Equities

The Strait of Hormuz remains closed. Even if the Strait were to open tomorrow, global consumers will be squeezed for the rest of the year. However, AI capex is accelerating, and signs of ROI are emerging. This capex boom will keep the world from an economic downturn. Upgrade equities to overweight and downgrade cash to underweight. Upgrade the US and downgrade Europe and Australia. Upgrade Communication Services.

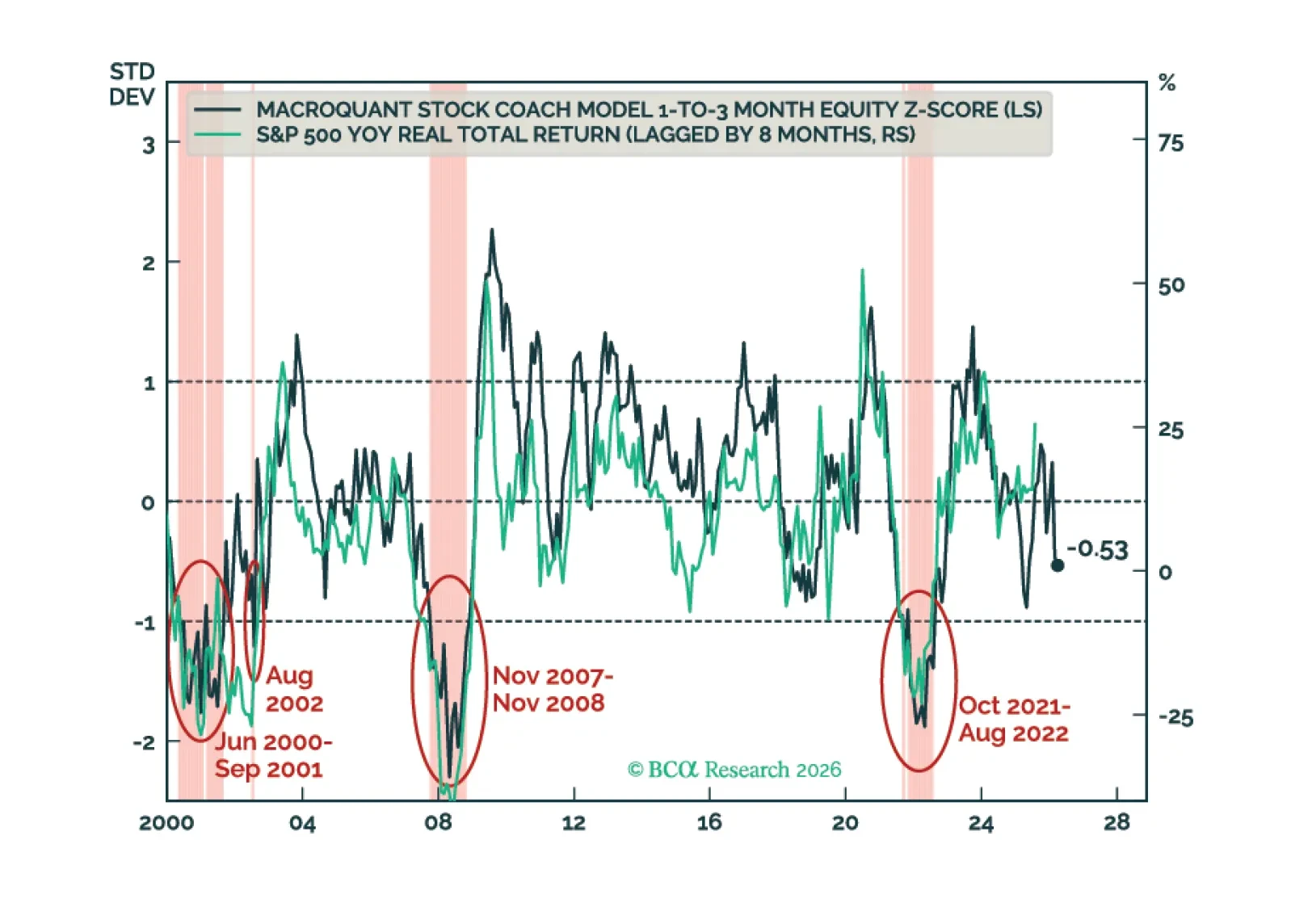

MacroQuant recommends an underweight position in equities, favors a below-benchmark duration stance in fixed-income portfolios, is neutral-to-slightly positive on the US dollar, remains neutral on gold, upgrades copper to neutral, and is very bullish on oil.

