Iran

Our March 13 tactical insight into the ongoing Third Gulf War has incited a lot of client feedback.

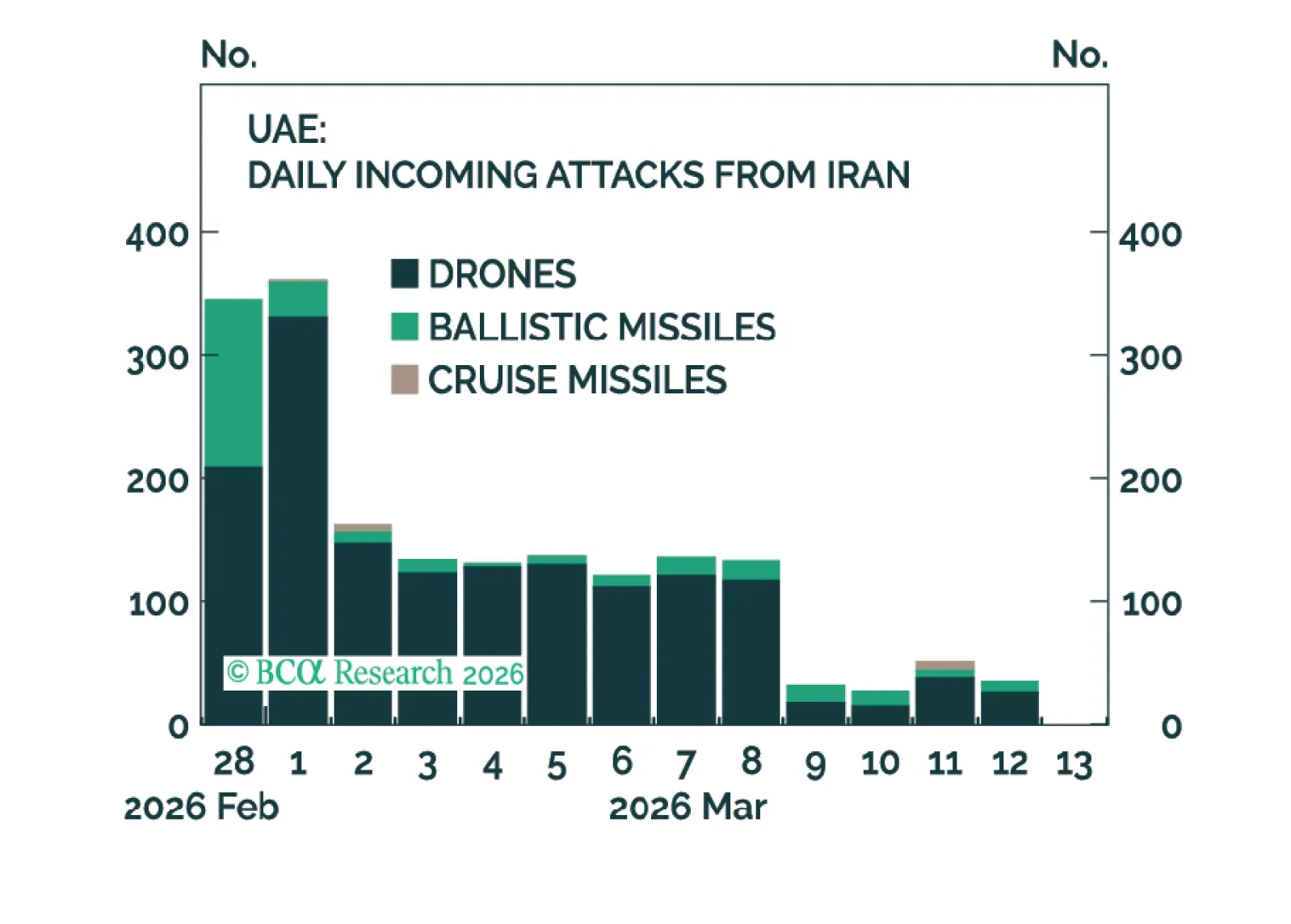

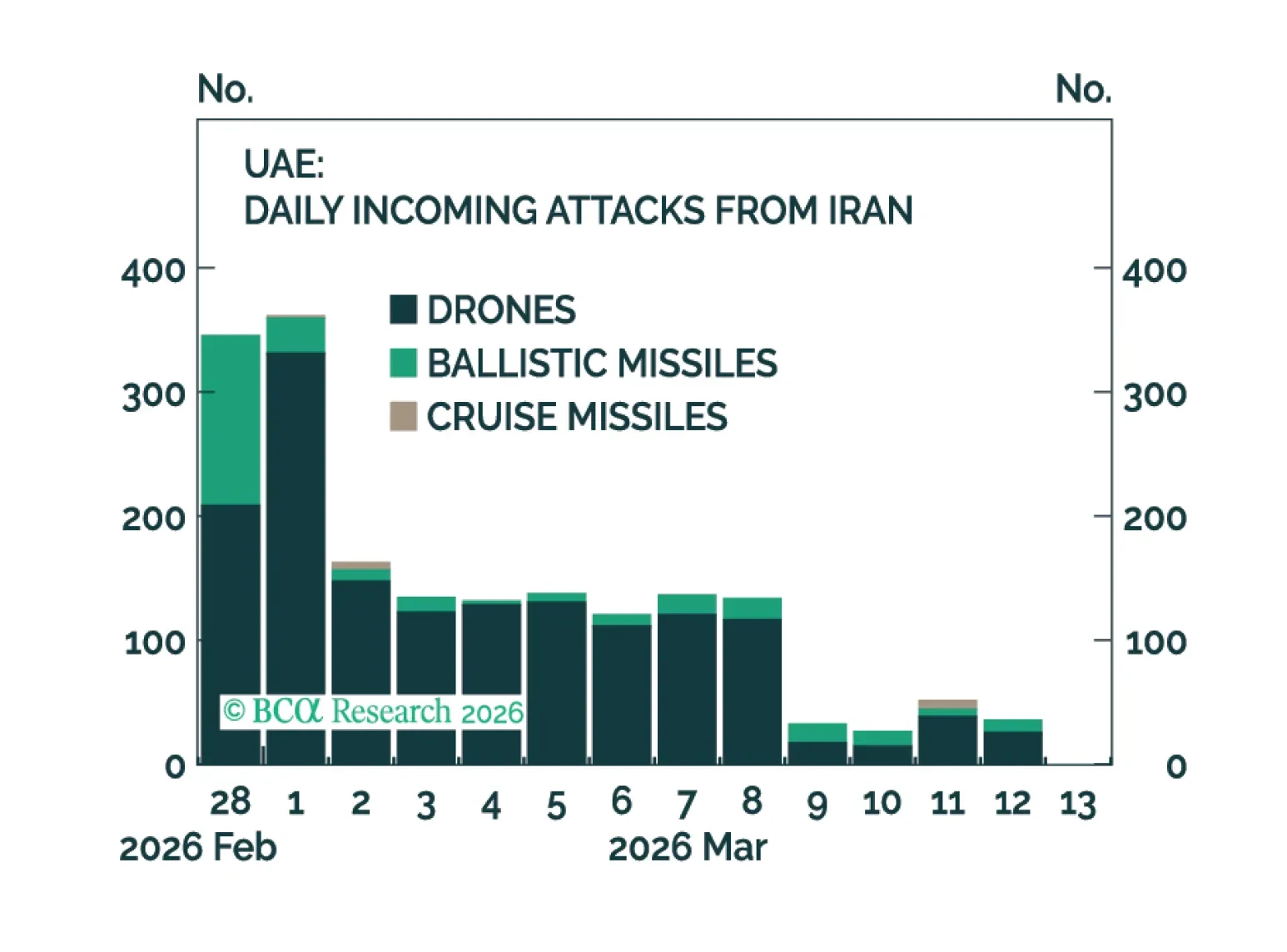

The conflict in the Middle East persists as the US and Israel continue their strikes, and so does Iran’s retaliation with drones and ballistic missiles against the Gulf States. The Strait of Hormuz is still essentially closed, despite some ships being allowed to traverse.

