Policy

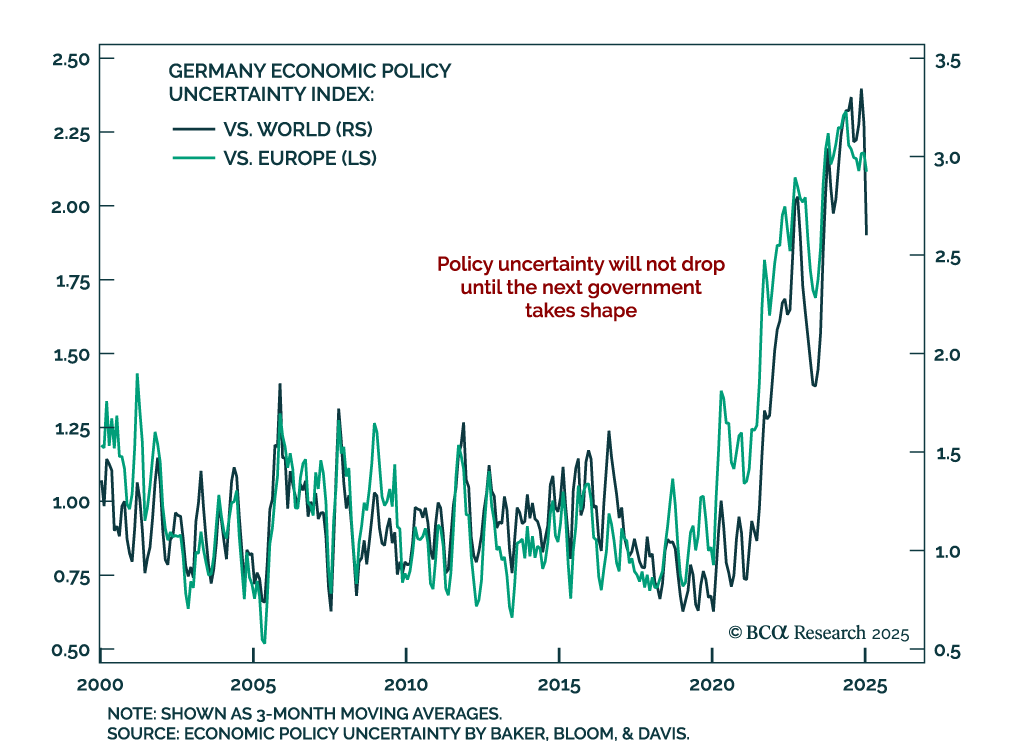

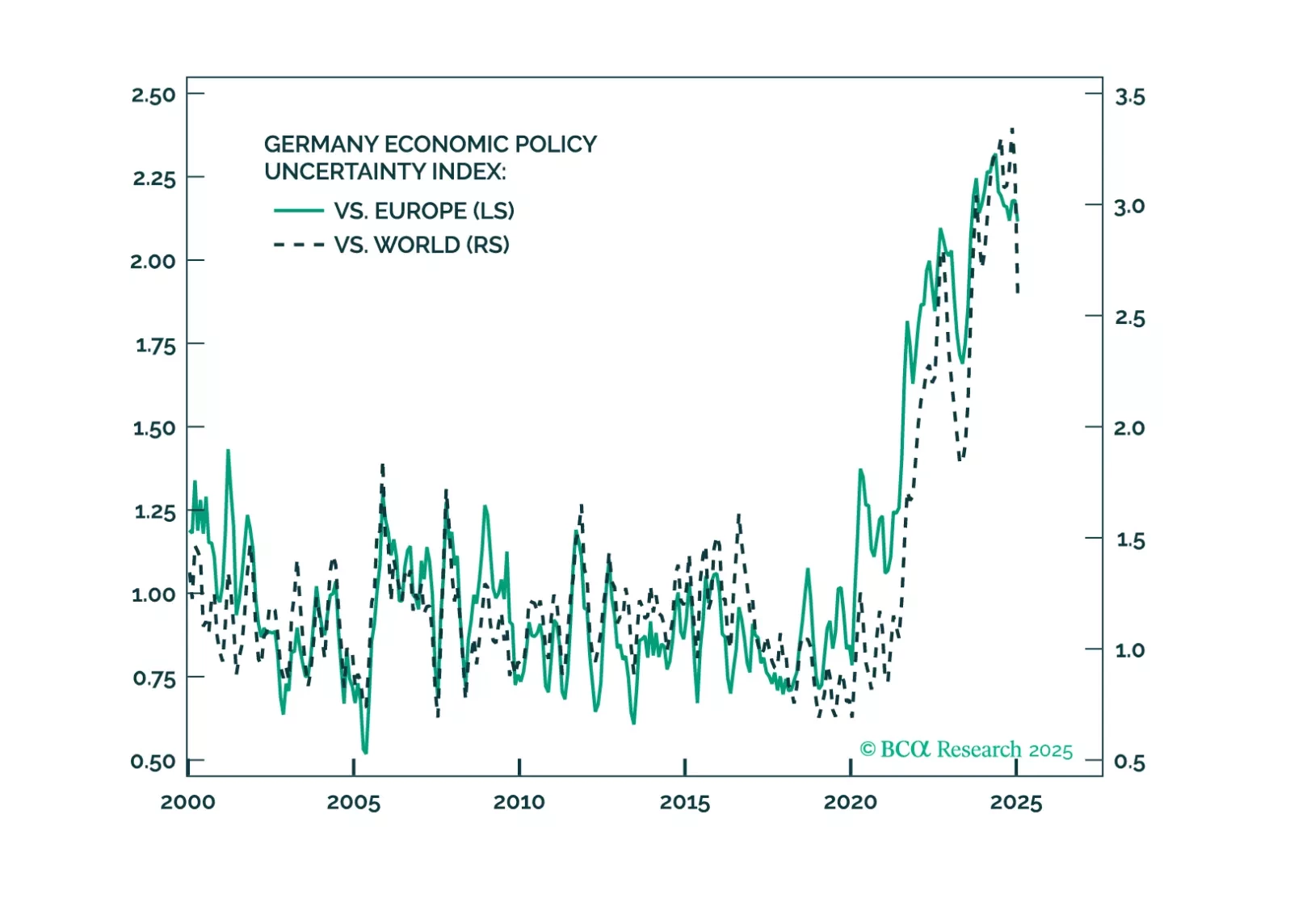

The rise of the far-right is challenging mainstream German politics. The CDU/CSU and SPD will govern Germany again after the election. A ceasefire in Ukraine will offer some relief, but Trump’s policies will keep tensions high.

