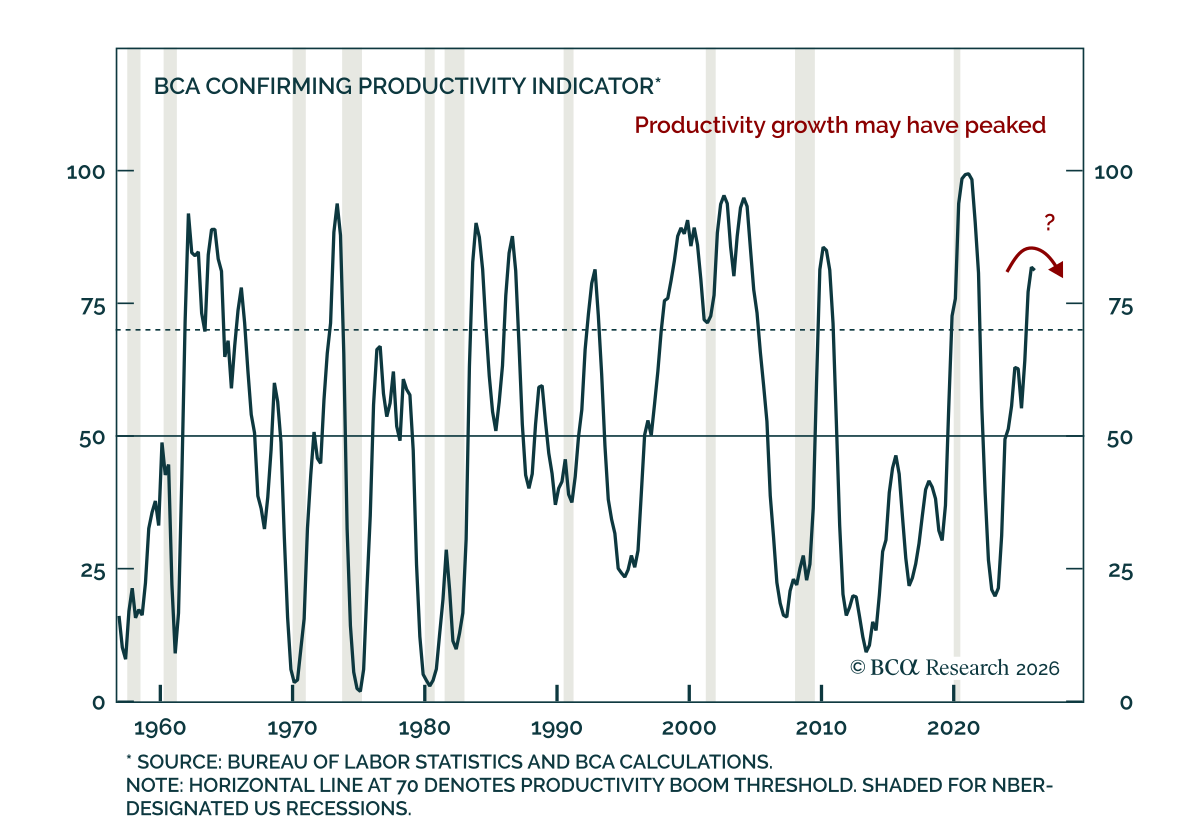

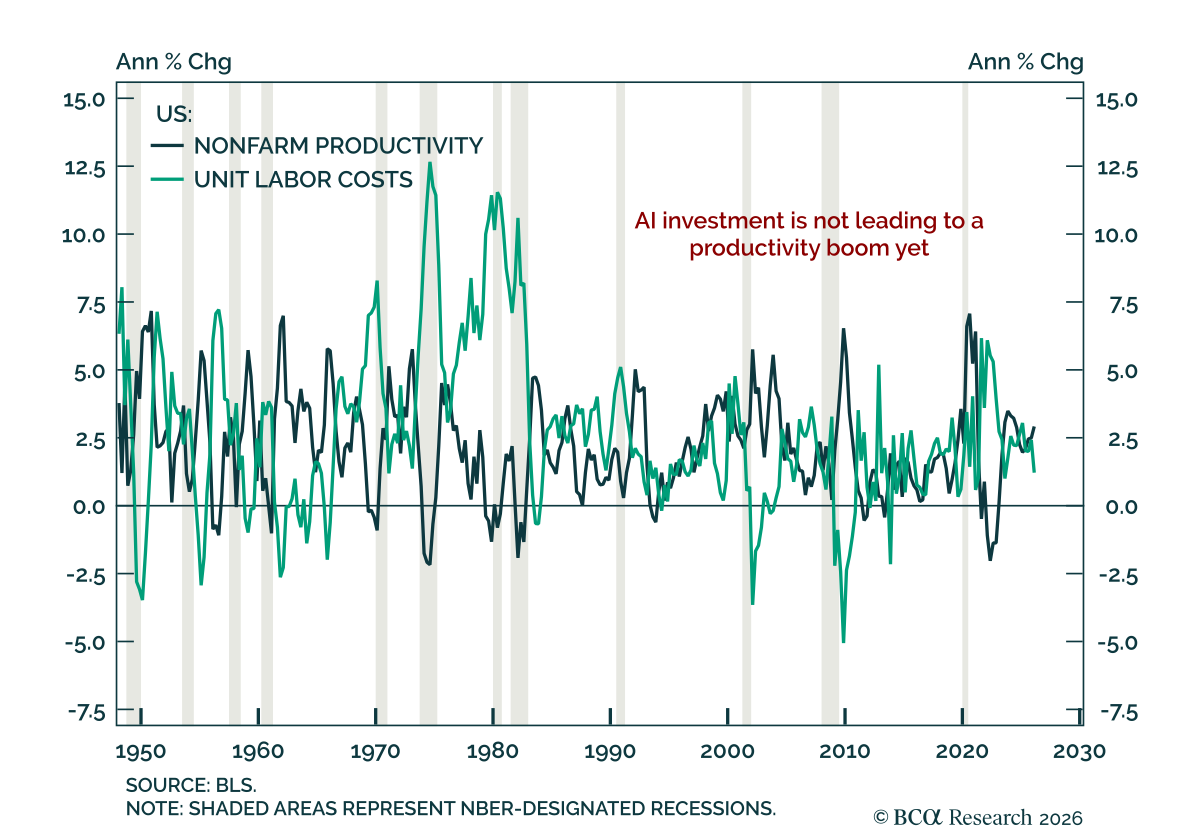

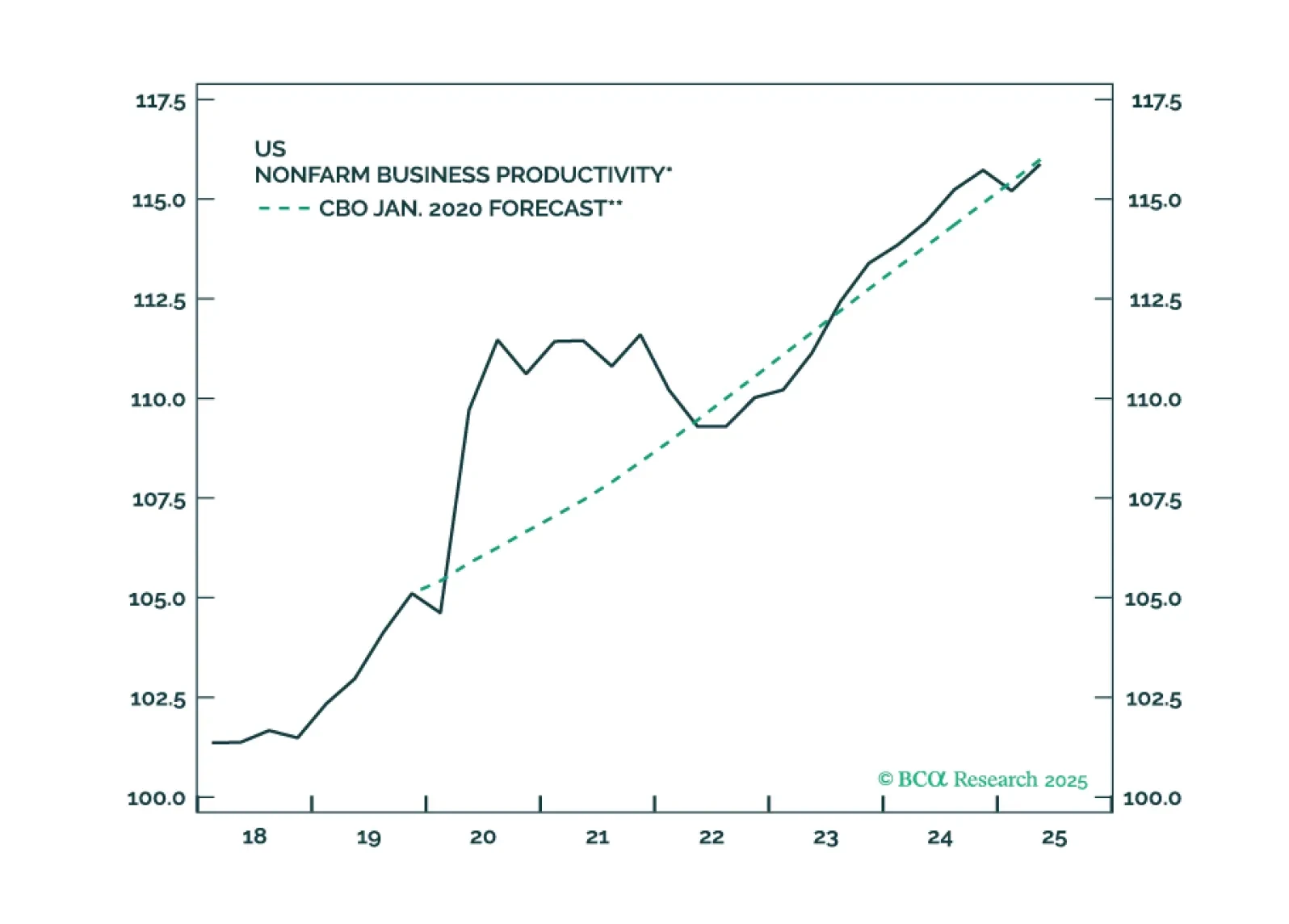

