Mega Themes

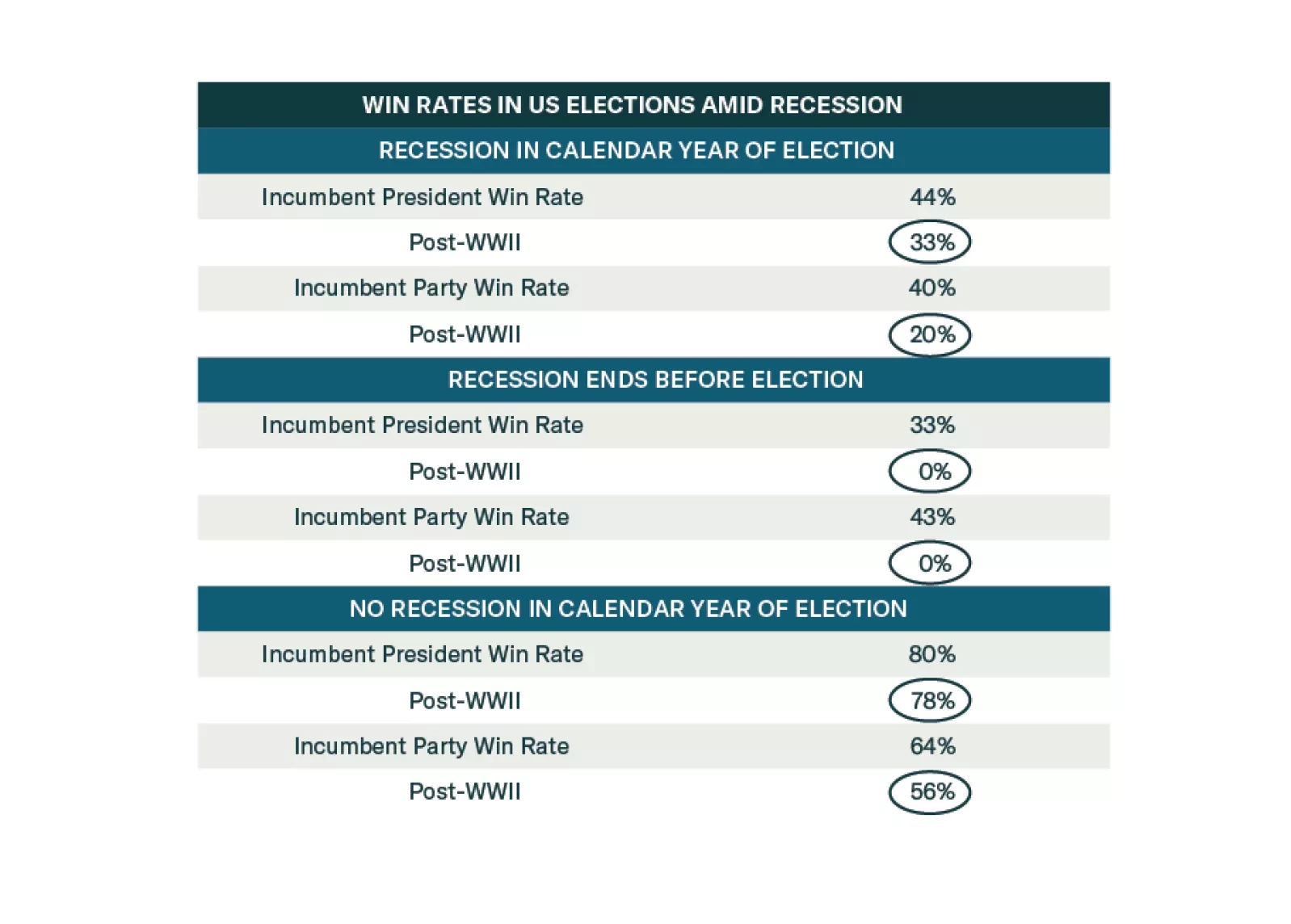

Democrats are favored to win the election until recession materializes. But recession risks are high. Investors should adopt a defensive and conservative strategy in 2024 amid extreme US policy uncertainty.