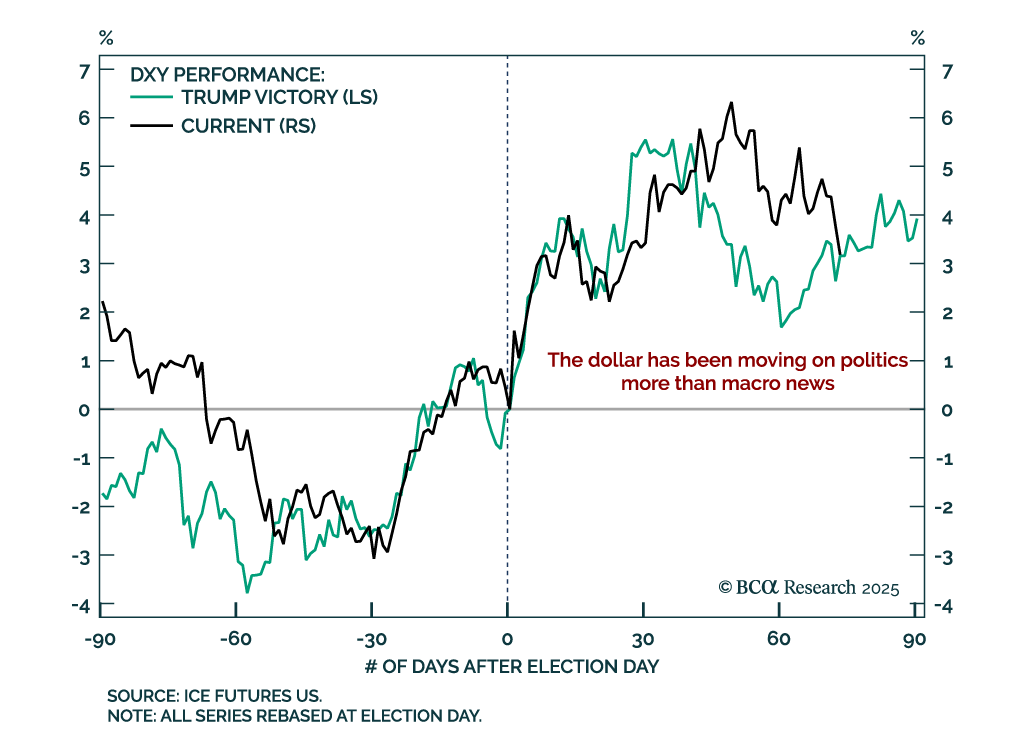

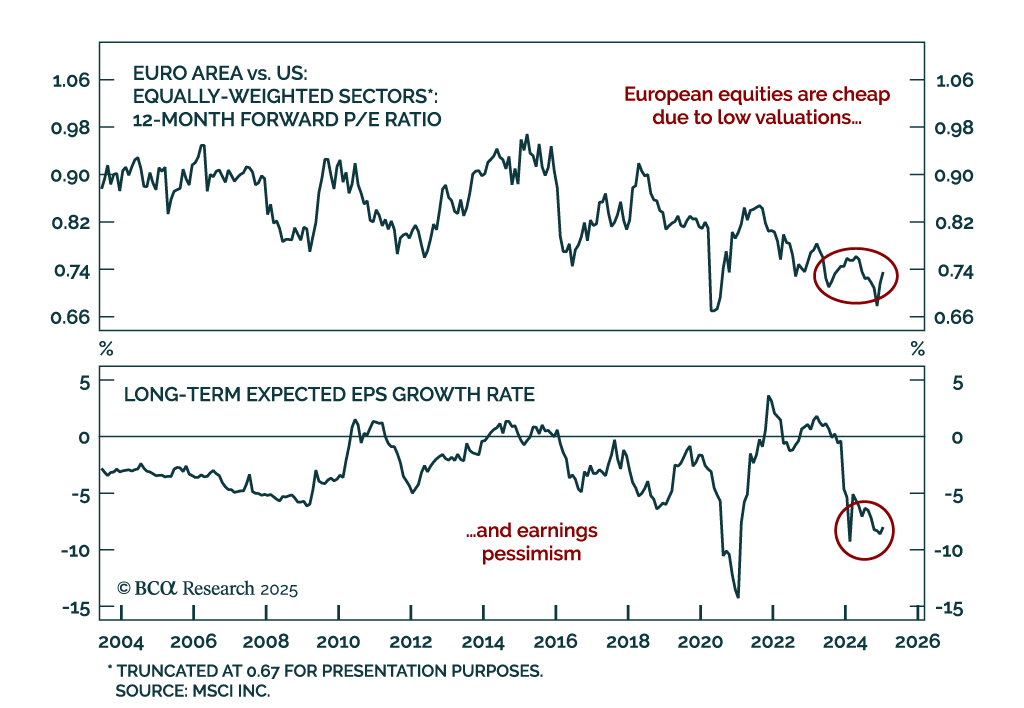

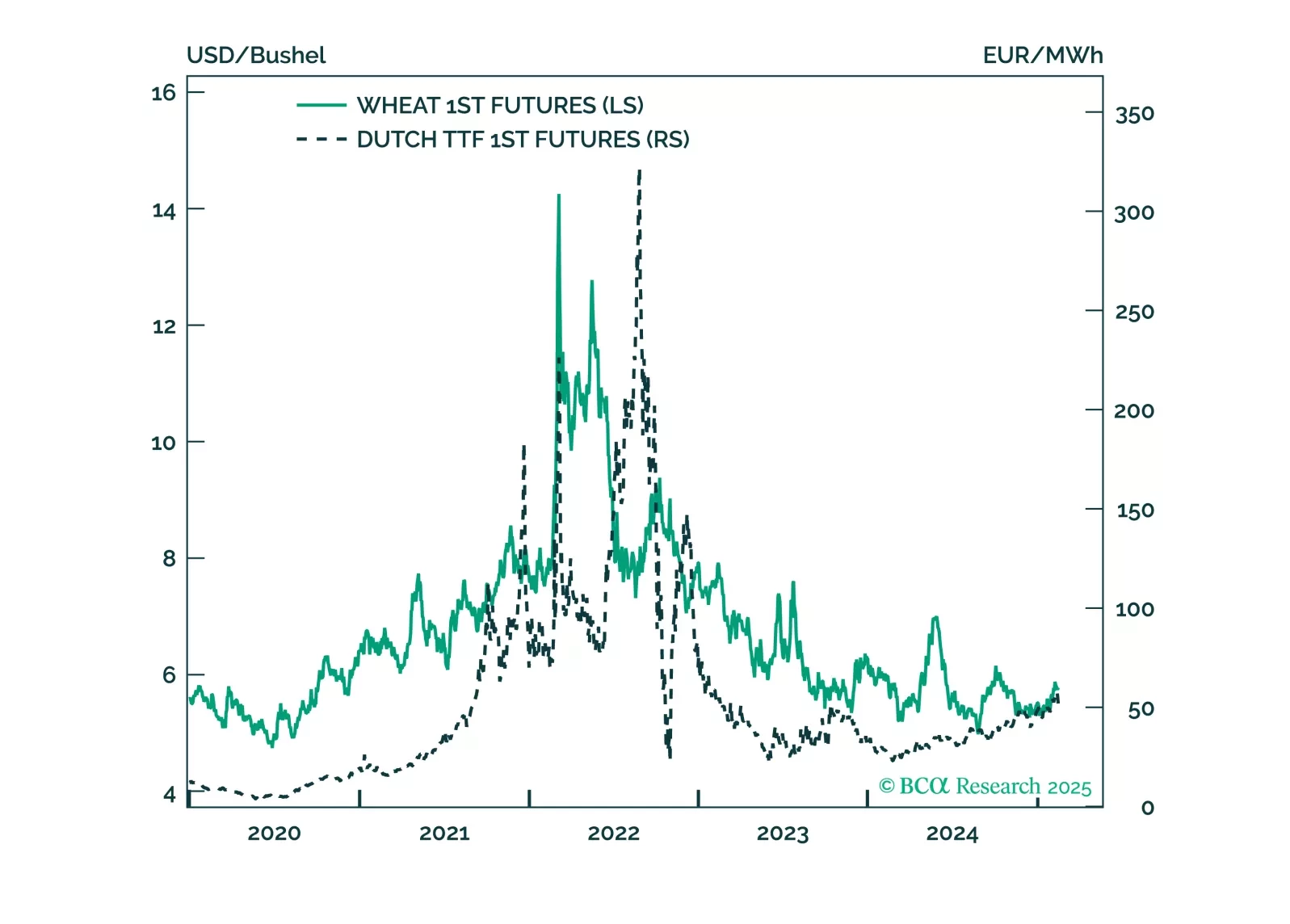

President Trump is negotiating a ceasefire in Ukraine. This will be a marginal headwind to some commodities which benefitted from the conflict like natural gas and wheat, and will be a marginal tailwind for European assets, specifically EM Europe. Use Trump’s tariff shock as an opportunity to buy European assets.

