Financial Markets

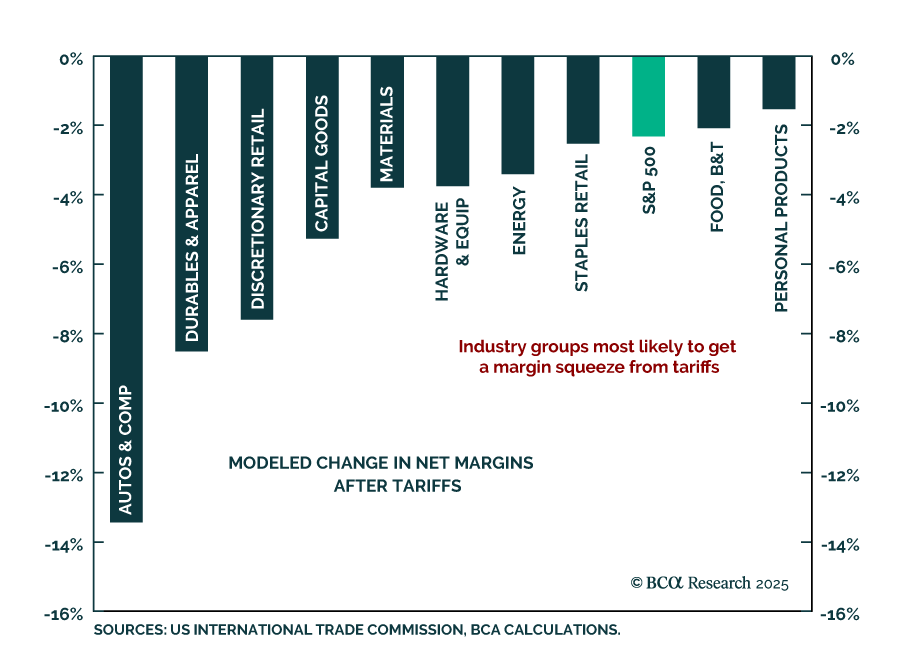

Our US Equity strategists warn that tariffs will meaningfully compress S&P 500 margins, with little pricing power to offset rising input costs. A two-point hit to net margins and falling multiples will drive earnings downgrades and negative forward…

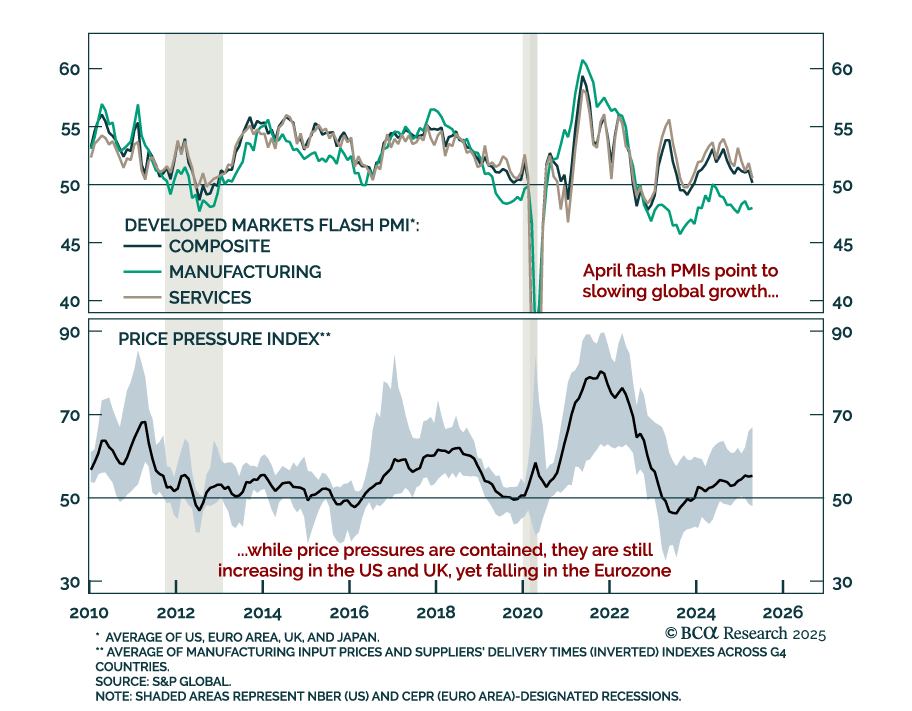

April PMIs confirm global growth is stalling, reinforcing our overweight in government bonds and underweight in risk assets. Services witnessed the worst deterioration, but manufacturing is still contracting even if broadly stable. This mirrors recent US…

