Fiscal

Markets have ripped in July, ignoring underwhelming payrolls and retail sales figures. This was our bet, so we don't think this is a mistake. The economy is transitioning from one catalyzed by cash to one led by lower borrowing rates. The combination of a growth slowdown tempered fiscal policy, and an uber-dovish Fed is good for bonds and equities, which has not yet been priced by markets.

The yen’s discount, surplus, and rising real rates line up for a multi-quarter surge. Find out why EUR/JPY is the first short and when USD/JPY follows.

We will only move to a fully defensive stance if the “whites of the recession’s eyes” appear. So far, they have not. We will be increasingly looking to our MacroQuant model for guidance on when the next turning point in markets may come.

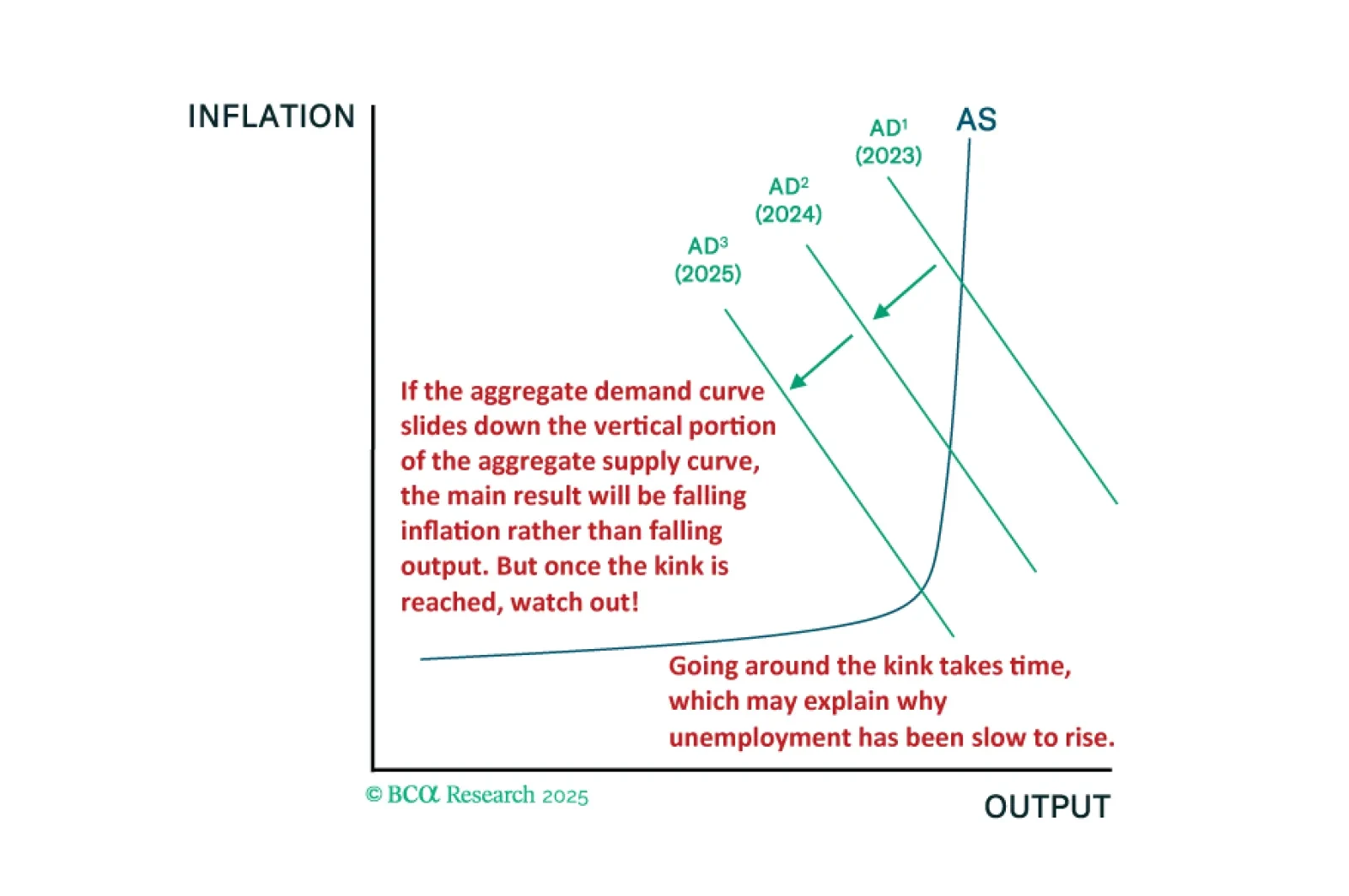

The fact that the US economy has been slower to deteriorate than in past cycles is entirely consistent with our kinked Phillips curve framework. We will be looking to our MacroQuant model for guidance on when to turn fully defensive.

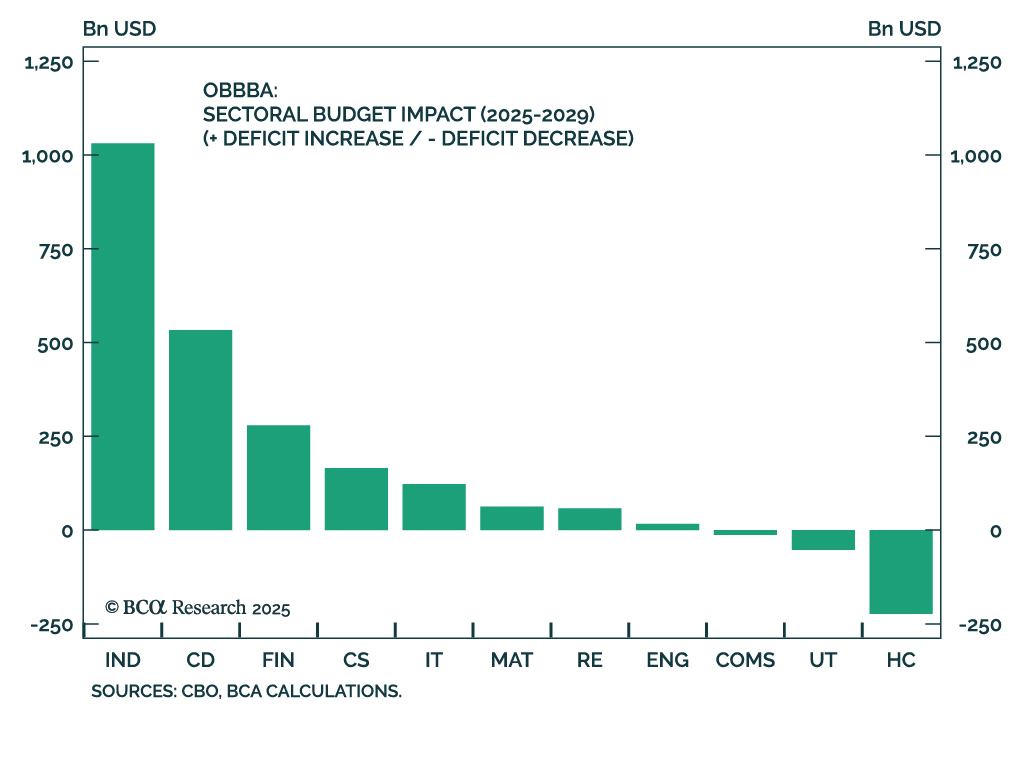

Despite macro headwinds, the OBBBA clearly favors Industrials, Financials, and Consumer Discretionary equity sectors. A carefully constructed, factor-aware basket in these sectors is well positioned to outperform in a fiscal-driven, uncertain environment.