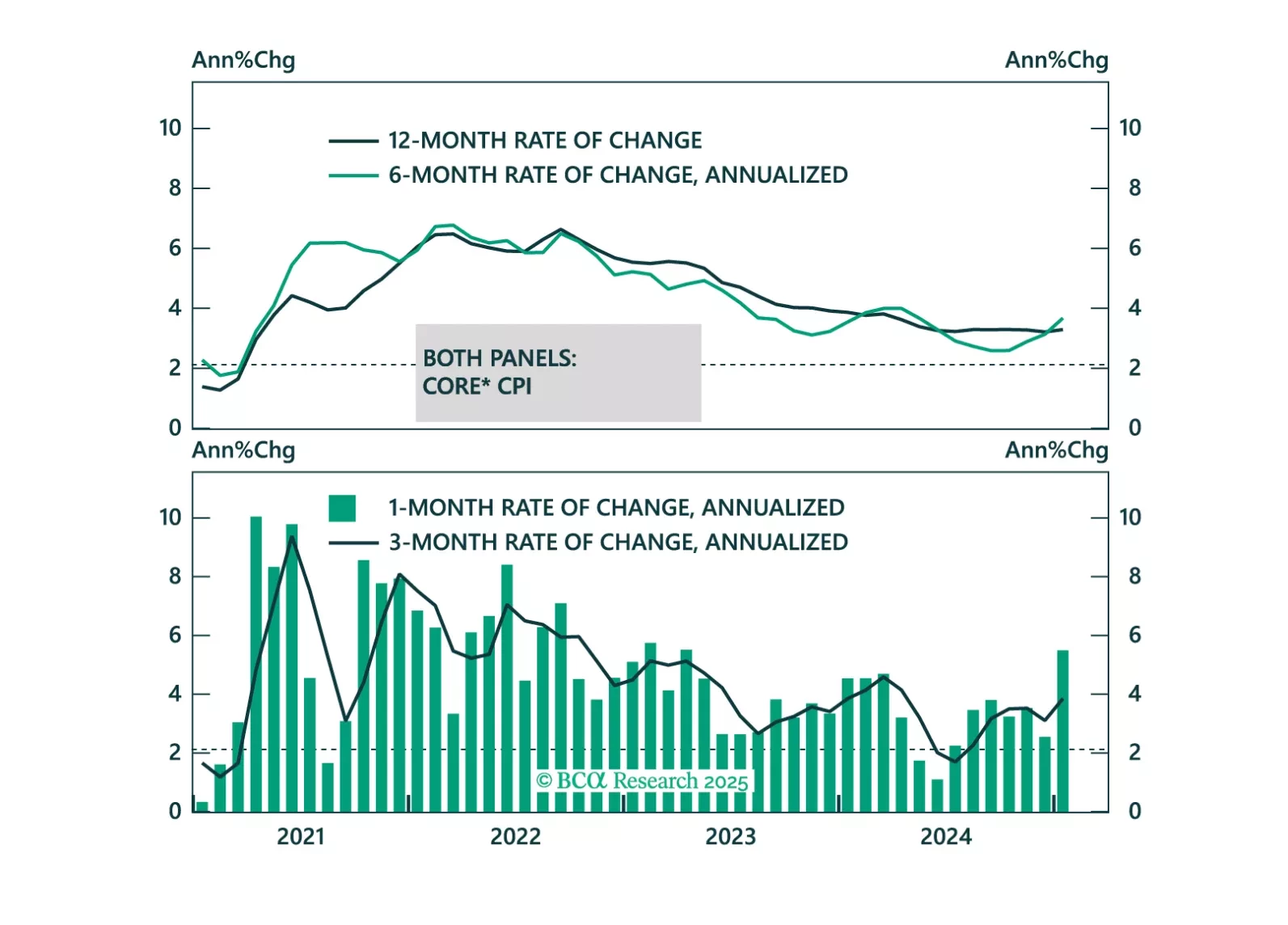

Some thoughts on this morning’s CPI report and its implications for the Fed and Treasury yields.

