Iran

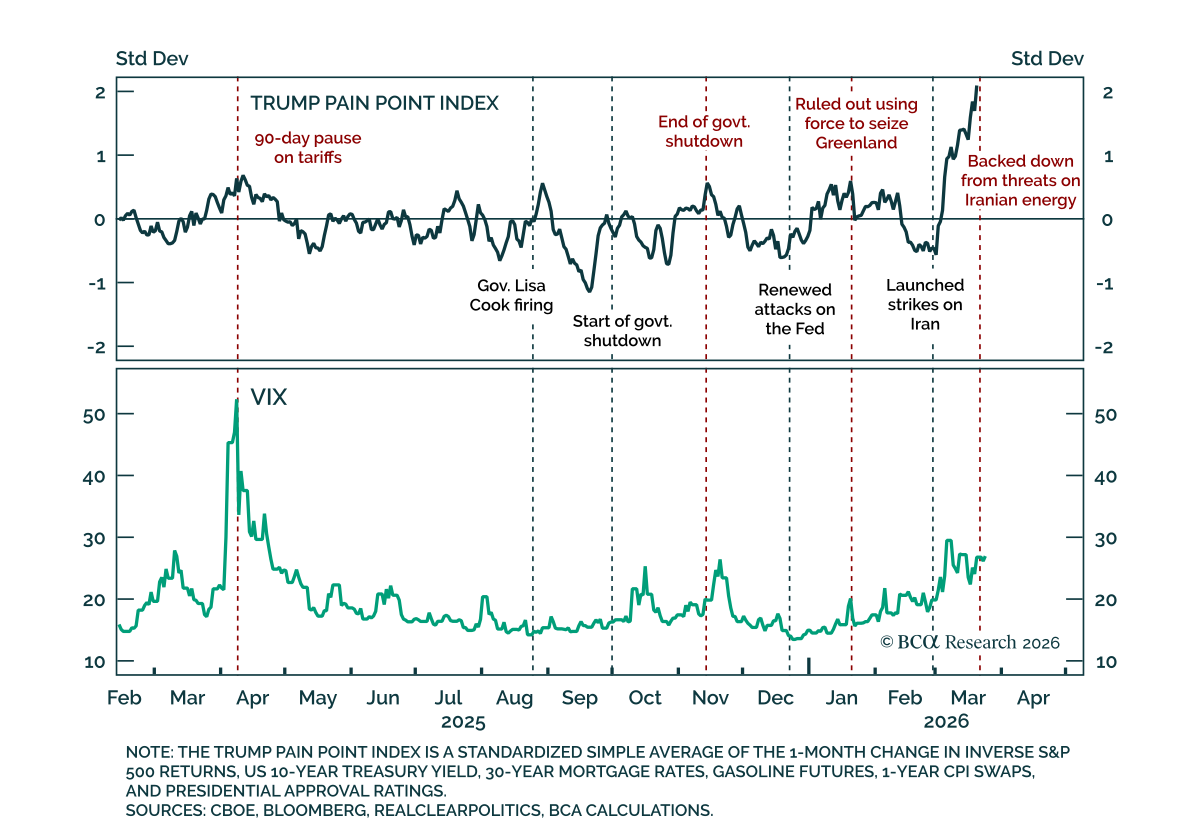

President Trump offered to deescalate the conflict in the Middle East on March 23. In a series of wide-ranging comments, President Trump said that regime change had already been achieved, that negotiations with Tehran were progressing, and that he was pausing his threat to target Iranian energy infrastructure for five days.

