Fixed Income

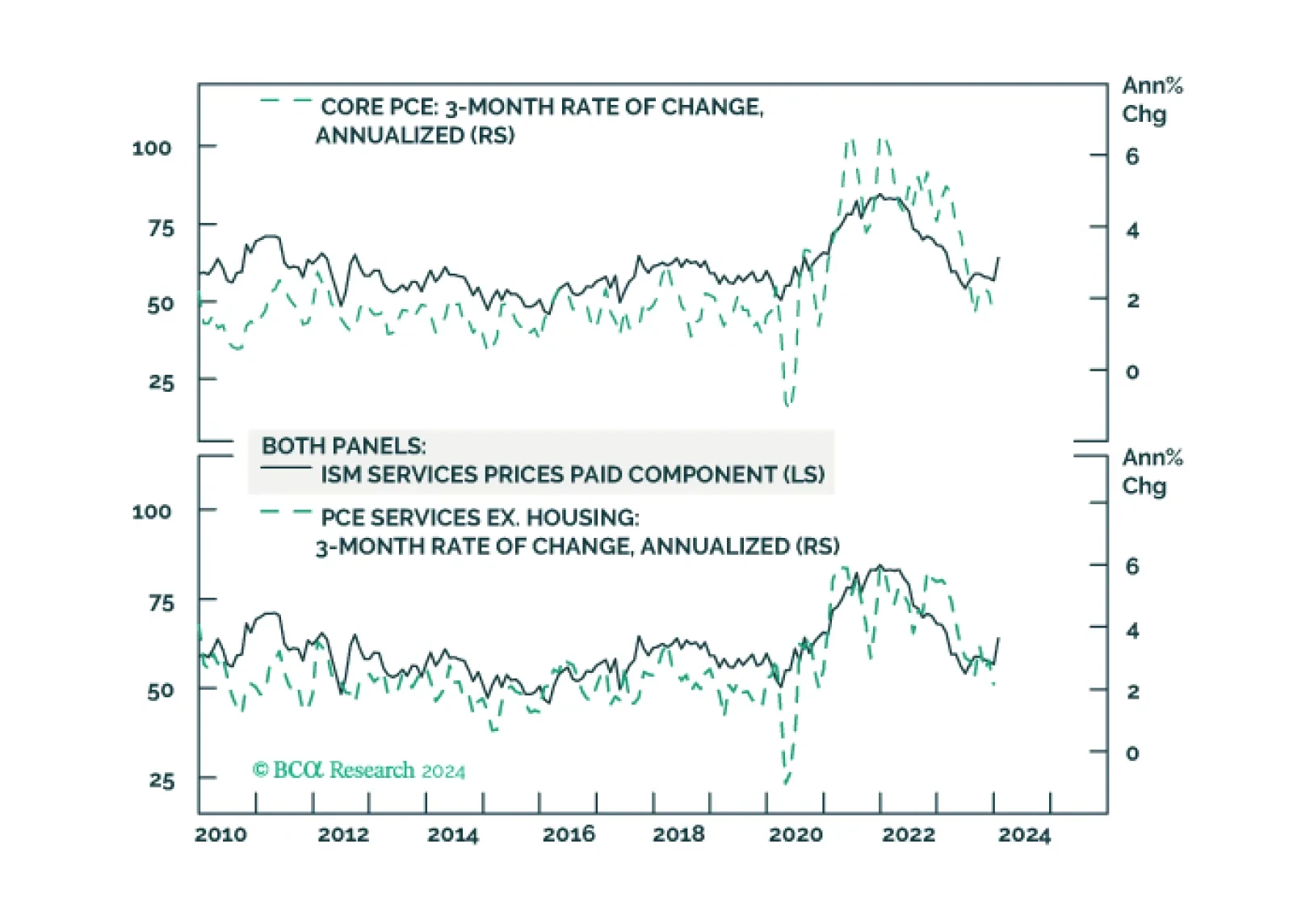

Treasury yields continued to push higher on Monday, bringing the total increase over the past two trading days to 29bps. The move comes on the back of strong economic data releases indicating that conditions in the US are resilient. Notably, Friday’s…

