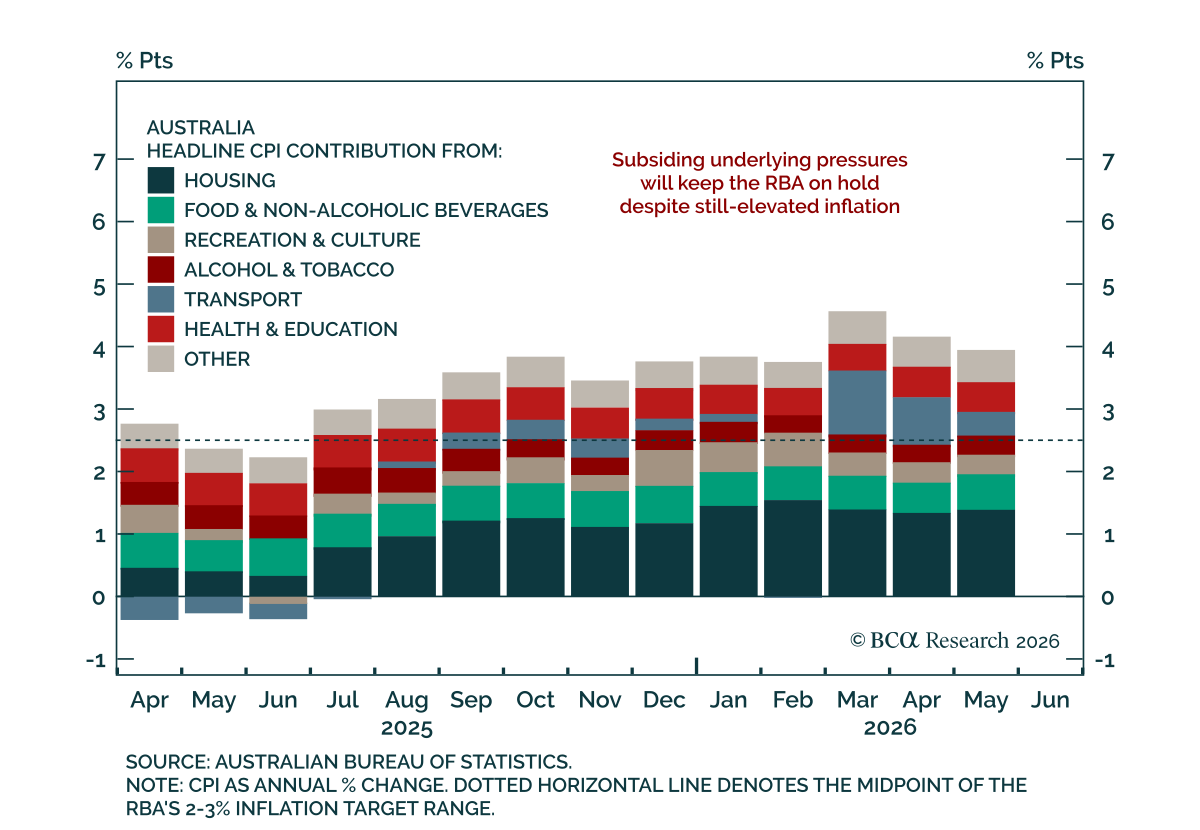

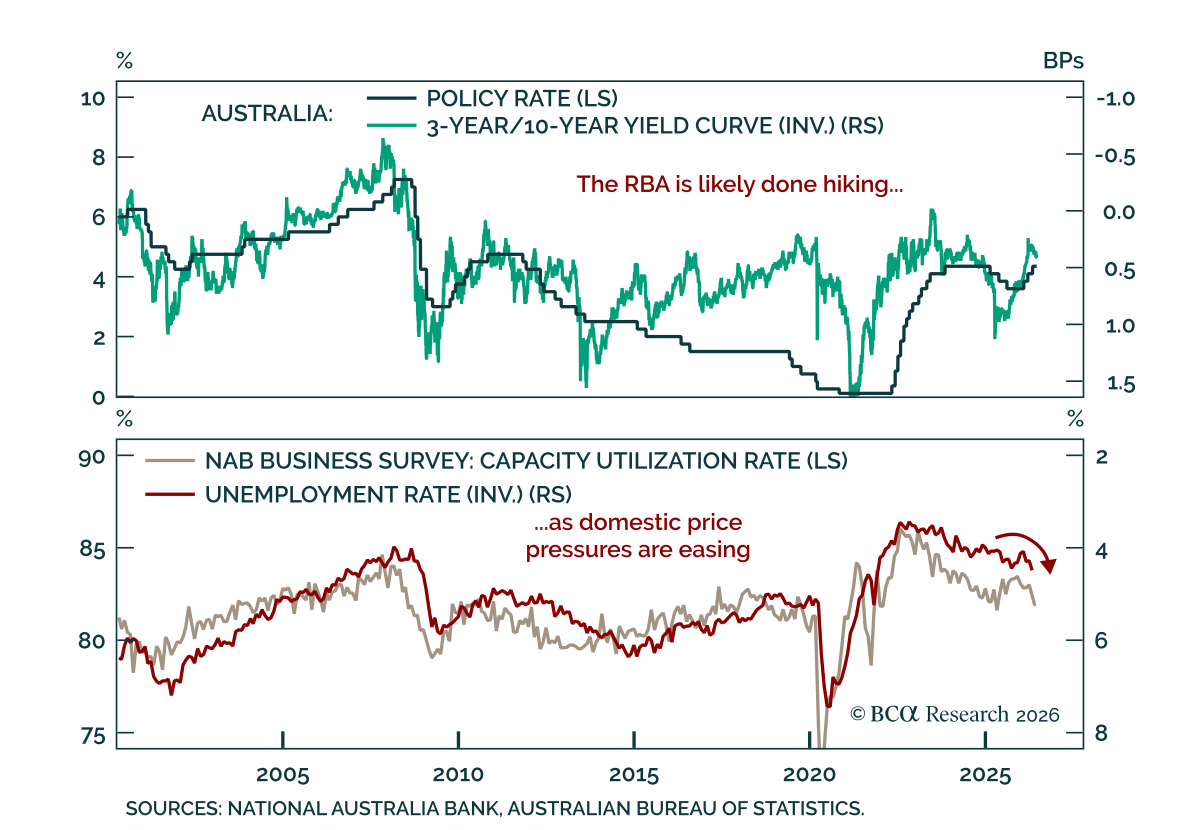

