South Africa

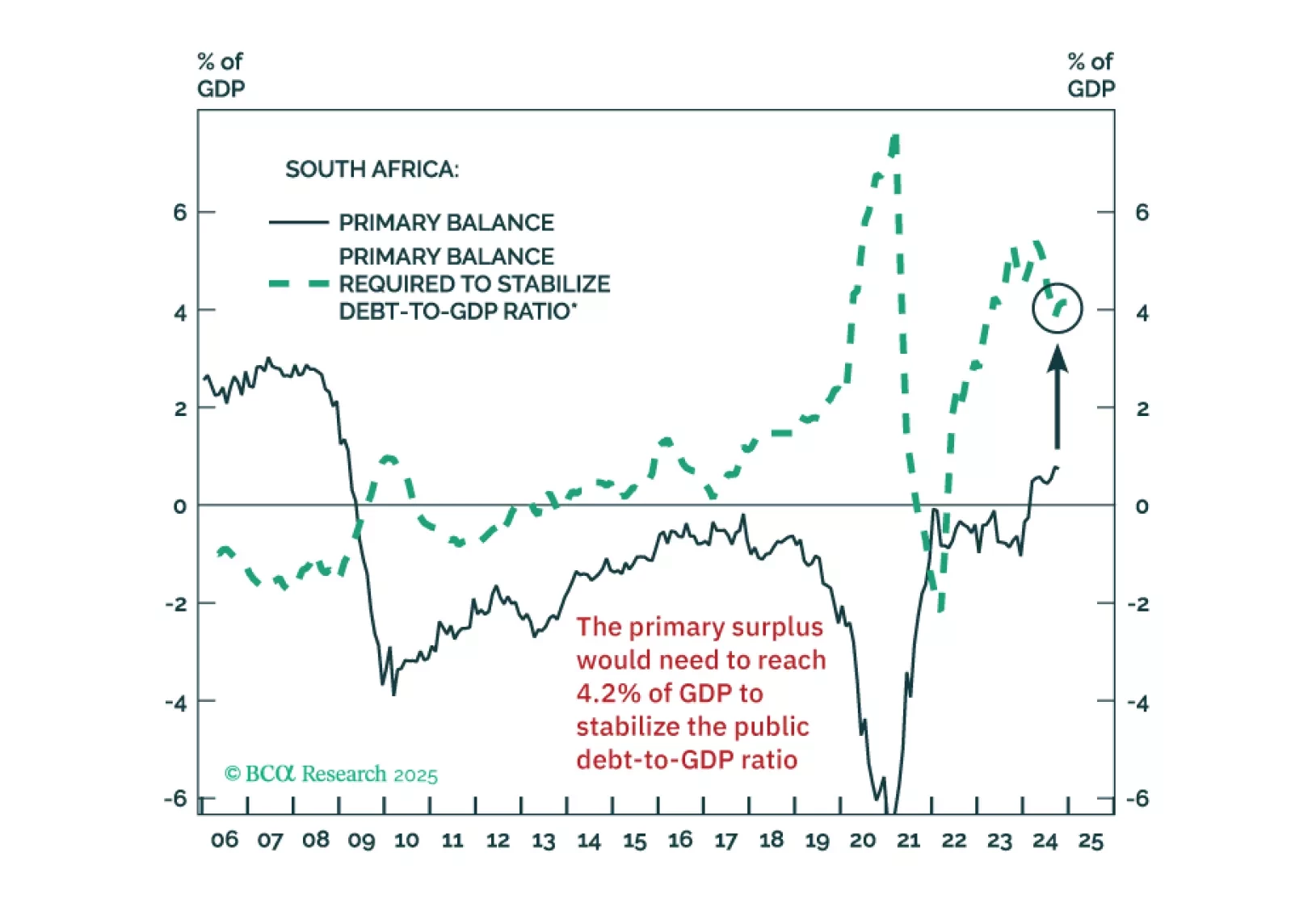

The South African government seems to believe that some fiscal retrenchment can stabilize the public debt-to-GDP ratio. But that’s a misconception. The country will need draconian spending cuts to achieve this.

The new national unity government in South Africa creates a geopolitical opportunity that investors should not bet against in the short term. A broad-based rally is likely to unfold relative to other emerging markets. However, structural problems and distrust within the new coalition hold out significant risks over the long run.

Despite the economy being on the verge of a recession, the South African Reserve Bank will not ease policy meaningfully. Doing so will accentuate the currency depreciation, which, in turn, will push up bond yields – an outcome the central bank would like to prevent.

While 2024 will see various election risks, global geopolitical uncertainty is driven by the US election and its struggle with Russia, China, and Iran. The stock market can manage local domestic political risk. But it will correct upon a major outbreak of geopolitical uncertainty.