Commodities

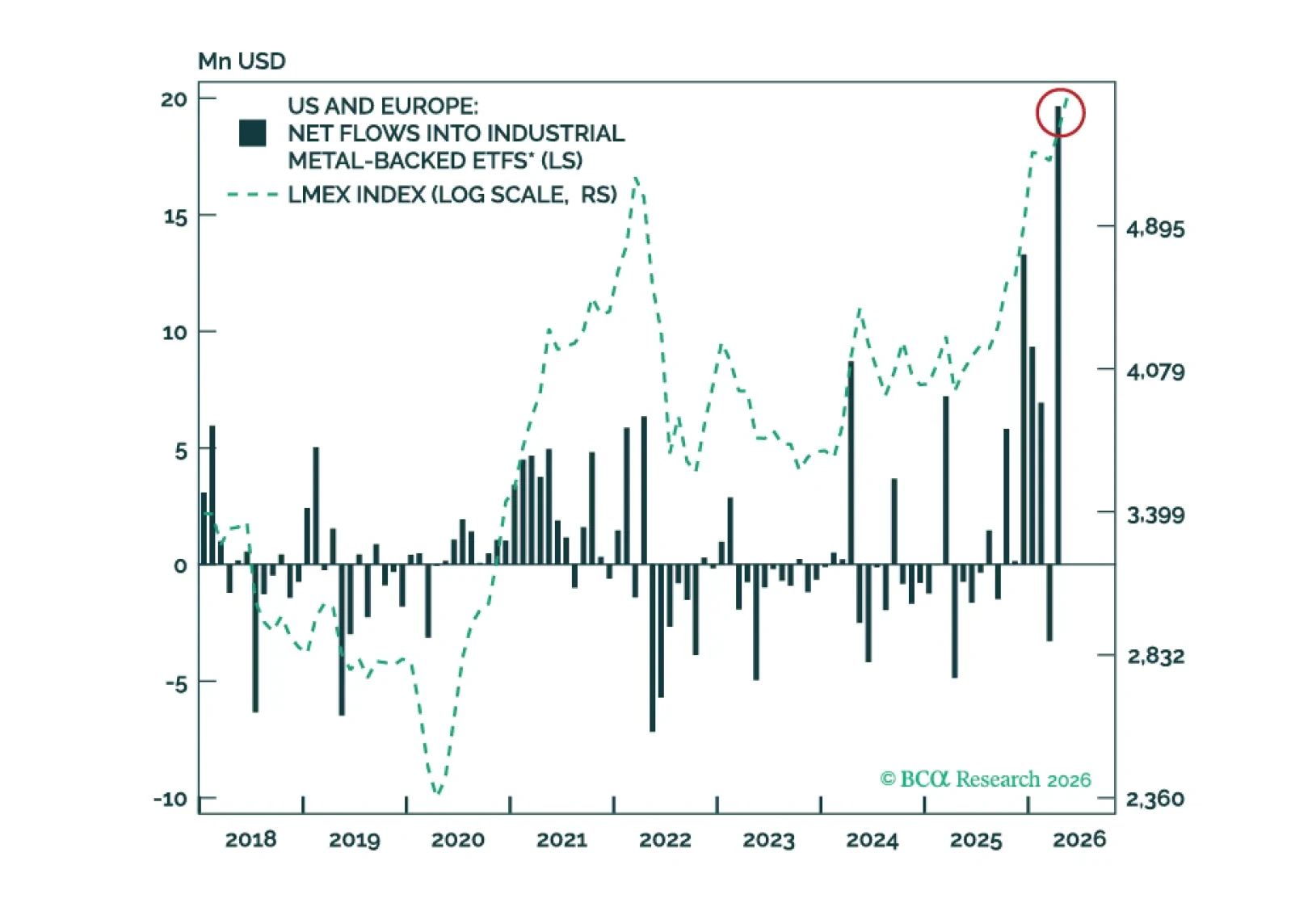

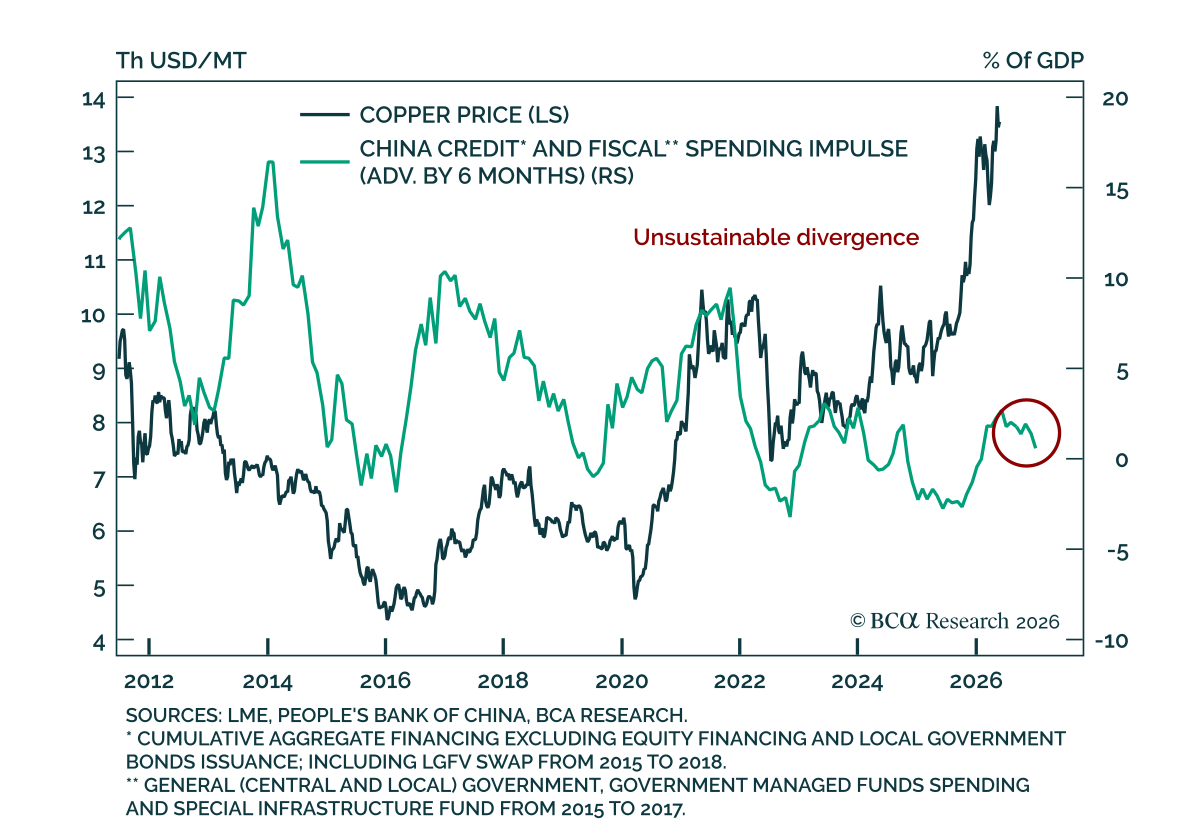

Copper prices are surging again after a brief pullback in the first quarter.

What is driving the renewed strength, and can it persist?