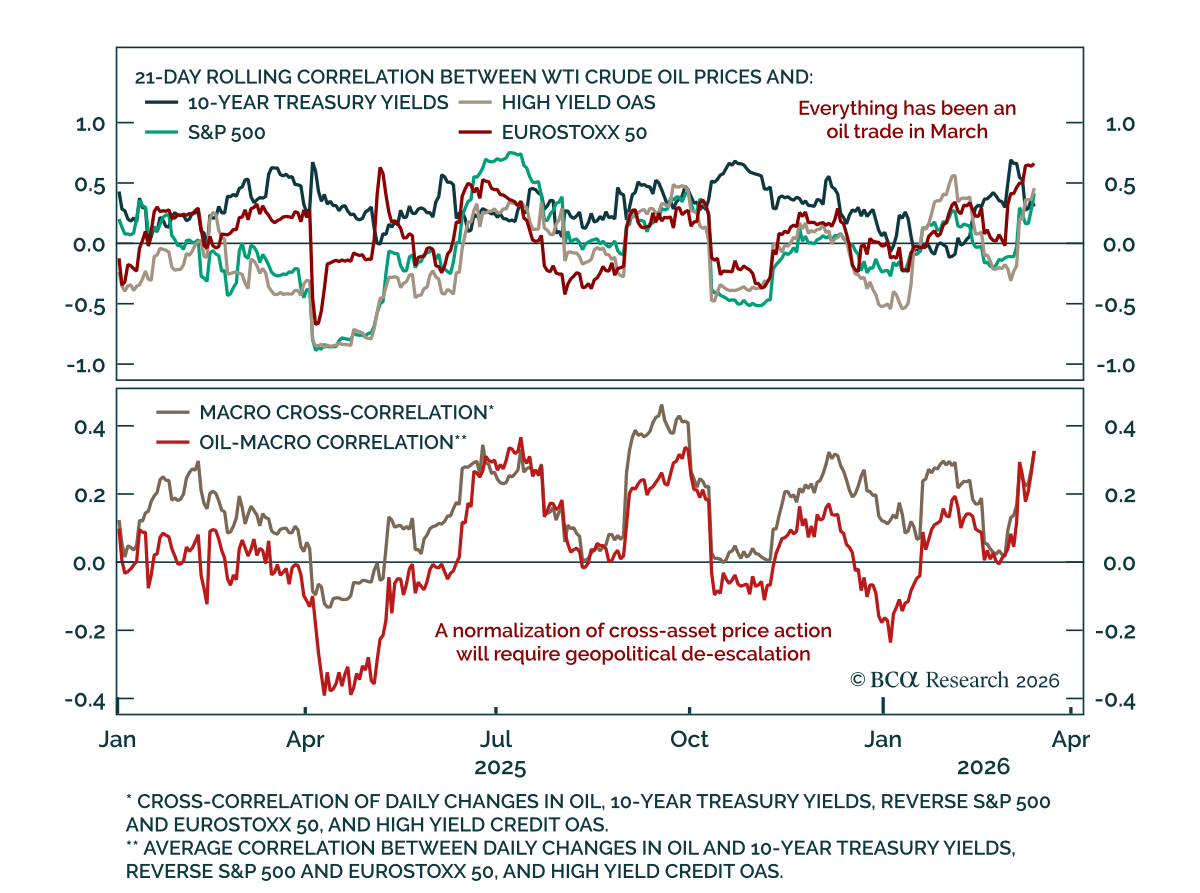

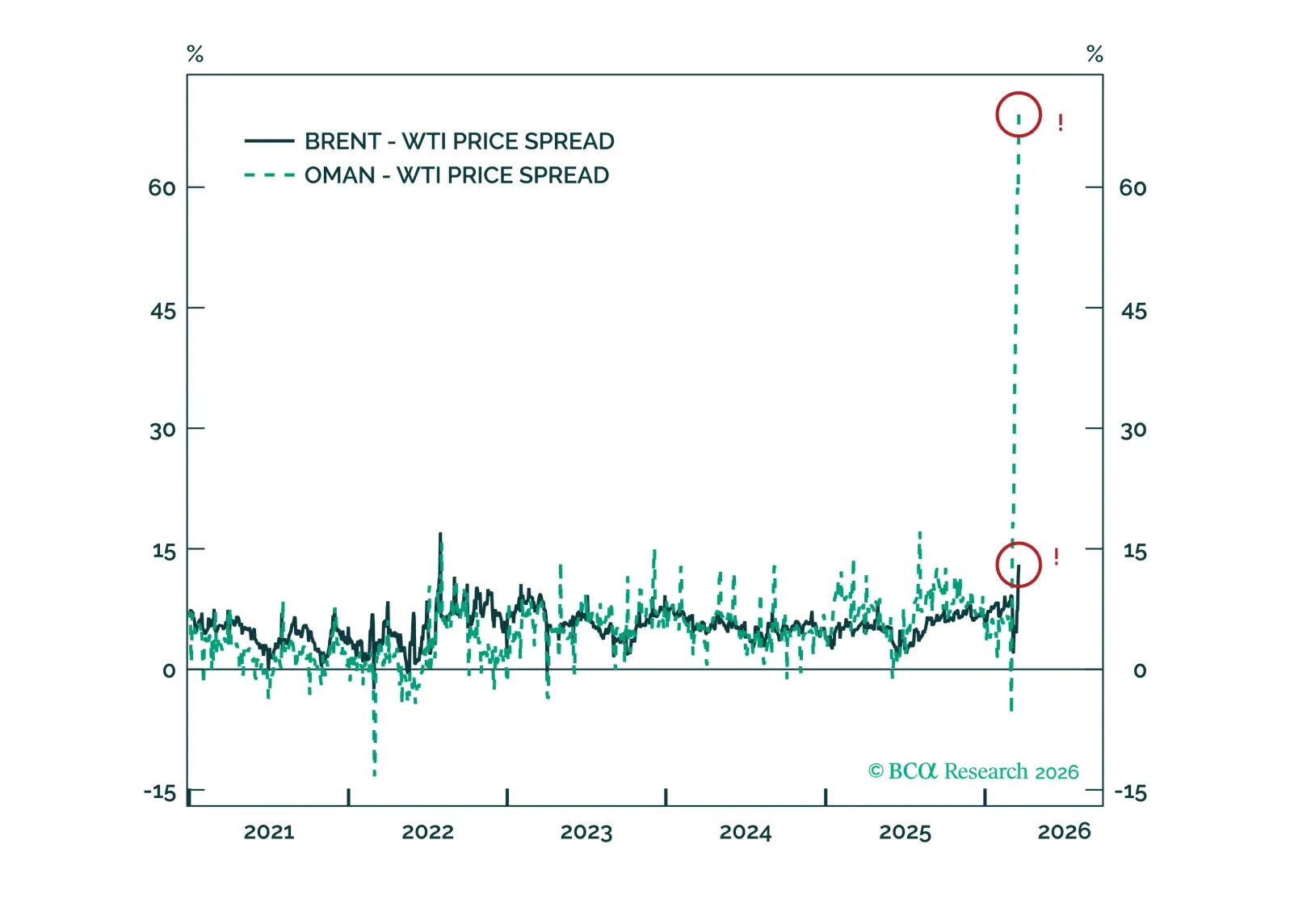

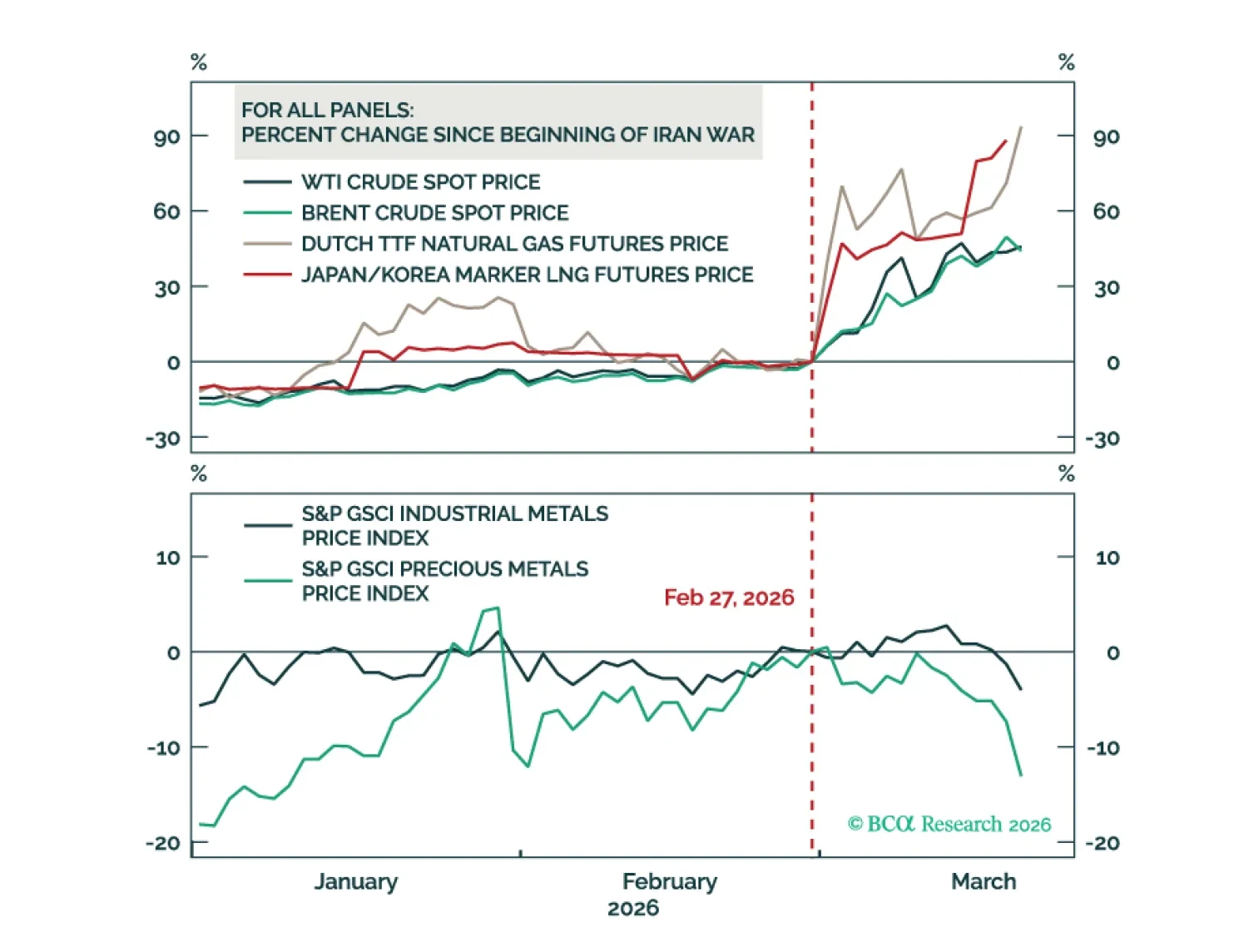

WTI is relatively calm amid the current conflict in the Middle East. Markets are too complacent on US crude relative to other international benchmarks.

