Inflation/Deflation

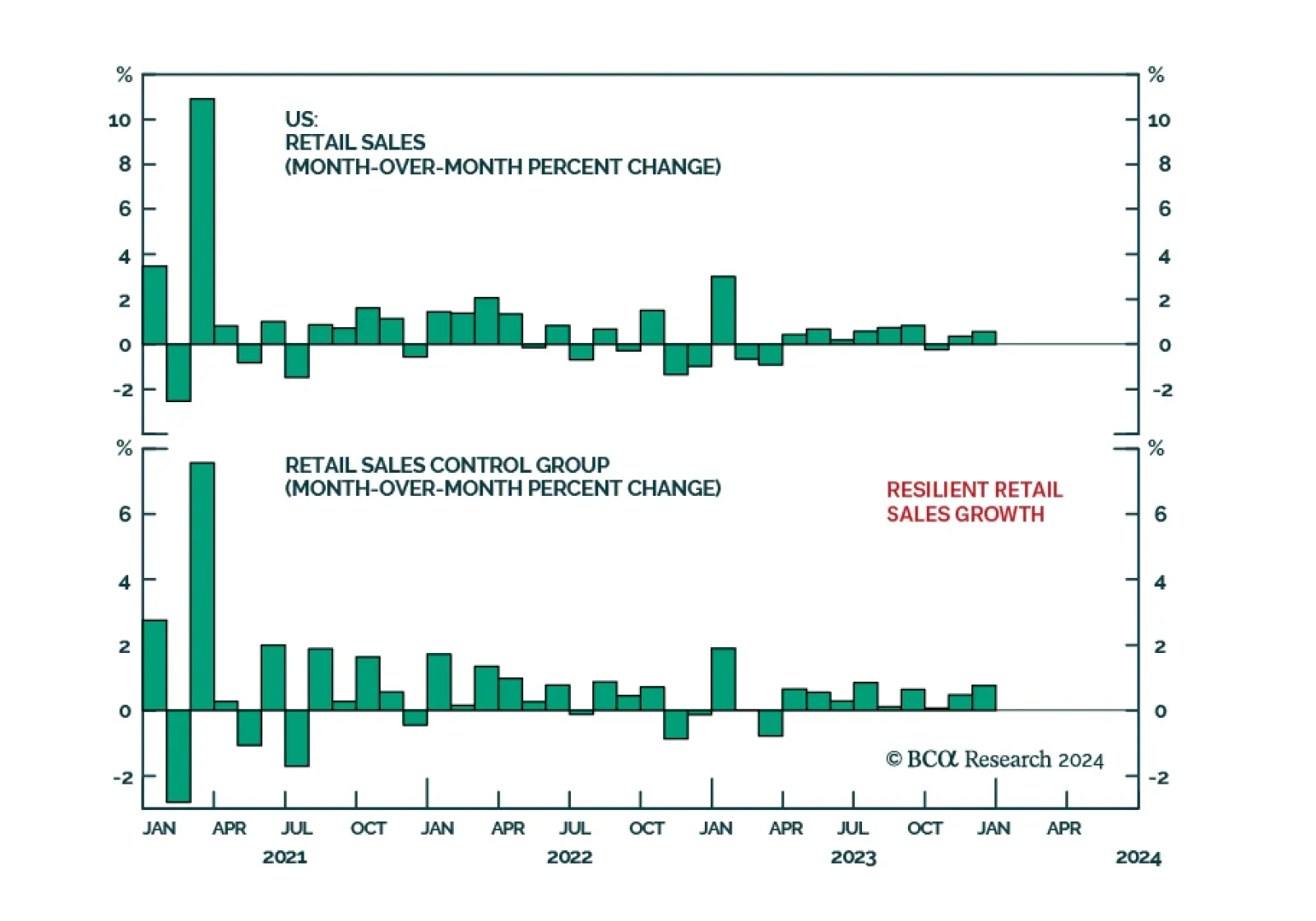

The US retail sales release delivered a positive signal about the US economy in December. The 0.6% m/m increase in overall retail sales beat expectations of a more muted acceleration from 0.3% m/m to 0.4% m/m. Importantly, the improvement was broad-based with…