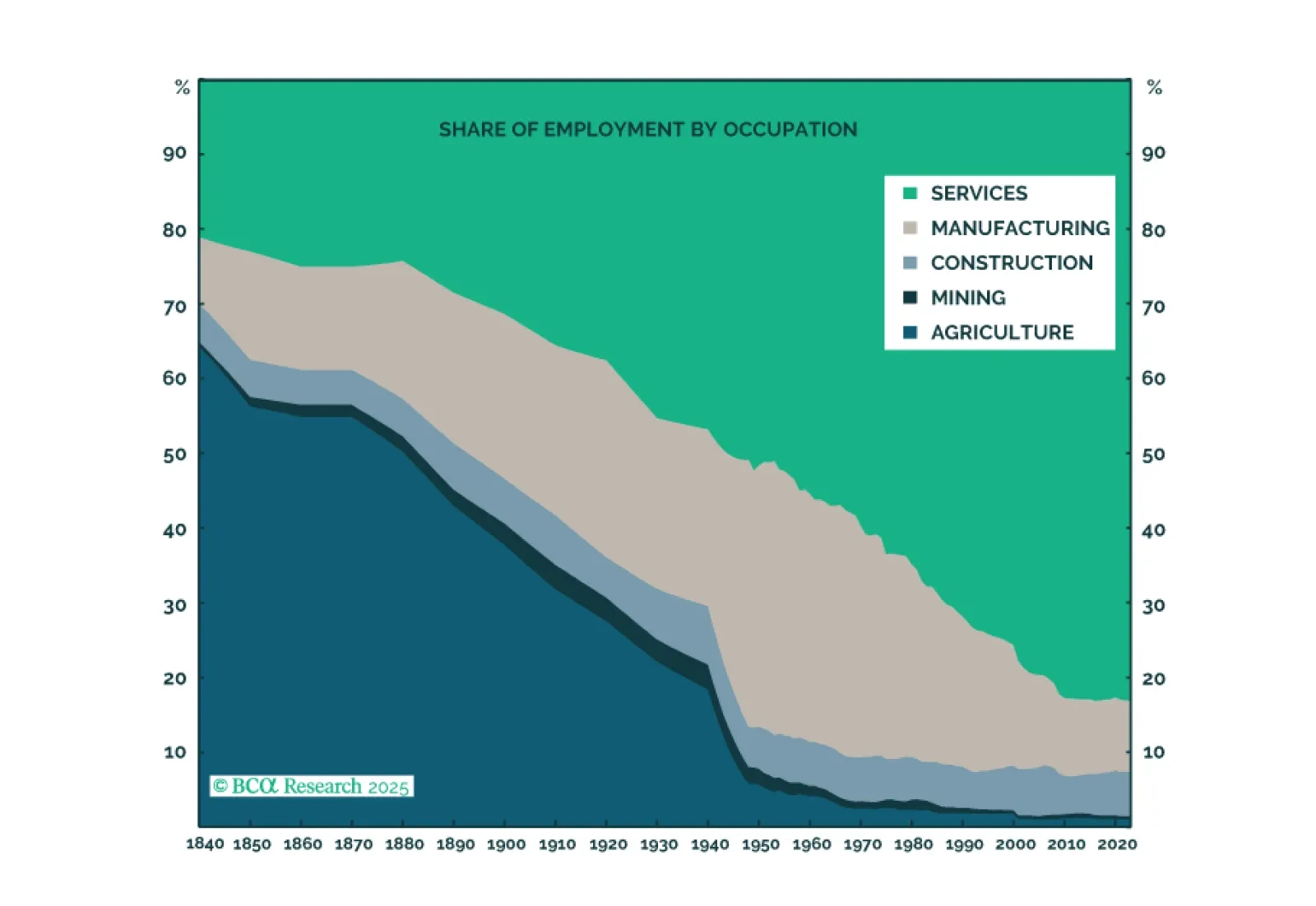

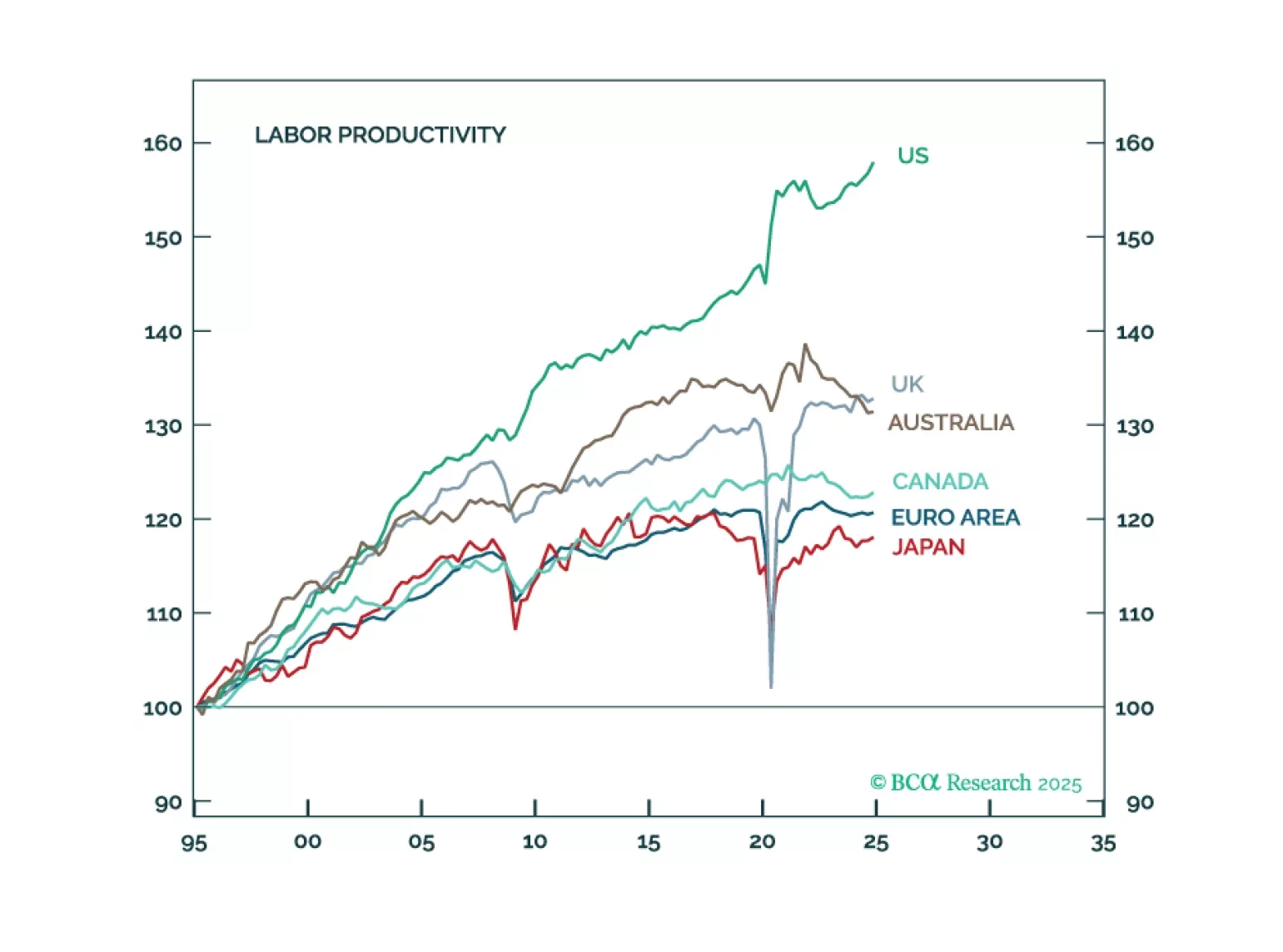

Productivity