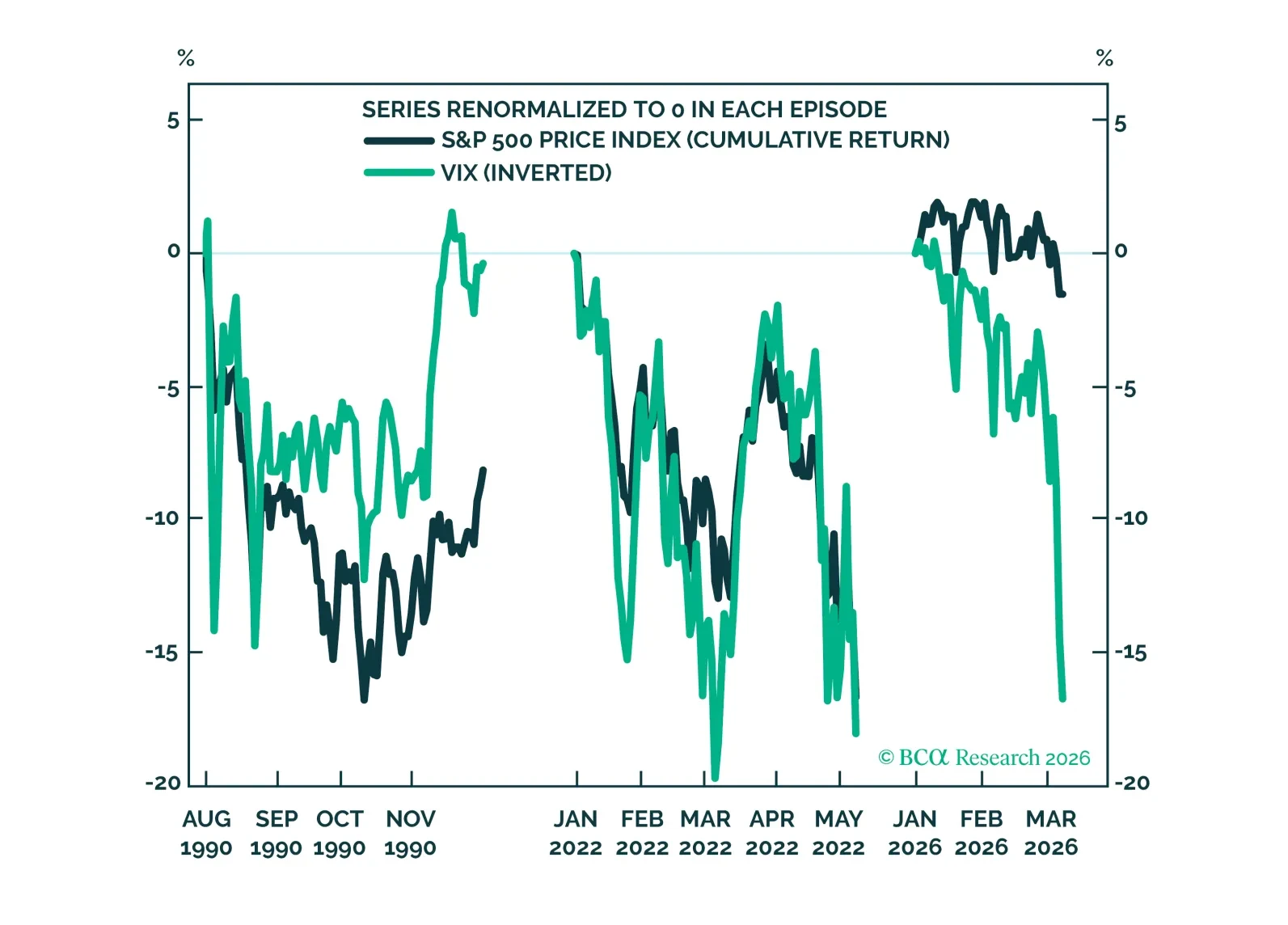

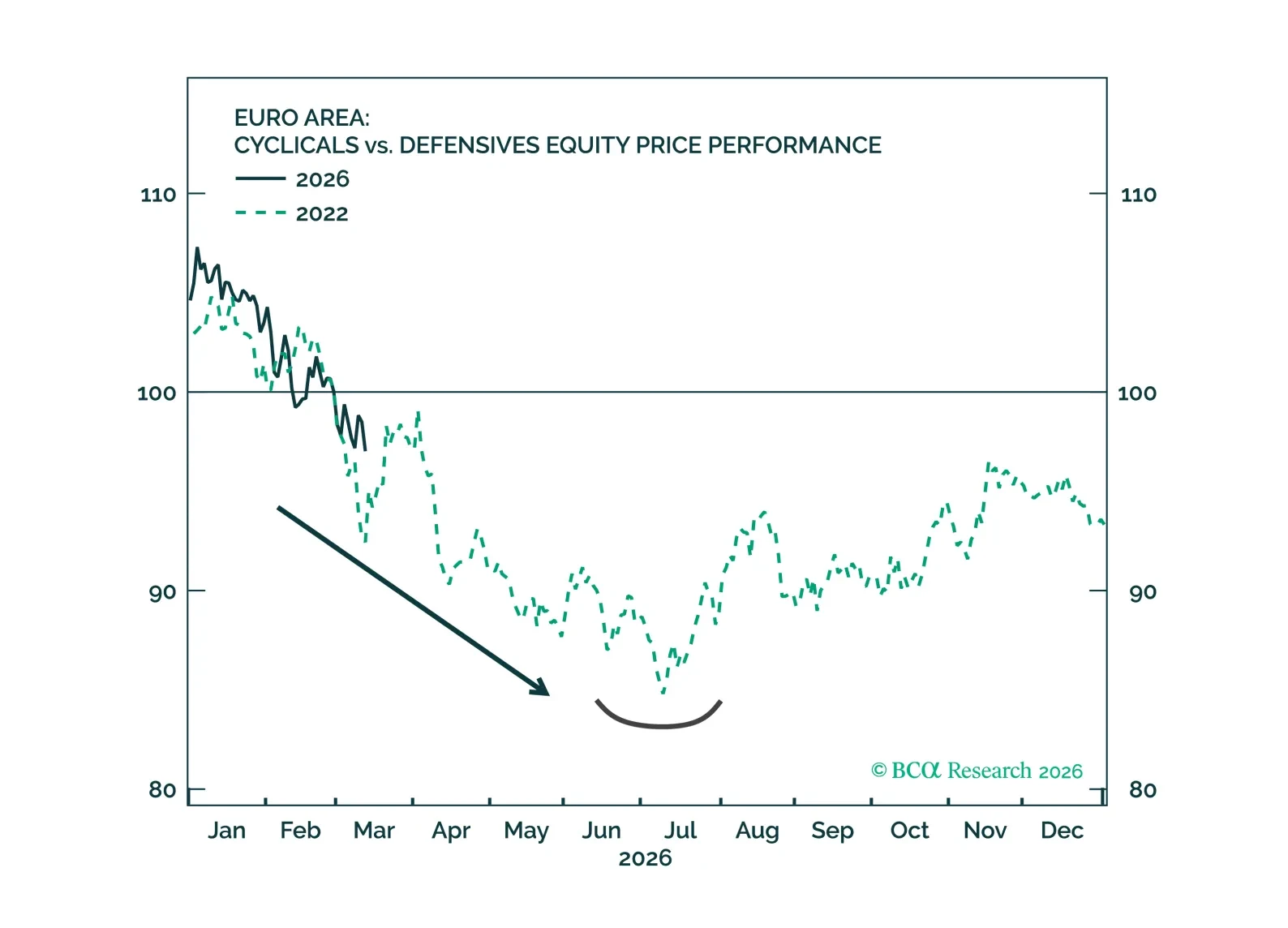

Middle East tensions sparked a surge in volatility, yet the S&P 500 decline has been comparatively modest. Across asset classes, moves seem related to risk preferences and near-term inflation concerns. Within equities, some cyclicals are under pressure, but the equity market’s growth view has been resilient, while the inflation view has climbed.