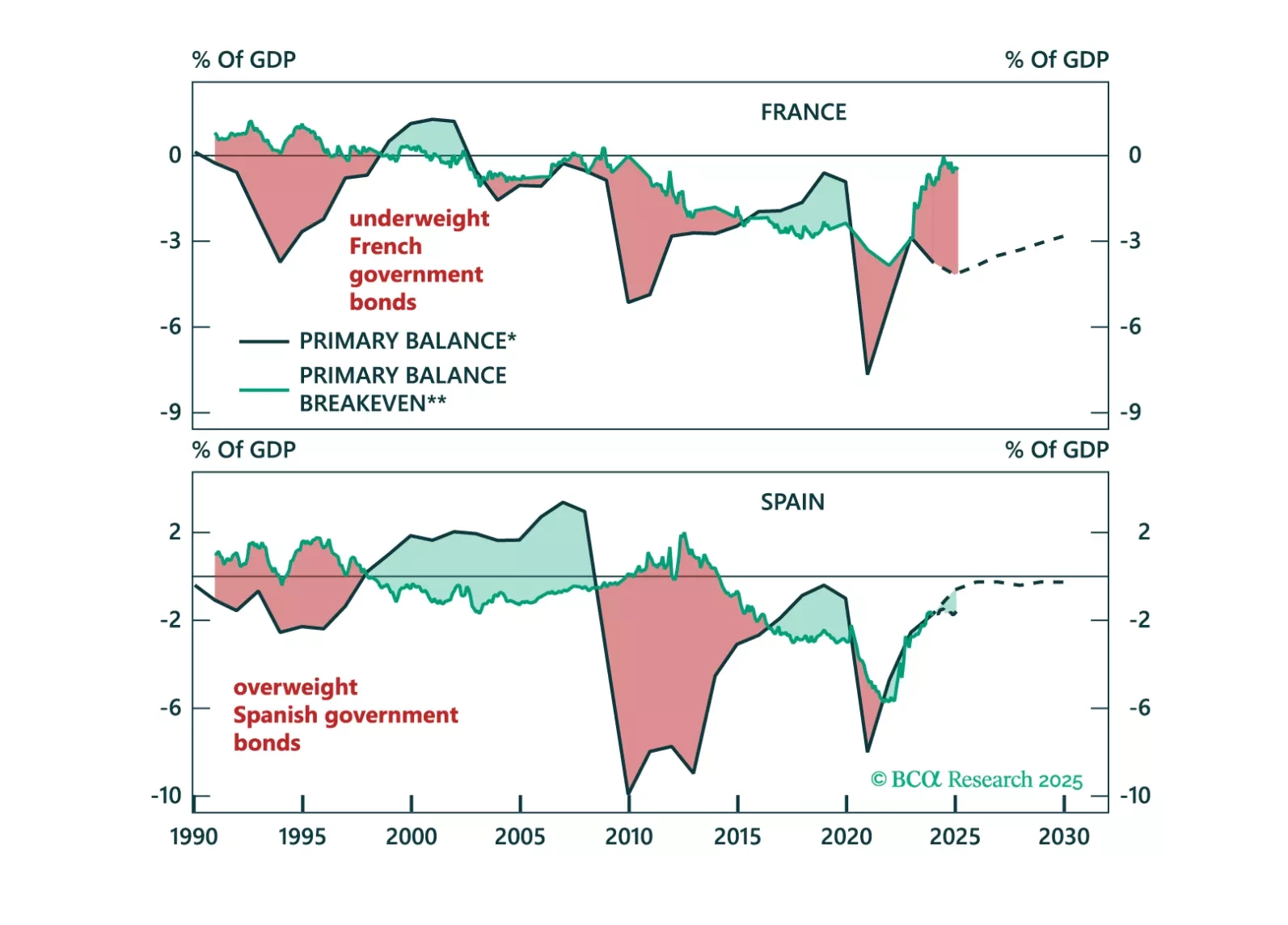

Questions about fiscal risks and their impact on bond markets have become more frequent in client conversations. This Special Report provides a framework to assess a country’s fiscal sustainability and how it affects its bond market outlook. On an individual country basis, Spain has shown a remarkable turnaround in its fiscal sustainability outlook while the fiscal outlook for France continues to deteriorate.