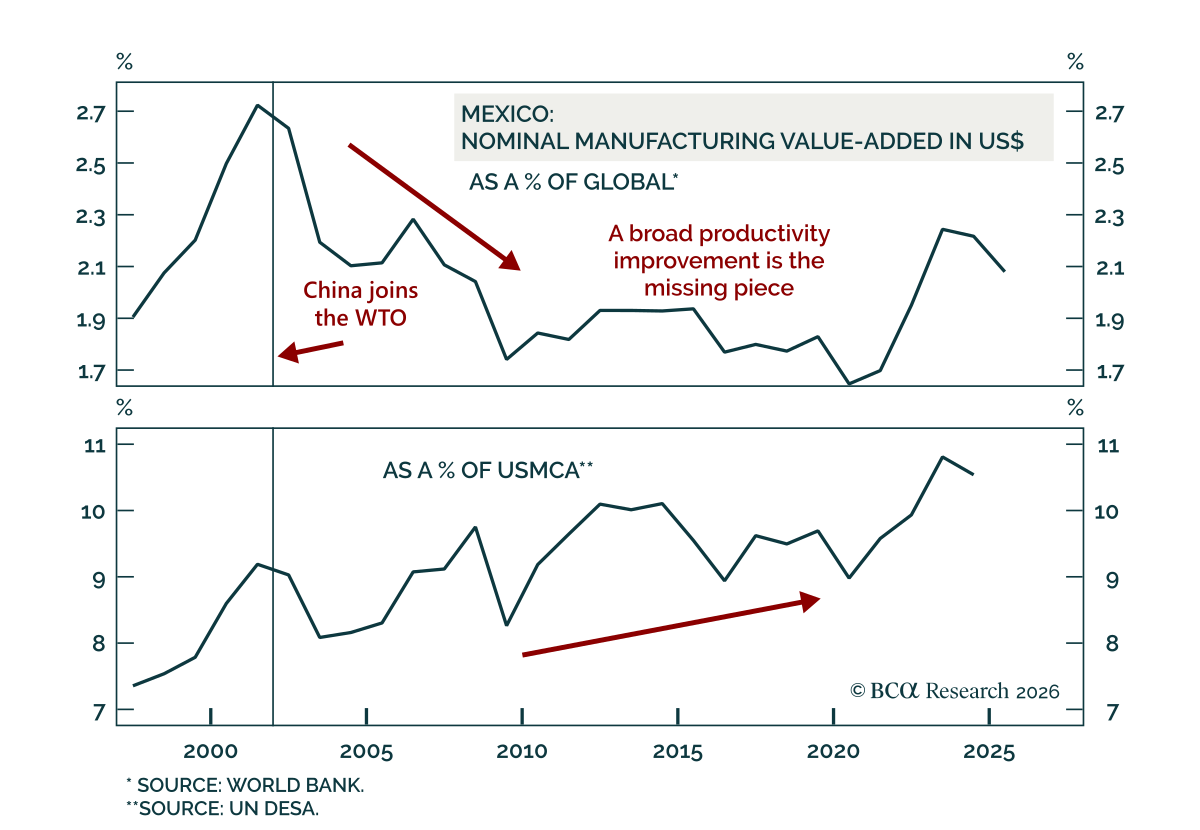

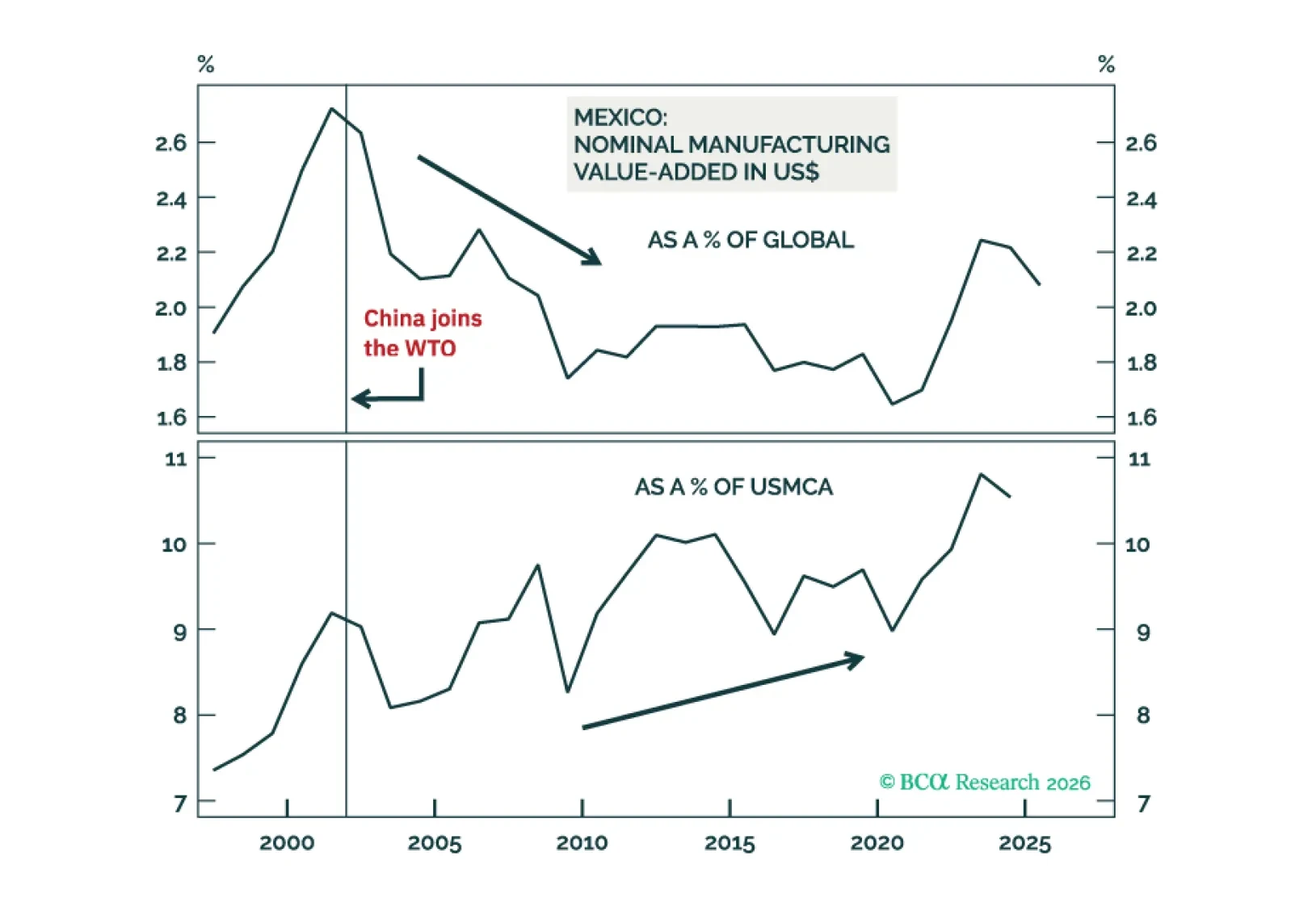

We continue to overweight Mexican stocks, local bonds, sovereign credit, and currency within their respective EM portfolios. Also, stay long Mexican equities / short the S&P500.

In Section II, Jonathan examines whether the AI “scaling laws” are likely to hold. They will over the near term, but cracks are already beginning to form in the narrative of ever-improving AI.