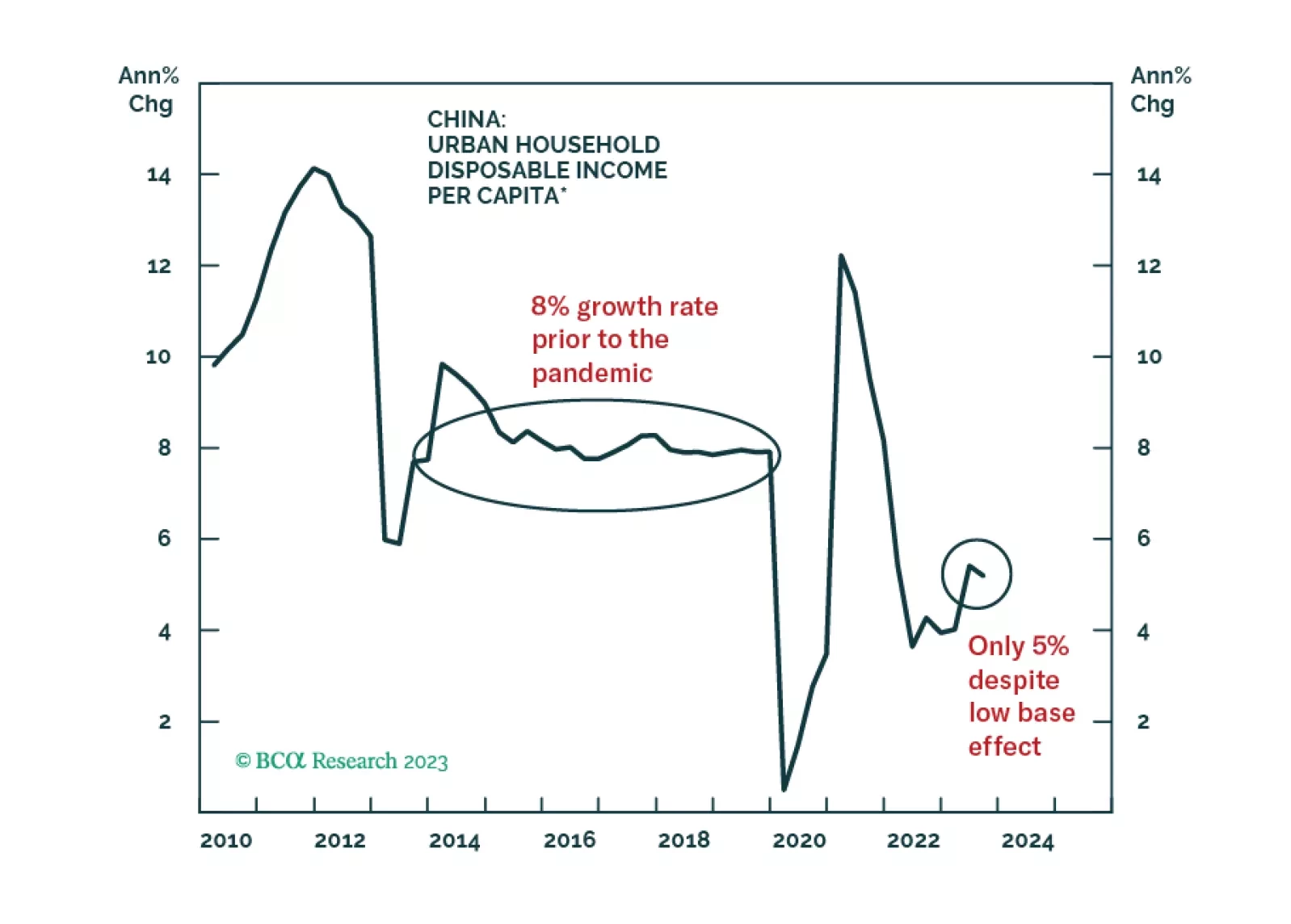

The overarching macro theme for China in 2024 will be deflation and its impact on the economy, macro policies, and financial markets. Widespread deflation, in combination with high debt levels and falling real estate prices, has unleashed debt deflation and balance sheet recession dynamics. The latter are rendering monetary policy inefficient.

