Liquidity

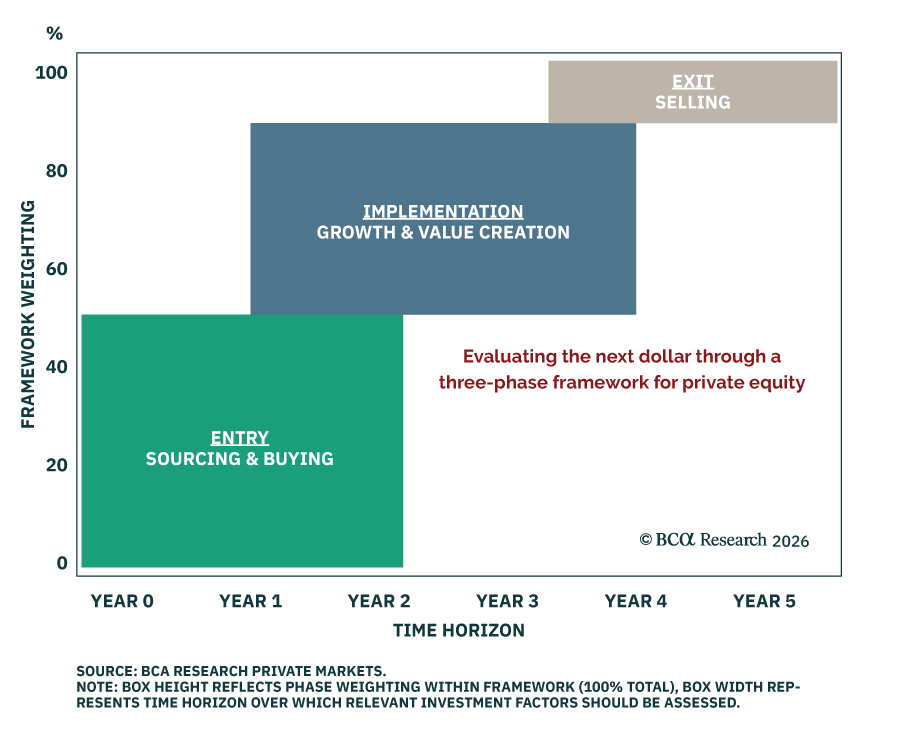

Private Equity fund vehicles may extend beyond 10 years, but the underlying assets that drive performance typically do not. We provide the framework for investors to capitalize on this reality.