The rush to build AI infrastructure is based on a false premise: that there are significant advantages to being the first to come to market.

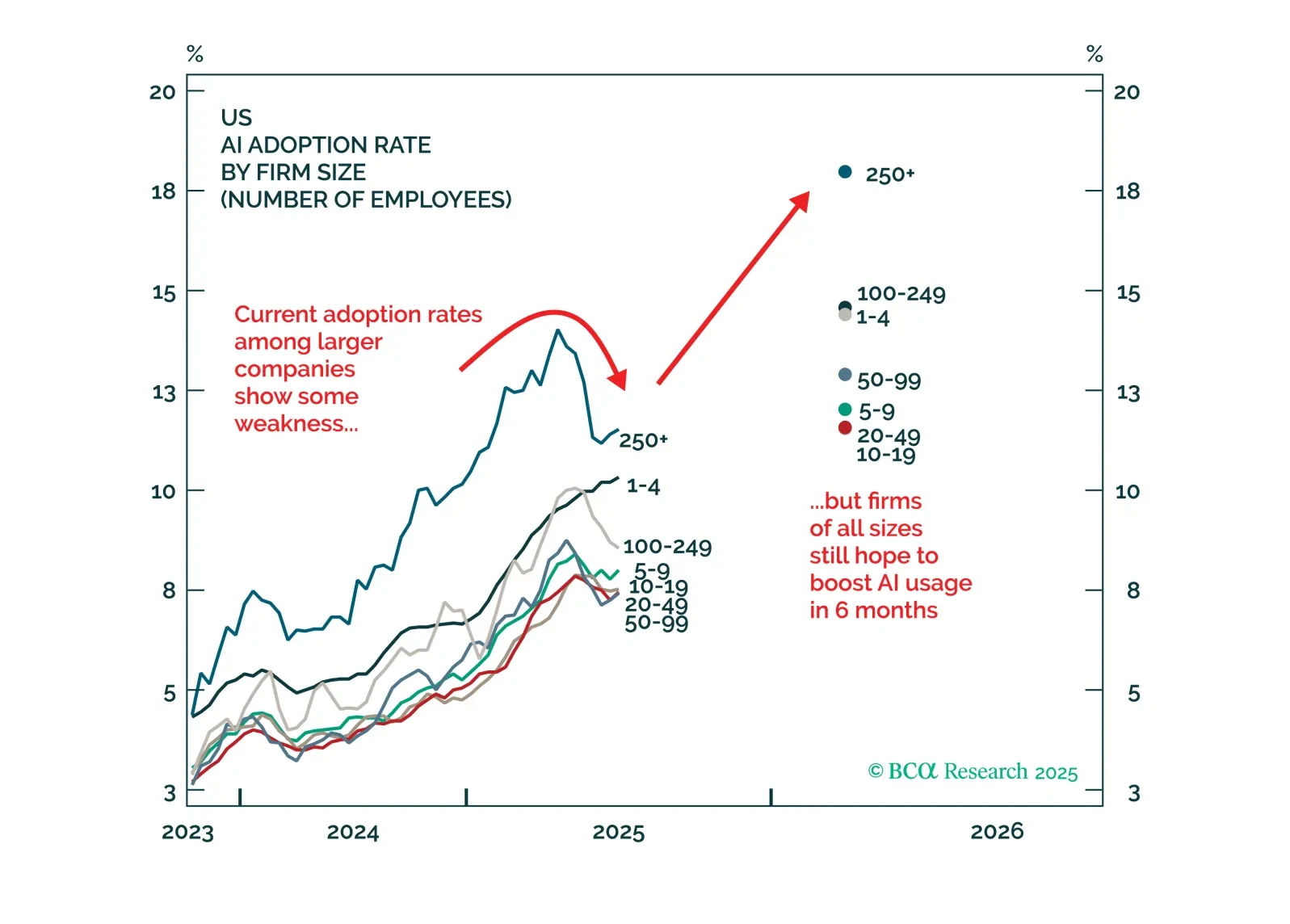

The AI boom has had less of an impact on the economy than widely believed. This may eventually change, but the risk is that investors grow impatient before it does.

Provided that humanity can overcome the existential risks posed by AI, real incomes will rise. Although most workers will ultimately gain from the transition to an AI-dominated economy, the biggest winners will be those who control the land and the natural resources beneath it.