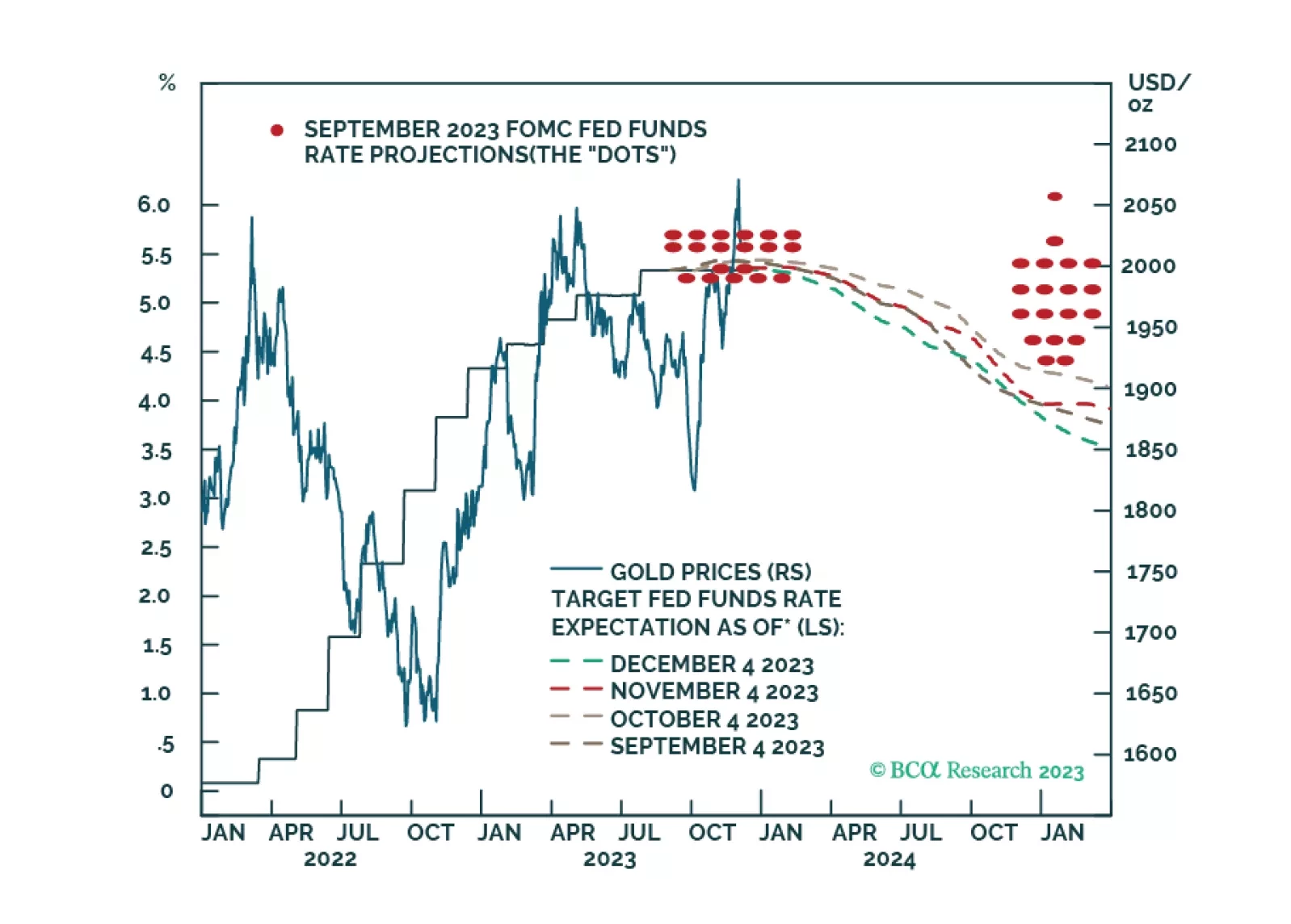

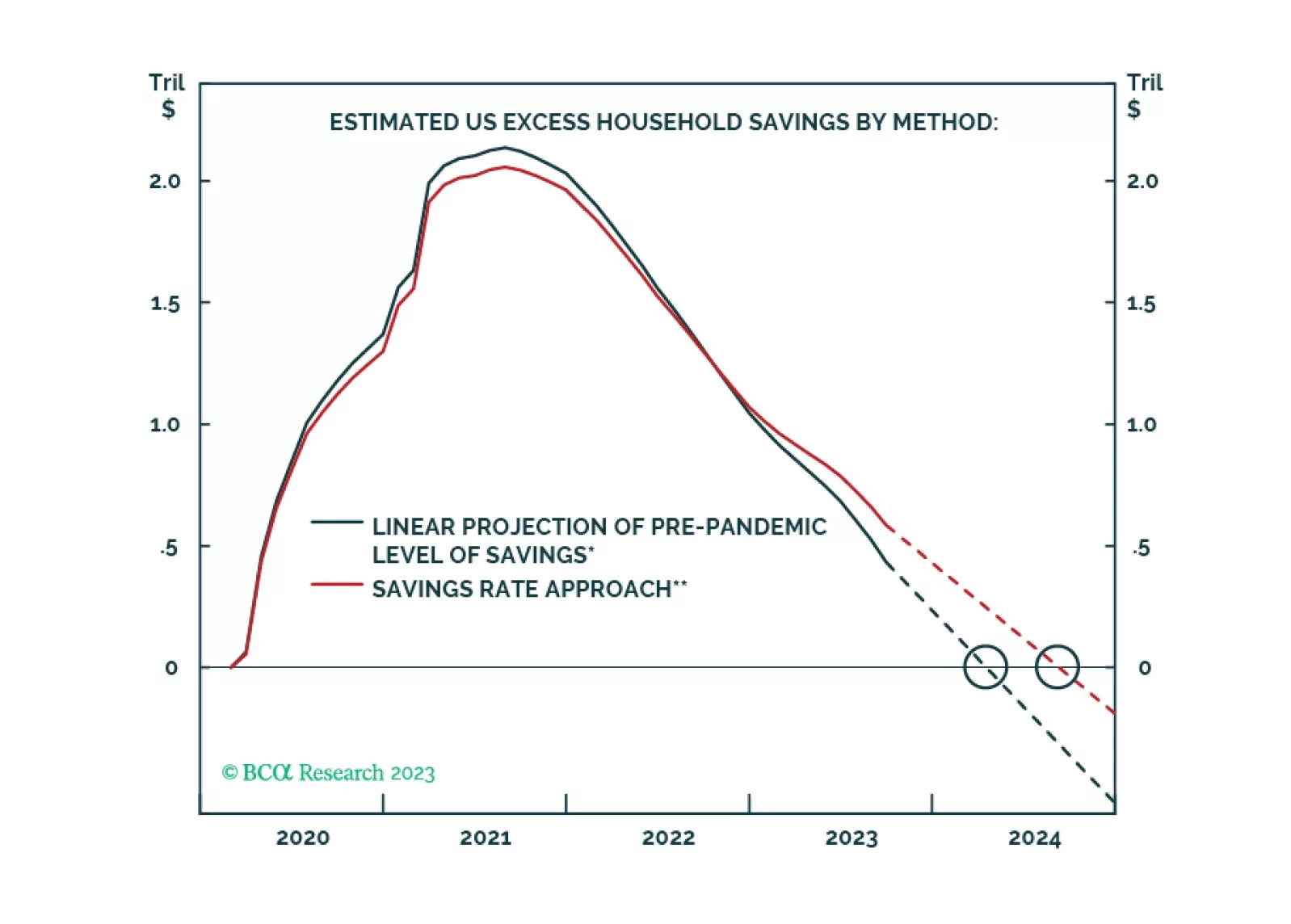

Falling core inflation in the US over the short run will boost real disposable household income, which will keep consumption – ~ 70% of US GDP – strong. Over the medium- to-longer term – 3 to 5 years out – inflation risks rise as fiscal dominance becomes the Fed’s modus operandi, and economic fragmentation becomes entrenched. War and the expansion of war remains an inflation risk. In this environment, gold remains our preferred hedge.

