Fiscal

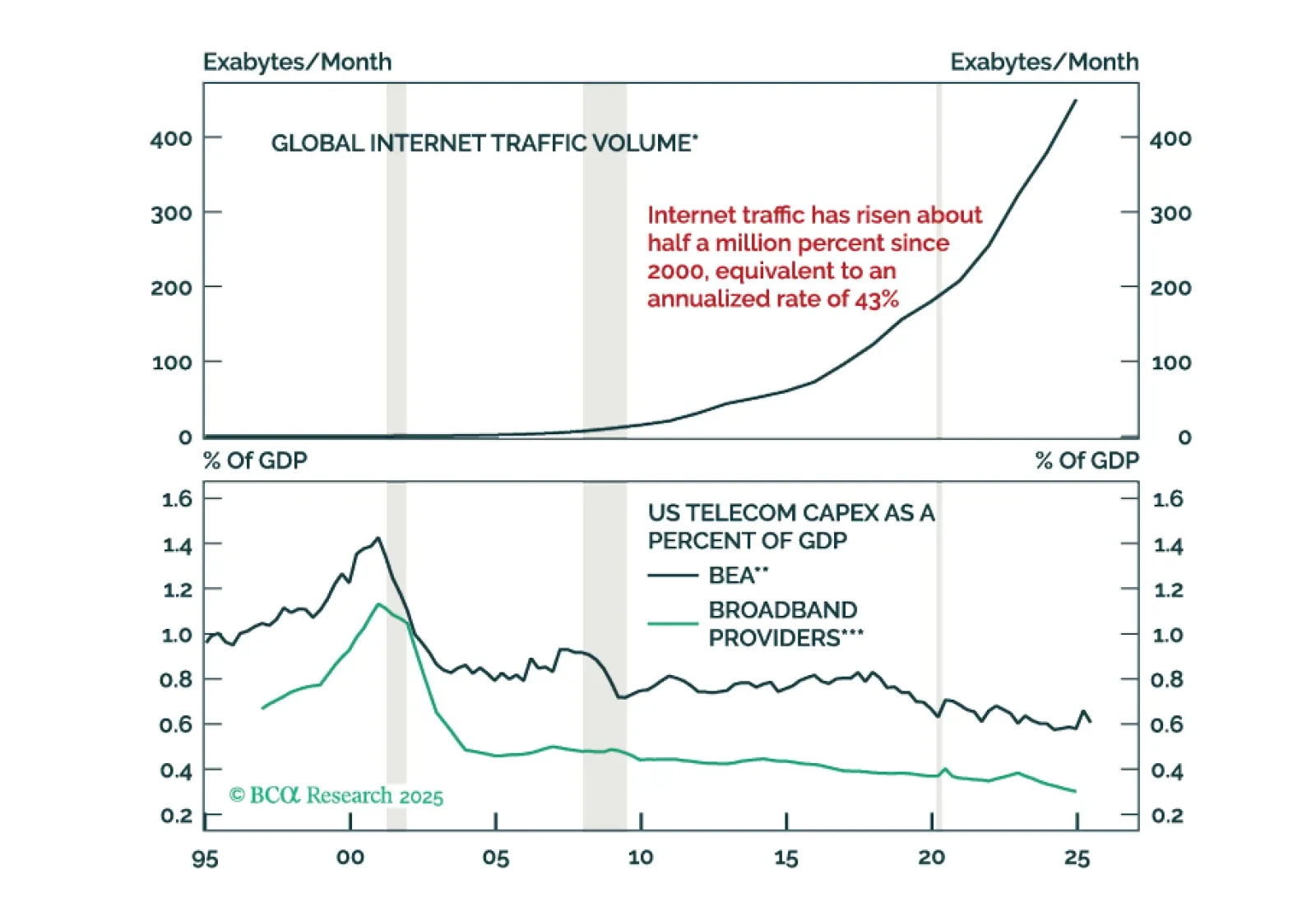

As long as the AI boom keeps booming, all other investment considerations will remain on the back burner. However, if the AI trade fizzles, this would expose deep-seated problems within the global economy, which could very well lead to an economic downturn as early as next year.

