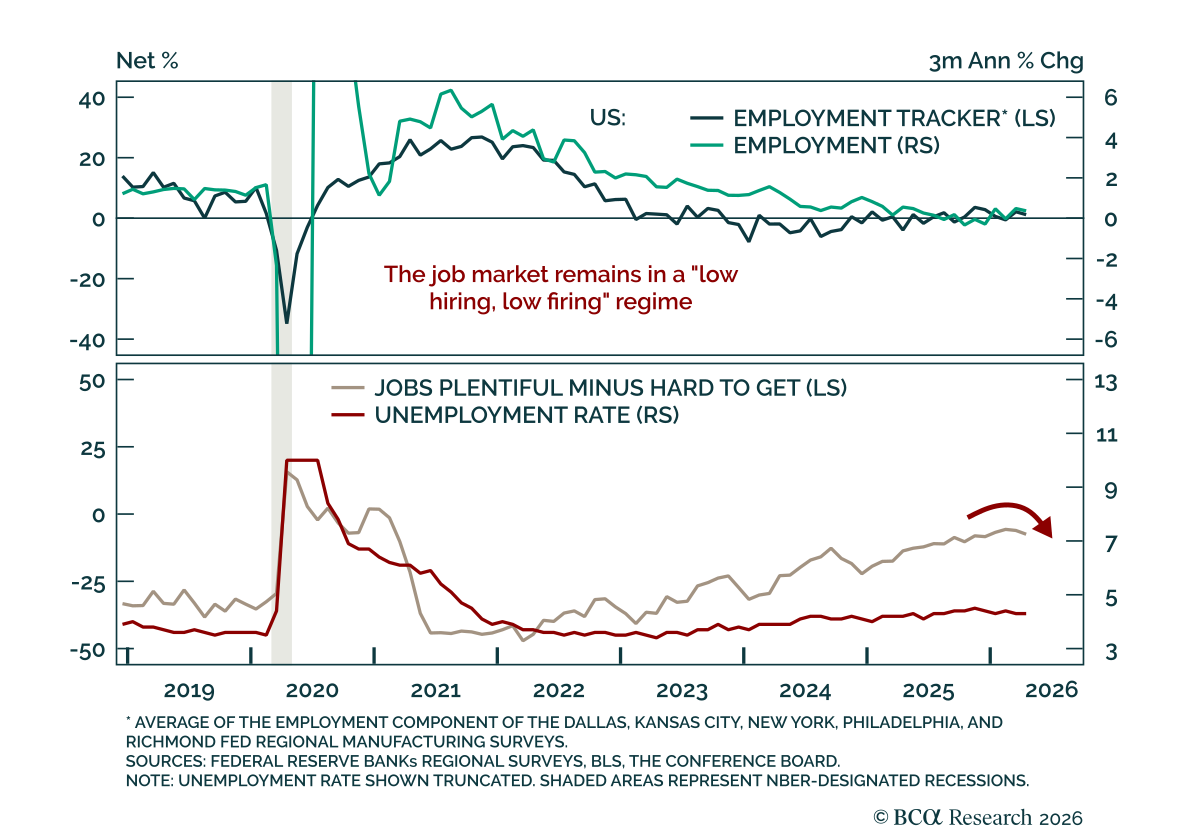

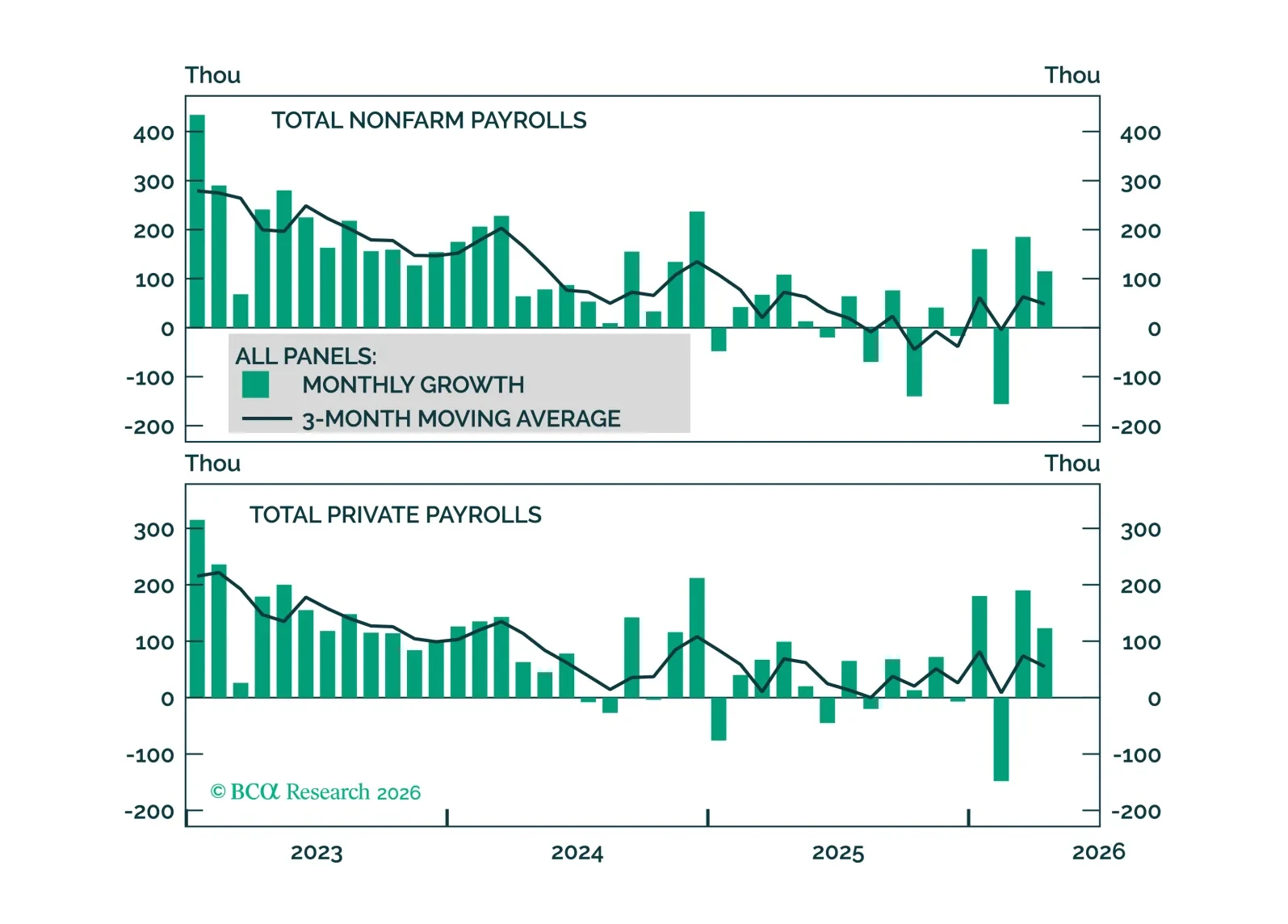

Labor Market

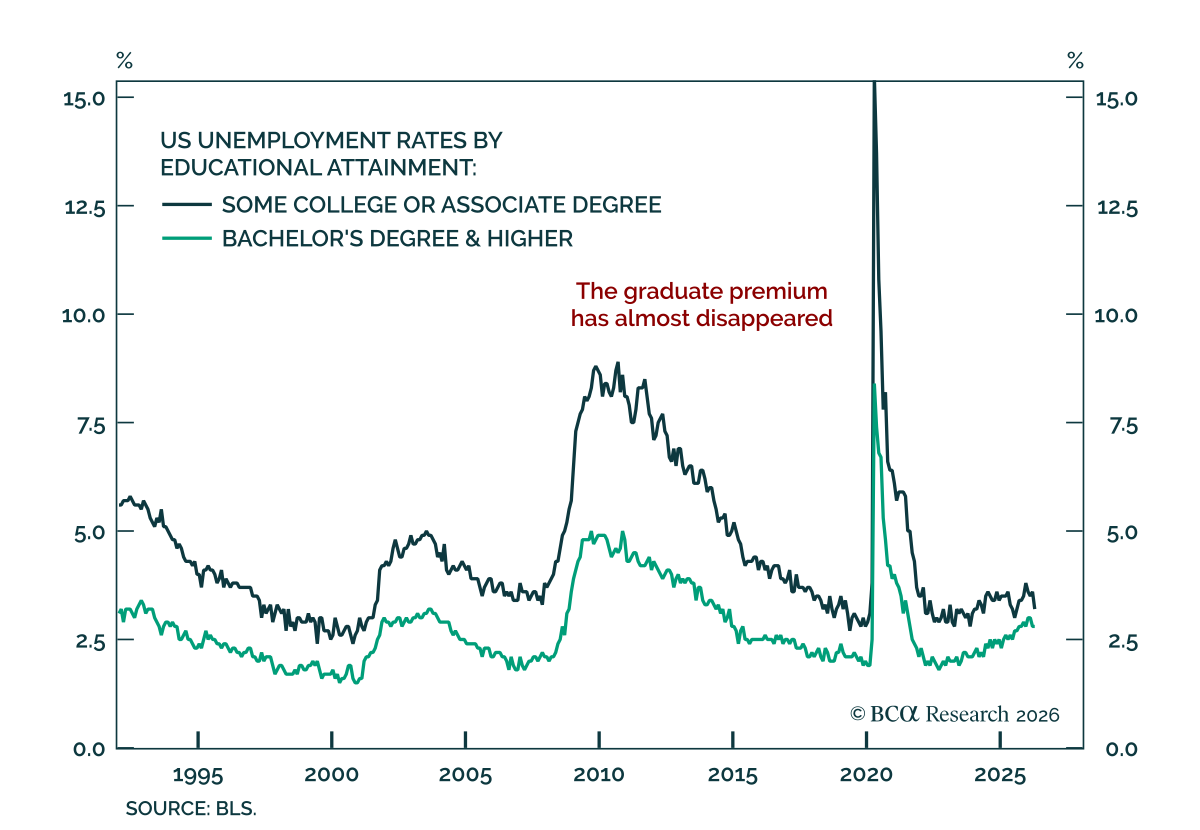

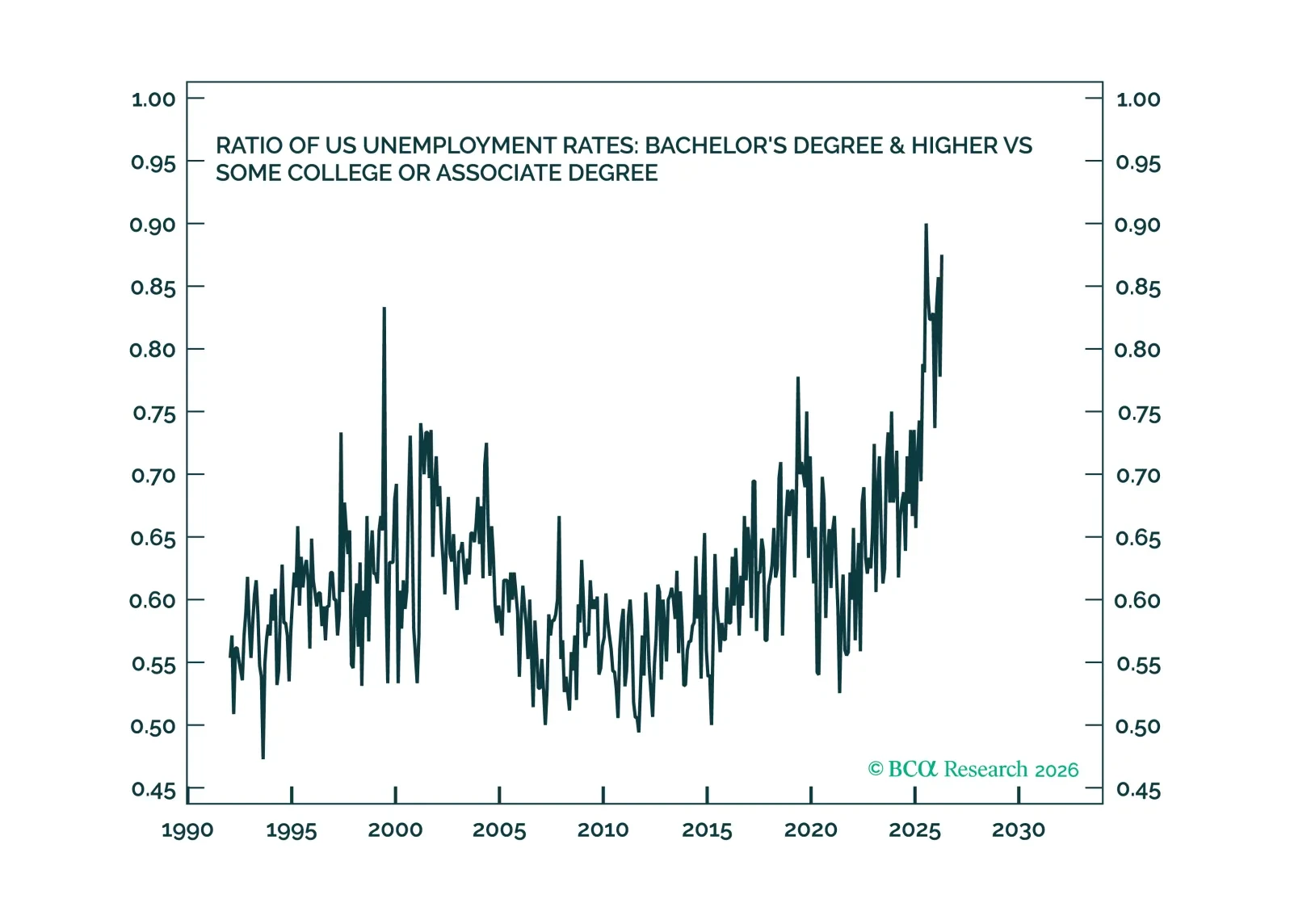