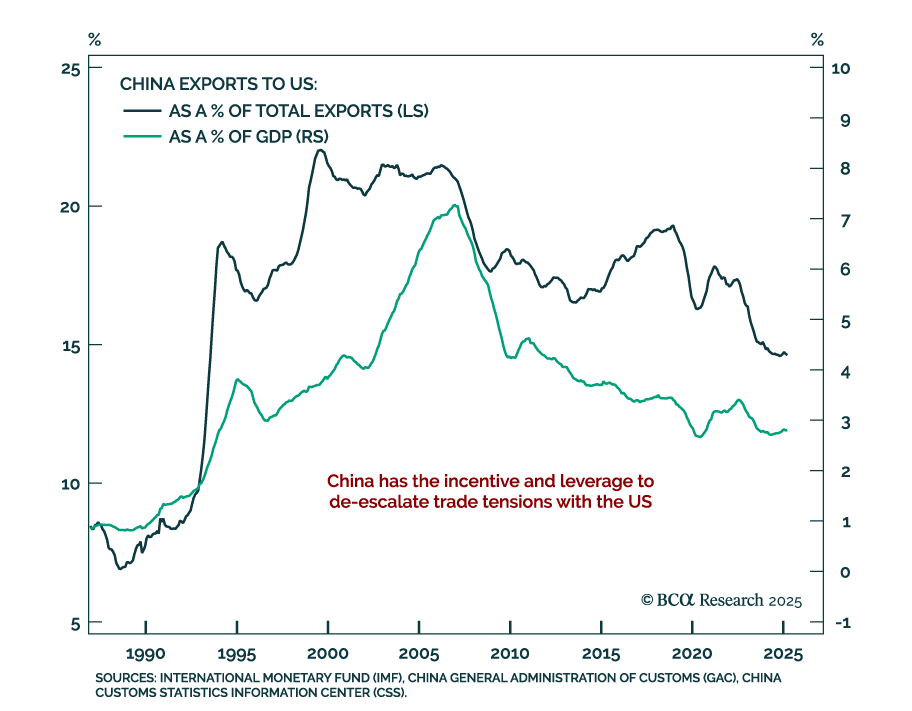

Trade headlines shift too fast to interpret reliably, but cutting through the noise reveals the US is pivoting from escalation to de-escalation. As the equity and bond selloff intensified, the tone from Washington softened, suggesting political limits to how…

Weak European consumer confidence adds to recent sentiment misses and reinforces our tactical long December 2025 ESTR futures versus SOFR position. April flash Consumer Confidence fell to -16.7 from -14.5 in March, missing expectations and aligning with…