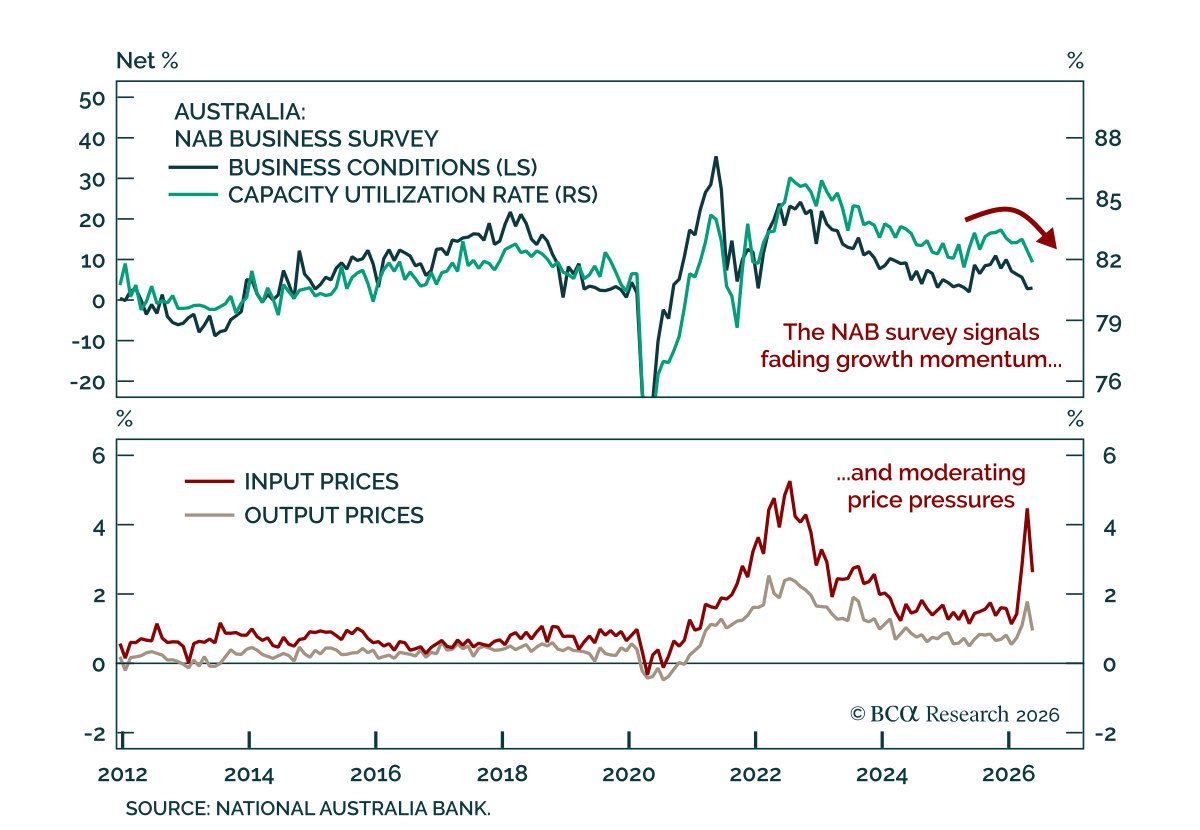

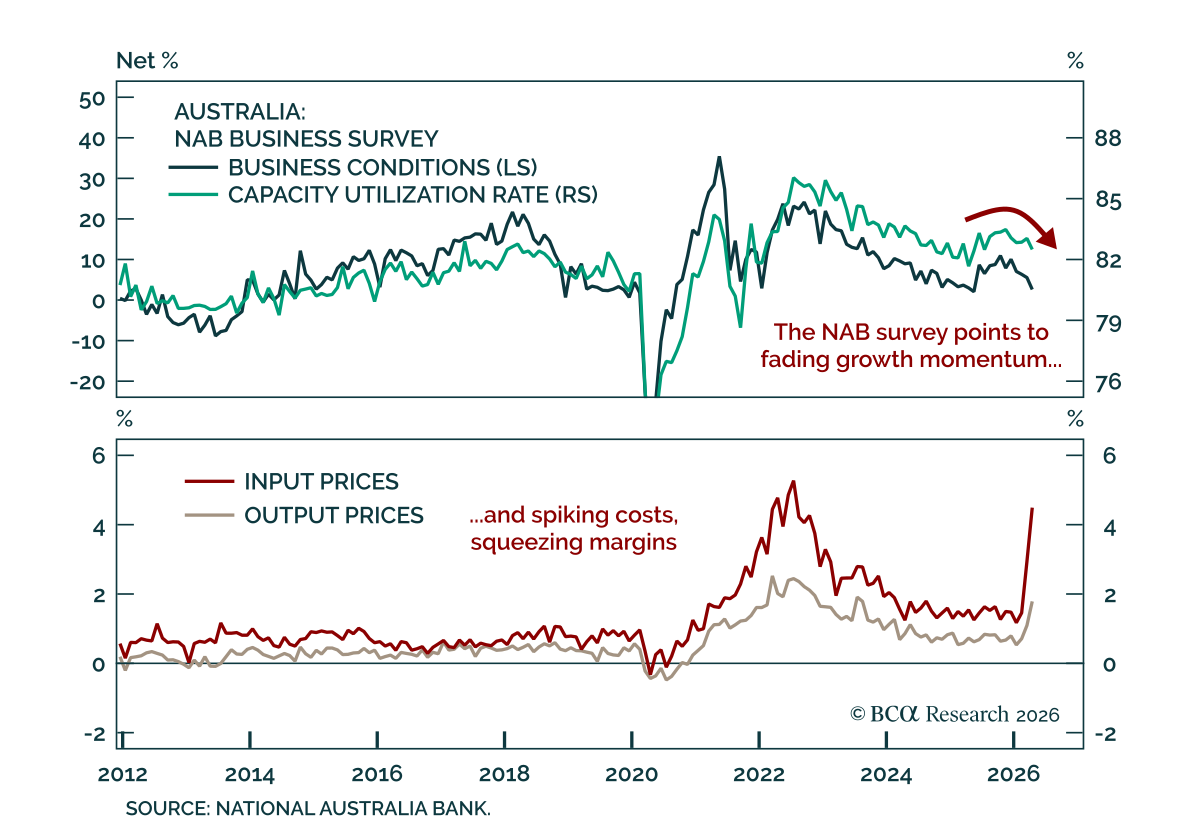

Australia