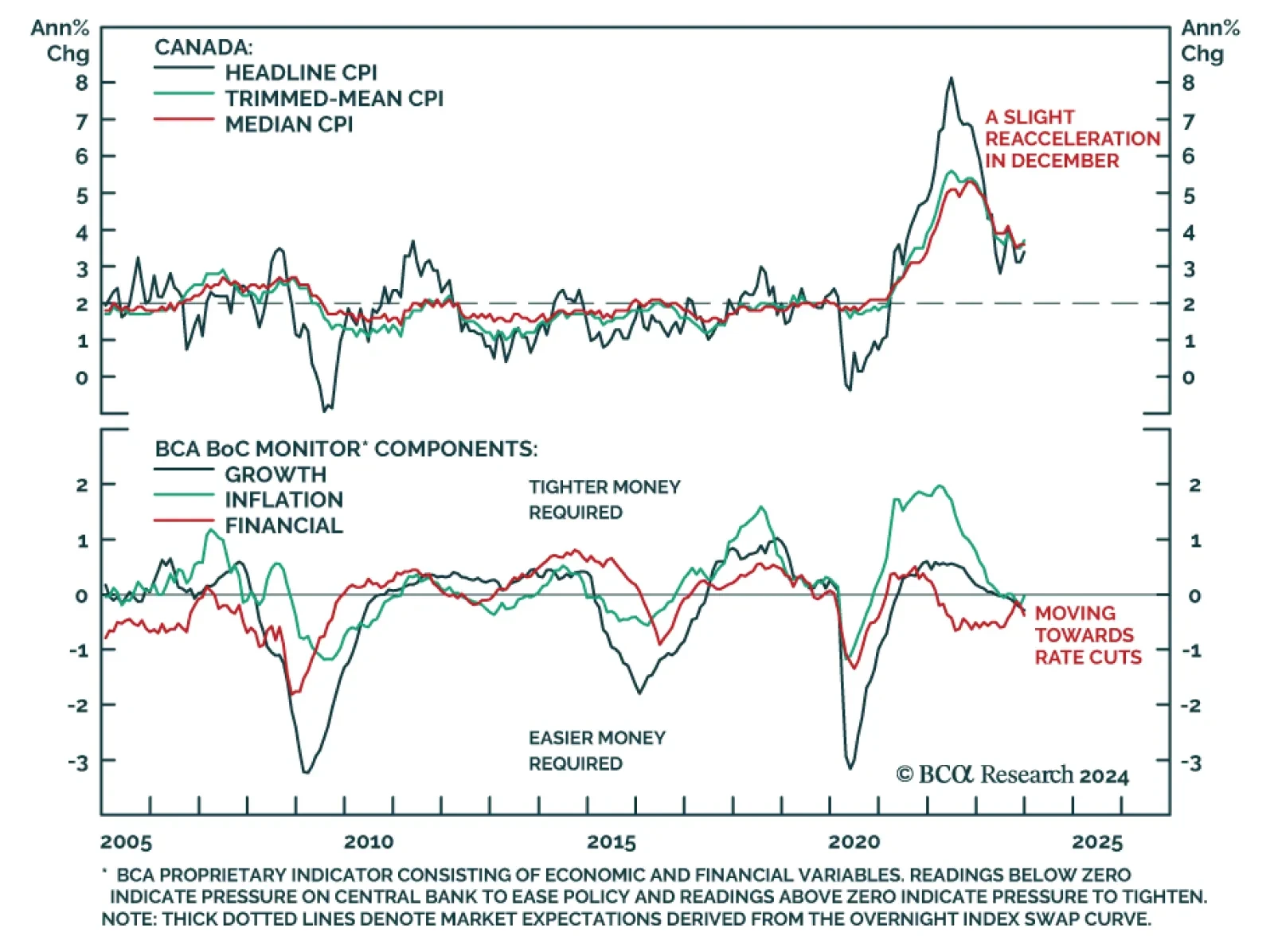

Canadian government bond yields jumped on Tuesday, with the 10-year yield rising by nearly 14 basis points. While most other major DM government bonds also sold off, the move in Canadian yields was relatively more pronounced. Both global and domestic forces…