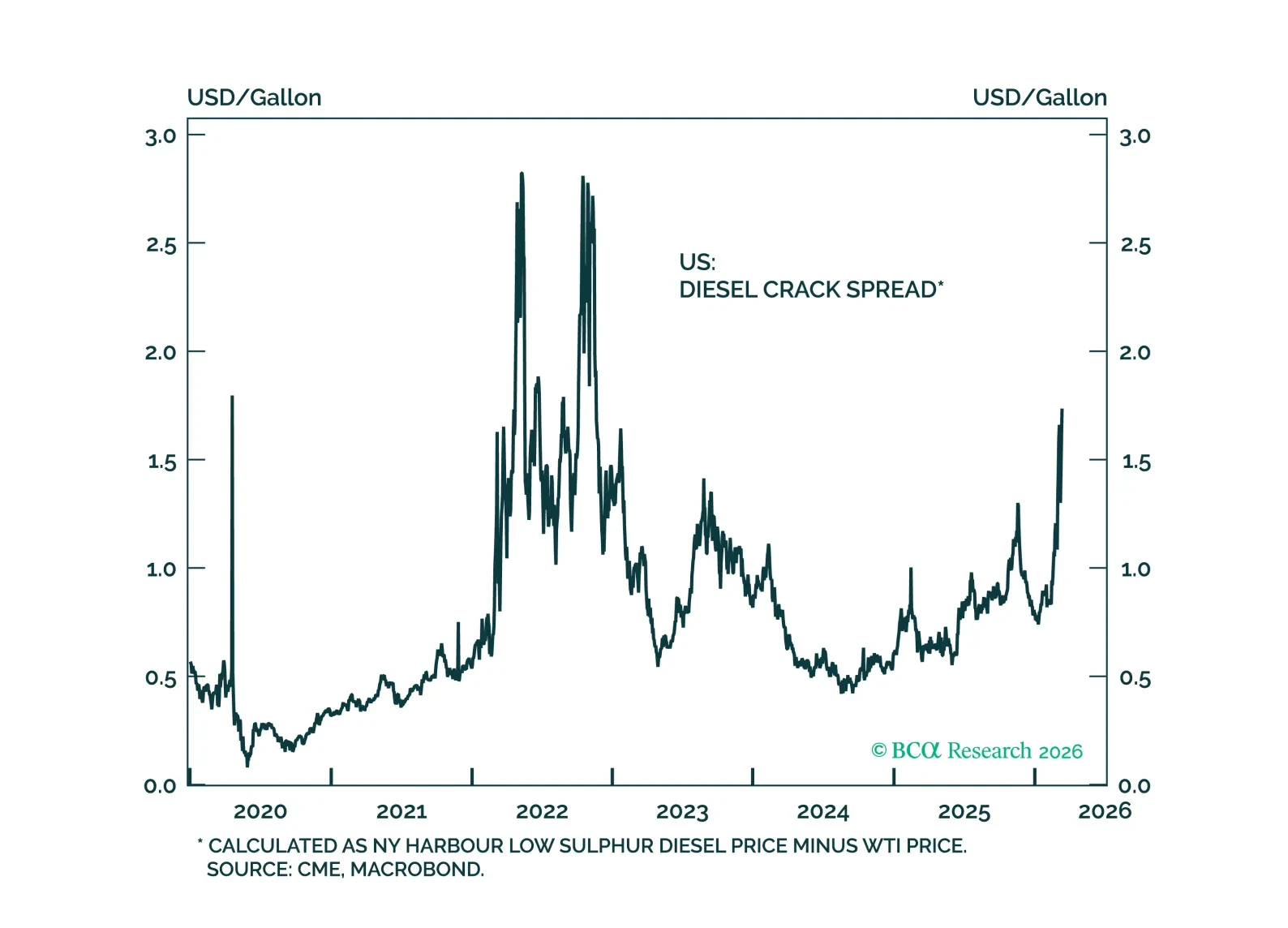

War momentum and escalating rhetoric around the Strait of Hormuz have pushed Brent above $100 and raised the risk of a broader supply shock. While parallels with 2022 offer a roadmap, today’s shock is likely shorter but more globally disruptive. Markets are repricing monetary tightening risks, though we see rate hikes as a mistake absent second-round inflation. Beyond oil, sulfur, helium, and fertilizer disruptions threaten food prices and the AI supply chain. Position defensively.

We outline a framework for the Iran war's impact on the commodity outlook in the event of a prolonged Strait of Hormuz disruption. We break it down into three phases: (1) the Initial Shockwave, (2) the Ripple Effects, and (3) the Backwash. The first phase has largely passed, and we are now in the Ripple Effects phase.