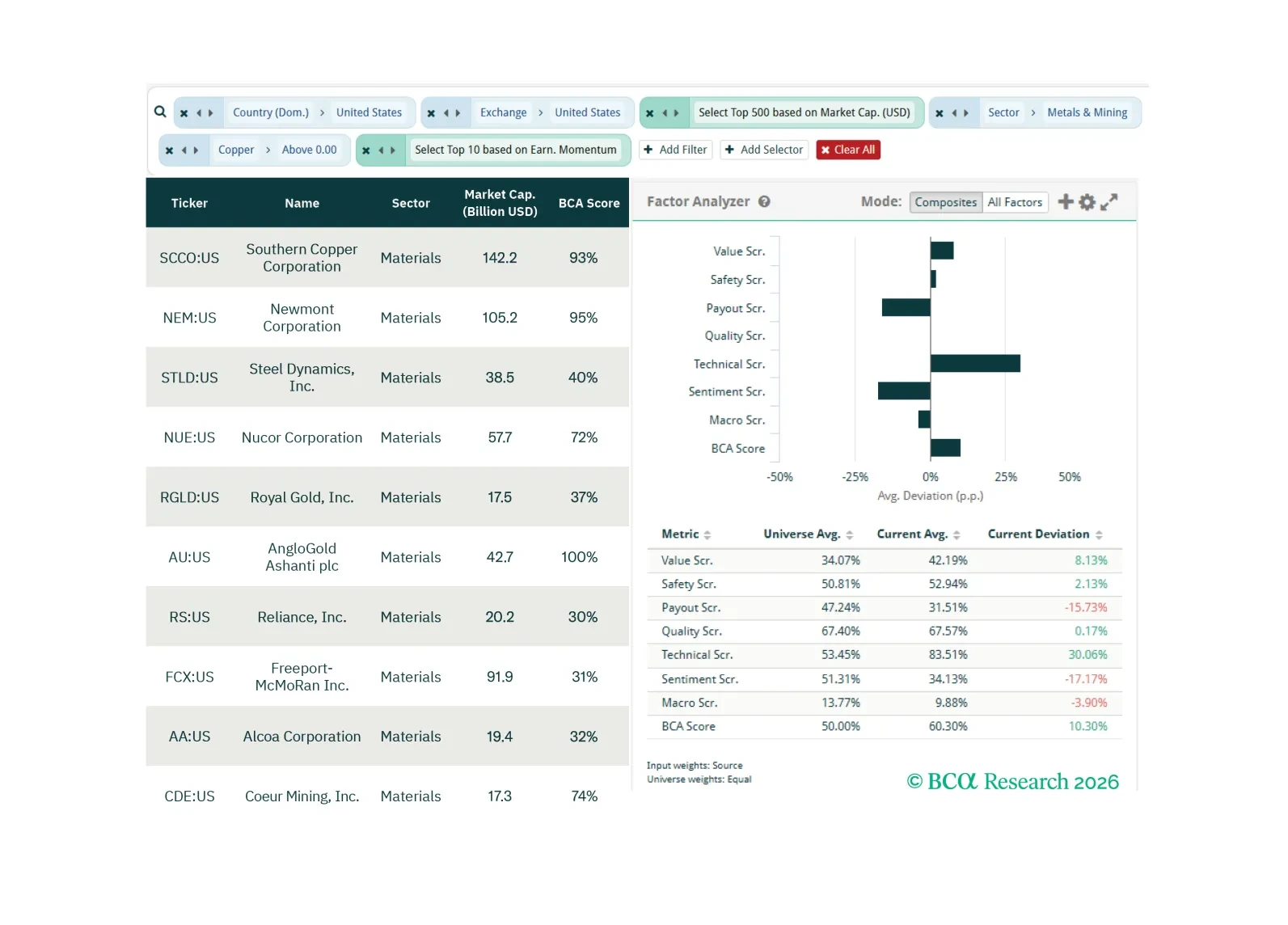

In this screener report, we explore opportunities in: US copper beneficiaries; Australian Materials, Energy, and Industrial stocks; and US reinvestment-led Tech stocks.