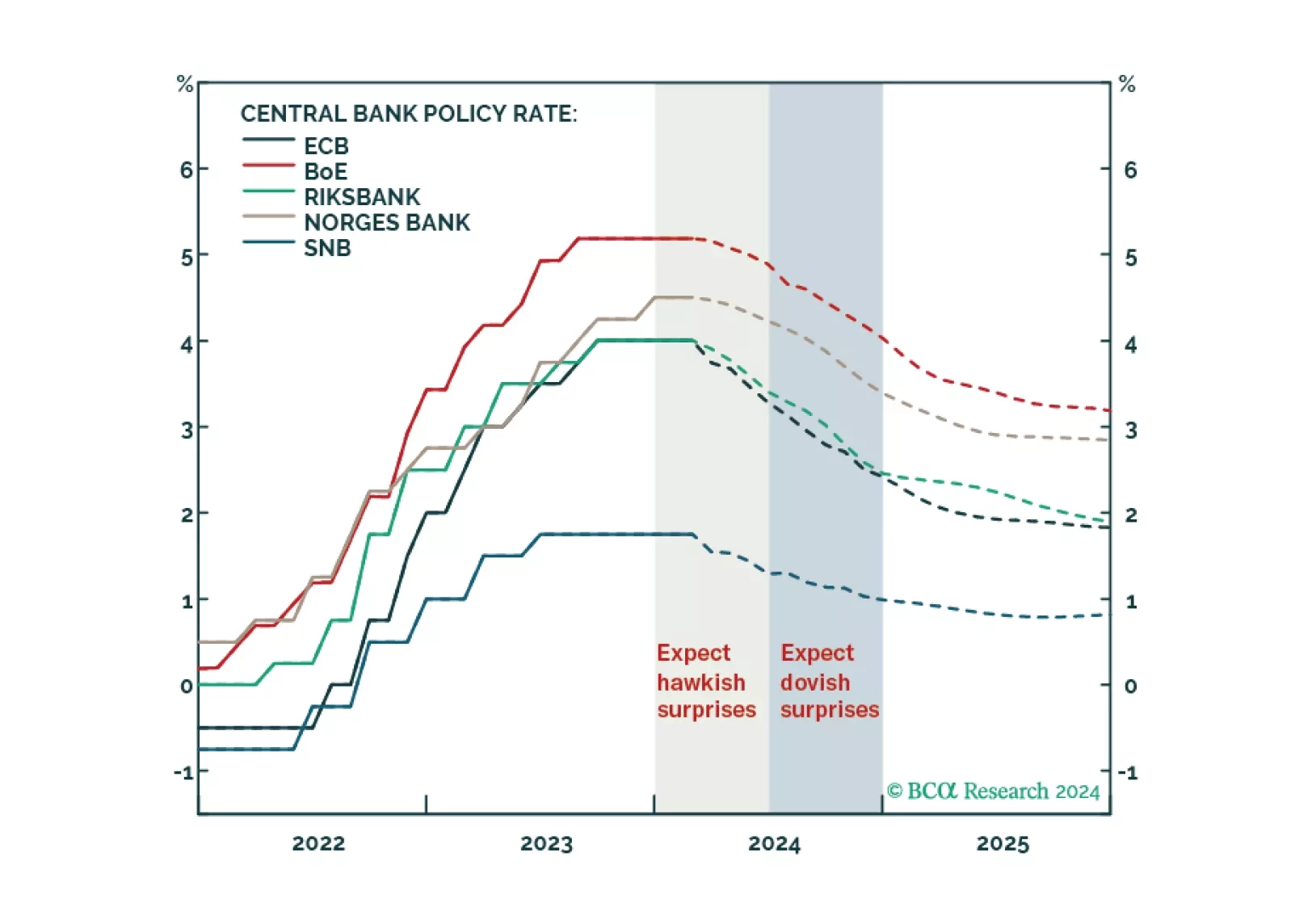

BCA Research’s European Investment Strategy service upgrades Swedish government bonds to neutral from underweight within European fixed-income portfolios. The Riksbank kept its policy rate steady at 4% last week. Governor Erik Thedéen and the Riksbank…

Our Central Bank Monitors support European central bankers’ decision to hold rates steady. Find out what it means for European fixed-income portfolio allocation.