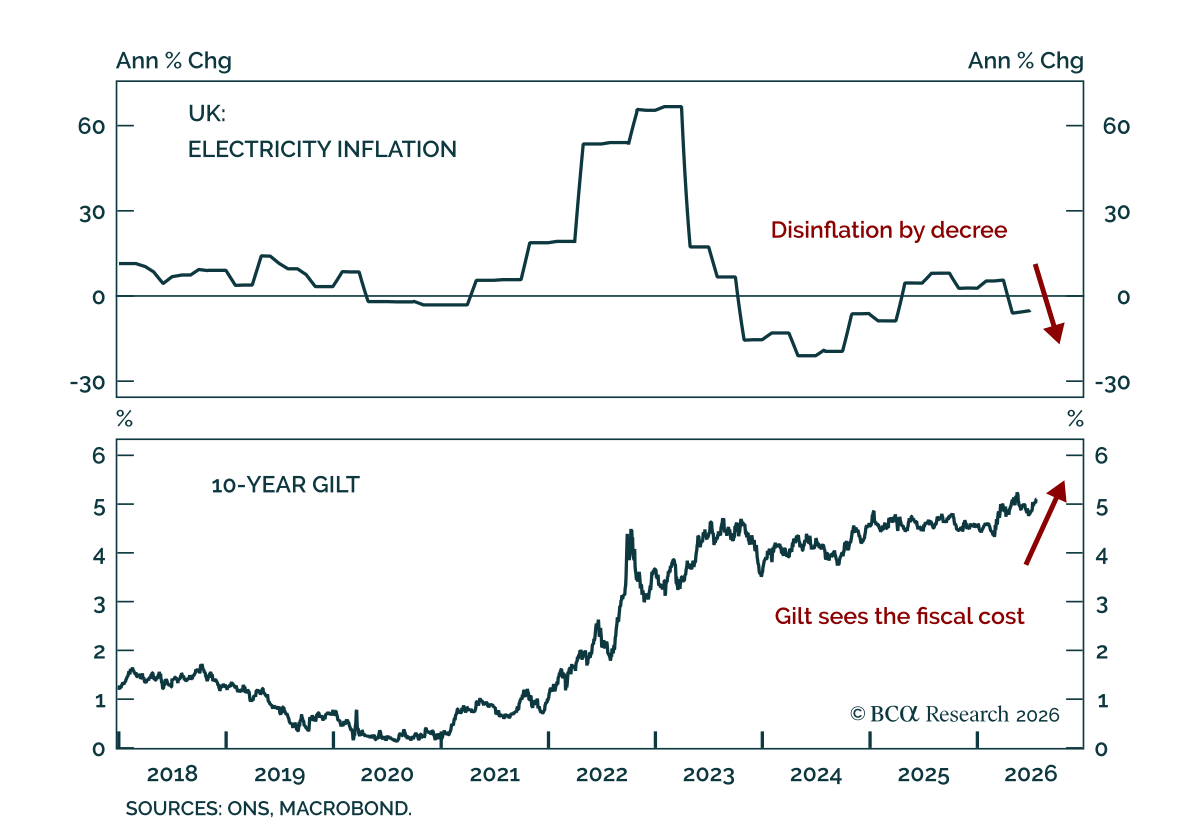

The UK economy is becoming increasingly fragile, but the investment outlook is improving. Slower growth and a more dovish BoE will support gilts, while UK equities will likely benefit from a favorable sector mix and a weaker pound.

