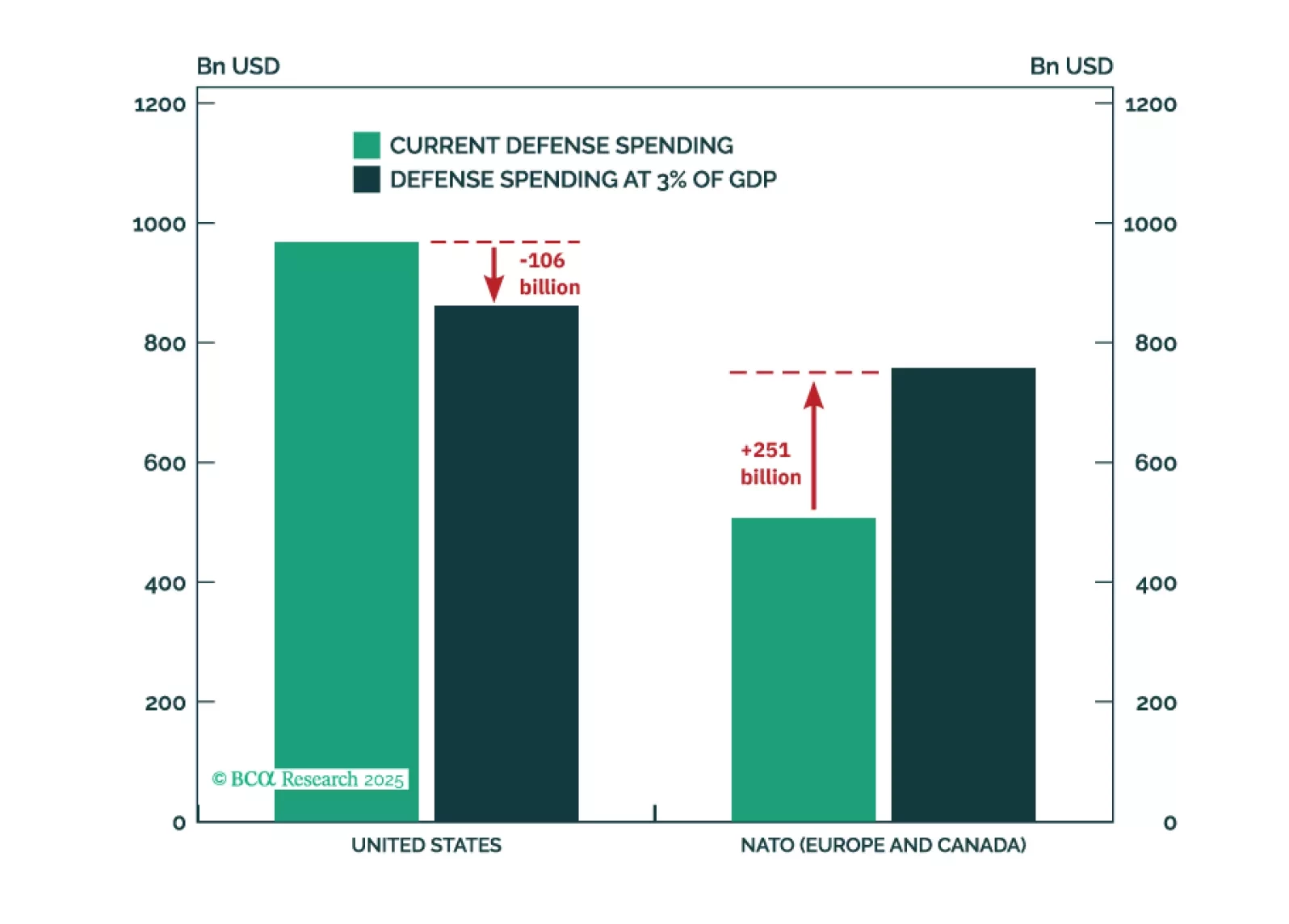

The Trump administration posits that the world owes the US for the provision of its security. In this report, we perform a quantitative analysis to come up with a naïve estimate of the cost of that peace. More importantly (and more seriously), our qualitative assessment argues that save for a number of frontline countries that rely on the US defense umbrella, the vast majority of the world faces manageable security threats due to the complex multipolar global environment and a growing number of alternatives to the US security blanket.

