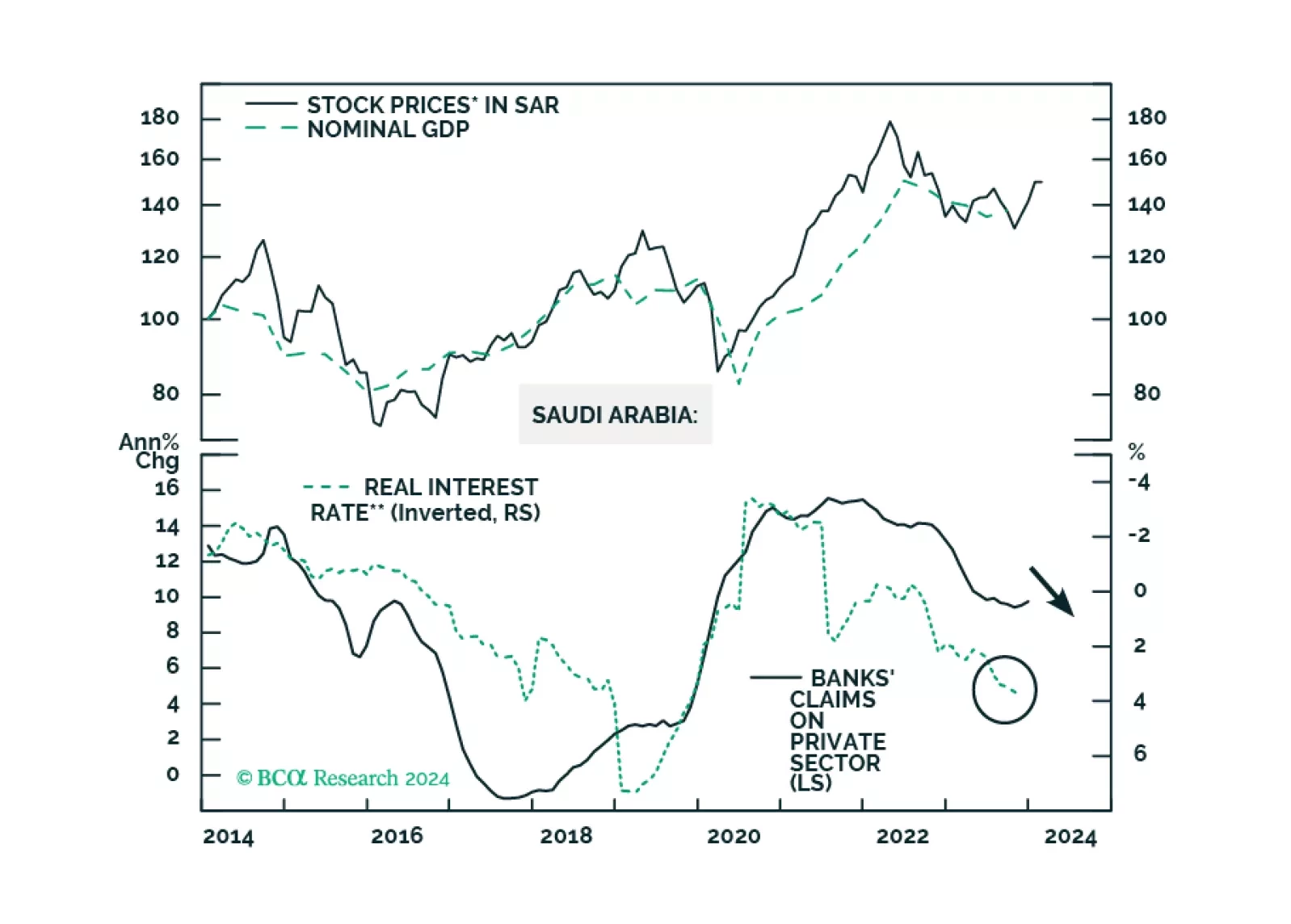

Saudi Arabia

The Saudi economy is facing internal and external headwinds. The geopolitical conflict is also escalating in the Middle East. EM equity portfolios should stay neutral on Saudi stocks. EM sovereign credit portfolios should upgrade Saudi Arabia from neutral to overweight.