Although the sell-off in the US dollar and relative outperformance of non-US stocks will pause over the coming months as a global recession begins, the fading of US exceptionalism will still cause the dollar to weaken and US stocks to underperform over a multi-year horizon.

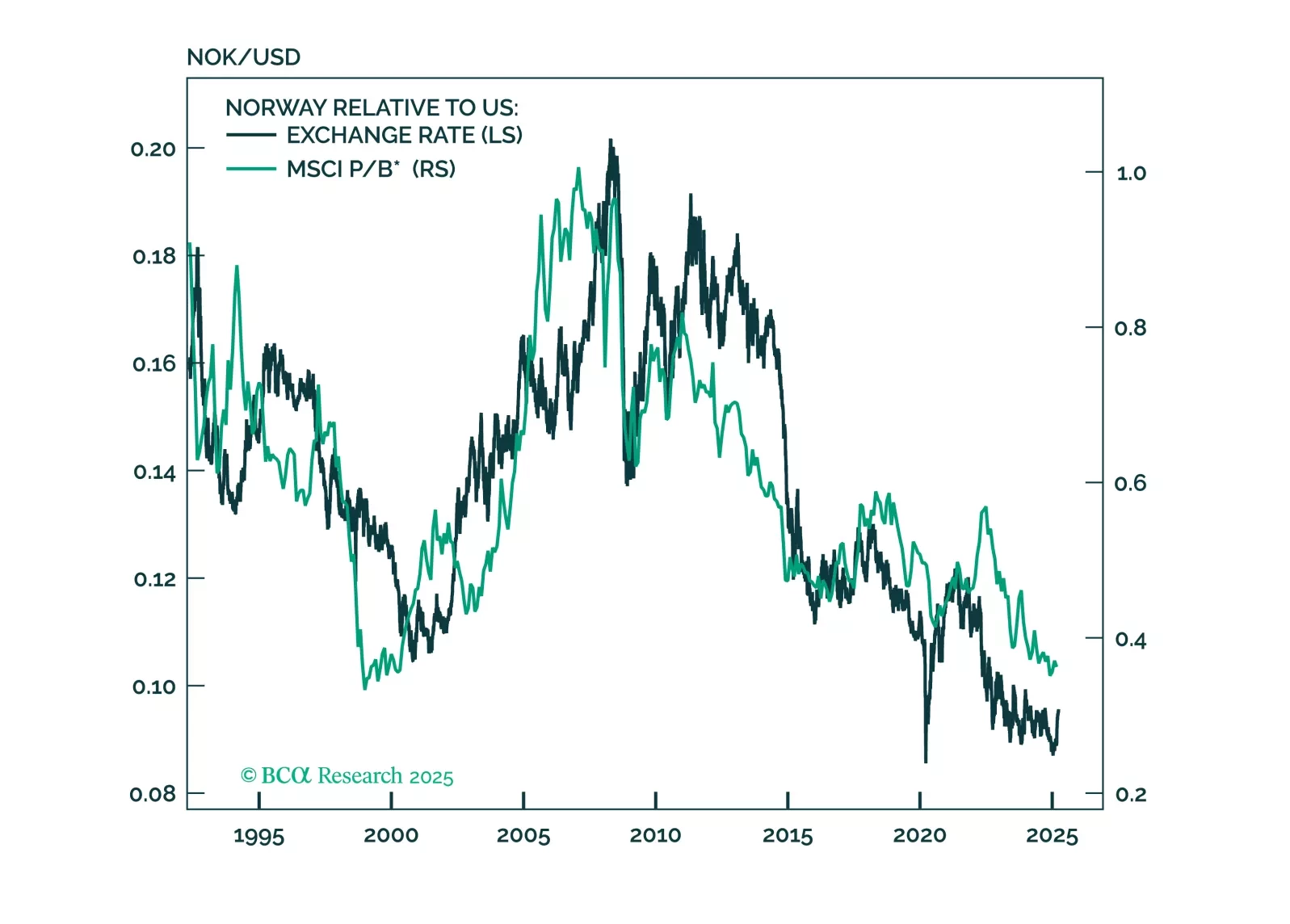

This report looks at investment implications, for Norwegian assets, given the recent meeting, from the Norges Bank.