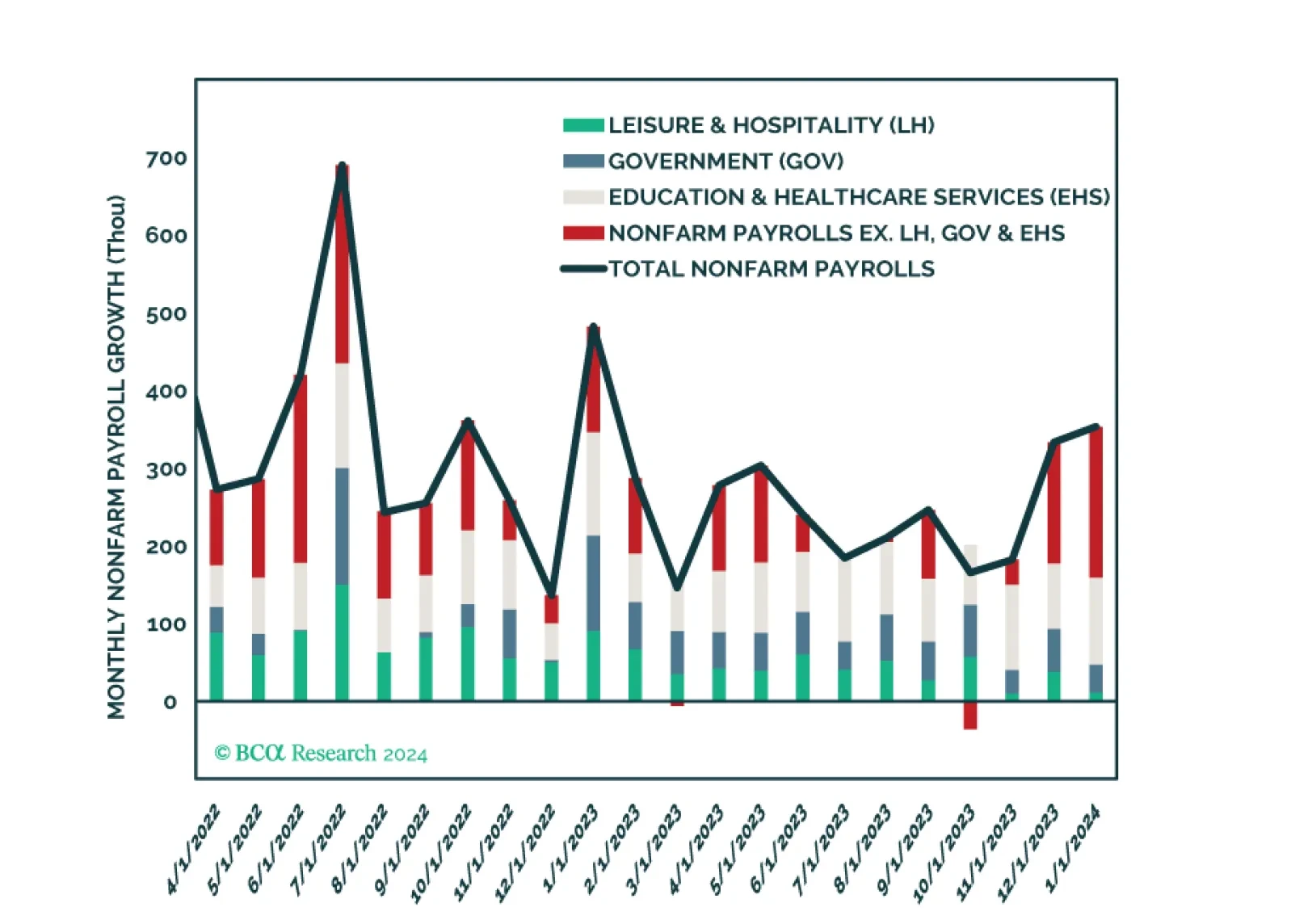

The US Employment report came in well above consensus expectations on Friday, delivering a strong positive signal on labor market conditions in January. The 353 thousand increase in nonfarm payroll employment beat expectations of a slowdown to 185 thousand.…

Our thoughts on bond positioning following this morning’s employment data.