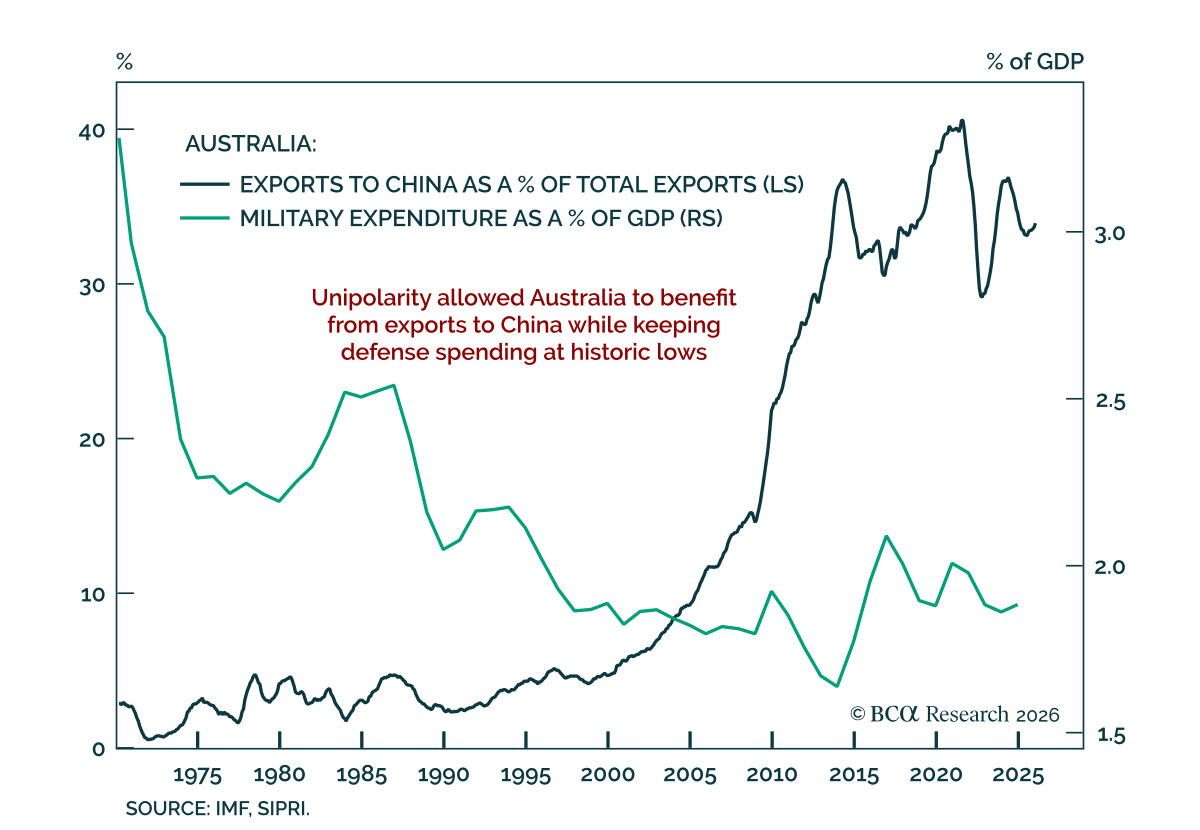

In this month’s Beta Report, we assess what that structural tension means for investors under two distinct scenarios. In our base case – a multipolar world order – Australia's position turns out to be more advantageous than it appears. The great power capital expenditure race generates demand for precisely what Australia produces. In the tail risk – a hard bipolar rupture – the calculus inverts, and the same commodity dependencies that long appeared as structural strengths begin to look like structural liabilities.