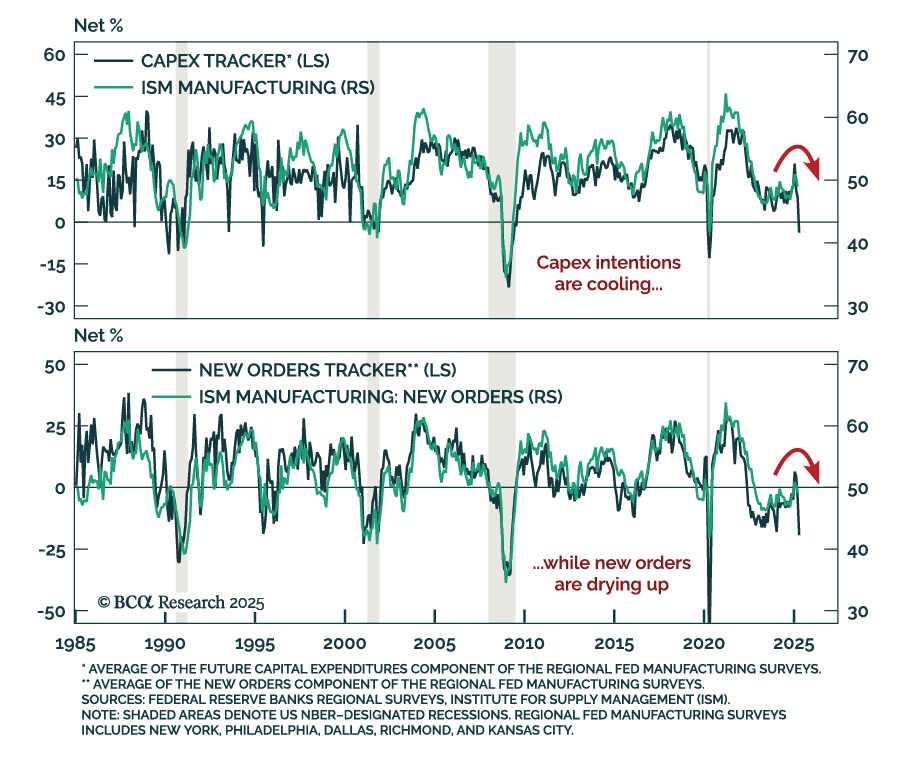

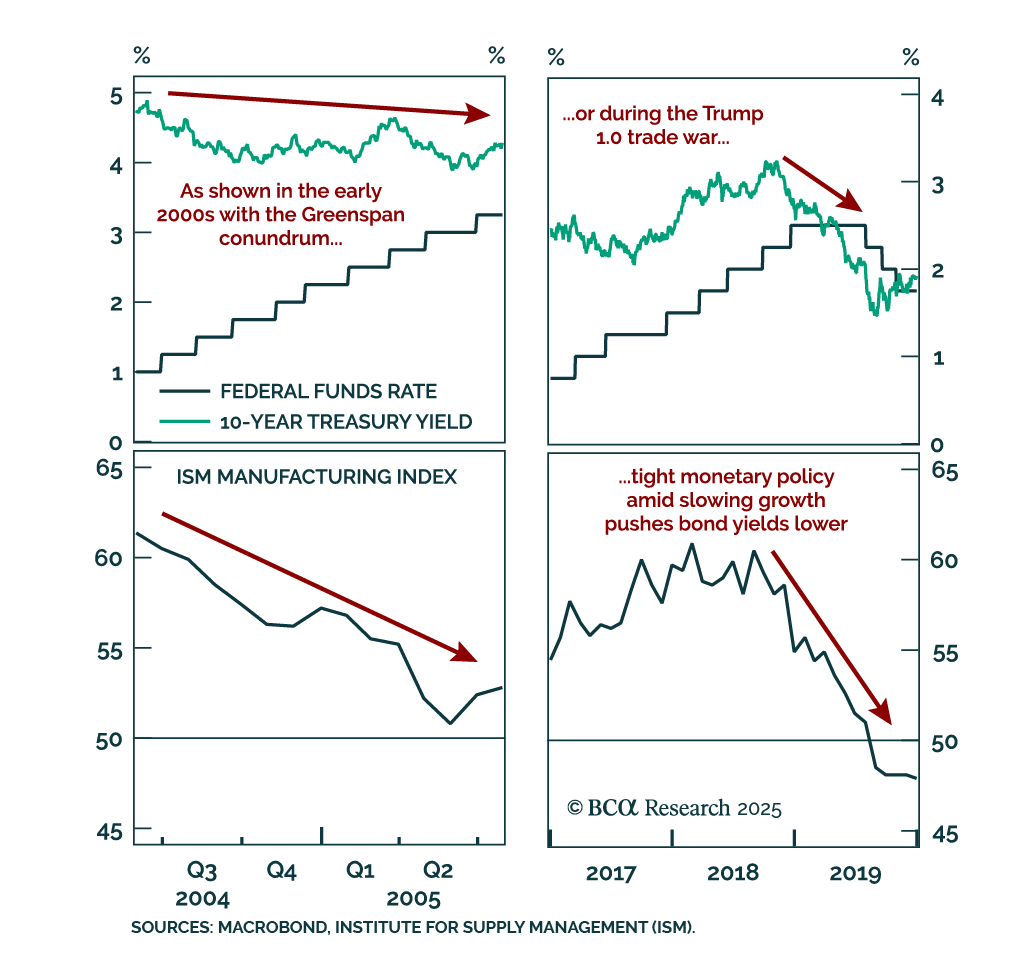

Advanced US indicators for April continue to deteriorate, reinforcing our defensive positioning as recession risks remain underpriced. After weak Empire and Philly Fed manufacturing prints, the Philly Fed services survey shows the slowdown is spreading beyond…