AI excels at IQ but fails miserably at EQ. Hence, AI will obsolete any job that relies on IQ, including many graduate-level jobs. But high-EQ humans will be in high demand to pair up with AI, and many of these jobs will be middle income jobs. We discuss the implication for the economy and markets. Plus, a new tactical trade is underweight global tech versus healthcare.

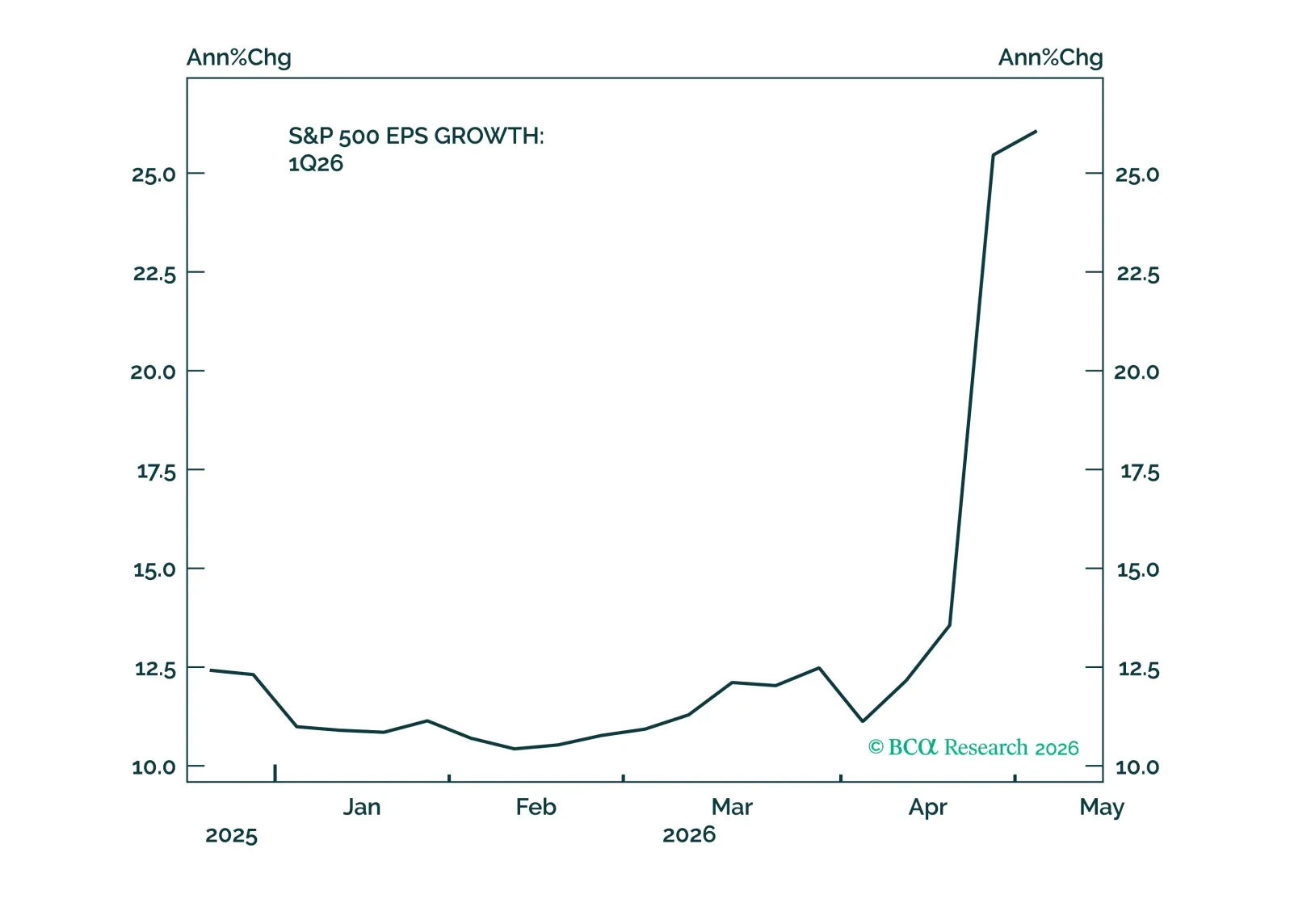

We take stock of earnings, AI capex and the labor market