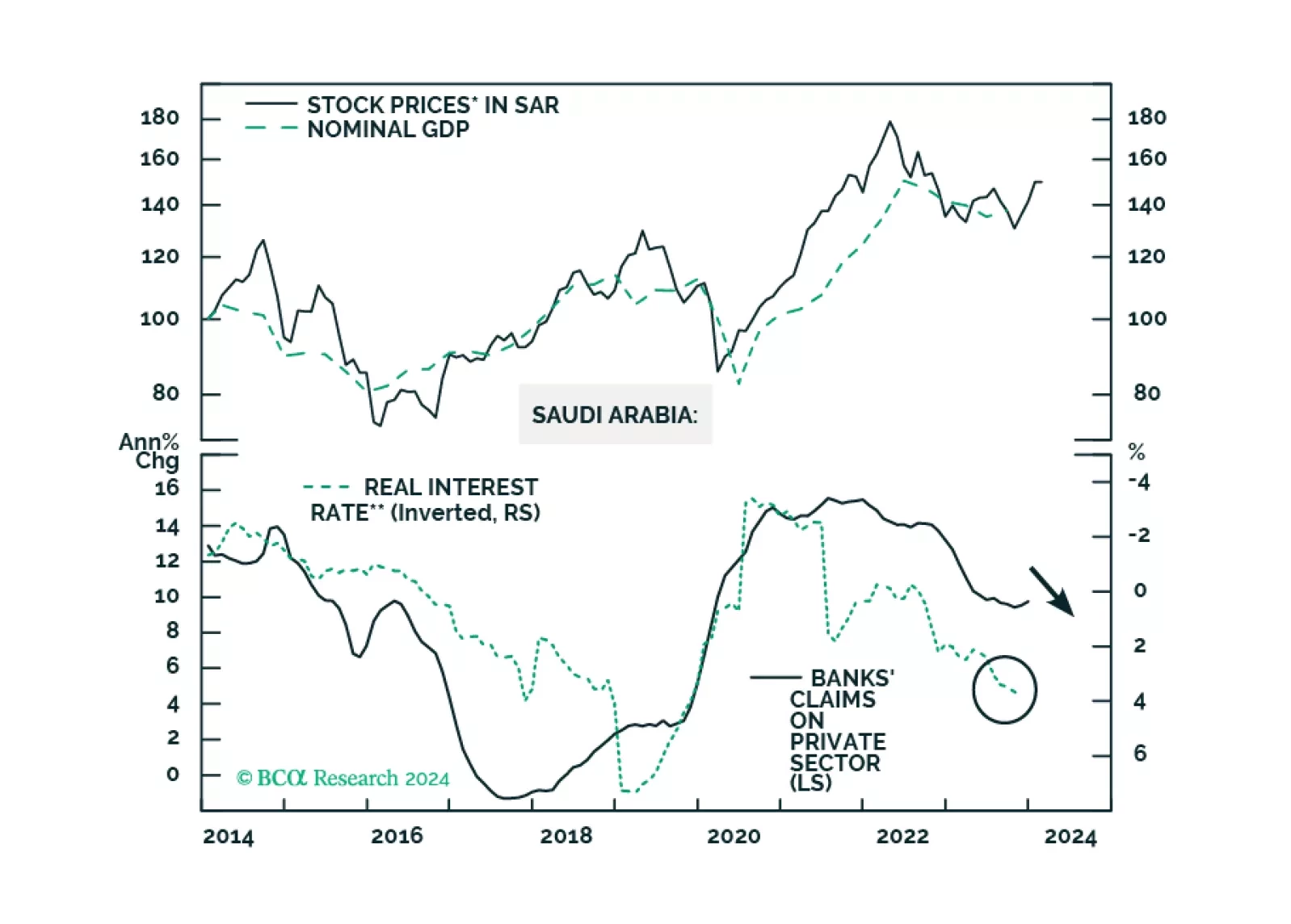

The Saudi economy is facing internal and external headwinds. The geopolitical conflict is also escalating in the Middle East. EM equity portfolios should stay neutral on Saudi stocks. EM sovereign credit portfolios should upgrade Saudi Arabia from neutral to overweight.