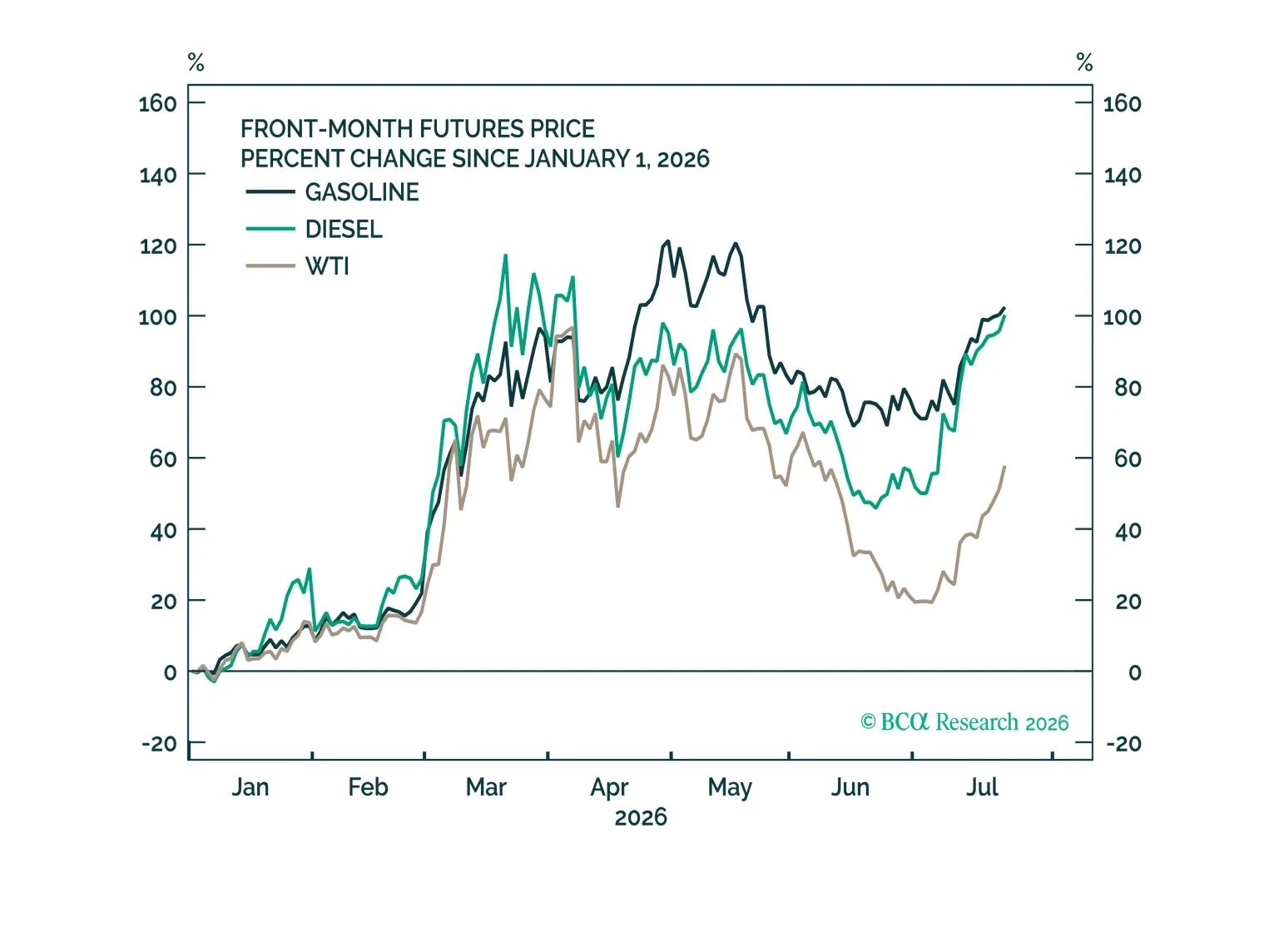

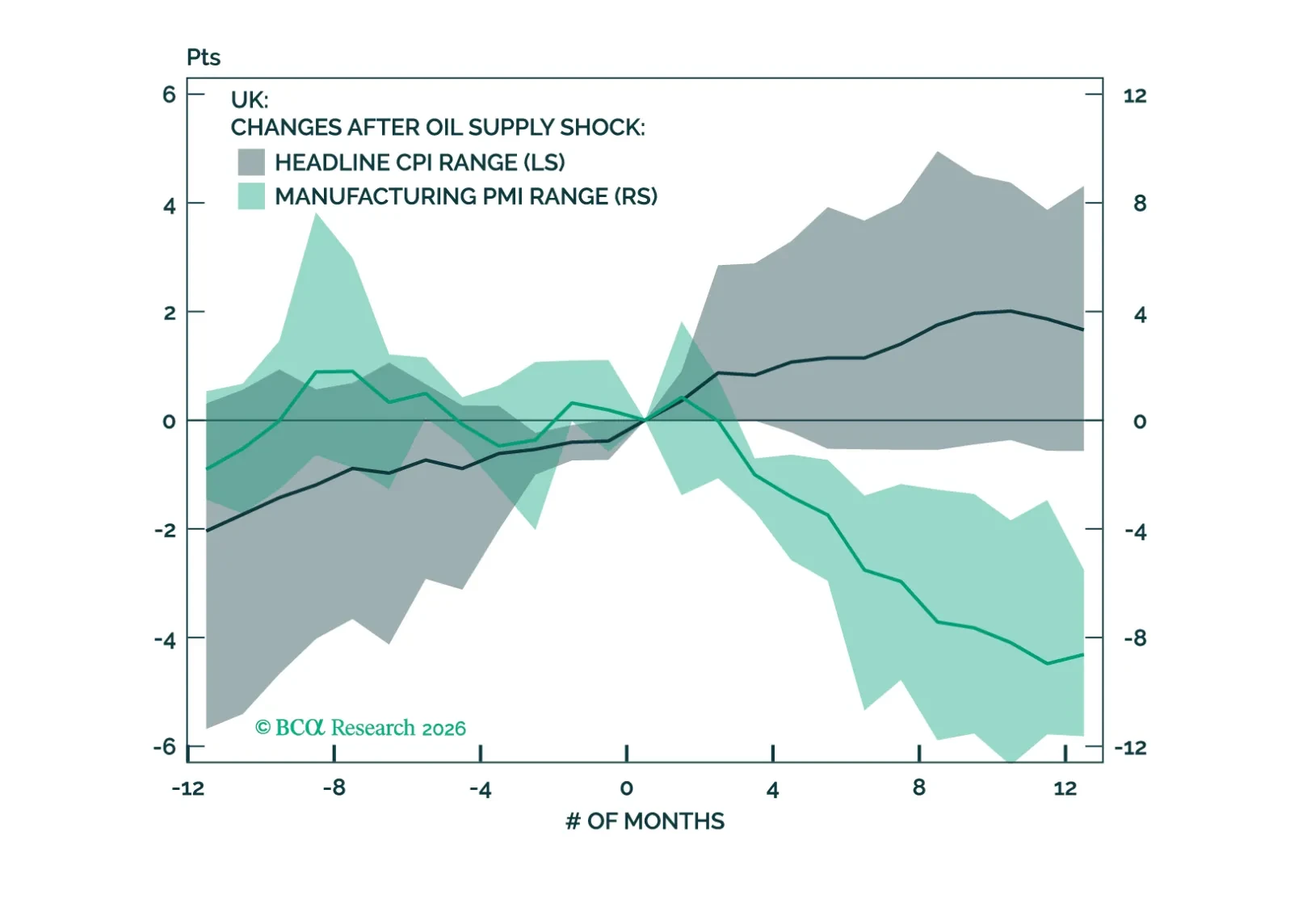

The global economy has weathered the oil shock reasonably well so far. However, the risk of a recession will increase meaningfully if the Strait of Hormuz remains closed into June.