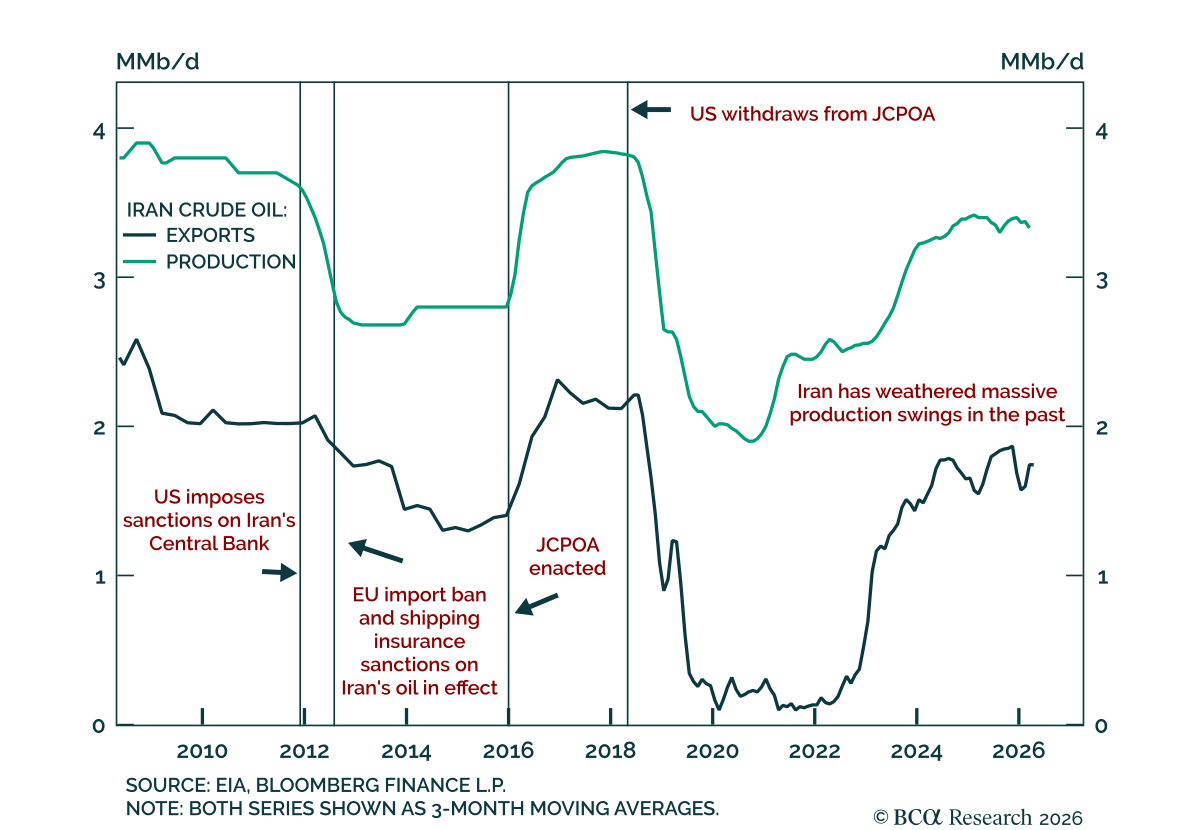

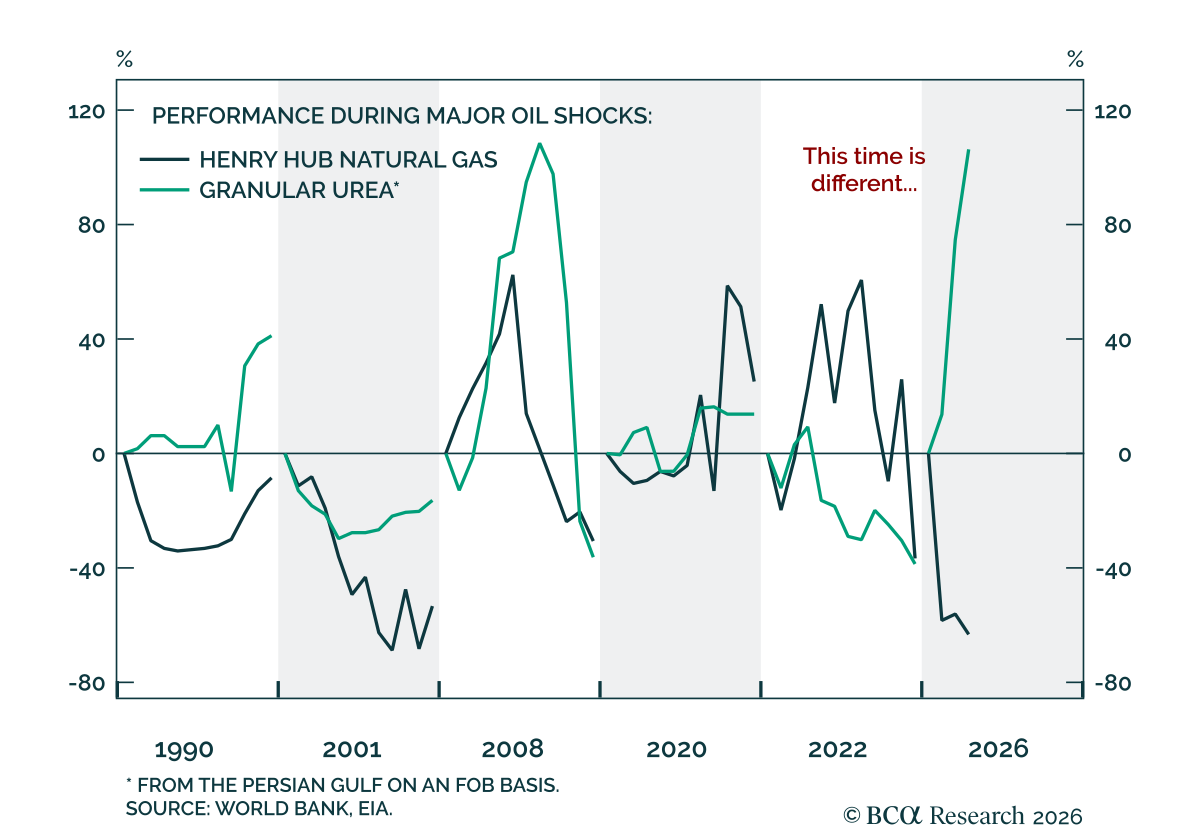

Hopes for an imminent Middle East de-escalation have capped oil prices in recent weeks, but that restraint may soon fade.