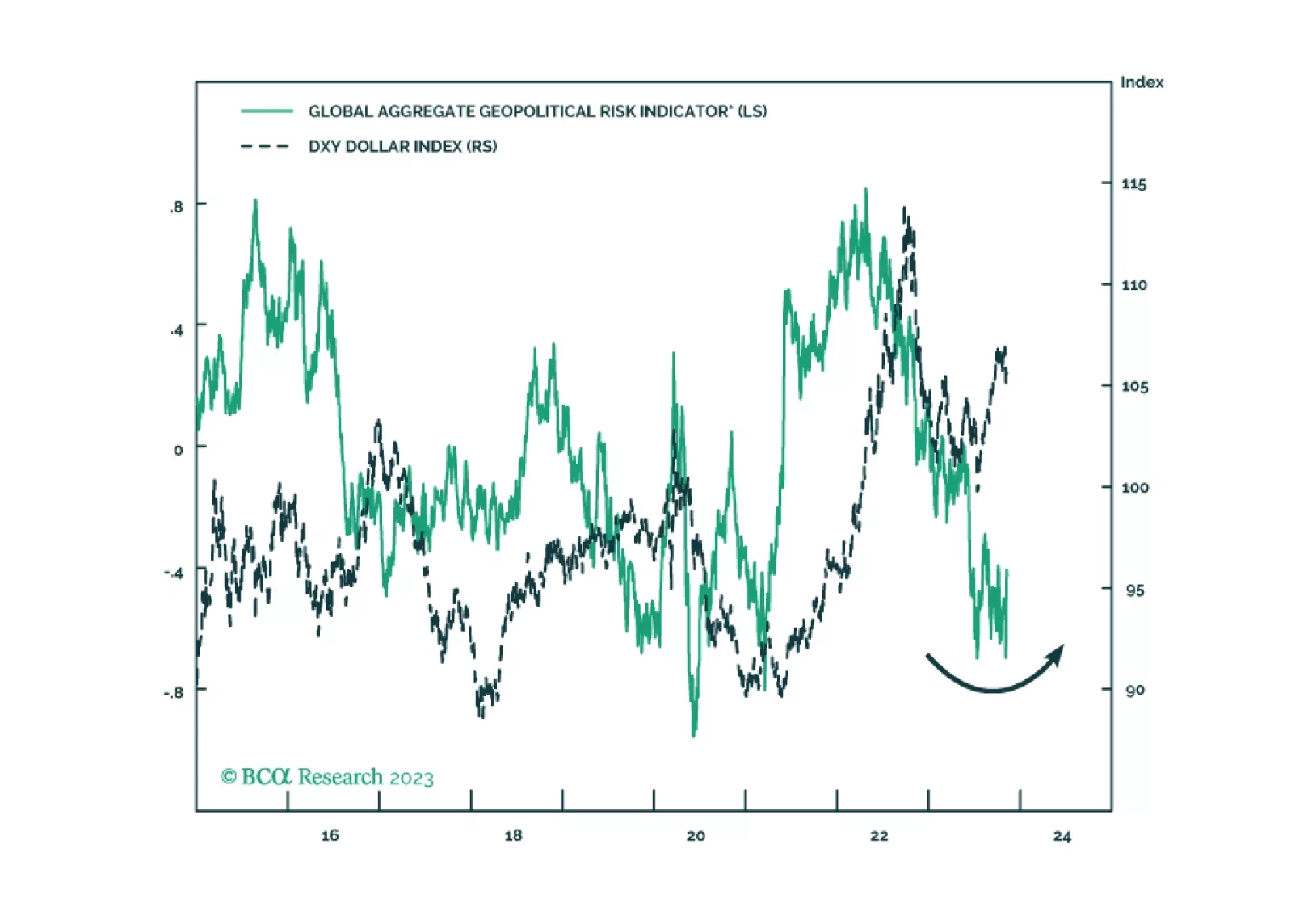

Amid a range of geopolitical narratives, what matters is that the US strategy of economic engagement with its rivals is failing, giving rise to a new strategy of containment that will reinforce the secular rise in geopolitical risk. Our market-based quantitative indicators of geopolitical risk are set to rise in the coming year.