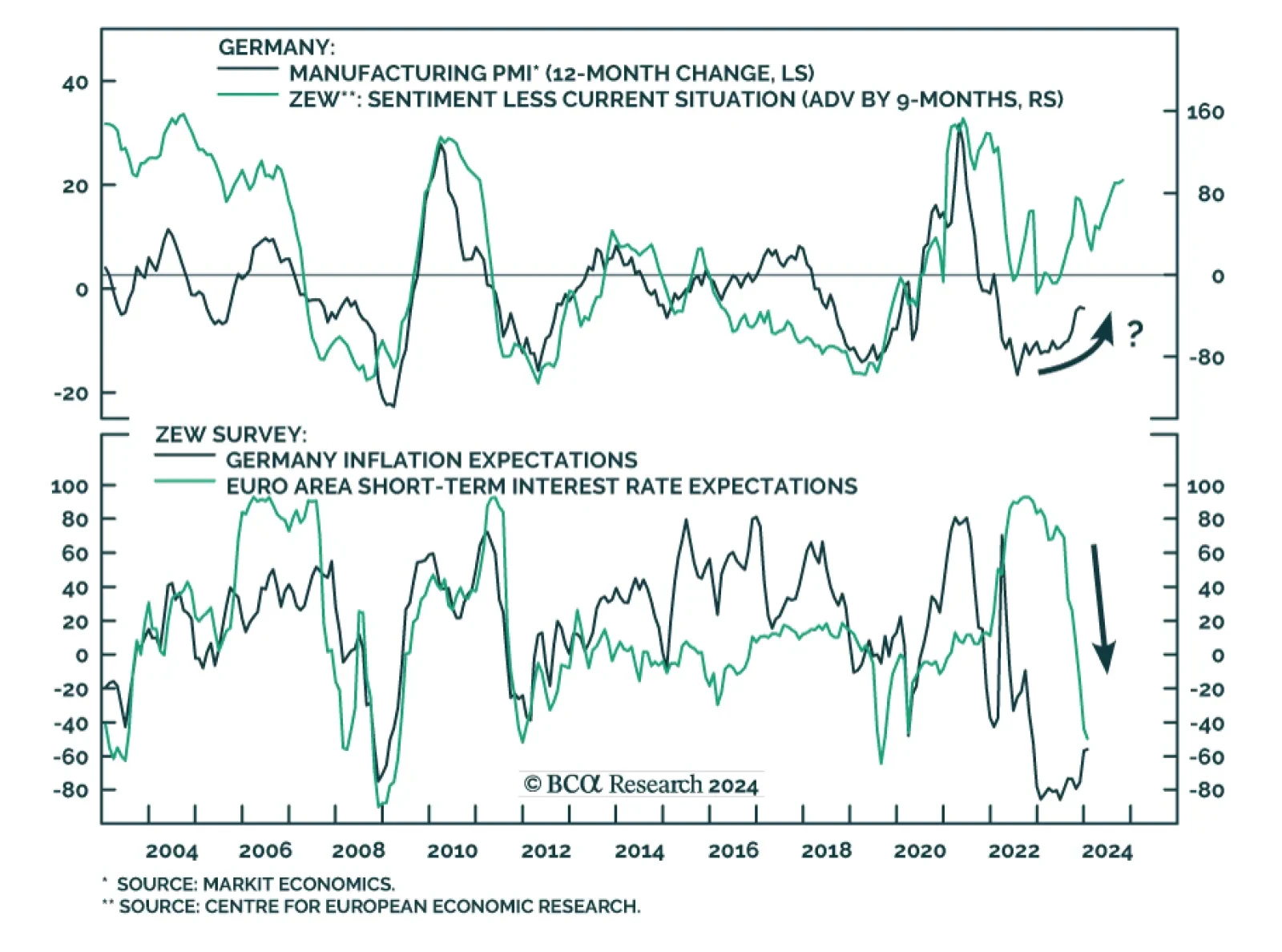

Results of the ZEW survey sent a slightly positive signal on German investor sentiment. The economic expectations indicator rose to an 11-month high in January – beating consensus estimates of a decline. This increased optimism about the outlook reflects an…

