Equities

A benign disinflation is probable during the remainder of 2023. Unfortunately, just when most people become convinced that a recession has been avoided, a recession will begin.

There are several widespread market narratives regarding US inflation, the Fed’s policy, global manufacturing/trade and China’s recovery that we disagree with. In this report, we explain our reasoning and where it puts us in terms of investment strategies.

Innovative Tech will face macroeconomic headwinds in a new “higher for longer” interest regime. Yet, the long-term opportunity of the cohort is tremendous. Investors need to be judicious with the timing of adding new capital to these themes to bolster long-term returns.

No, the secular rise in geopolitical risk has not peaked. EU-China trade ties underscore the multipolar context, but this multipolarity is unbalanced, as the US has not reached a new equilibrium with its rivals. While the second quarter is murky, investors should stay defensive this year on the whole.

Through February and March, the number of US ‘job losers’ surged by almost half a million. Constituting the largest two-month increase in Americans who have lost their job since the depth of the pandemic. Unless we see a big drop in the number of job losers in the coming months, the correct investment strategy is still to position for a US recession that starts in 2023.

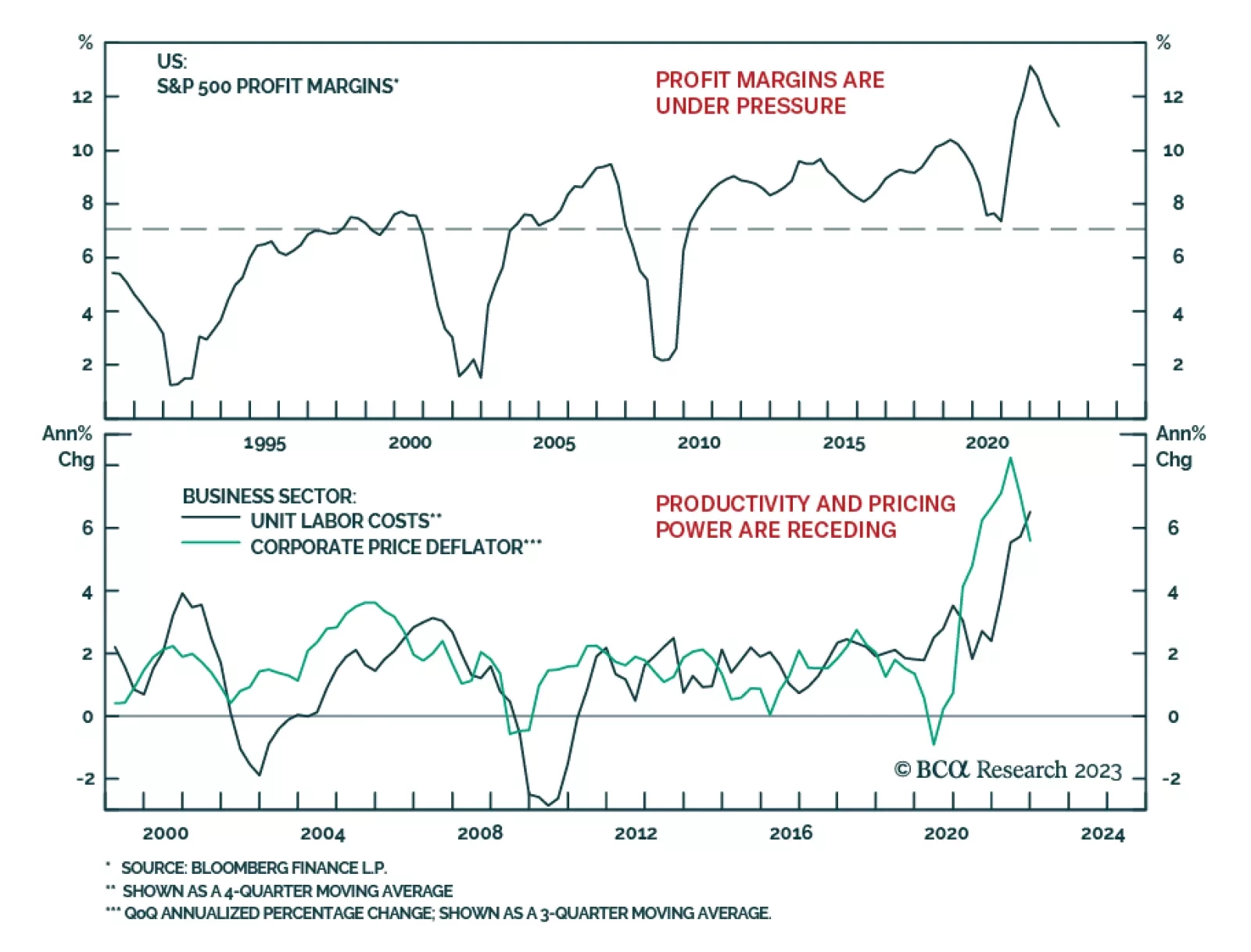

Several signs have emerged that the “bad news is good news” rally has run its course. Despite deteriorating economic data, the Fed is expected to maintain its “higher for longer” stance, disappointing the market. A rate cut is likely is only in case of a severe downturn, but that will not offer support to equities, until earnings growth bottoms. We recommend shifting a portfolio toward a defensive stance, and away from cyclicals at this juncture. We downgrade Auto to an underweight, and Capital Goods and Energy Equipment and Services to an equal weight.

European inflation has further downside and core CPI will soon begin to fall too. However, European growth will remain soggy in Q2. What does this environment mean for investors?