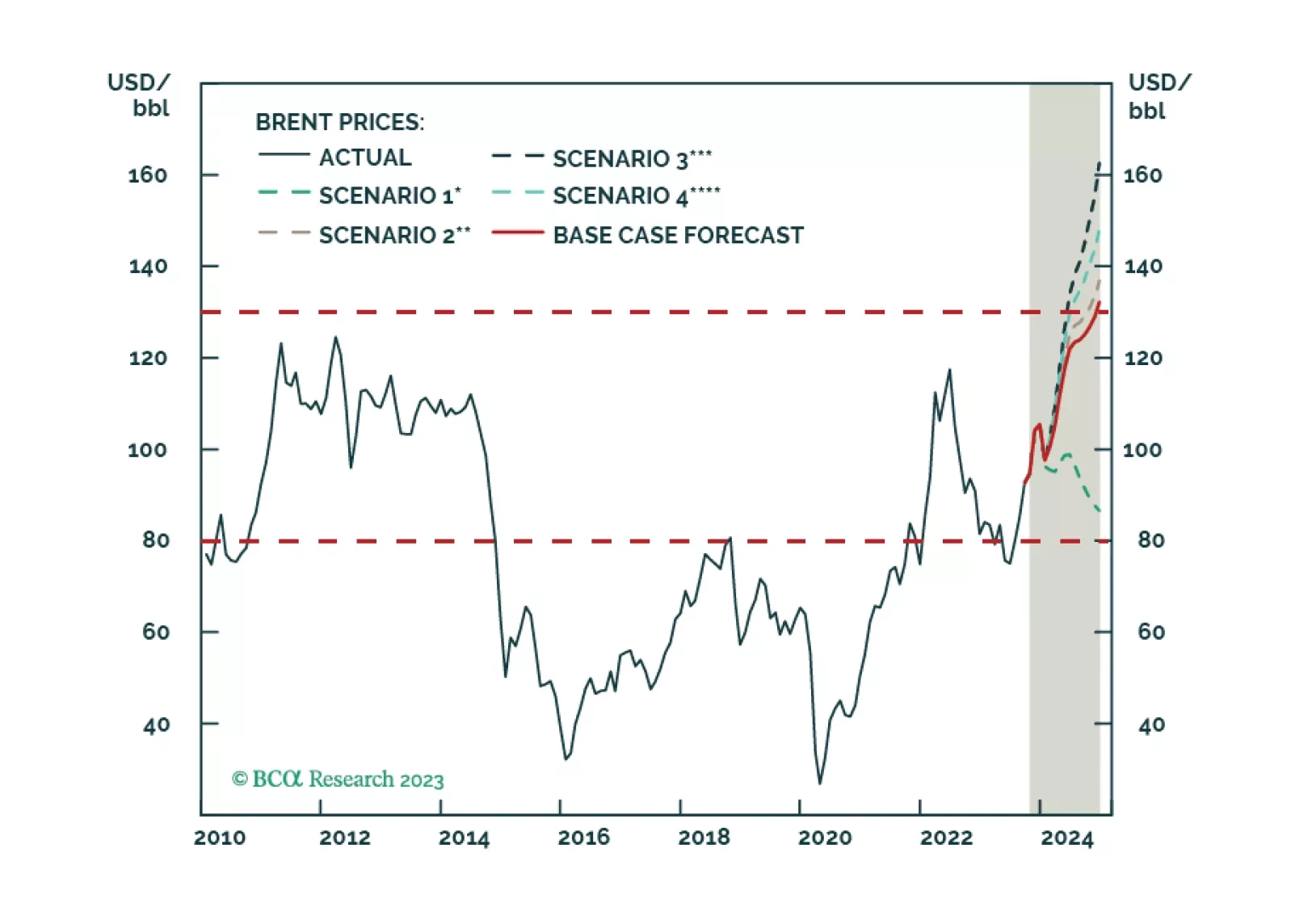

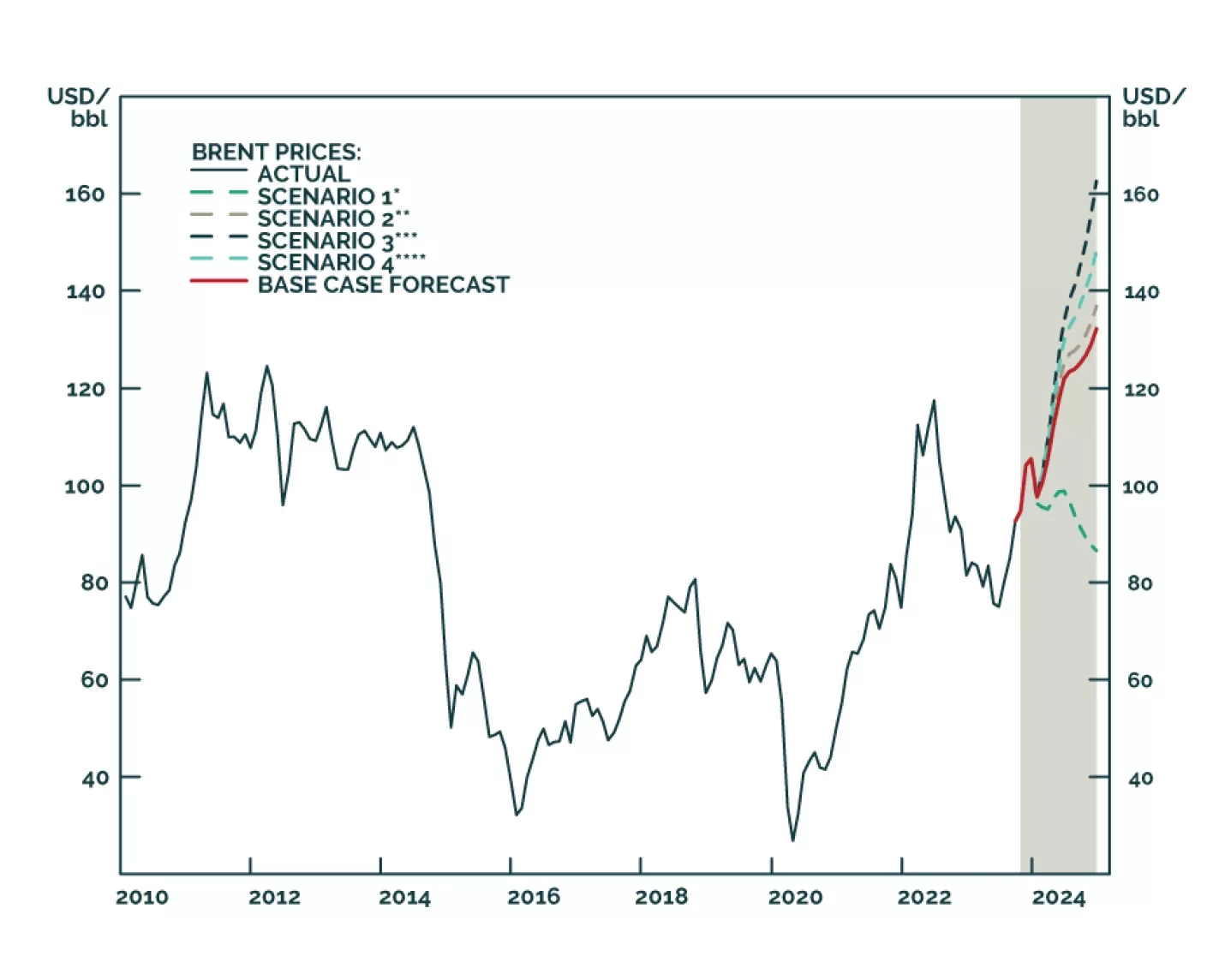

Investors should reduce risk, increase allocation to safe havens, and brace for oil price volatility and supply disruptions stemming from the Middle East over the next zero-to-12 months.