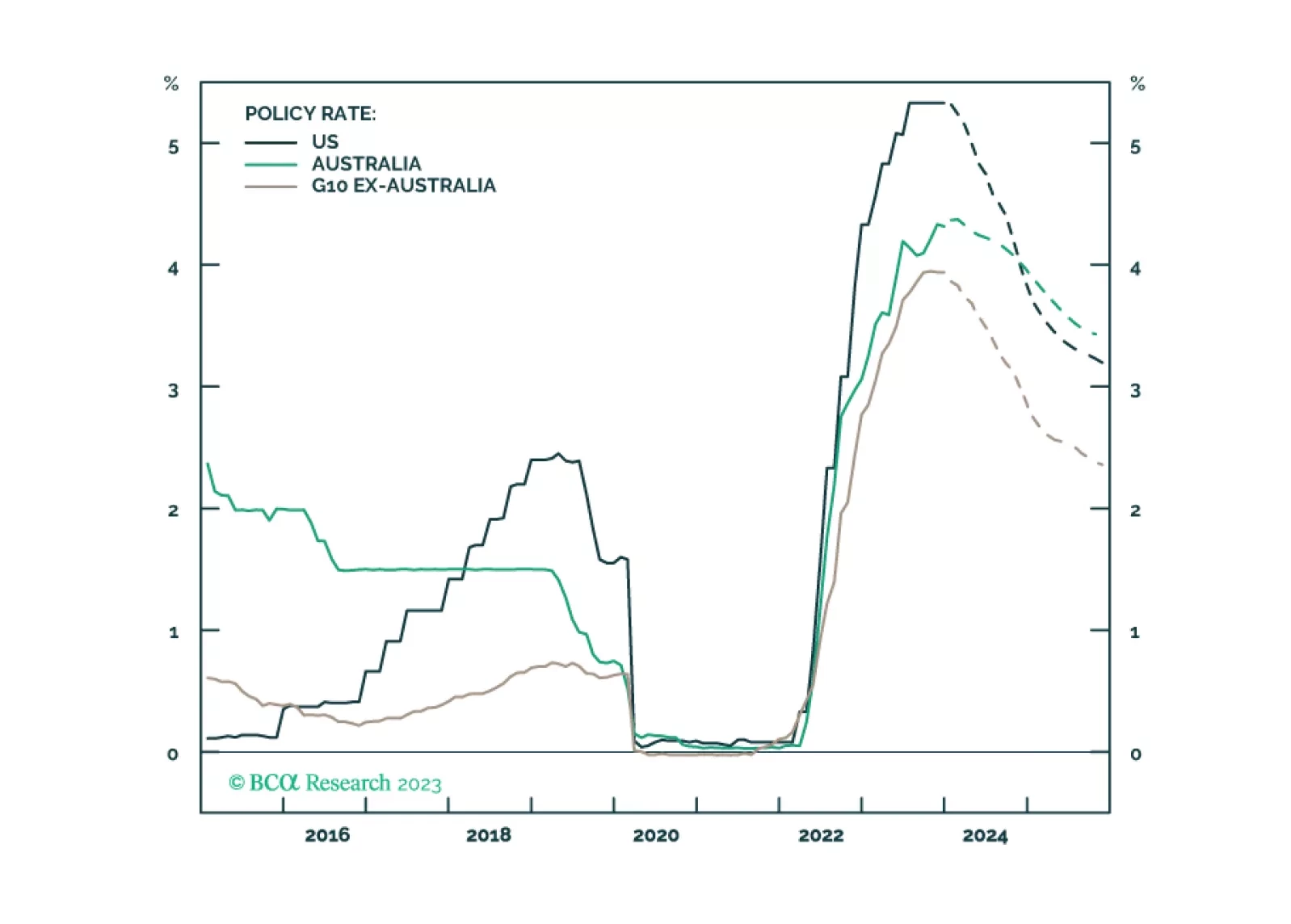

In this Special Report, we take an in-depth look at the outlook for monetary policy in Australia and discuss the impact of an elevated policy rate on the economy. We recommend an underweight country allocation to Australian government bonds and look for opportunities to go long the Australian dollar.