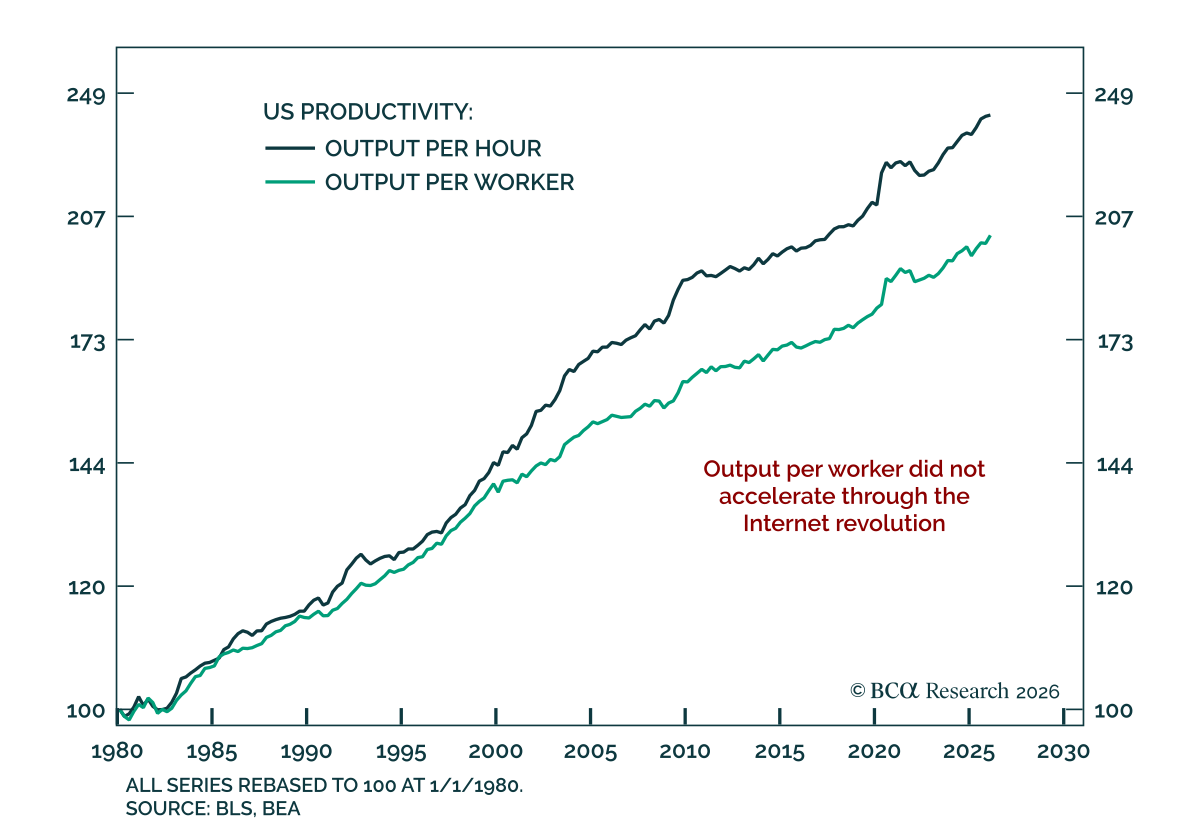

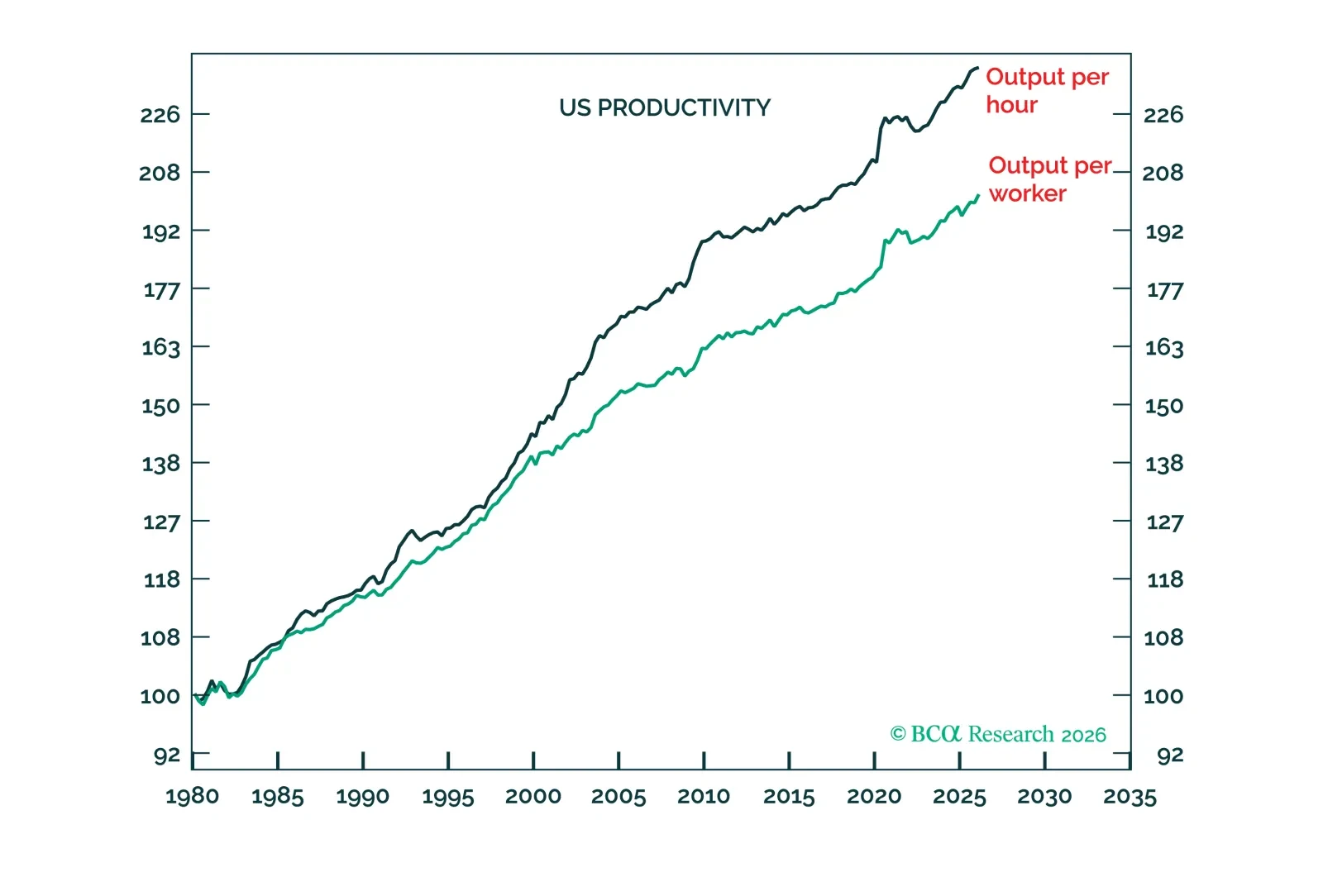

New Fed Chair, Kevin Warsh, is betting that an AI-driven productivity acceleration will get the Fed out of jail for persistently missing its 2 percent inflation target. But history informs us that while new technology adoption is exponential, total productivity growth is not. So, if Warsh’s bet goes wrong, as is likely, the US inflation overshoot will persist. We discuss the investment implications. Plus, a new trade is short cotton.