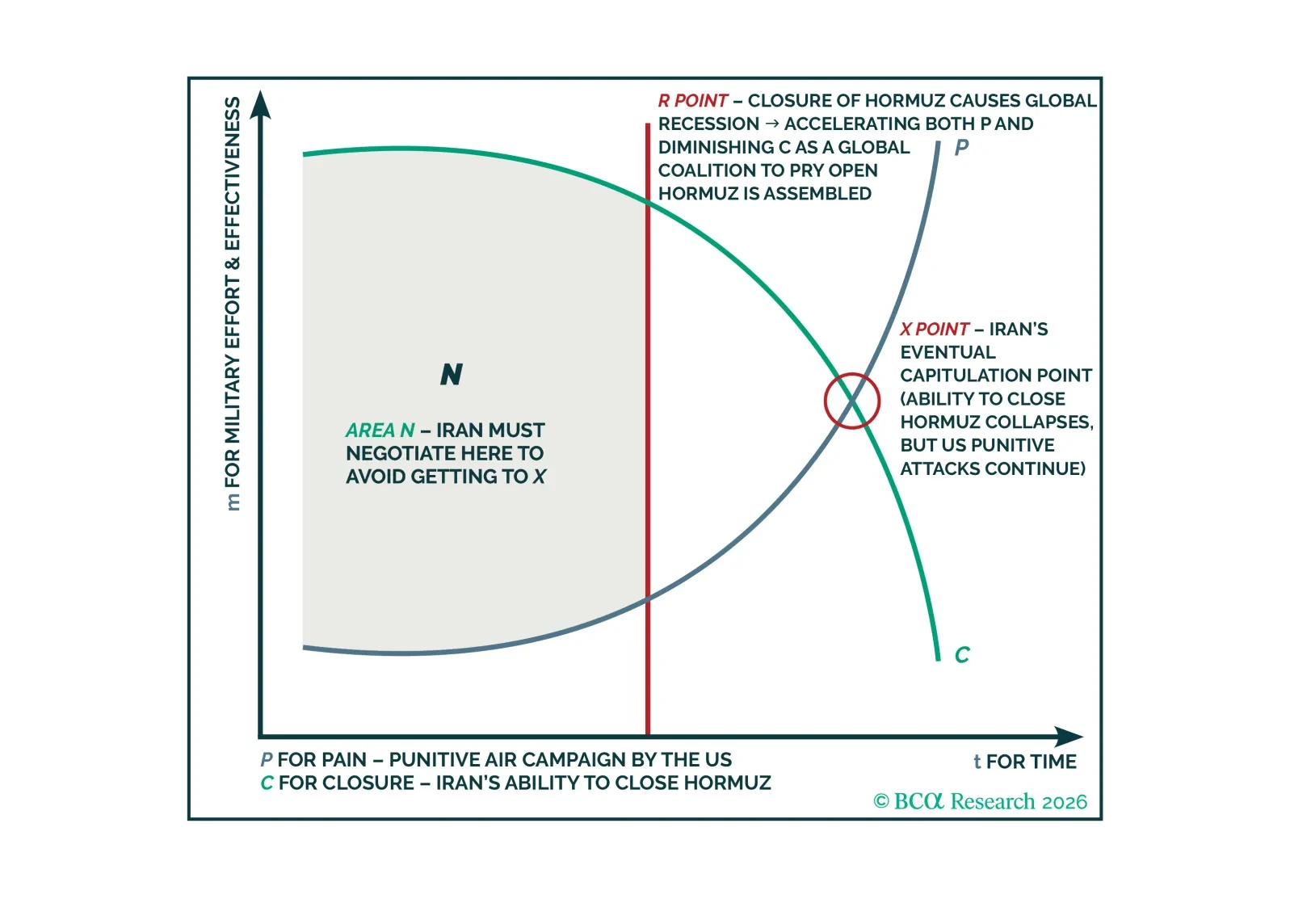

Investors are too complacent on the closure of the Strait of Hormuz. Upgrade cash and downgrade equities, both to neutral.