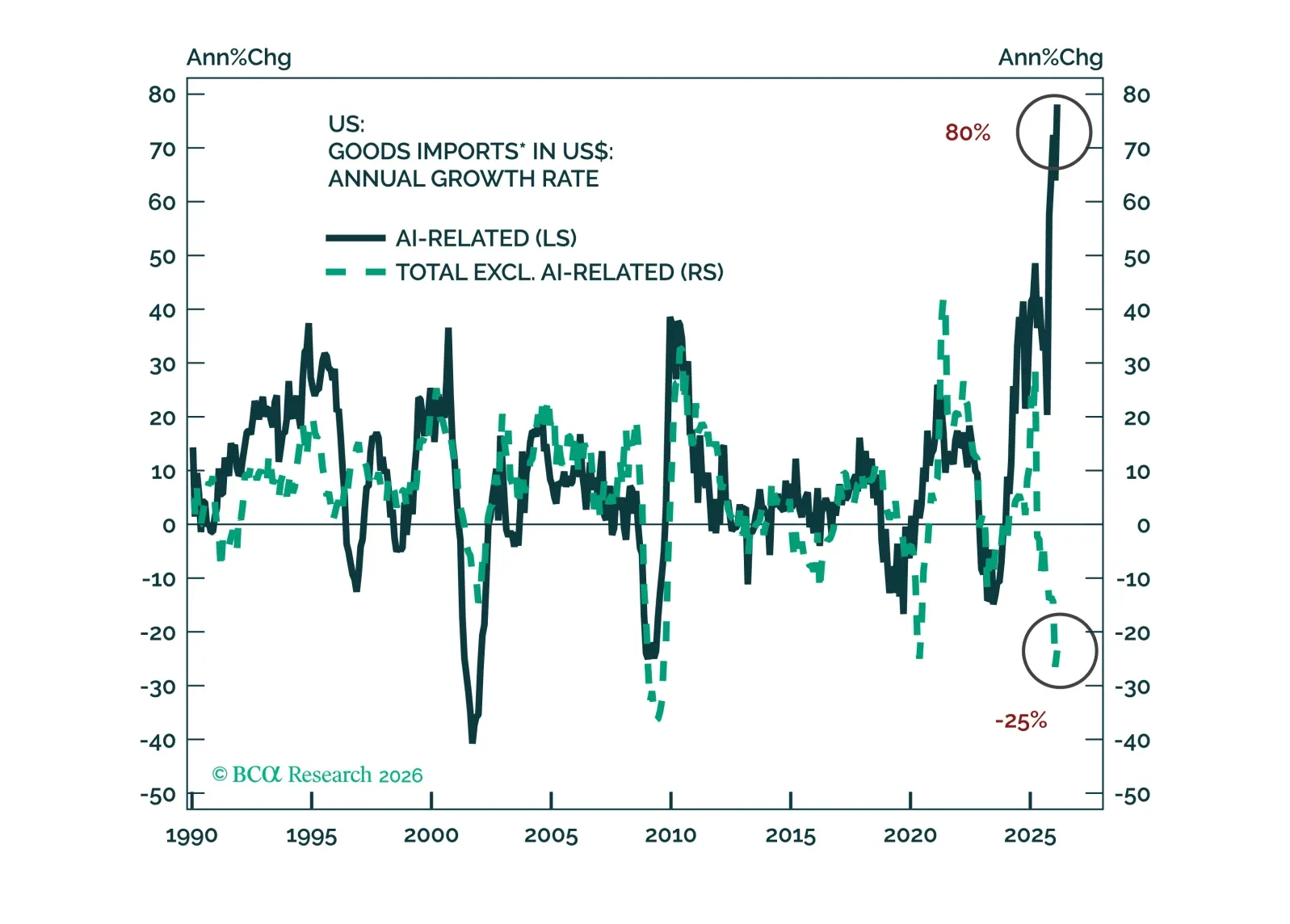

Global trade has held up despite US non-AI import volumes contracting by 25% over the past 12 months. The strength in global trade has concentrated in two areas: (1) imports of AI-related hardware and (2) developing countries’ imports, especially from China. Will these continue?