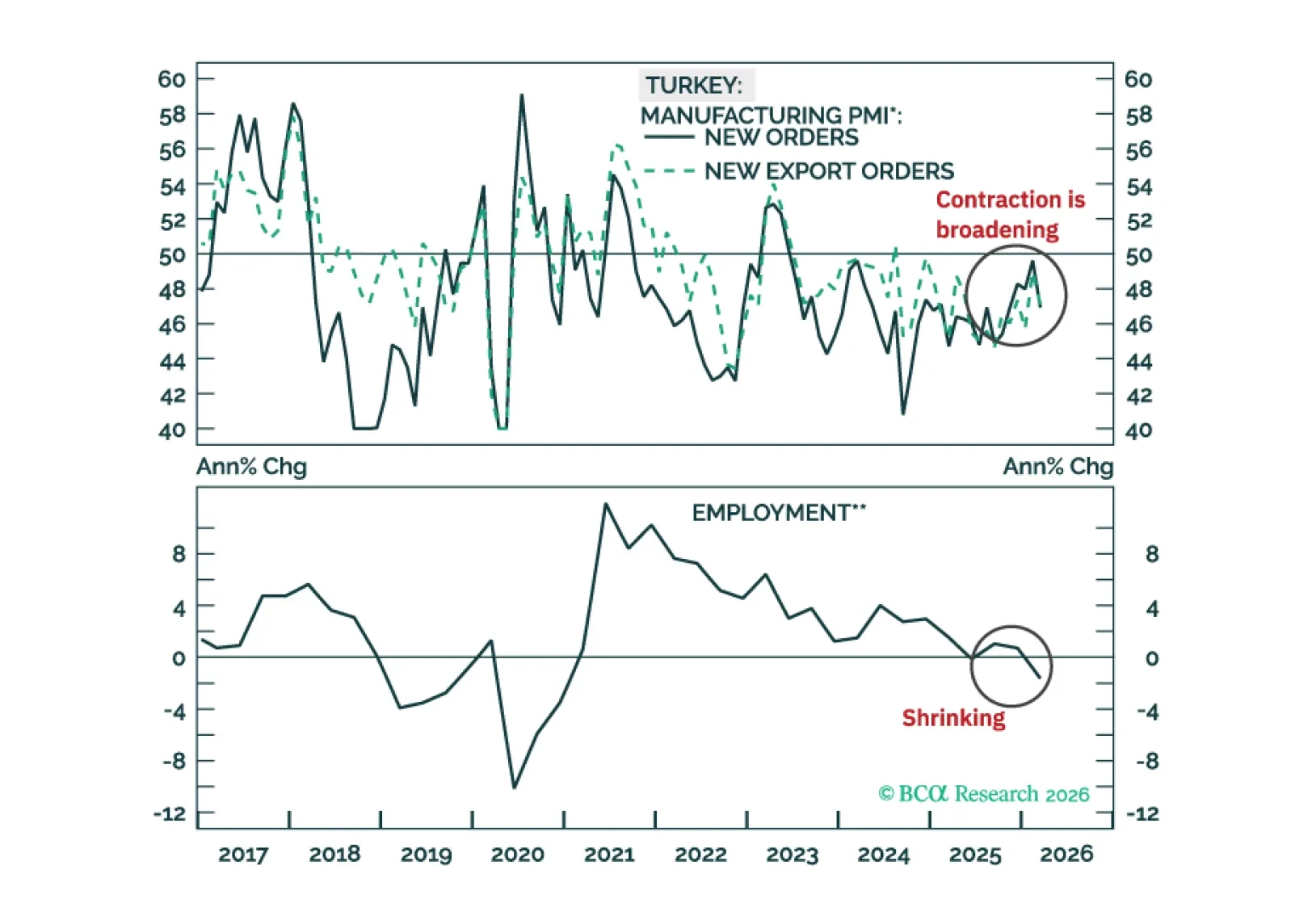

The Turkish financial markets will struggle in the very near term, but beyond that, the cyclical disinflation process will resume. Fixed-income investors should put Turkish 2-year local currencybonds on a ‘buy’ watch list.

Europe’s fiscal debate has resurfaced as interest rates normalize and new spending pressures emerge. Yet alarmism is misplaced. Aggregate debt levels are high but broadly stable, servicing costs remain historically low, and r–g dynamics are broadly benign. Fiscal space matters less as the ECB and EU backstop growth and spreads. Structural reforms—not wanton fiscal spending—is Europe’s real opportunity.

