Semiconductors

Our political forecasting scored wins in 2023 but we failed to capitalize on it adequately in our trade recommendations.

Global smartphone demand will likely find a bottom in 2024Q1 and rebound modestly between 2024Q2 and Q4. Competition in the global smartphone market will intensify. Chinese phone makers will gain market share from Apple and Samsung. Continue overweighting Taiwanese stocks, including tech, within the global equity benchmark.

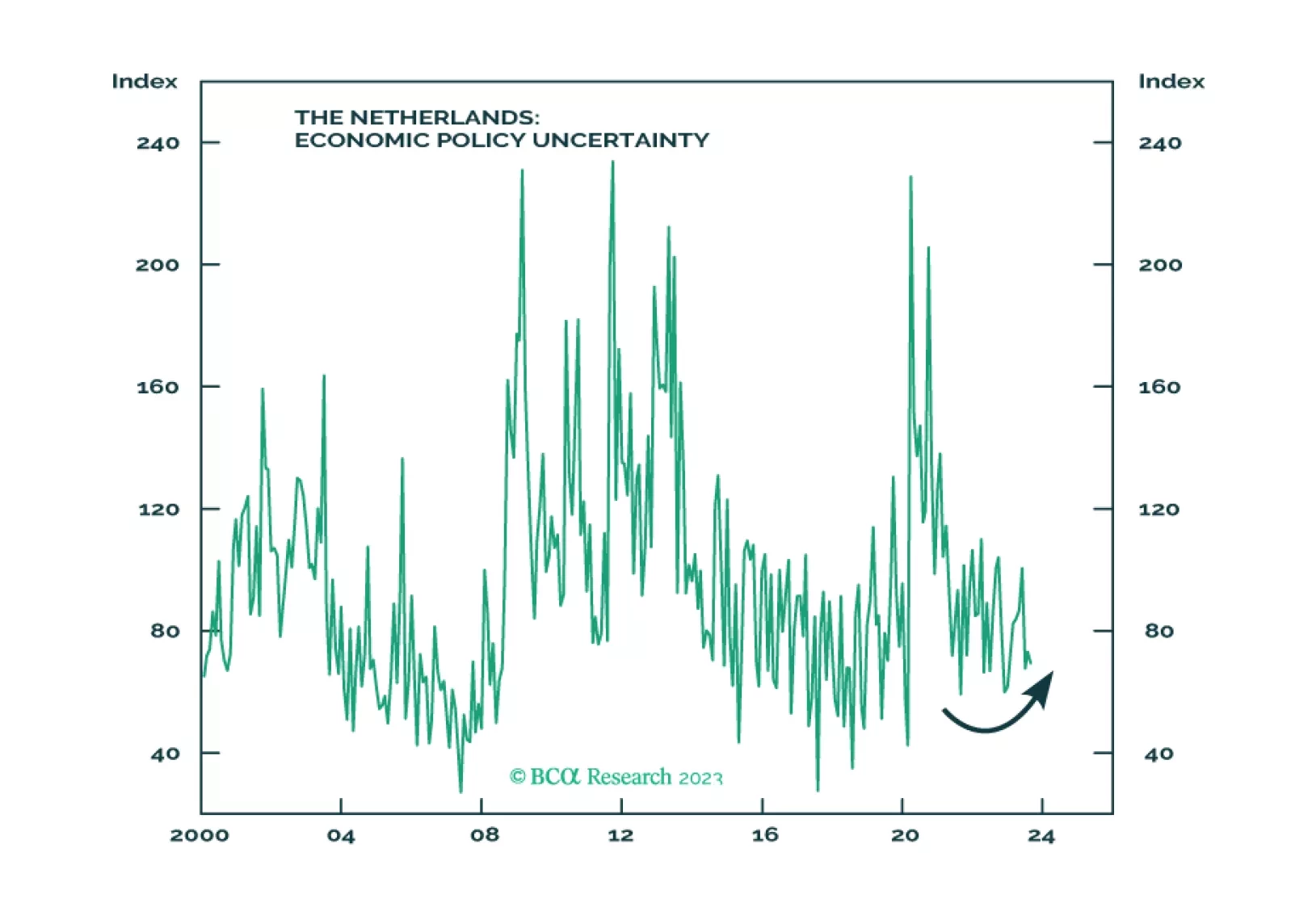

The Netherlands has a healthier and more stable economy and demography than its European peers. Investors should stay overweight developed European equities, including Dutch equities, relative to emerging European equities.

Outperformance of Growth sectors most likely has run its course. It is time to shift Growth vs. Value allocation to neutral, downgrade Semis, and upgrade Energy to overweight.