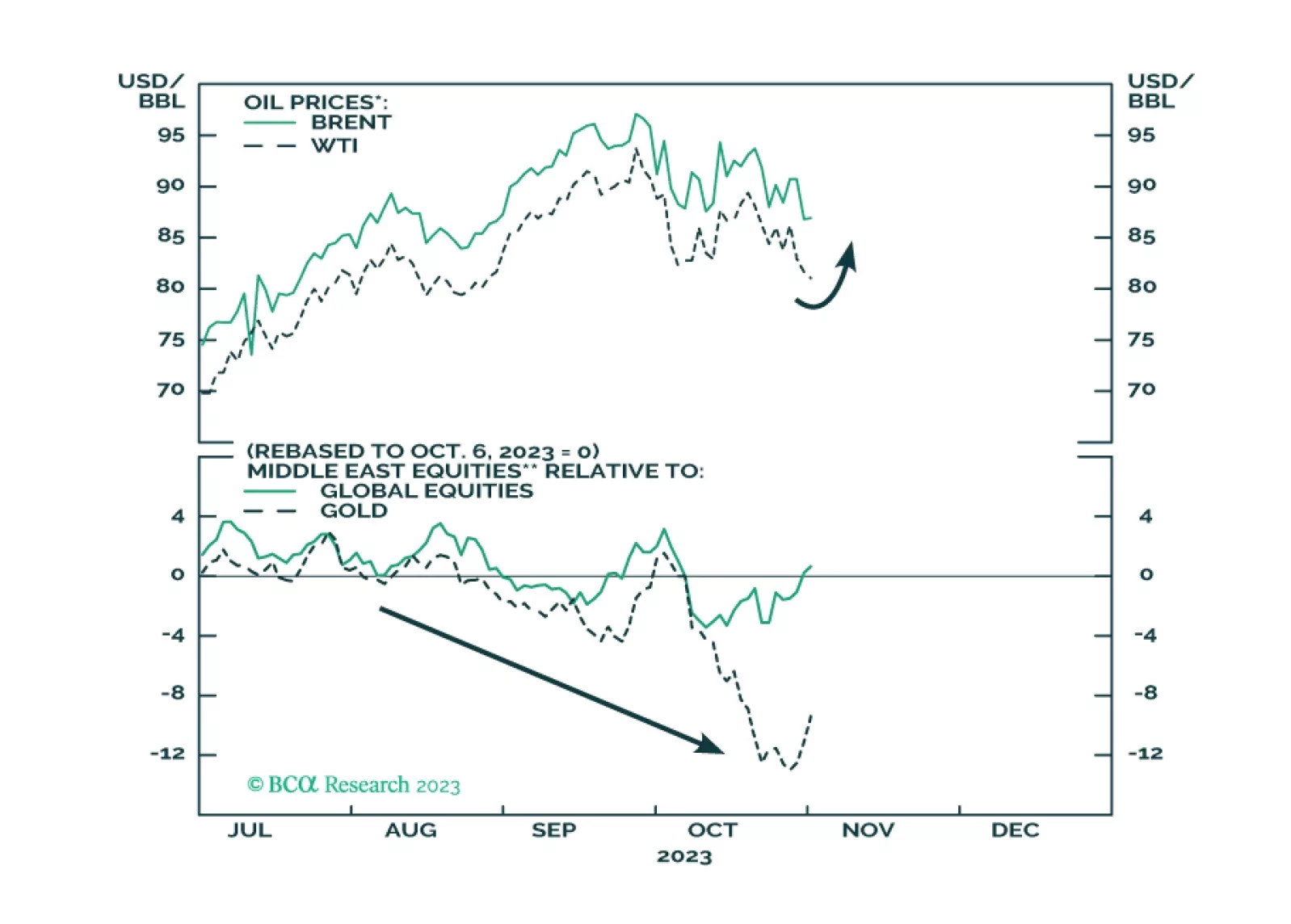

Economic fragmentation will accelerate in the wake of the Israel-Hamas and Russia-Ukraine wars. China’s fis-cal support for its economy; a still-strong US economy, and the preparation for a wider war in the Middle East involving Iran will elevate volatility and bias oil prices upward. We remain long equity and commodity exposure via the XOP, XME and COMT ETFs.