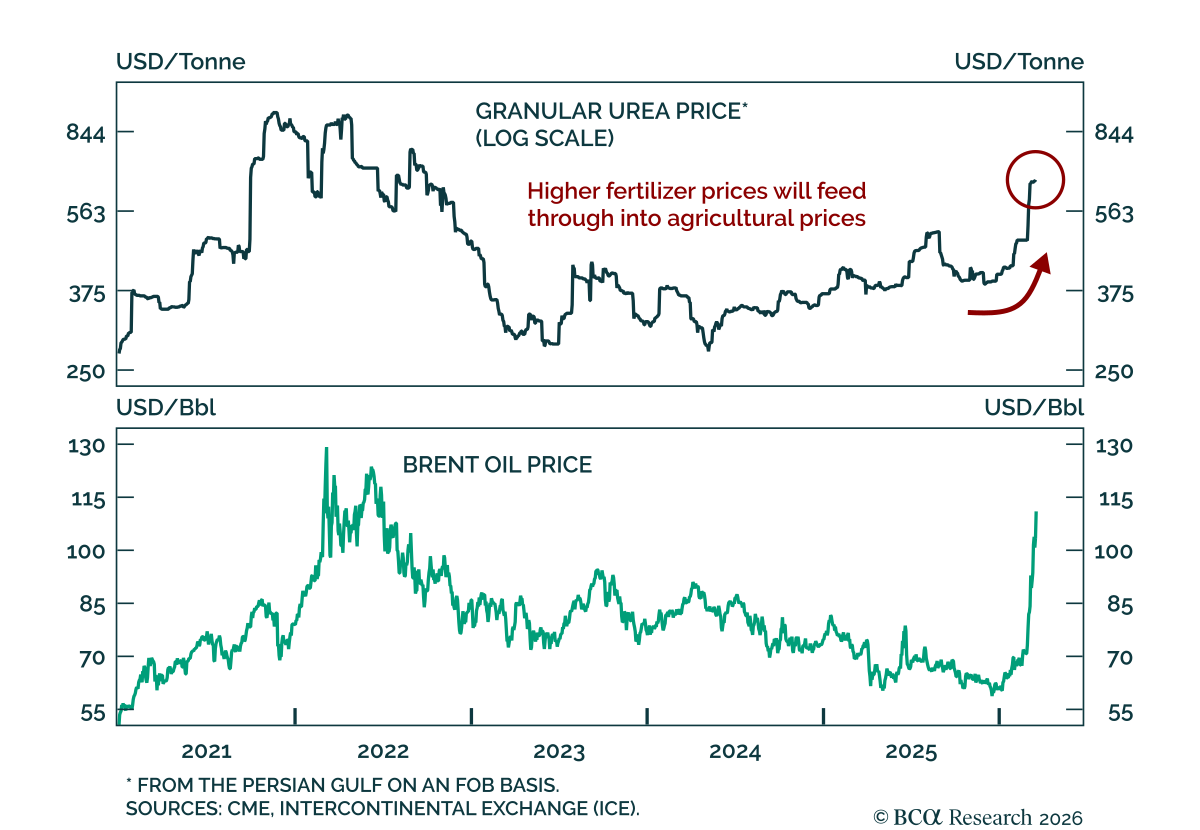

Higher oil prices threaten the global economy, warranting an underweight stance on equities. Over the long haul, industrial metals will fare better than crude.