Global semiconductor demand will continue contracting, even though the pace of decline will moderate in 2023H2. While demand has increased briskly for Artificial Intelligence-type semiconductors, this will not be enough to lift aggregate global chip sales out of contraction. While momentum could push Emerging Asian semiconductor stocks higher in the short term, their share prices are vulnerable to the downside due to shrinking demand.

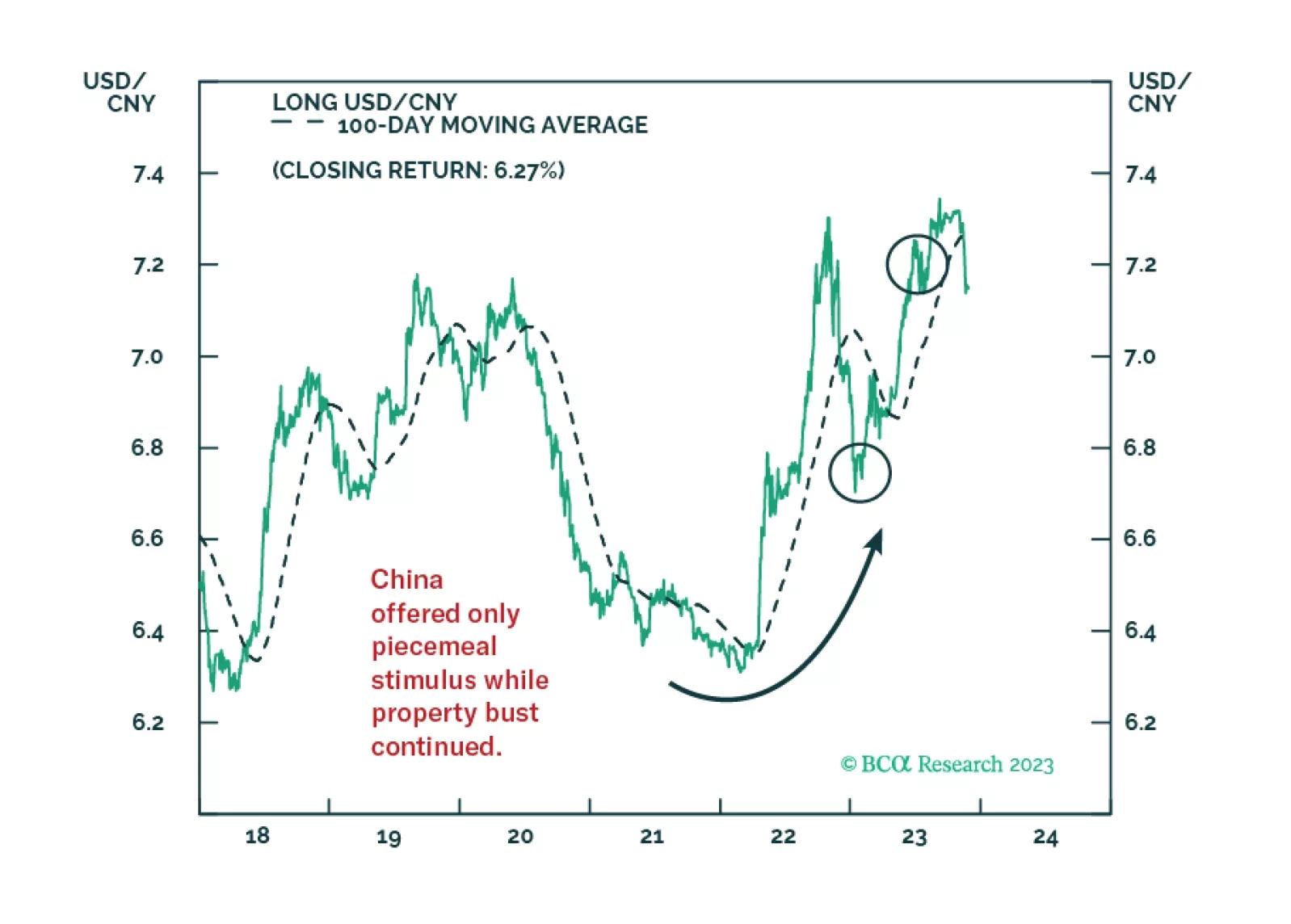

No, the secular rise in geopolitical risk has not peaked. EU-China trade ties underscore the multipolar context, but this multipolarity is unbalanced, as the US has not reached a new equilibrium with its rivals. While the second quarter is murky, investors should stay defensive this year on the whole.

Generative AI is a major technological breakthrough that holds tremendous economic and investment promise and will have sweeping effects on wide swaths of the economy. We are bullish on generative AI as a long-term investment theme. However, at the moment we observe hallmarks of an investment frenzy. We believe that there will be a more attractive entry point for patient investors.