and explain why we think the repeated new highs in the S&P 500 are justified.

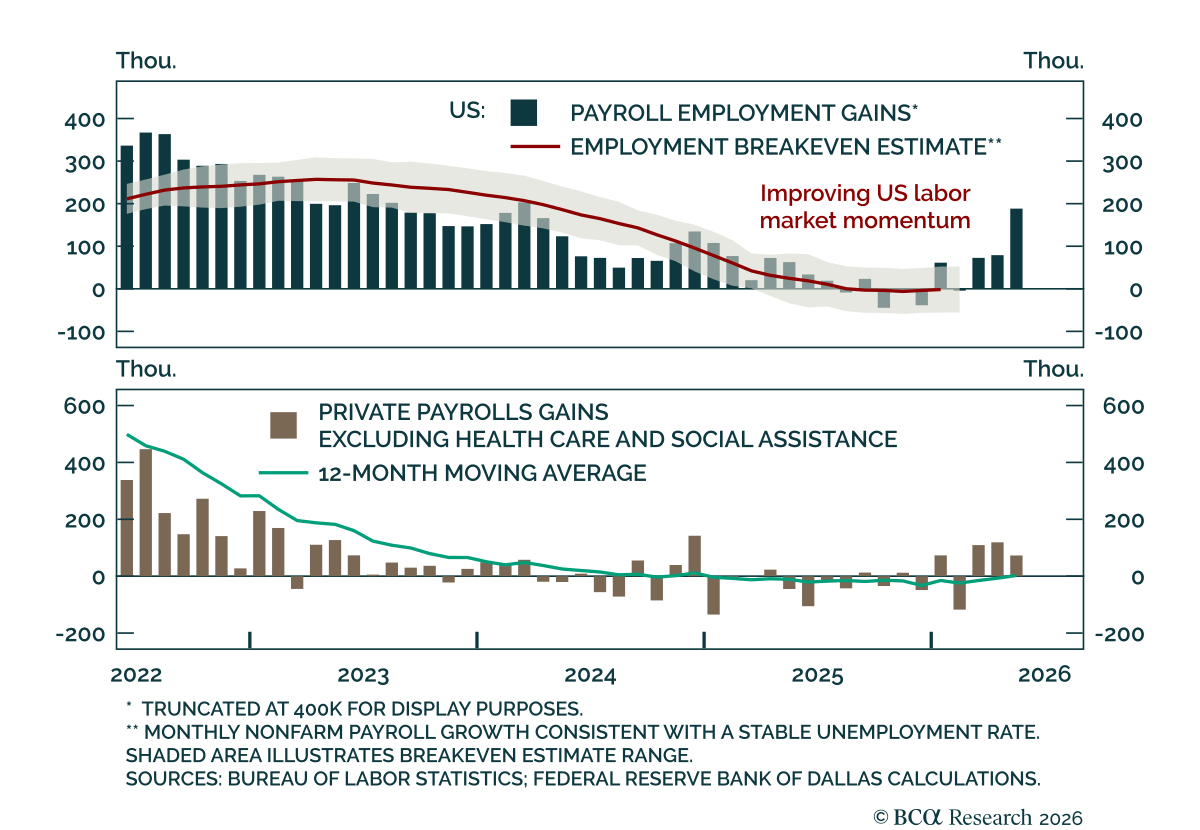

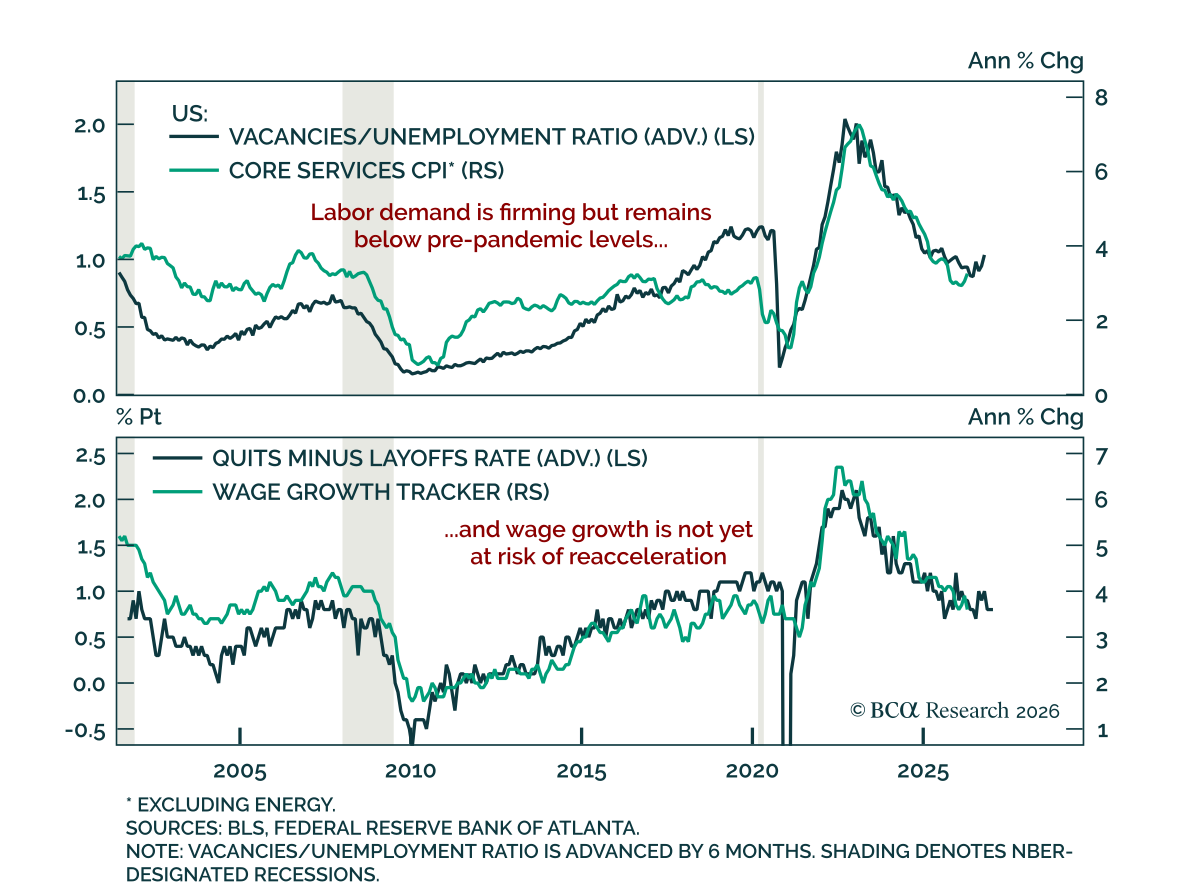

Improving job growth keeps Fed rate cuts off the table, but evidence of labor market tightening will be required before rate hikes become part of the discussion.