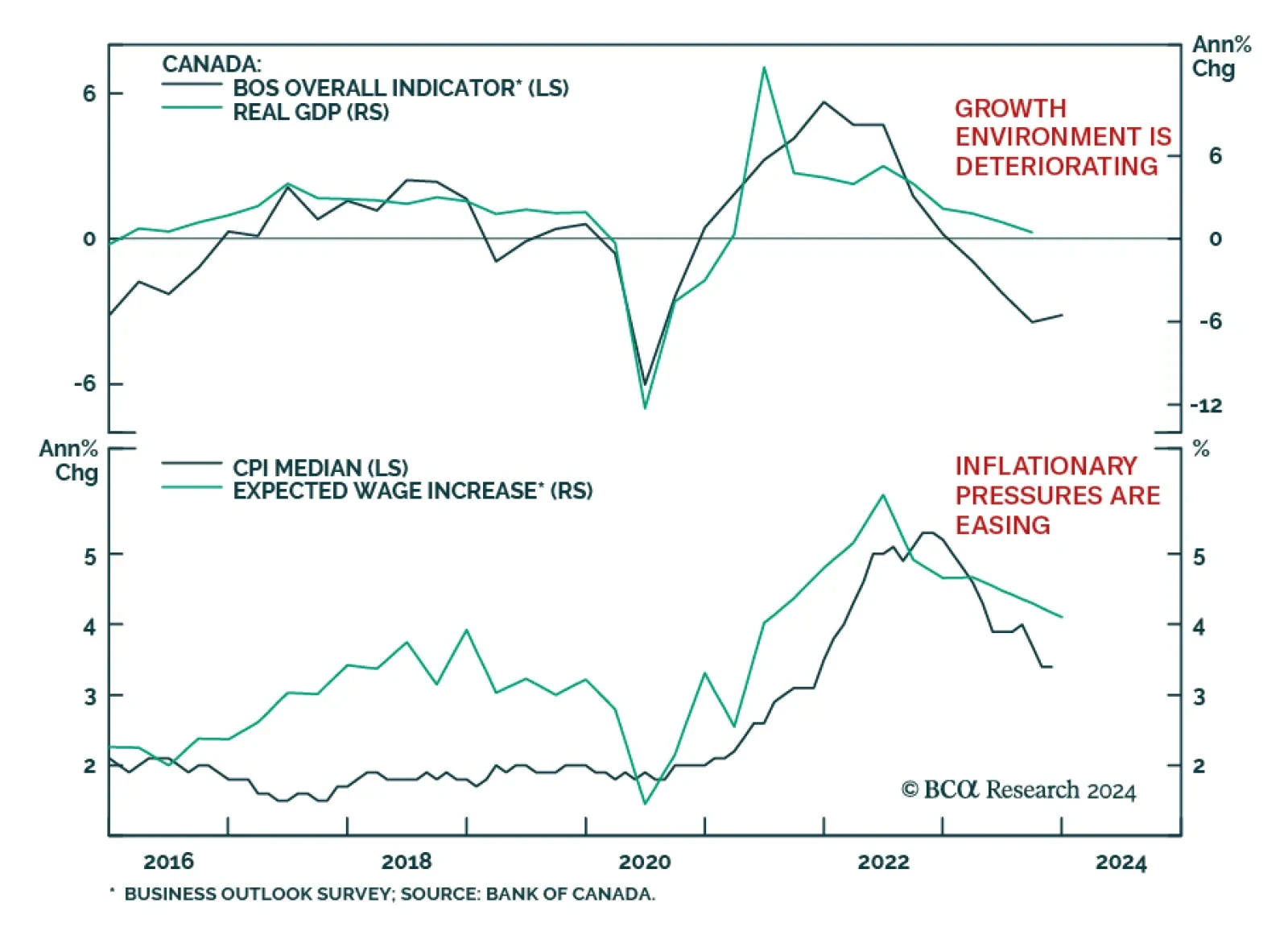

Canada’s Business Outlook Survey (BOS) indicator increased slightly in Q4, suggesting that sentiment stabilized at the end of 2023. In particular, easing inflationary pressures amid weaker demand and greater competition drove the 0.3-point uptick. Notably,…

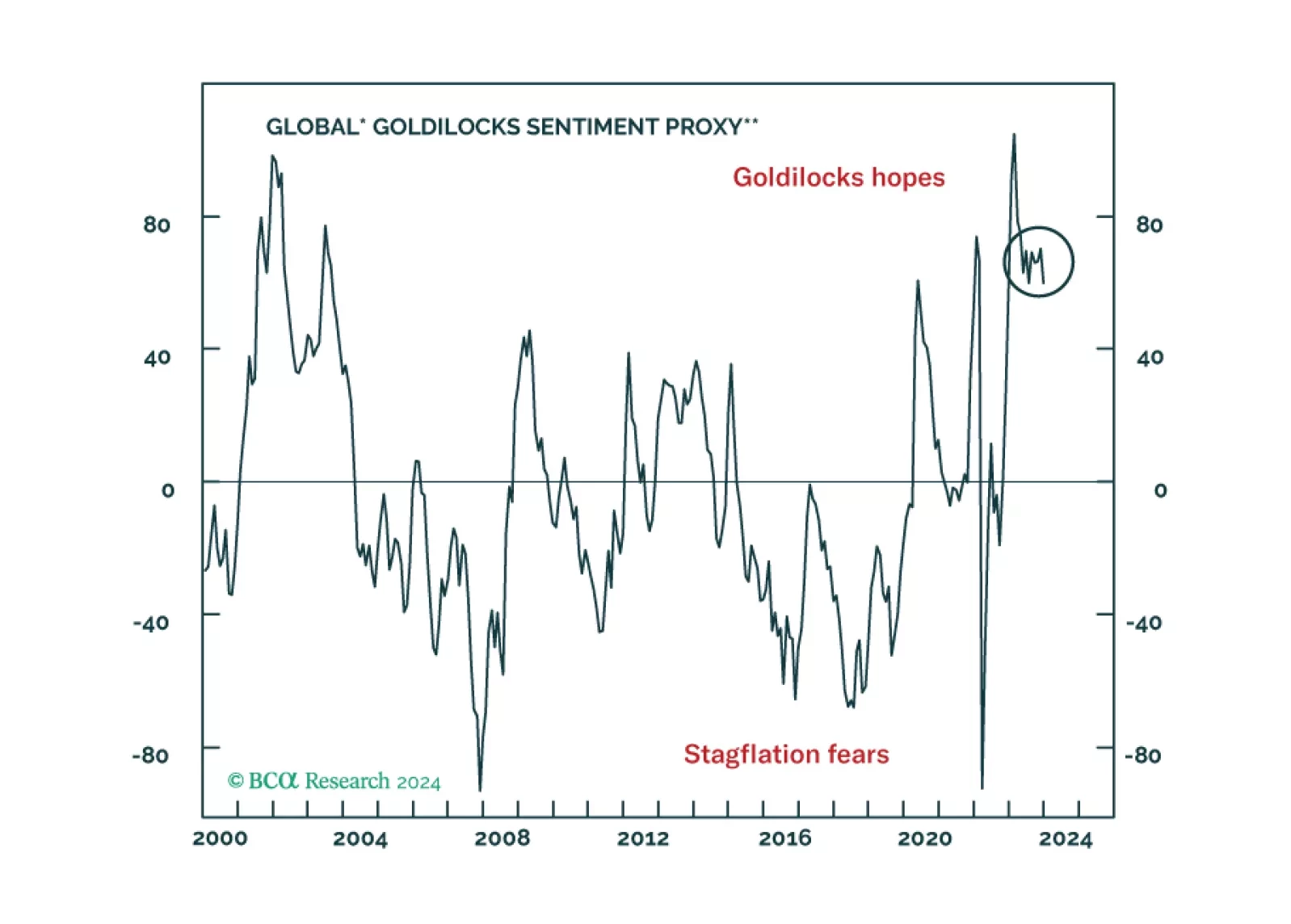

The soft-landing narrative has won, but is too much of a good thing now expected by investors?