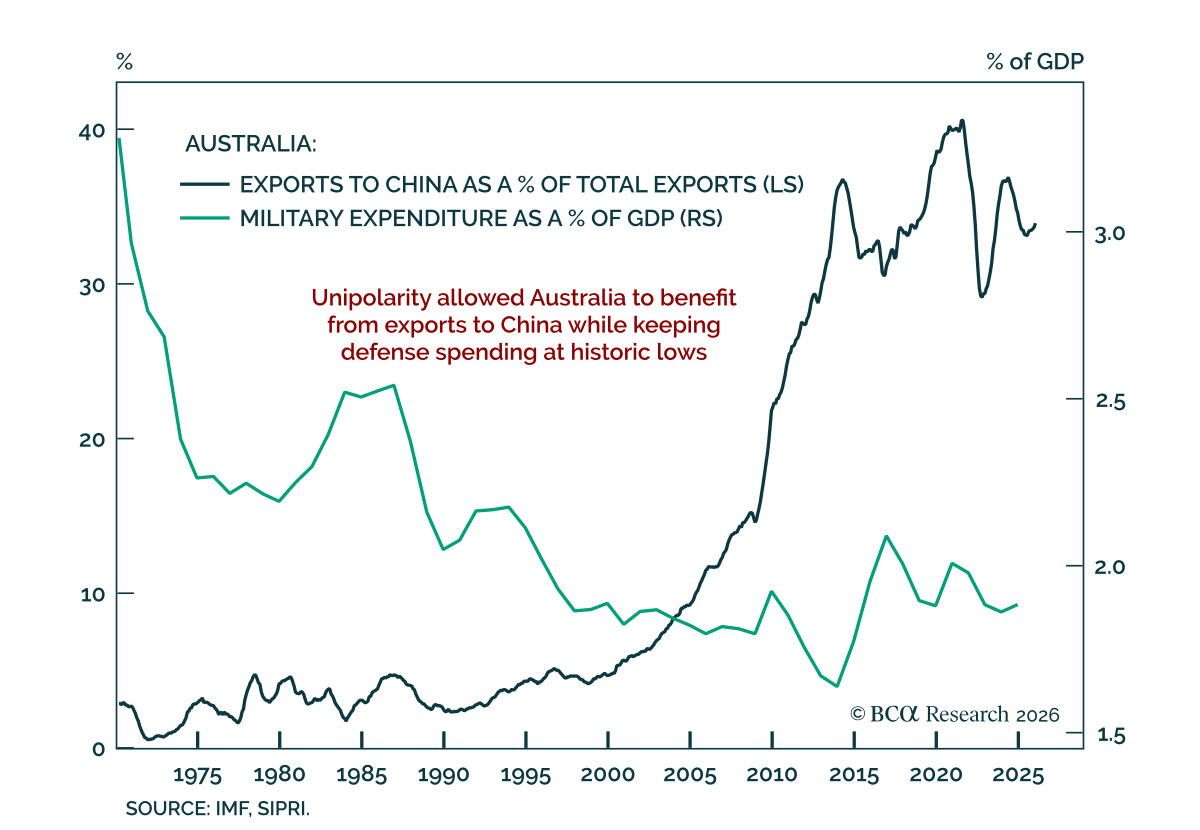

In this month’s Beta Report, we assess what that structural tension means for investors under two distinct scenarios. In our base case – a multipolar world order – Australia's position turns out to be more advantageous than it appears. The great power capital expenditure race generates demand for precisely what Australia produces. In the tail risk – a hard bipolar rupture – the calculus inverts, and the same commodity dependencies that long appeared as structural strengths begin to look like structural liabilities.