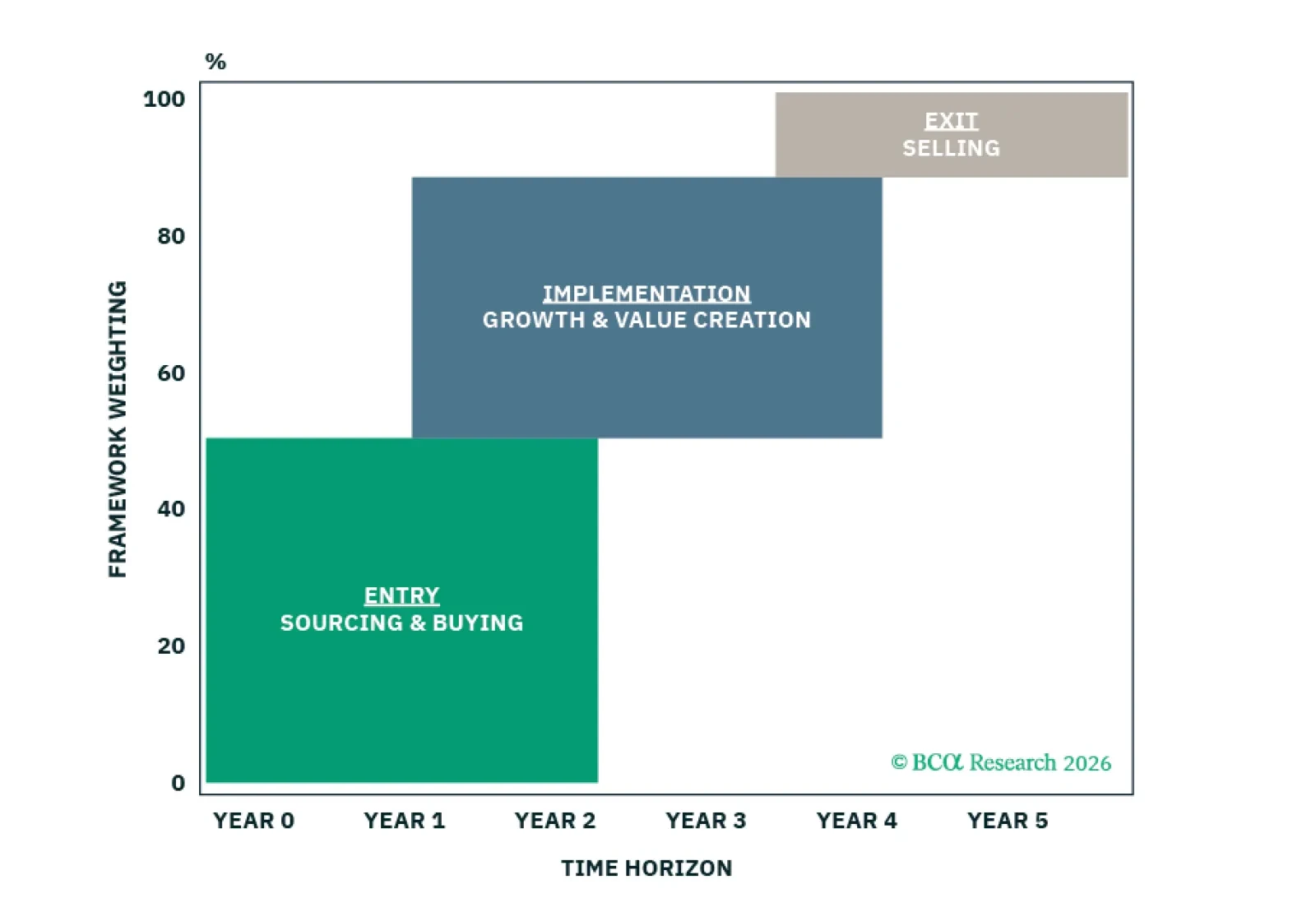

Stablecoins are evolving from a niche crypto instrument into a macro-relevant financial layer. This Special Report maps the transmission channels and consequences for the Treasury market, bank funding dynamics, and the dollar’s global footprint.