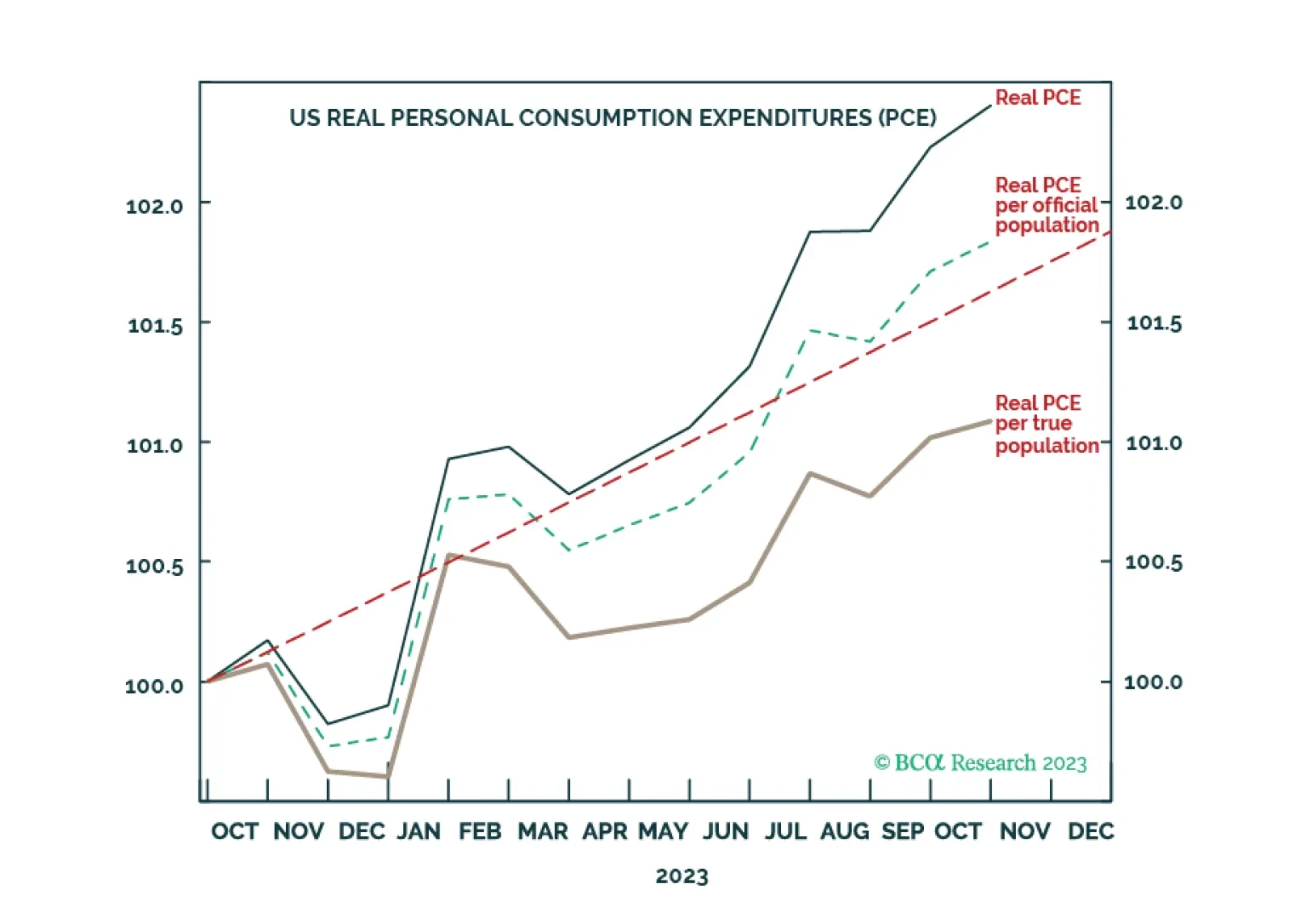

Illegal immigration into the US has skyrocketed to record levels. Correctly accounting for this, US real consumption growth on a per head basis is already fragile. Meanwhile, the real bond yield is only now approaching the pain point that typically triggers a recession. Ahead of the upcoming US jobs report, we point out what it would take for the Joshi rule real-time US recession