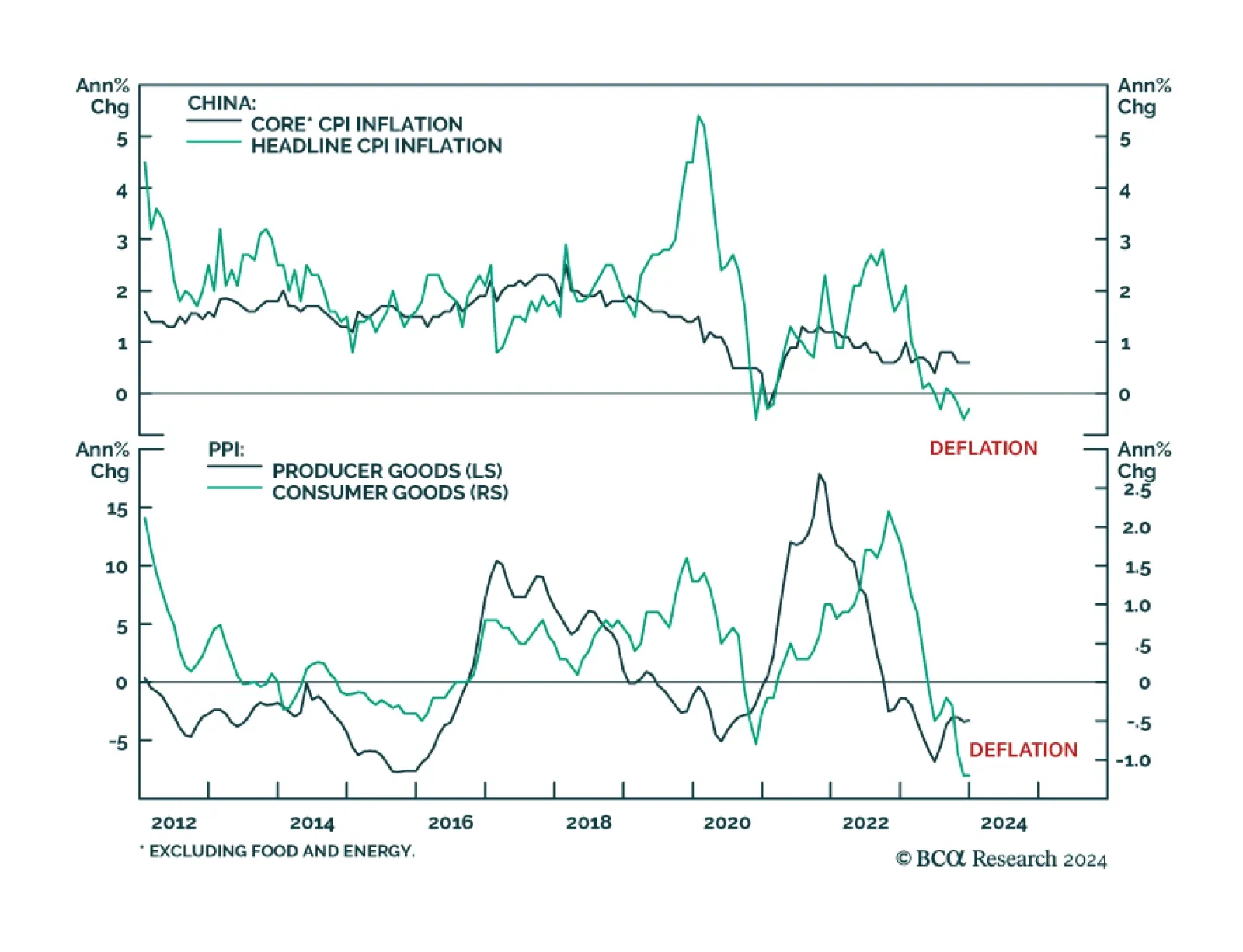

On the surface, domestic economic data painted a mixed picture of conditions in China at the end of 2023. On the positive side, the December trade data beat expectations. The dollar value of Chinese imports expanded by 0.2% y/y, surprising anticipations…