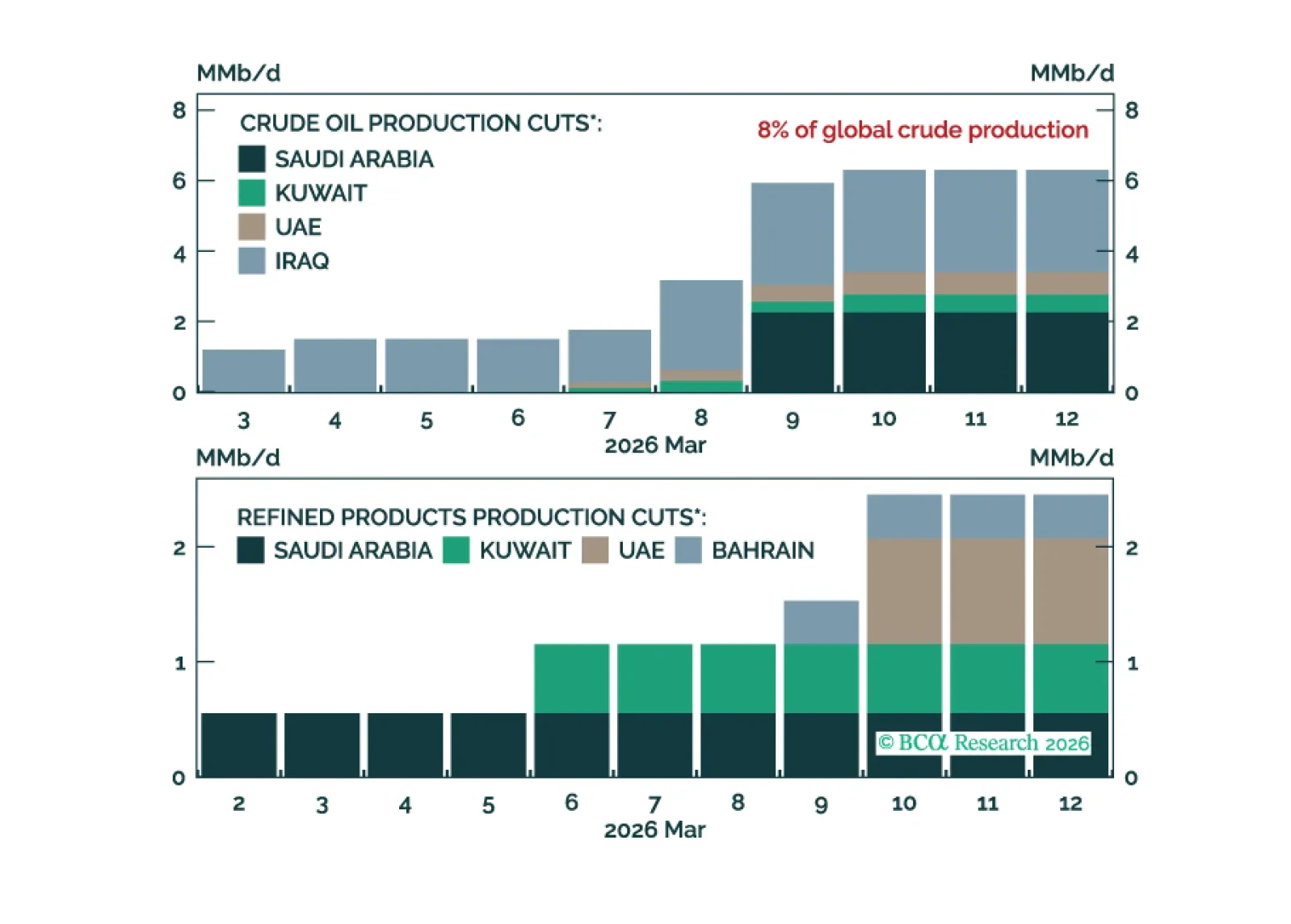

The conflict in the Middle East persists as the US and Israel keep striking at Iranian military and internal security sites, and Iran has responded with its own missiles and drones against the Gulf States. Although the pace of Iranian retaliation has declined, it appears to have stabilized, as evidenced by attacks against the UAE.

The conflict in Iran has entered the “post-Trump taco zone” where it is now all about Tehran’s reaction function.