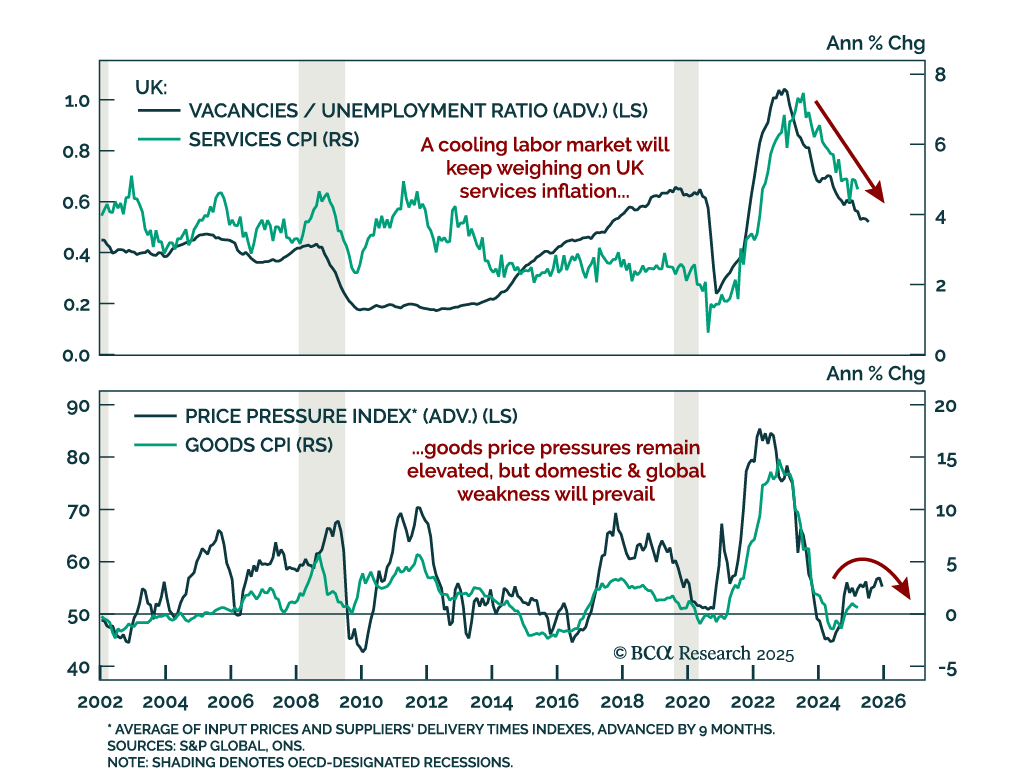

The latest UK data supports a May BoE cut, reinforcing our overweight in Gilts as growth headwinds build and inflation cools. Employment declined by 78k in March, accelerating from February’s downwardly revised 8k drop, while vacancies fell below pre-COVID…

President Trump's pressure on Fed Chairman Powell is intensifying, but keeping Powell in place offers the administration political cover while keeping bond yields contained. Removing Powell would be legally difficult and risk unsettling markets, while his…

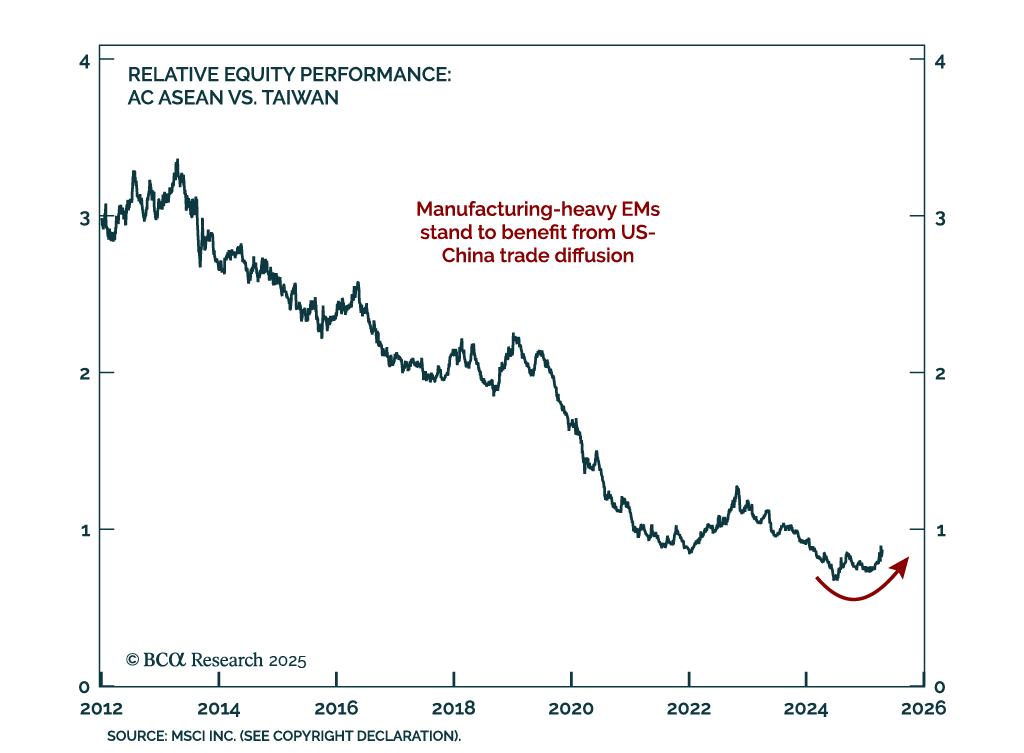

Our Geopolitical and GeoMacro strategists recommend buying tail-risk protection and adding exposure to manufacturing-oriented EMs as the risk of US-China military escalation rises. They now see a 10% chance of full-scale war over Taiwan and a 25% chance of a…

The ECB’s latest 25 bps cut and President Lagarde's notably dovish tone amid rising trade uncertainty reinforce our long December 2025 ESTR futures versus SOFR position. The deposit facility rate now stands at 2.25%, and Lagarde reiterated the disinflationary…

Our China strategists remain defensive and tactically downgrade MSCI China to underweight, citing escalating US China tariff tensions and subdued domestic demand. Favor government bonds over equities, defensive sectors, and A-Shares over offshore Chinese…