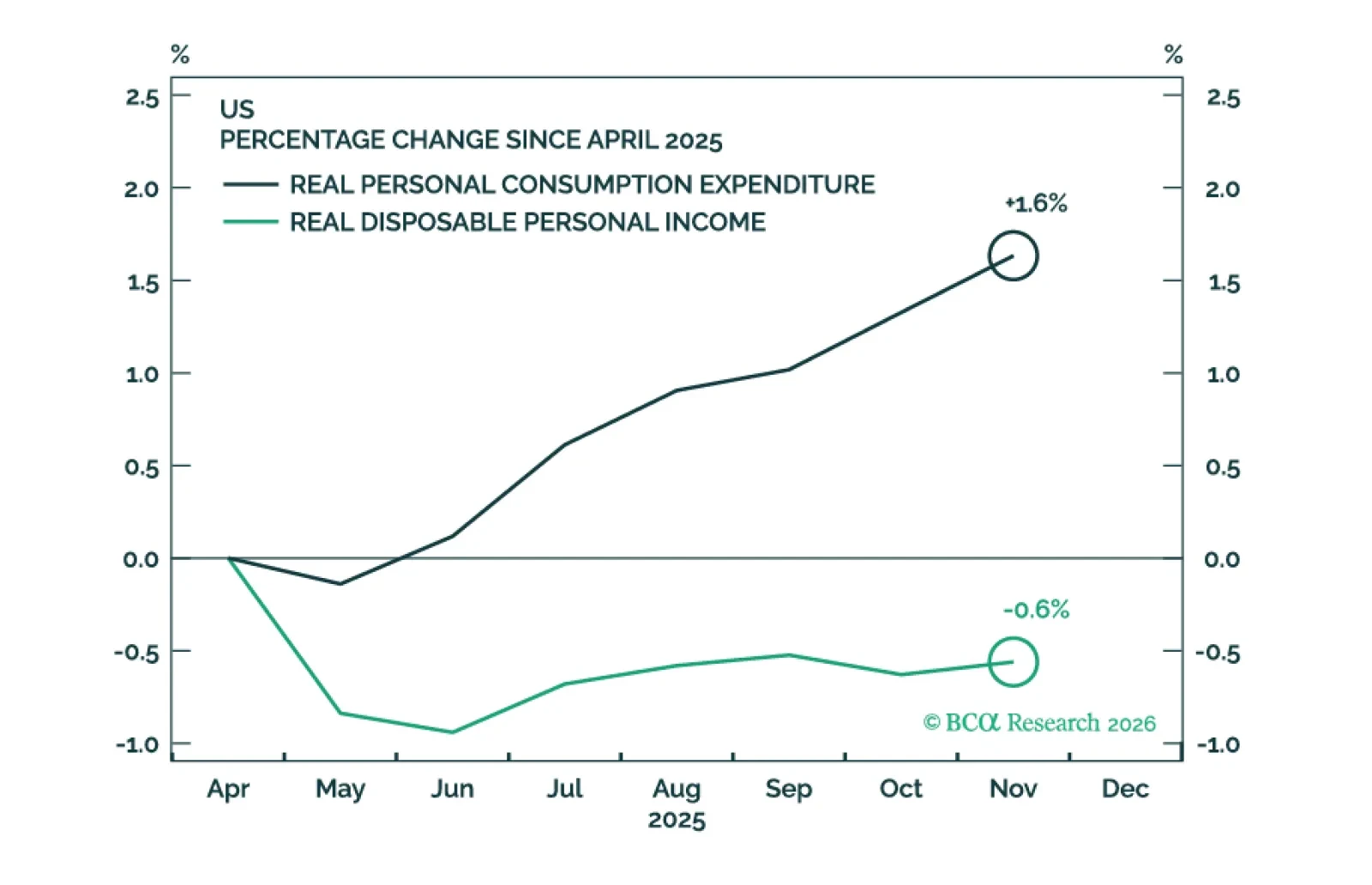

Recent economic data have been reasonably firm. We will cut our 12-month US recession probability to 40% from 50% if the Supreme Court strikes down President Trump’s tariffs. This would take our scenario-weighted year-end 2026 price target for the S&P 500 to 6375 from 6200.