indicator to breach its event horizon. And how to position in stocks and bonds, both tactically and cyclically. Plus: potential turning points in Biotech and Genome, ADBE, and Taiwan versus China.

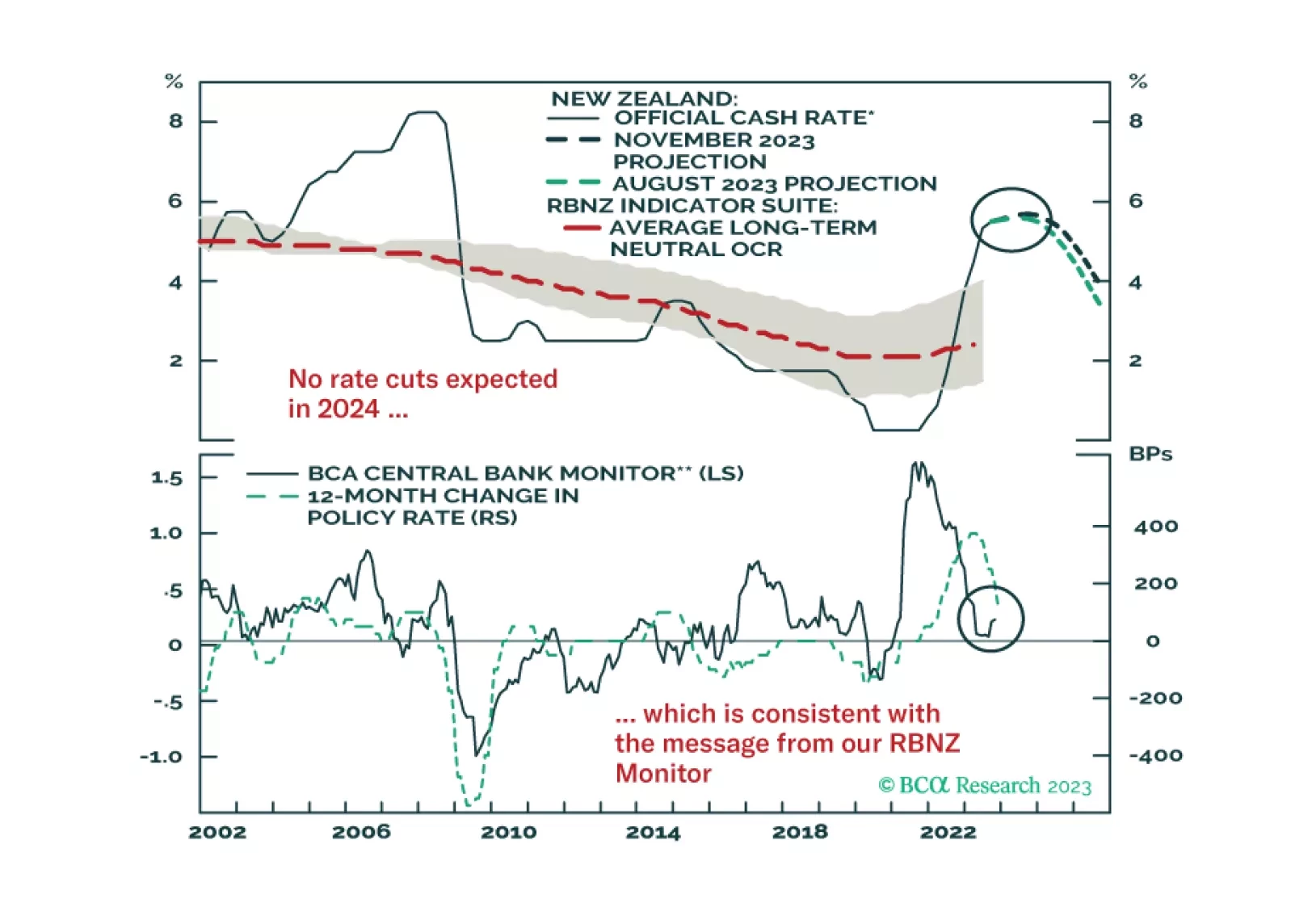

In this Insight, we discuss the outlook for monetary policy in New Zealand after this week’s RBNZ policy meeting, and introduce related fixed income and currency trade ideas.