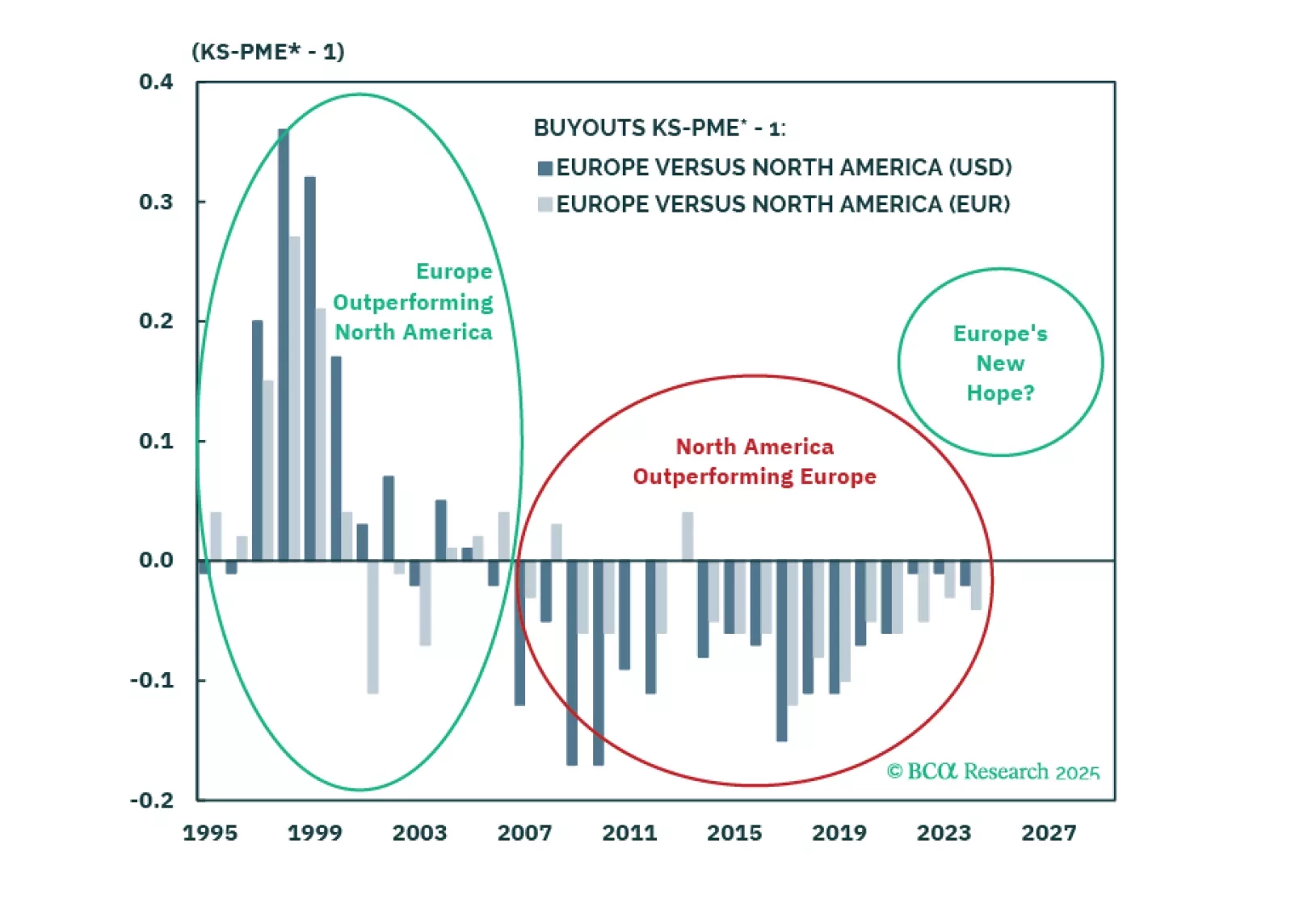

We are at a pivotal moment for Europe, supported by structural reforms and macro catalysts. While expanding credit markets and lower rates favor Private Equity over Private Credit, opportunities vary by segment. Large+ Buyouts are attractive as markets have priced in structural challenges. We downgrade Europe Private Credit, remain neutral on Europe Private Equity broadly but overweight Europe vs. North America in PE portfolios.