Mega Themes

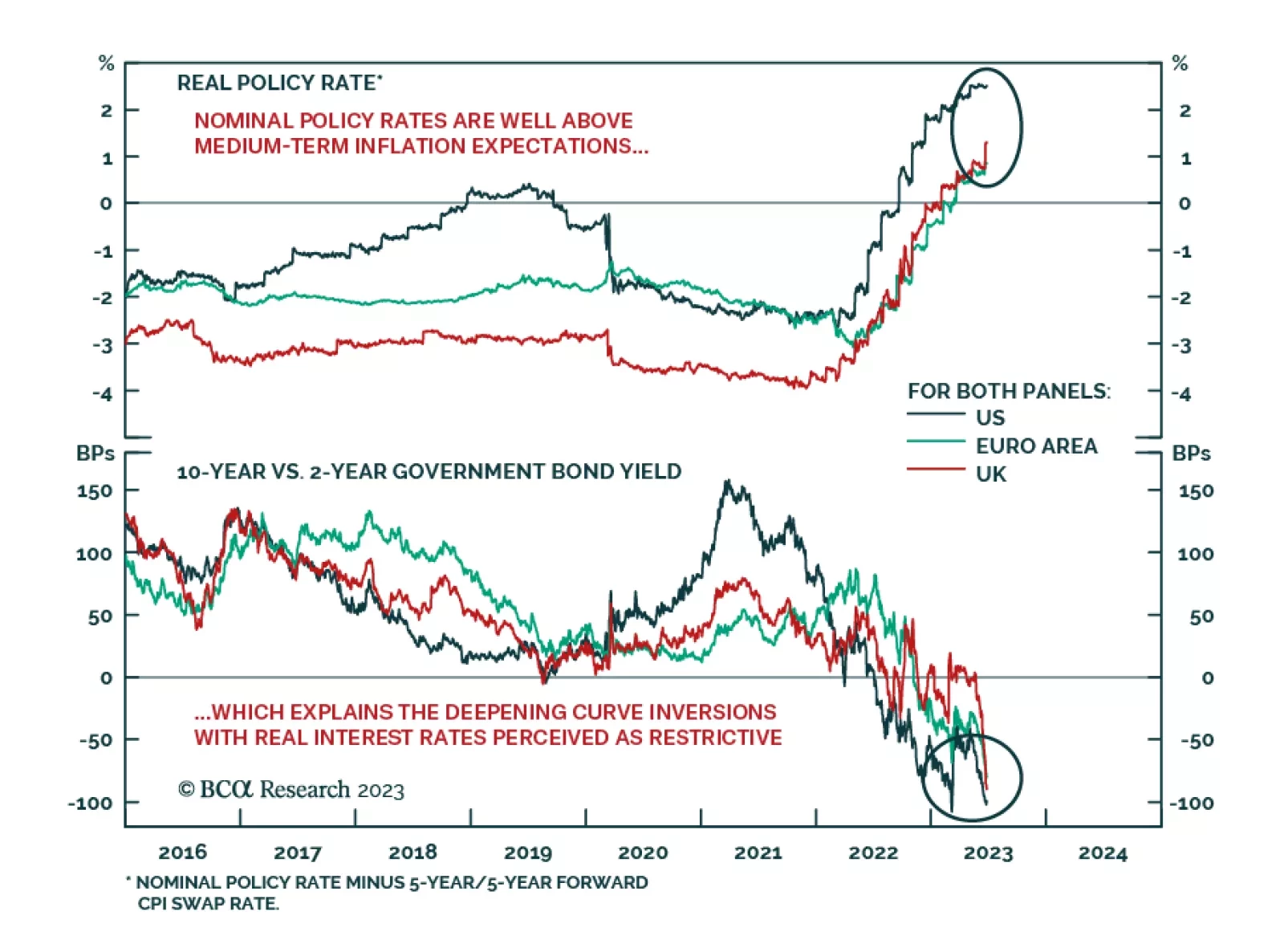

The market does not grasp the implied depths of recessions that will be needed to prevent inflation expectations from un-anchoring. Among the major economies, the most vulnerable to a deep recession is the UK. We explain why, and some investment implications. Plus: the yen is a rebound candidate, while Japanese equities are a reversal candidate.

This week’s Special Report updates our US default rate forecast and considers whether corporate bond spreads offer value given the trend in credit fundamentals. We also consider the relative value proposition between investment grade and high-yield credit and between European and US corporate bonds.

Assuming yesterday’s policy rate hike is a sign that Turkey is finally veering towards orthodox economic policies; should investors rush in?

Machine learning has made significant progress in the physical sciences, although it has some ways to go in the social sciences. When asked to make predictions on oil markets, ChatGPT's responses lack in-depth analysis given its inability to understand the language and think critically. While in its current form, AI cannot replace forecasters, its wide breadth of 'knowledge' makes it useful in developing forecasting frameworks in unfamiliar domains.

We are strategically bullish on the outlook of the energy sector. Domestic and external political constraints asserted themselves, restraining the most negative impulse against this sector by the Biden administration. Go long energy versus cyclicals (ex-tech).

China is facing a risk of deflation. Marginal interest rate cuts and targeted stimulus will be insufficient to boost China’s growth given the current deflationary mindset and the danger is that the economy may be entering a liquidity trap. Deflation is bullish for government bonds, but negative for equity prices. Chinese share prices will continue to decline.