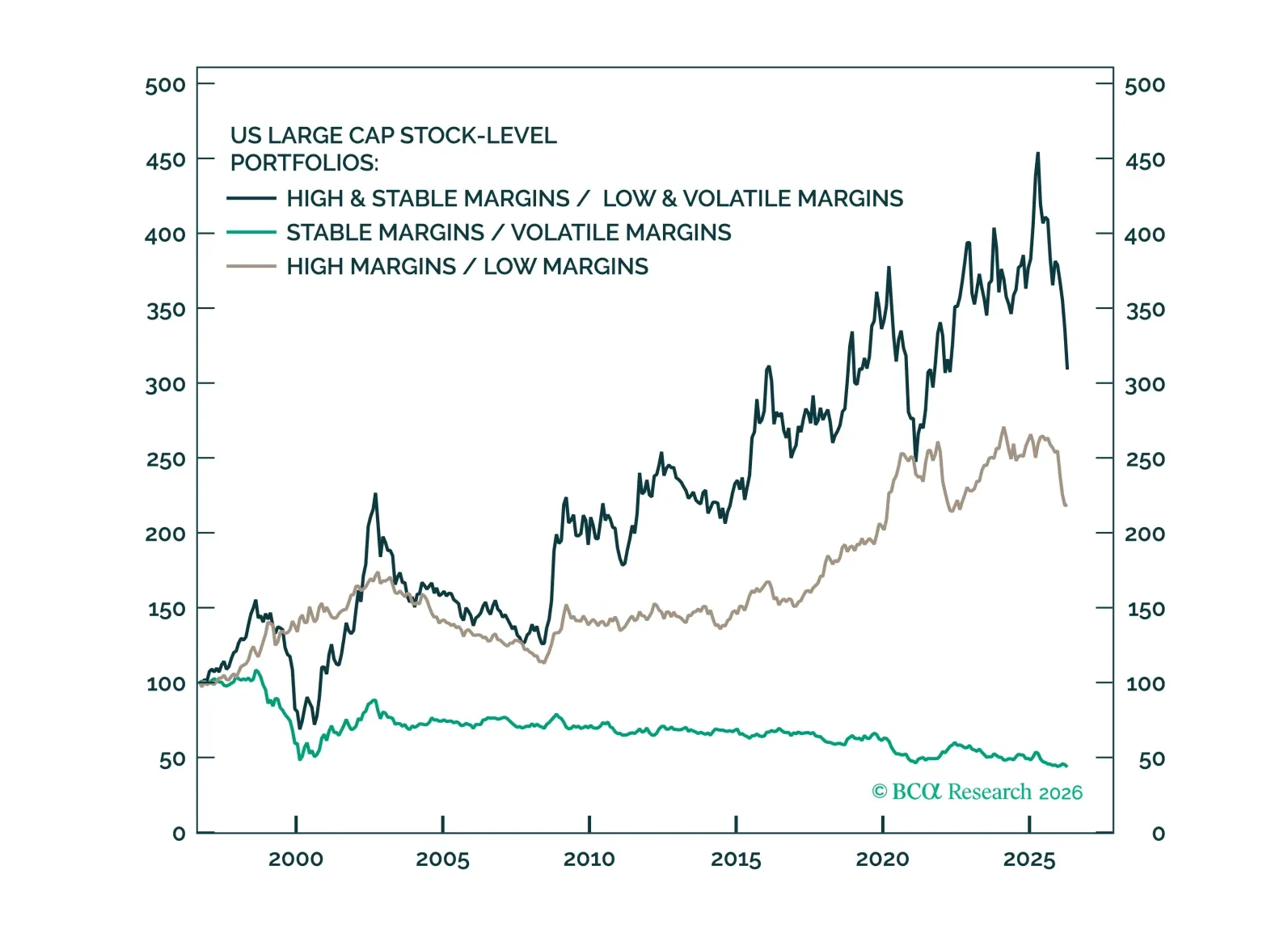

Based on our previous work on margins, three aspects of margins may matter to investors: their level, their variability, and their likely trend. We add two margin-themed baskets: a stock-level High & Stable vs. Low & Volatile basket and an industry-level AI-Supported vs. AI-Insulated basket.

Based on our previous work on margins, three aspects of margins may matter to investors: their level, their variability, and their likely trend. We add two margin-themed baskets: a stock-level High & Stable vs. Low & Volatile basket and an industry-level AI-Supported vs. AI-Insulated basket.

The longer the Strait of Hormuz remains closed, the more likely the Eurozone will experience an economic recession, as higher energy prices, supply chain disruptions, and weaker global demand slowly grind the European economy to a halt. The relief rally is running out of time. Investors should add exposure to the best-performing sectors following past oil supply shocks: Energy, pharma, and utilities.

The S&P 500 finished last week at an all-time high as optimism over earnings has pushed the Iran conflict out of the spotlight. Despite uncertainty in the Strait of Hormuz, we do not think investors have enough evidence to justify underweighting equities and other risk assets.

Chinese onshore equities are riding the global “scarcity trade,” powered by tight semi supply and surging alternative-energy demand. How should investors position in this environment?

The S&P 500 rally is likely more than just risk-relief. Market internals reflect strengthening economic growth and higher inflation, with support coming from robust earnings. Tight financial conditions have compressed valuations, particularly within the Tech sector. We are initiating a long Software trade ahead of earnings season, given that multiples have declined and earnings growth is strong.

In this screener report, we explore opportunities in nuclear theme, geopolitical hedge, and winners from AI productivity boom.