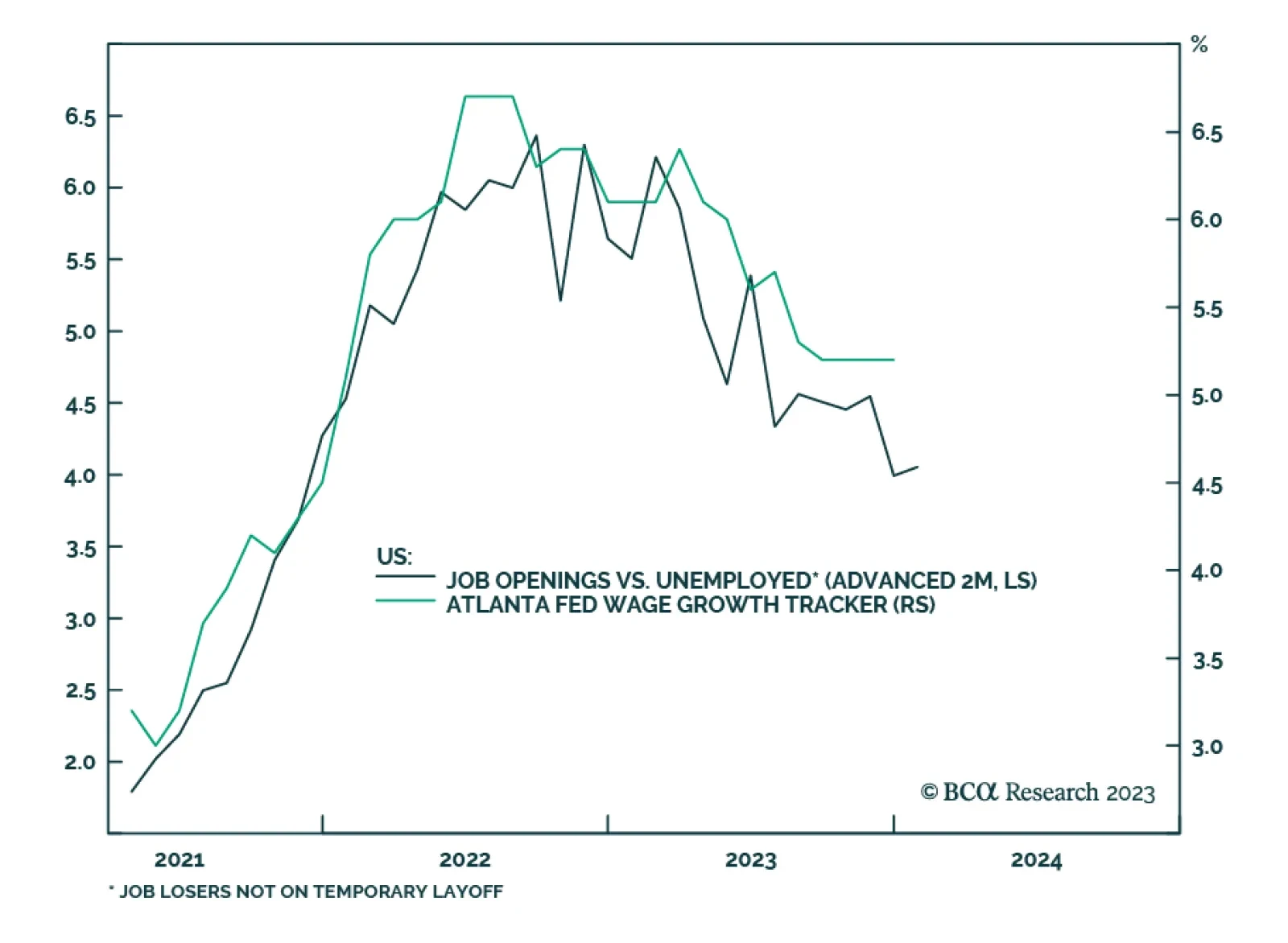

The best leading indicator for post-pandemic US wage inflation is the ratio of job vacancies to ‘bad’ unemployment (V/U), where bad unemployment refers to ‘job losers not on temporary layoff’. This ratio has already declined from 6.4 to 4.1 and wage…