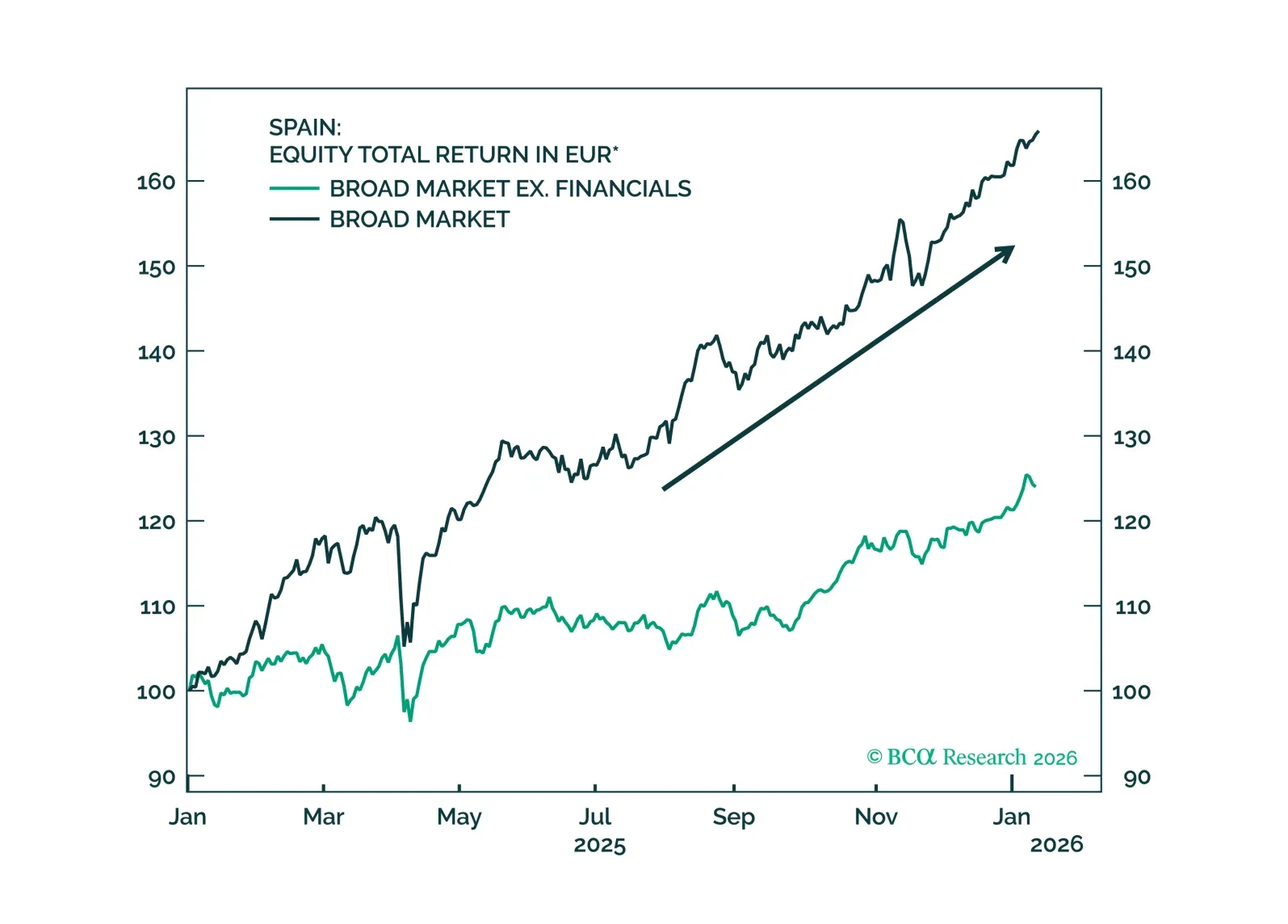

Spain's equity and bond outperformance reflects genuine fundamental repair: Lower bad loans, stronger profitability, and sustained earnings upgrades. Valuations remain undemanding despite the rally. Productivity is the key structural risk, but near-term fundamentals continue to surprise to the upside.