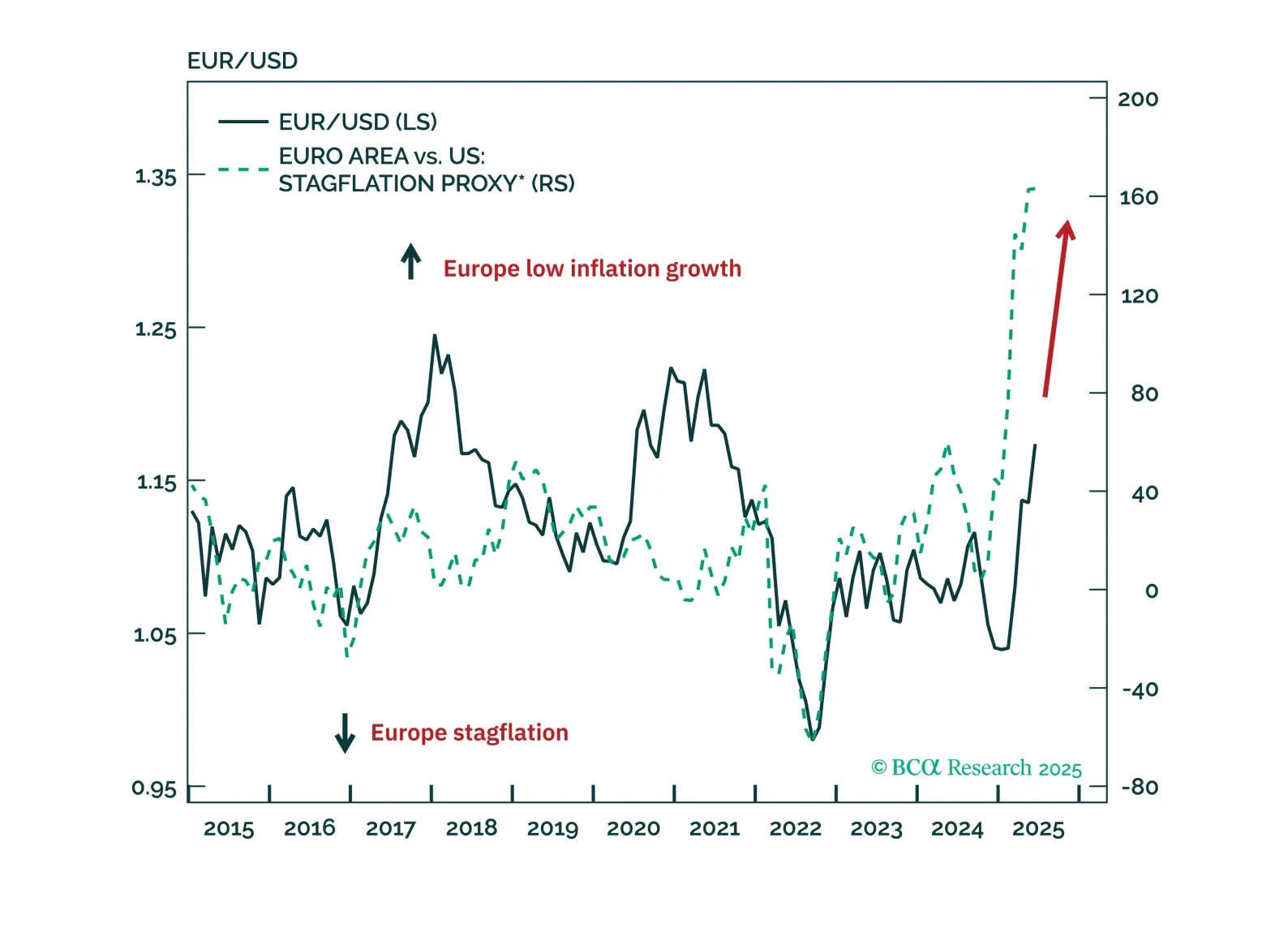

EUR/USD is in a multi-year bull market. A short-term pause is likely, but the longer-term trend remains higher toward 1.25, and eventually 1.40.

We will abandon our recession call if US economic data show clear signs of stabilization over the summer months. For now, that has not happened. Maintain a modest underweight to stocks but look to get more defensive if MacroQuant’s equity z-score falls below -1.