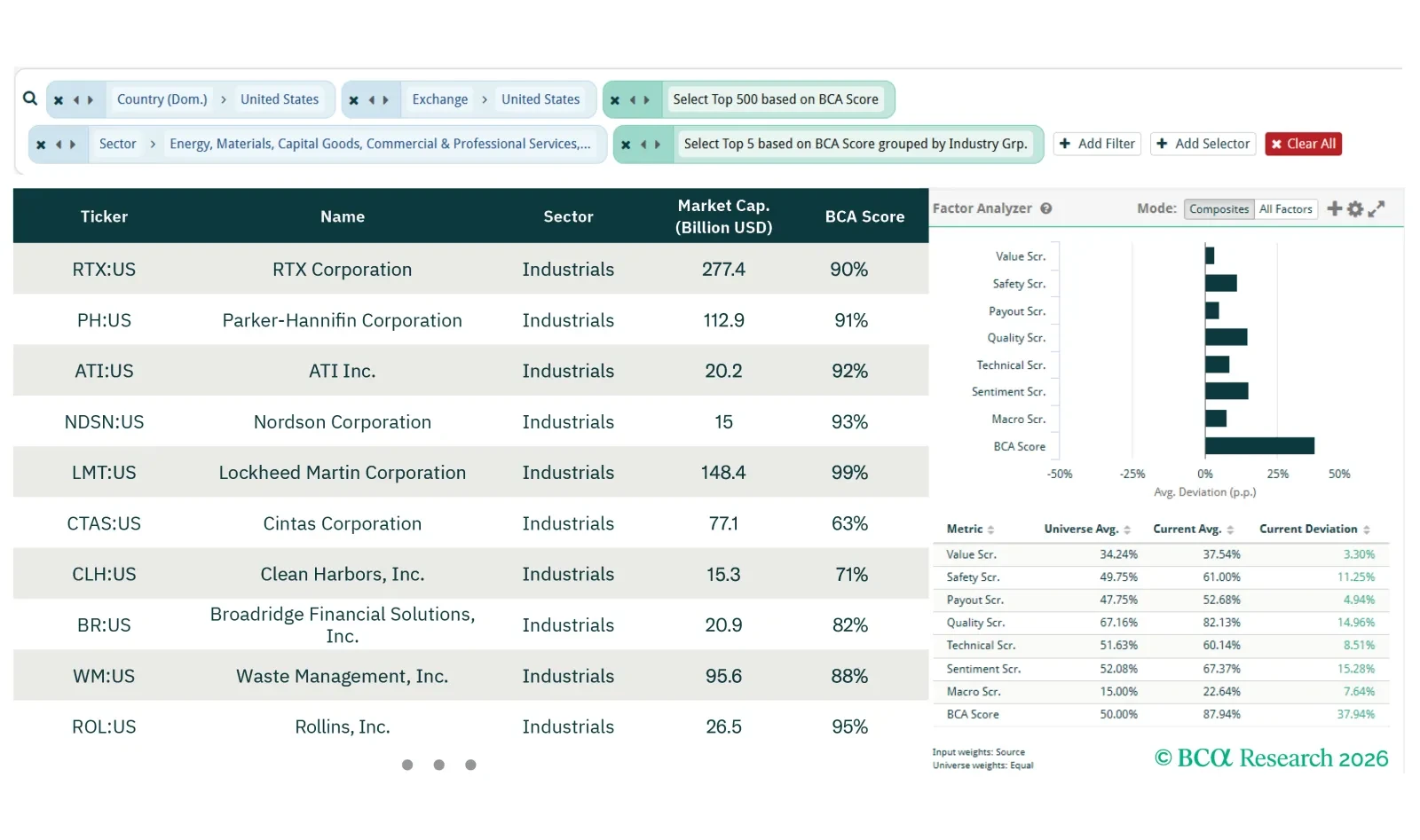

This screener report builds on the macro risk portfolio framework developed in the US Equity Strategy and Equity Analyzer collaboration published on 9 March 2026. Here, we apply the framework to analyze recent Middle East hostilities and identify how bottom-up equity positioning should adapt as the conflict evolves, which we analyzed in a US Equity Strategy report published on 16 March 2026.