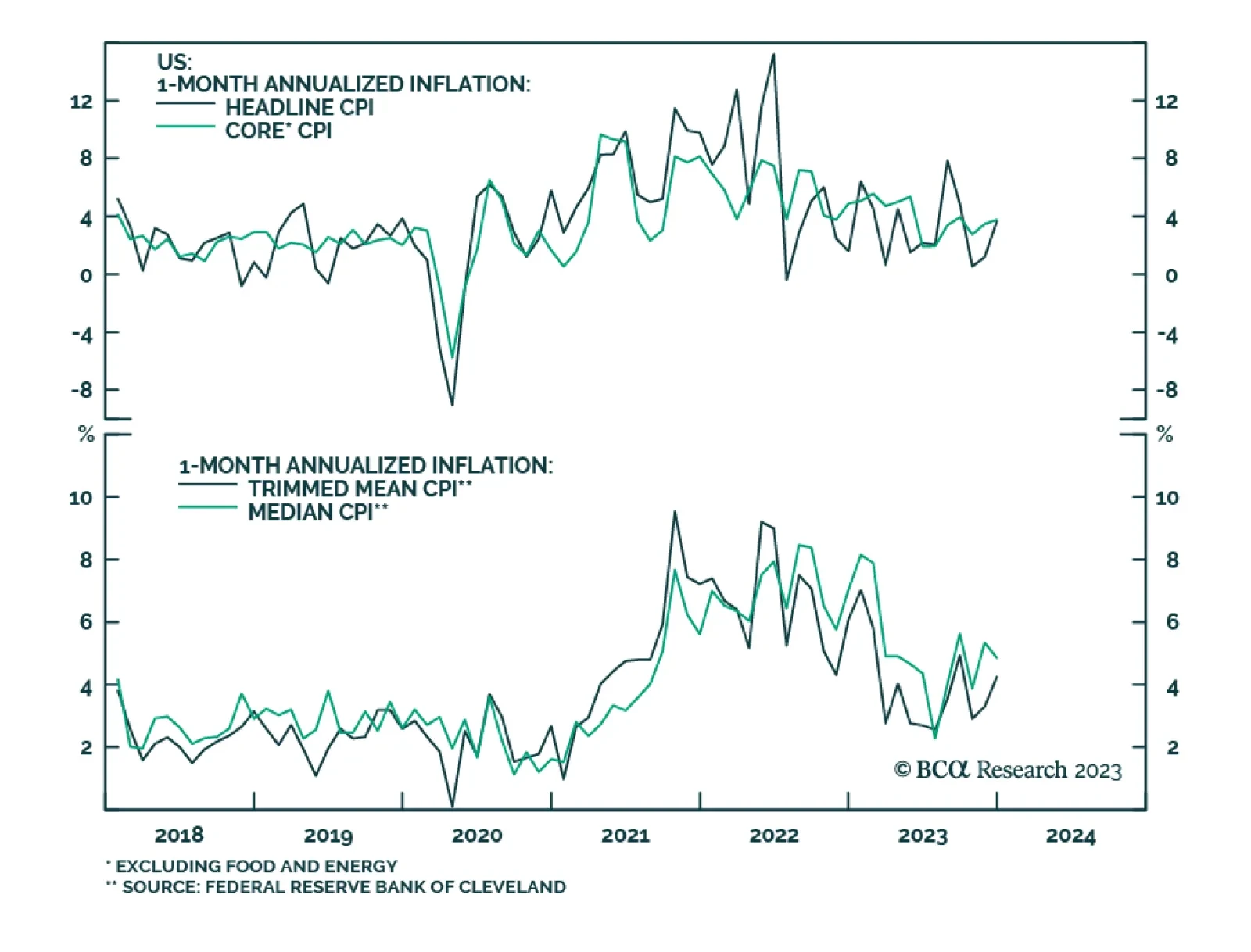

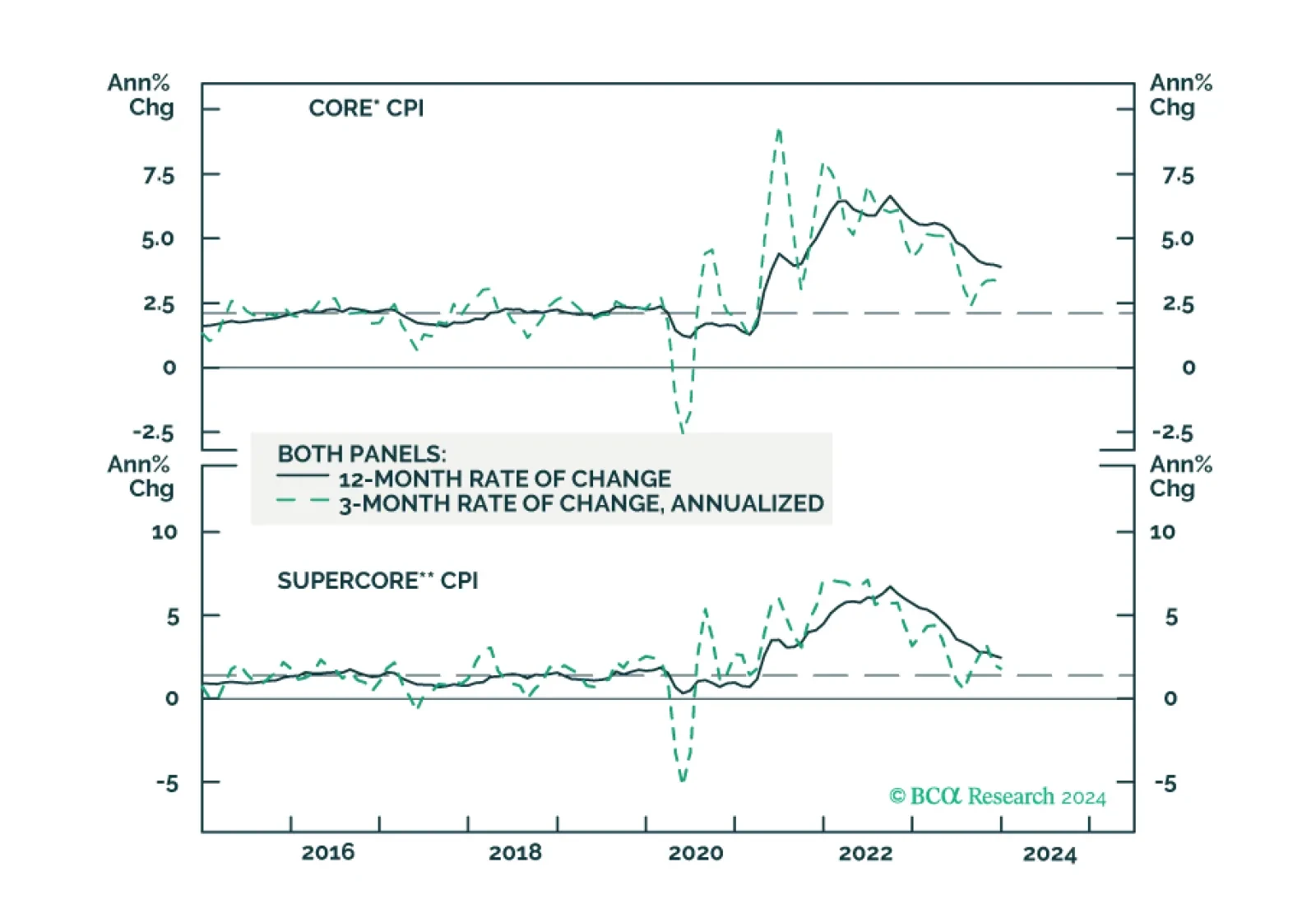

US CPI inflation for December came in slightly hotter than anticipated. Headline inflation accelerated from 0.1% to 0.3% on a month-over-month basis and rose from 3.1% to 3.4% on a year-over-year basis. Both the monthly and yearly changes in headline…

We update our inflation forecast following this morning’s CPI report.