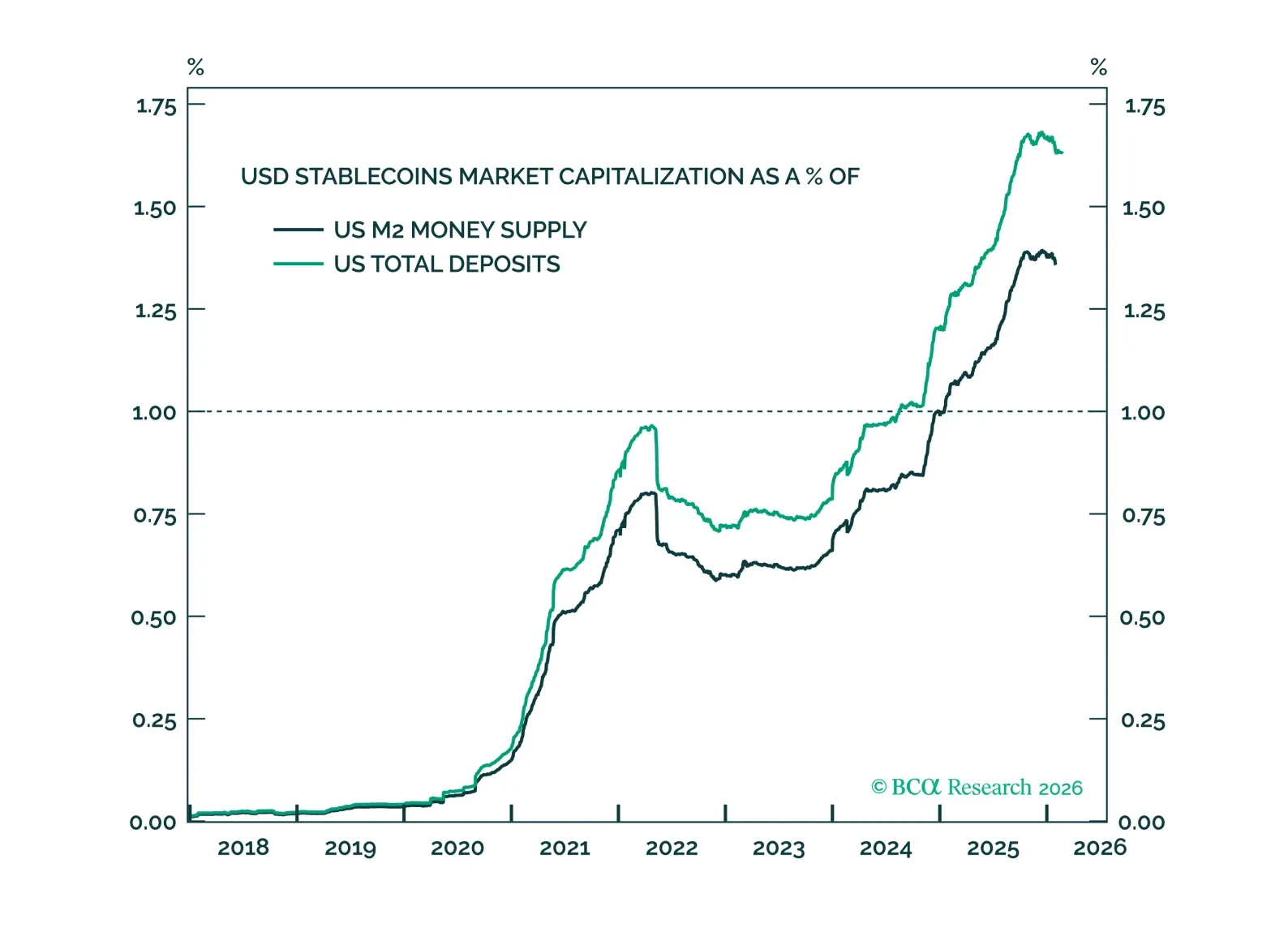

Global liquidity has been the decisive macro variable in 2025, and should stay broadly supportive through most of 2026. We therefore stay neutral equities versus bonds (valuations are stretched), keep a positive bias toward metals (especially gold), and prefer European and Japanese equities over US ones. The key risk is a late-2026 volatility regime shift as overheating fears force a repricing in rates.