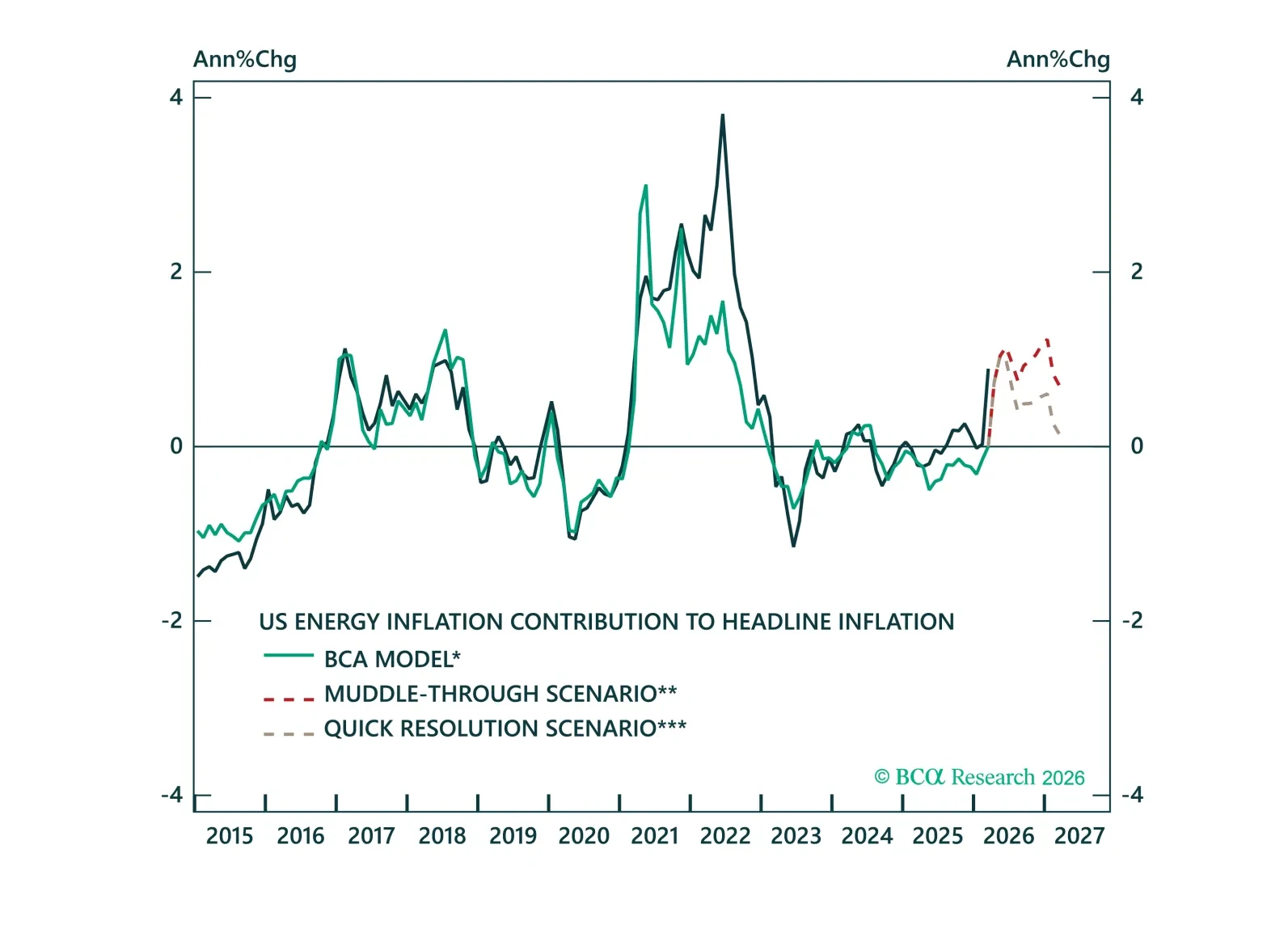

Volatility is high, but the path for yields is clearer than it looks. Across three oil scenarios, we show how policy responses shape fixed income markets and why the balance of risks still points to lower yields.