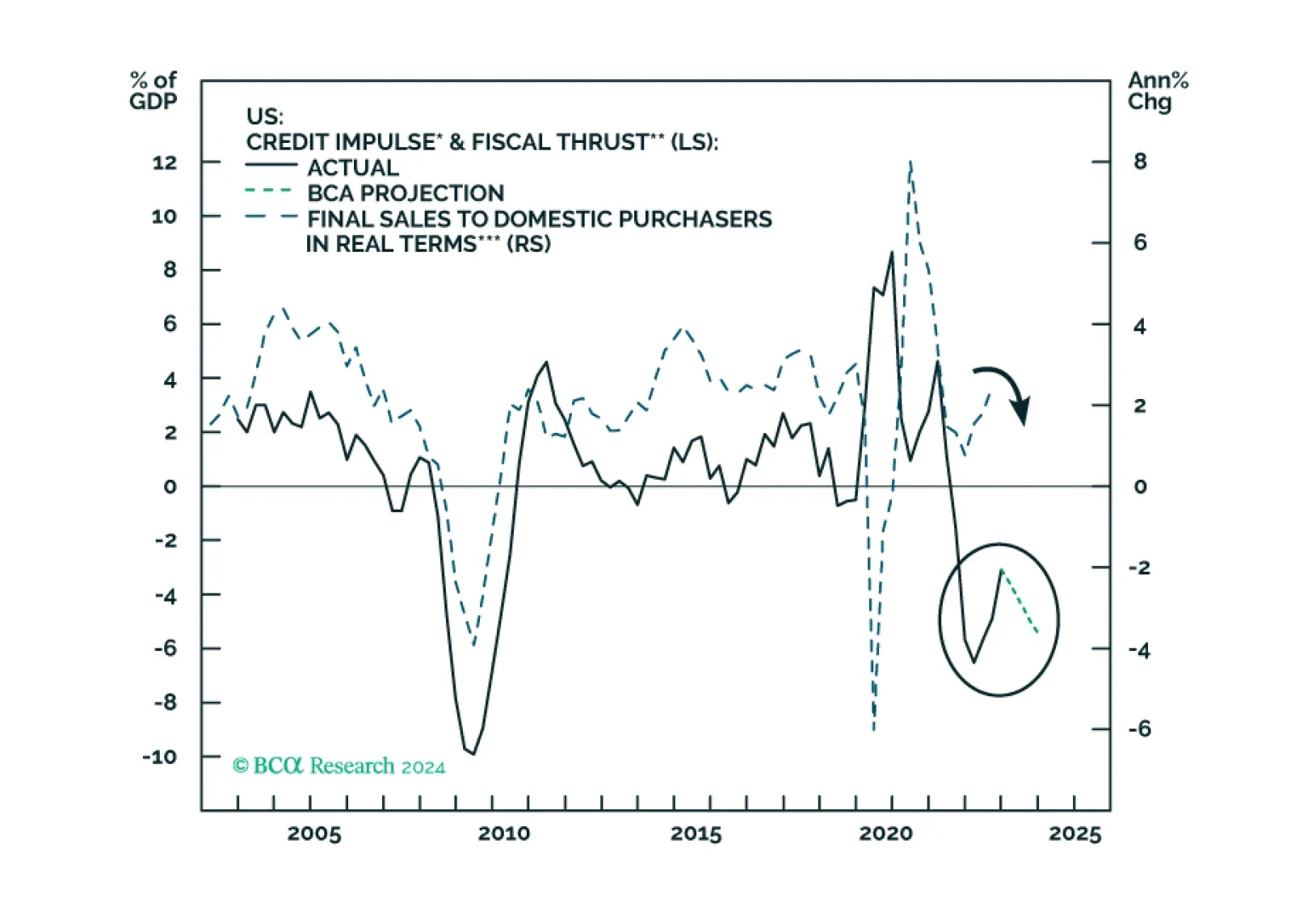

The combined US credit impulse and fiscal thrust indicator will likely relapse in 2024, heralding growth weakness. Stalling US sales volume and falling inflation, combined with sticky labor costs, will herald a non-trivial profit margin compression. The recent increase in Asian exports will likely prove to be a mid-cycle improvement rather than a cyclical recovery.