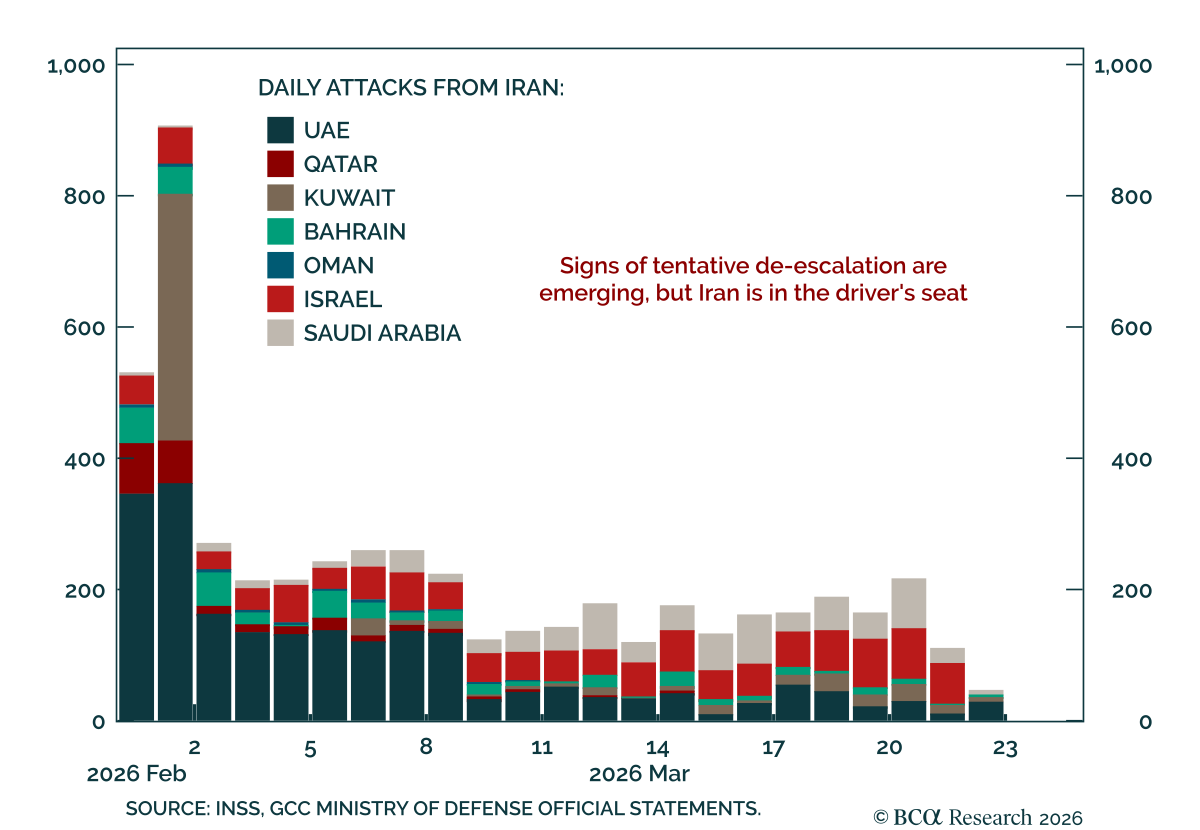

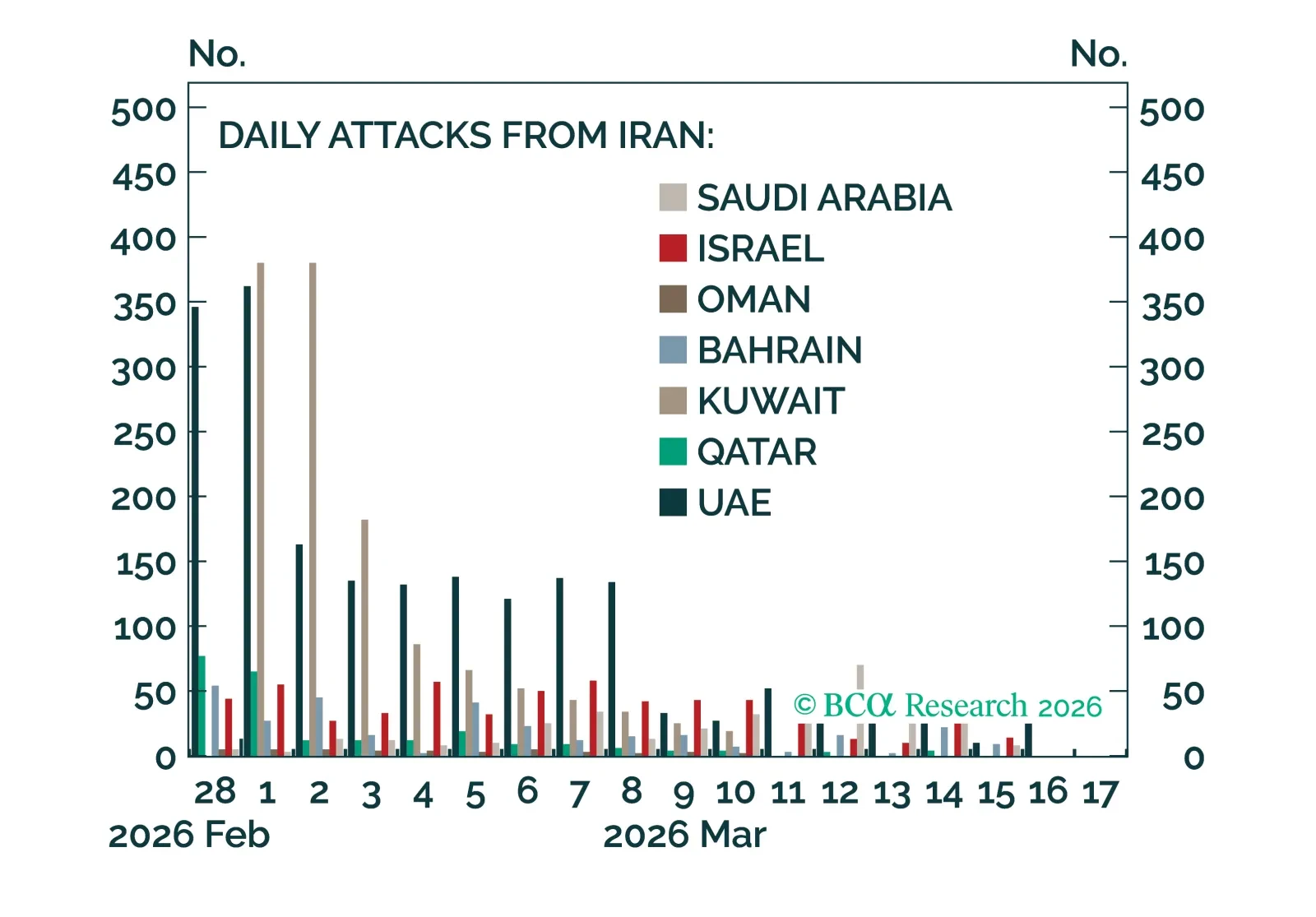

Overnight, the Israeli military reported that it managed to kill two high-profile Iranian leaders: the Secretary of the Supreme National Security Council and the leader of the internal paramilitary group, the Basij. Meanwhile, the Gulf States reported more interceptions of drones and missiles from Iran.

The market narrative around the Gulf conflict rests on three flawed myths: the UAE is not “finished,” Iran cannot close Hormuz indefinitely, and the war is not fundamentally about China.