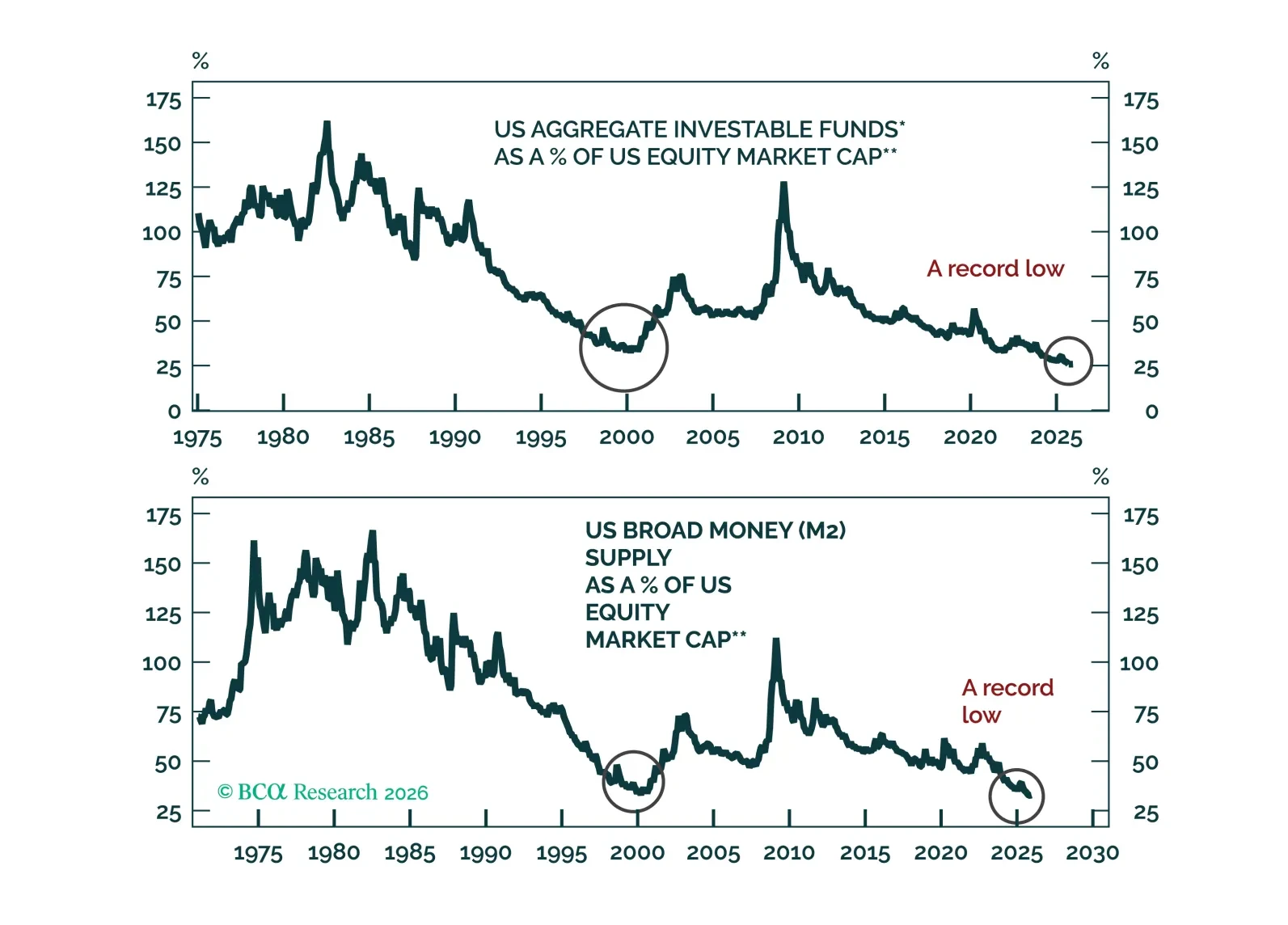

Contrary to widespread narratives, there is little cash on the sidelines. The aggregate amount of investable funds-to-equity market cap ratio is at an all-time low in the US and very low in other developed markets.

China is trying to export its way out of its economic slowdown while the US has already formed a hawkish consensus on foreign policy and trade. Investors should take cover as global financial markets are underrating the new phase of the trade war, which will escalate from here.

Commodity volatility will continue its rising trend since 2014. The US is on the brink of a major election, the outcome of which could reduce its willingness to engage with the outside world. So, states seeking to carve out their own spheres of influence are incentivized to raise the economic costs to the US and discourage its influence in their regions. These states can do this by interfering in key trading routes in their regions. As a result, geopolitical threats to maritime chokepoints are a structural as well as cyclical problem and will persist due to the revival of superpower competition.

The statement from last week’s Central Economic Work Conference indicates that Chinese authorities are still not considering large-scale stimulus in 2024. Odds are that a full-fledged business cycle recovery in 2024 is unlikely. Chinese share prices remain vulnerable, and strengthening in the RMB will be short-lived.

Today, we are sending you the BCA annual outlook for 2024. The report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who are long-time BCA clients with whom we discuss the economic and financial market outlook for the next twelve months toward the end of each year.