As expected, the Bank of England voted to keep its bank rate unchanged at 5.25% on Thursday – maintaining policy on hold for the fourth consecutive meeting. Two of the nine MPC members voted in favor of a 25bps rise (one less than in December) while one…

The late-2023 broad-based rally across major global financial assets fizzled at the start of this year, with most of the assets we track selling off in January. Chinese stocks continued to perform exceptionally poorly, with the investable and domestic…

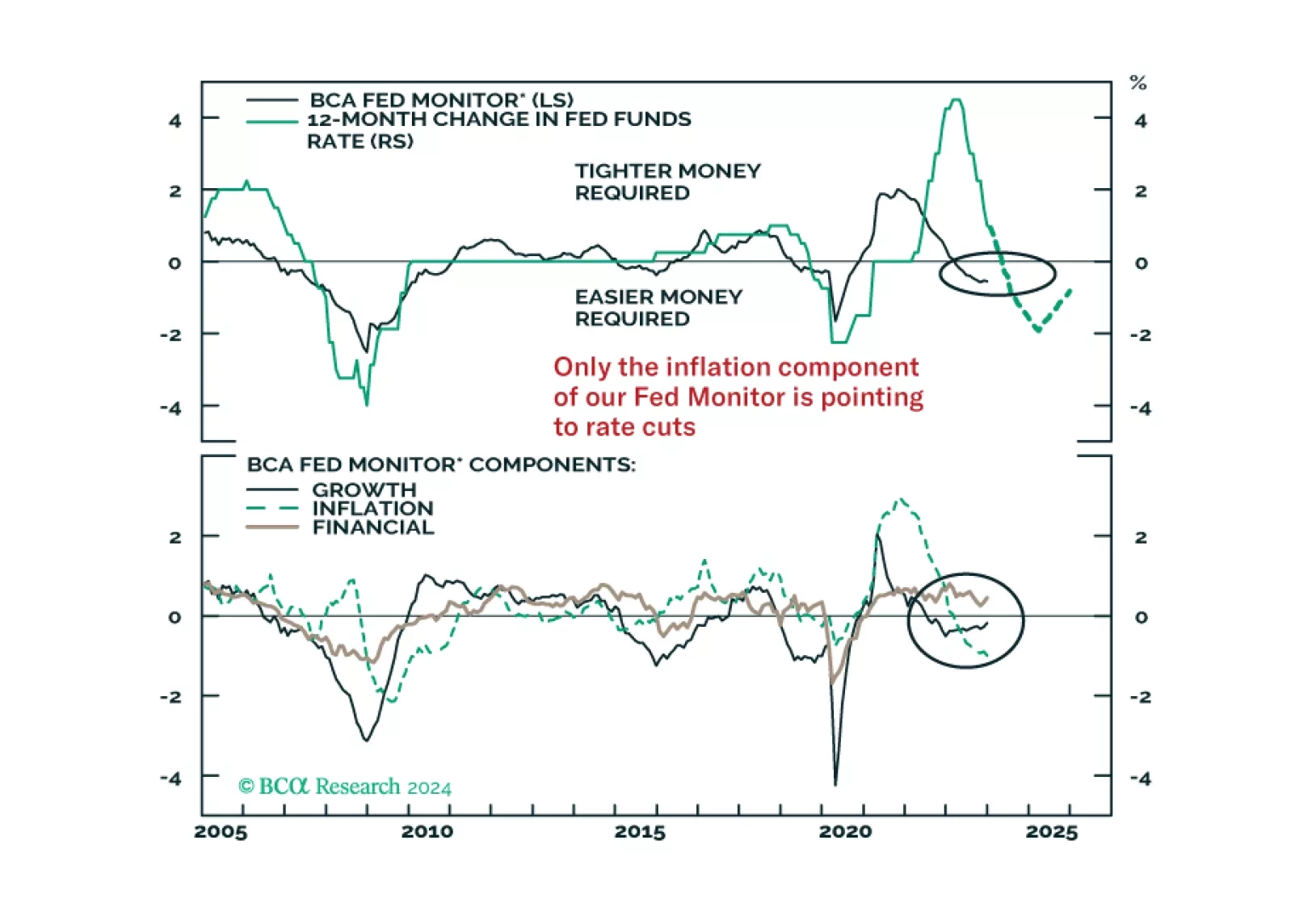

In this Insight, we share our thoughts on yesterday’s FOMC meeting and the Fed’s likely next moves, with implications for US bond strategy.