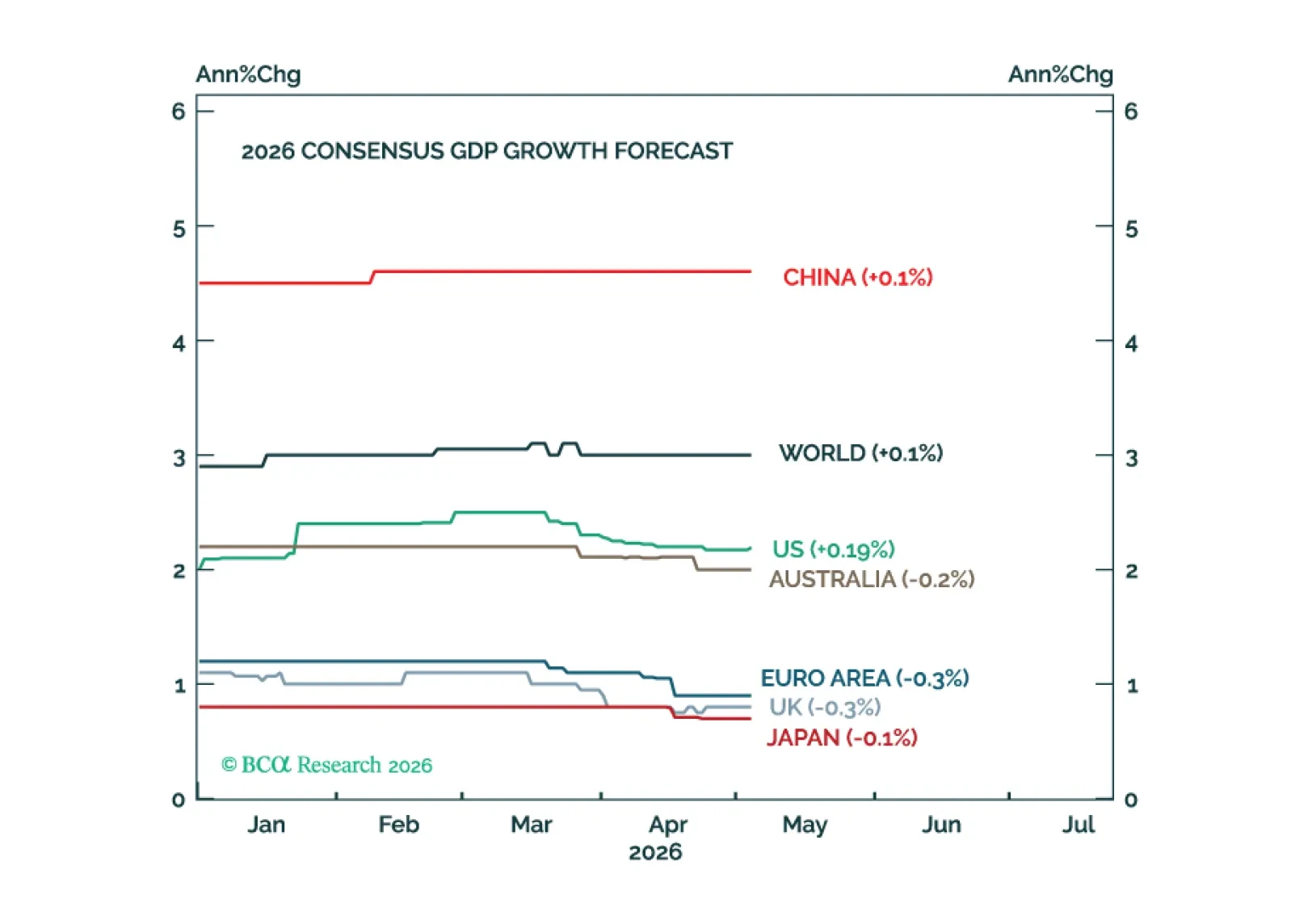

The global economy has weathered the oil shock reasonably well so far. However, the risk of a recession will increase meaningfully if the Strait of Hormuz remains closed into June.