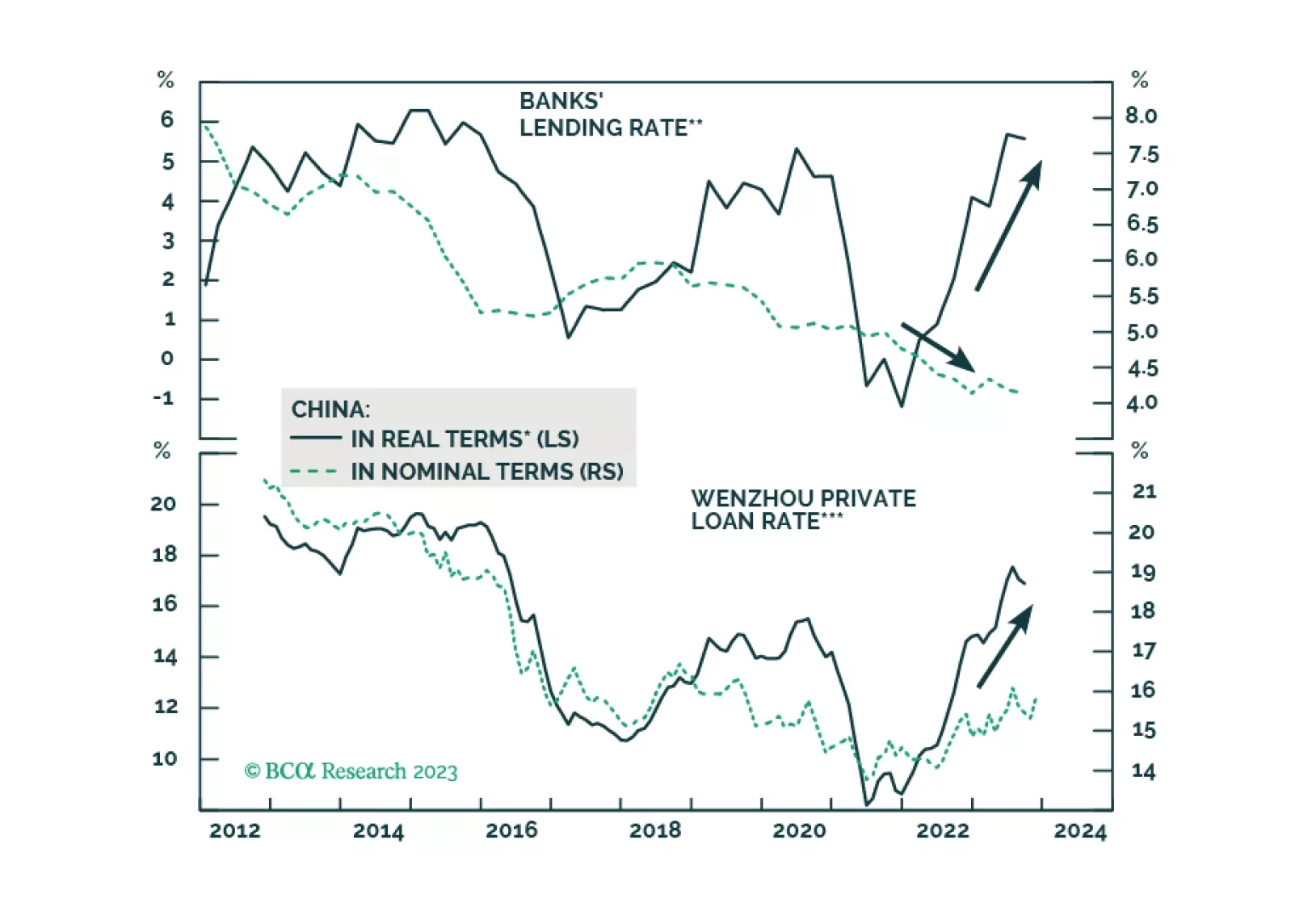

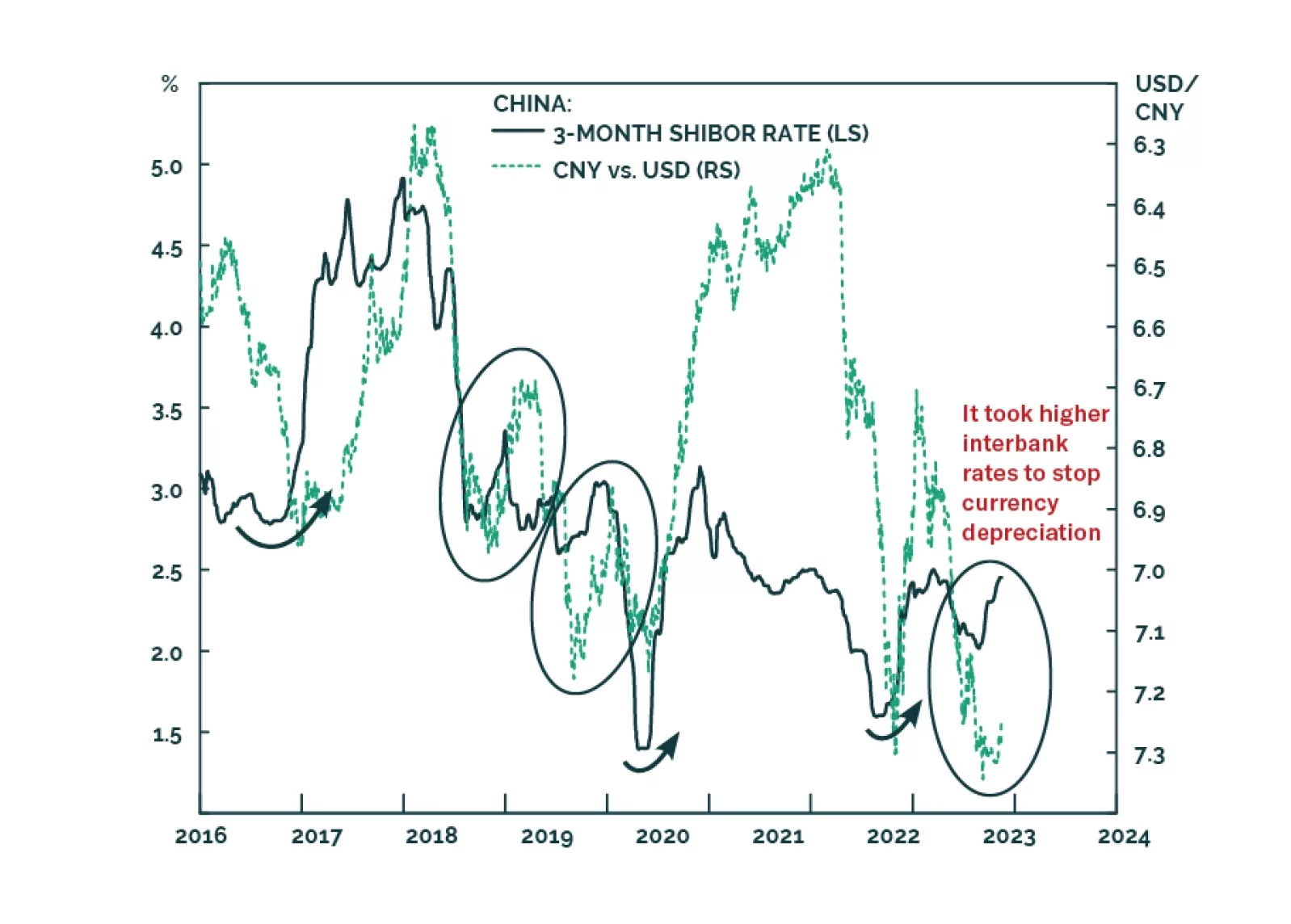

Many commentators have attributed the latest increase in Chinese interest rates to an improving economy, the large issuance of government bonds, the tax payments season, and other technical factors. Yet, these explanations are missing the key point: the PBoC has steered interbank rates higher to defend the currency. Higher borrowing costs are the last thing the mainland economy now needs.