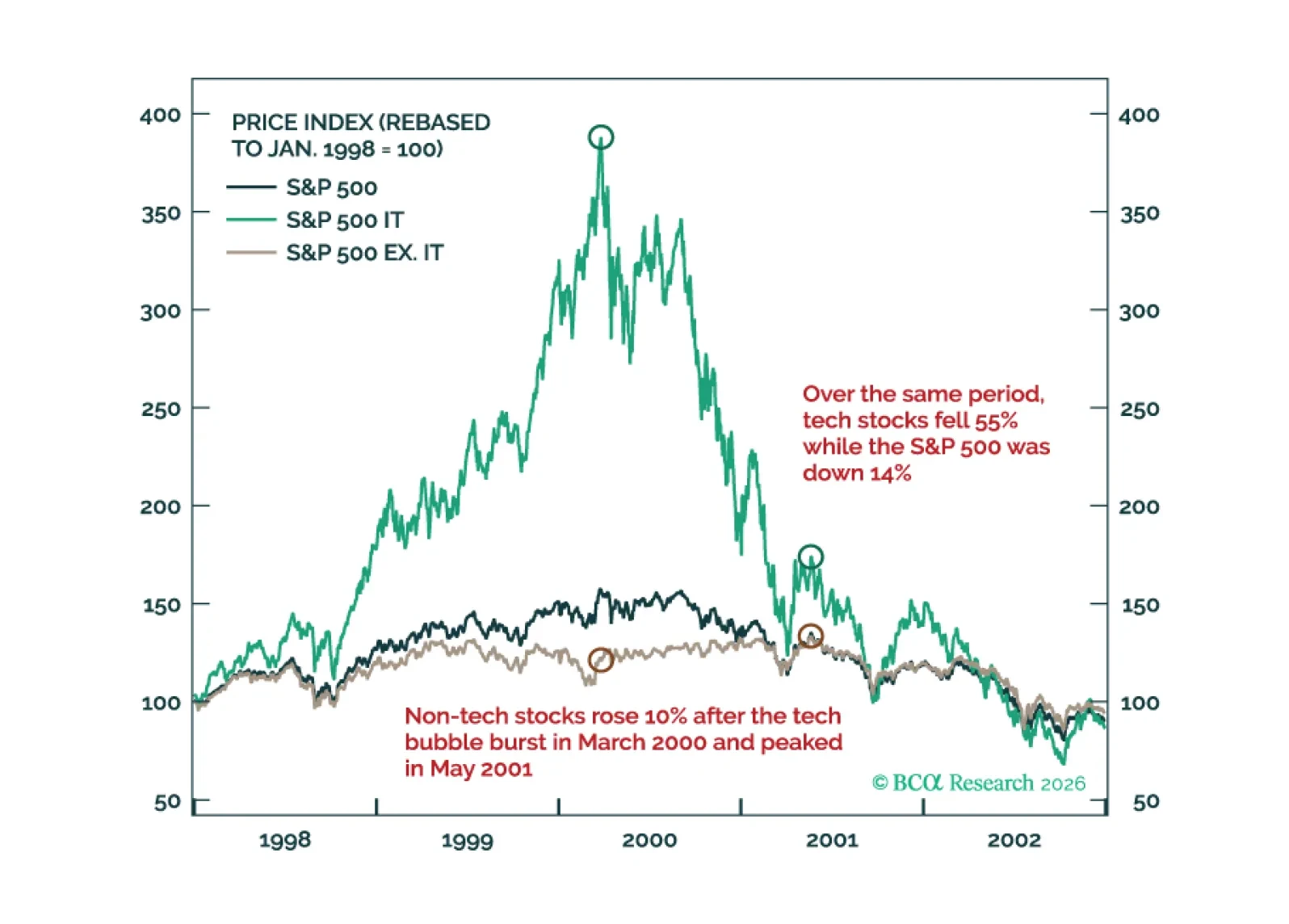

Much like the 2000 episode, we expect this year to unfold in two stages: A “Great Rotation” from tech stocks to non-tech names in the first half of 2026 followed by a broad-based selloff in stocks in the second half on the back of a weakening US economy.

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.