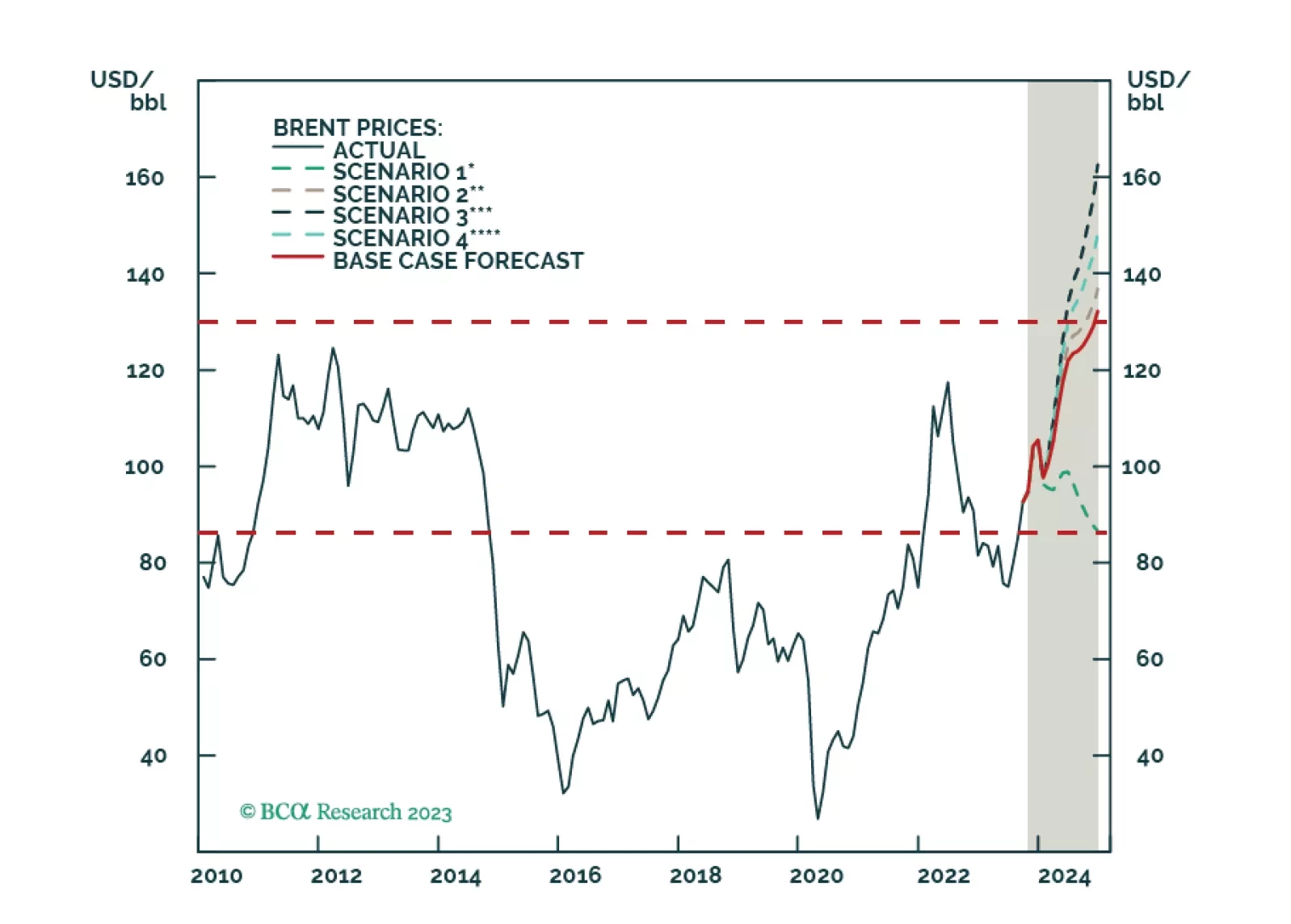

The US and core OPEC 2.0 are – wittingly or not – laying the groundwork for a price band with a floor and cap on oil prices – at $79/bbl and $130/bbl, respectively – “at least” to May 2024. This accommodates multiple goals for both. To meaningfully support policy, the US would need to scale up purchases to refill its SPR. We remain long the XOP and COMT ETFs for direct exposure to energy E+P equities and commodities.

Despite higher uncertainty, our Brent price forecasts remain unchanged at just over $101/bbl for 4Q23 and $118/bbl for next year. We remain long equity exposure to oil and gas producers via the XOP ETF, and commodity exposure via the COMT ETF. We also remain long $100 Dec24 Brent calls and long 1Q24 Brent futures vs. short 1Q25 Brent futures in anticipation of stronger backwardation.

Volatility will remain the key dynamic in oil markets in the aftermath of the surprise Hamas attacks against Israel on October 7. The risk of a major oil supply shock has gone up, but meanwhile supply constraints will remain at variance with global growth problems stemming from restrictive monetary policy over the next 12 months. Favor bonds over stocks, large caps over small caps, defense and energy stocks over other cyclicals, and US equities relative to global equities.

Investors should underweight global equities and risk assets; overweight US stocks relative to global; and overweight defensive sectors versus cyclicals.

China’s economic and diplomatic interests in the GCC region will expand, as will its military presence. Whether or not this stabilizes the region is yet to be determined, particularly if tensions in the South China Sea and other international waters traversed by both the US and China escalate. Underlying risk in energy markets will remain elevated. We remain bullish energy generally, and continue to favor equity ETF exposure to energy (XOP and XME), and commodity exposure via the COMT ETF.