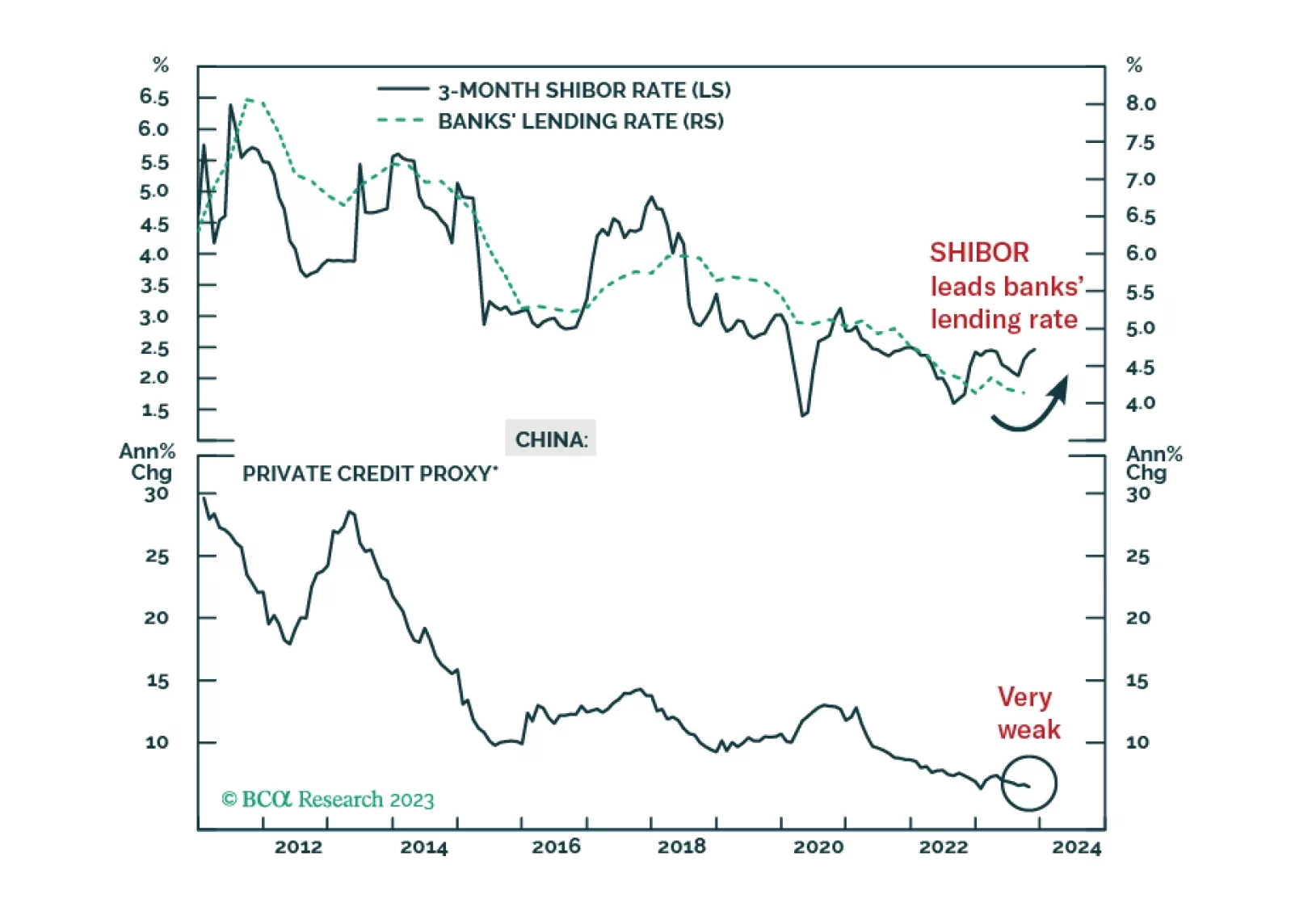

A cyclical recovery in China’s economy is still not imminent. The PBoC has tightened interbank liquidity to stabilize the exchange rate since late August. This does not bode well for the real economy. The uptick in onshore bond yields and the RMB’s appreciation will be transient. Equity investors should stay cautious.

Today, we are sending you the BCA annual outlook for 2024. The report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who are long-time BCA clients with whom we discuss the economic and financial market outlook for the next twelve months toward the end of each year.

Global smartphone demand will likely find a bottom in 2024Q1 and rebound modestly between 2024Q2 and Q4. Competition in the global smartphone market will intensify. Chinese phone makers will gain market share from Apple and Samsung. Continue overweighting Taiwanese stocks, including tech, within the global equity benchmark.

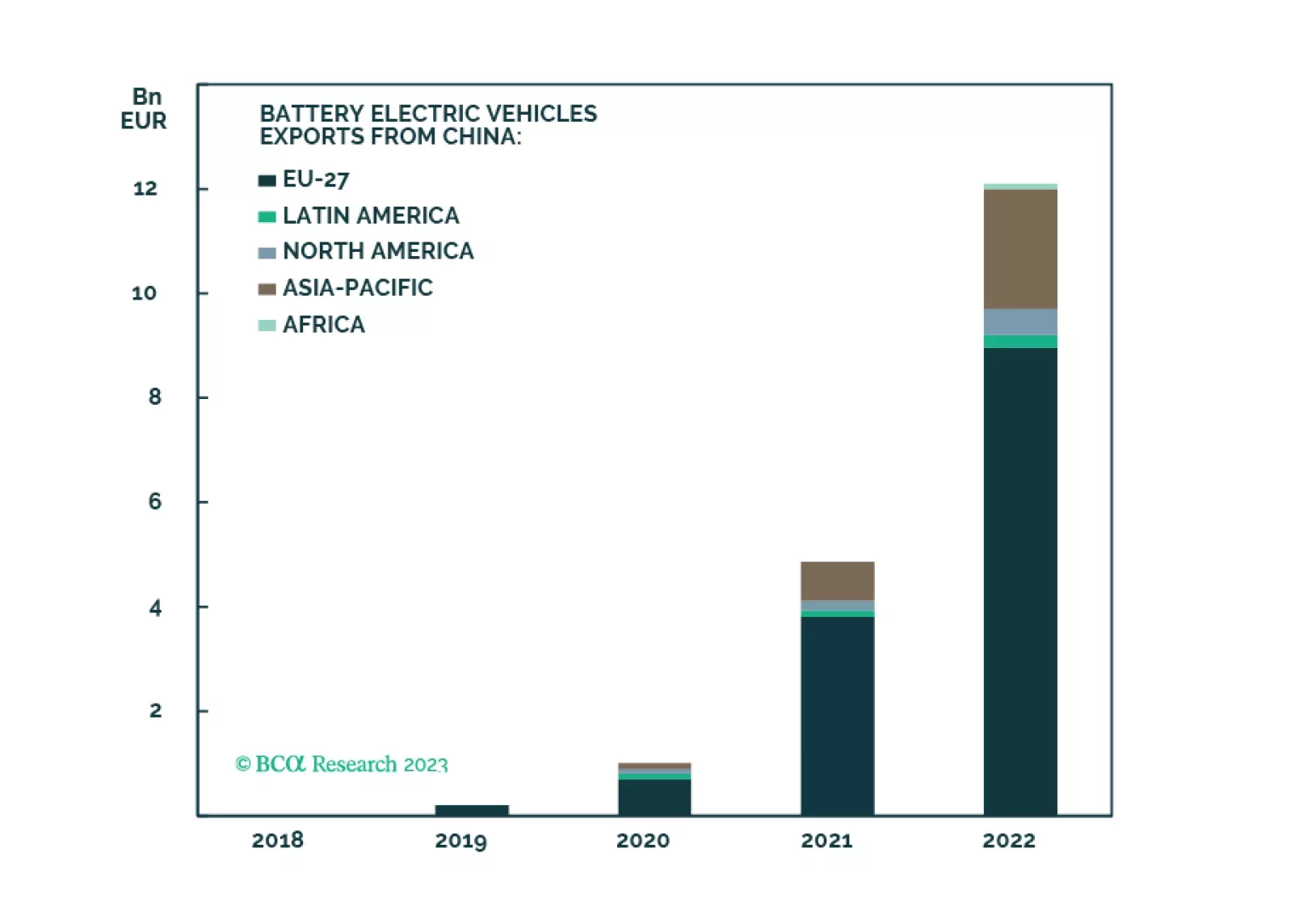

China’s push to dramatically expand its copper-refining capacity will be complemented by further vertical integration of mining assets. However, surplus refining capacity will push treatment and refining charges lower in the short run. The threat of EU tariffs on Chinese EV imports looms large, and could be costly to China’s expansion of its already-dominant supply-chain ecosystem for EVs and metals refining. We remain long the XME and COMT ETFs to retain exposure to metals miners and refiners.