Equities

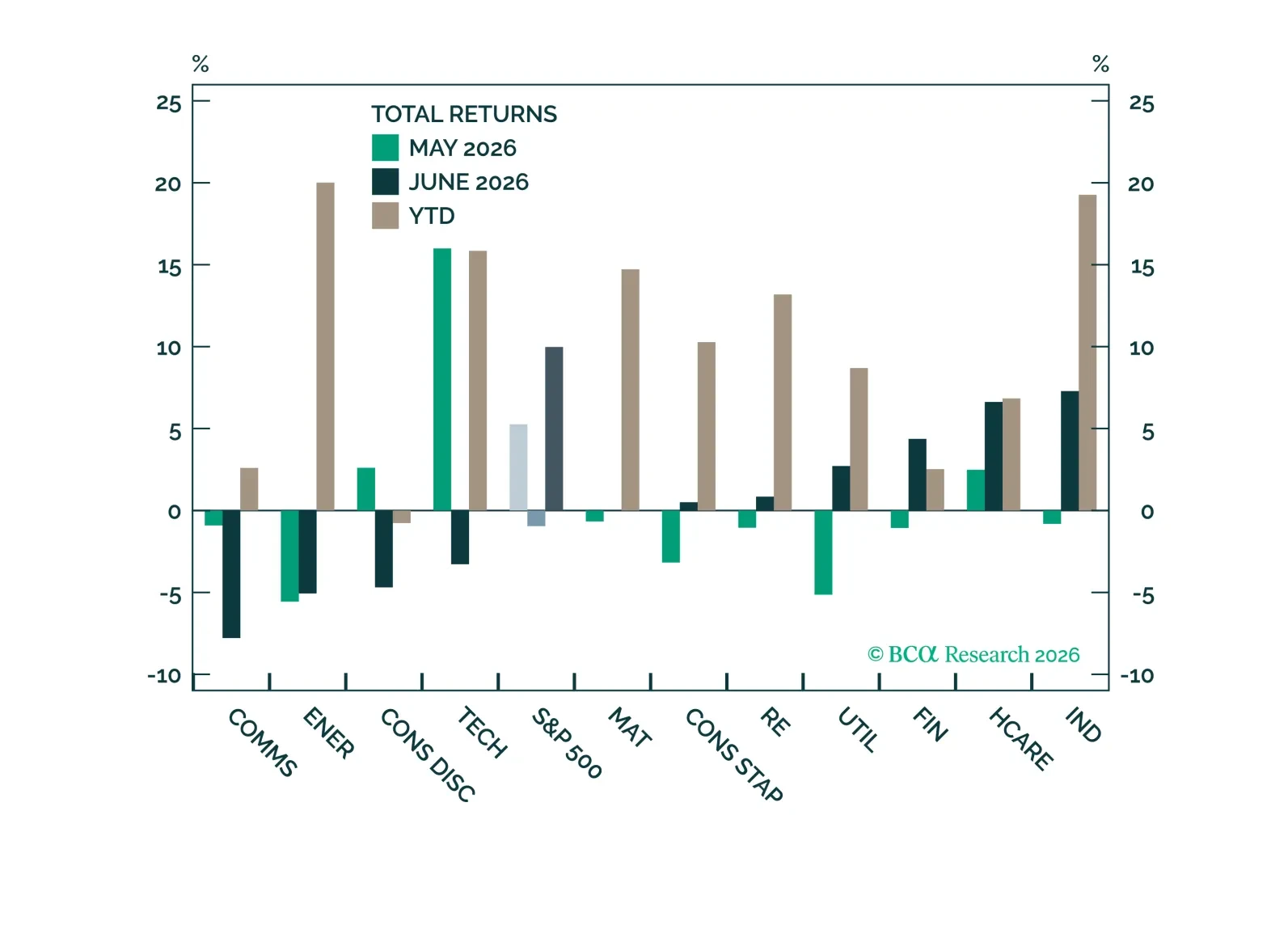

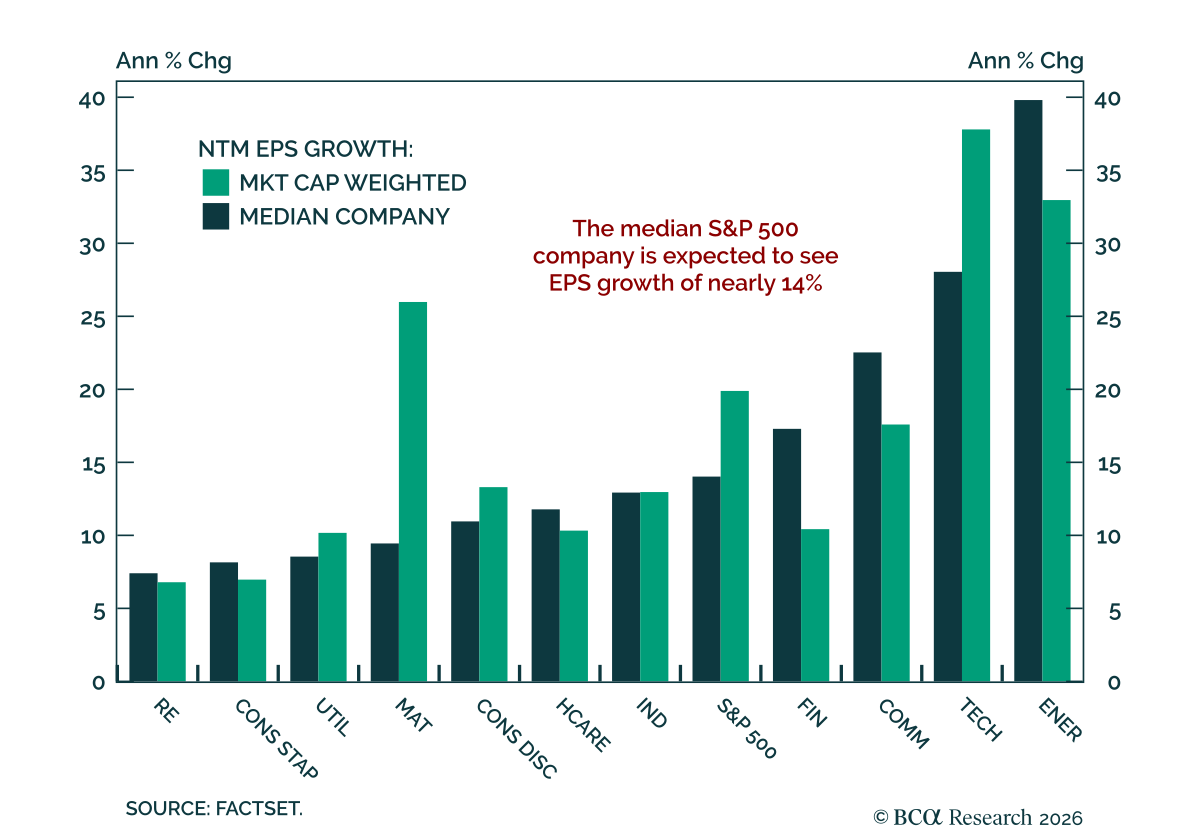

S&P 500 performance rotated in June, but fundamental growth remains strong across sectors, with earnings and revenue growth extending well beyond the largest mega-cap companies.

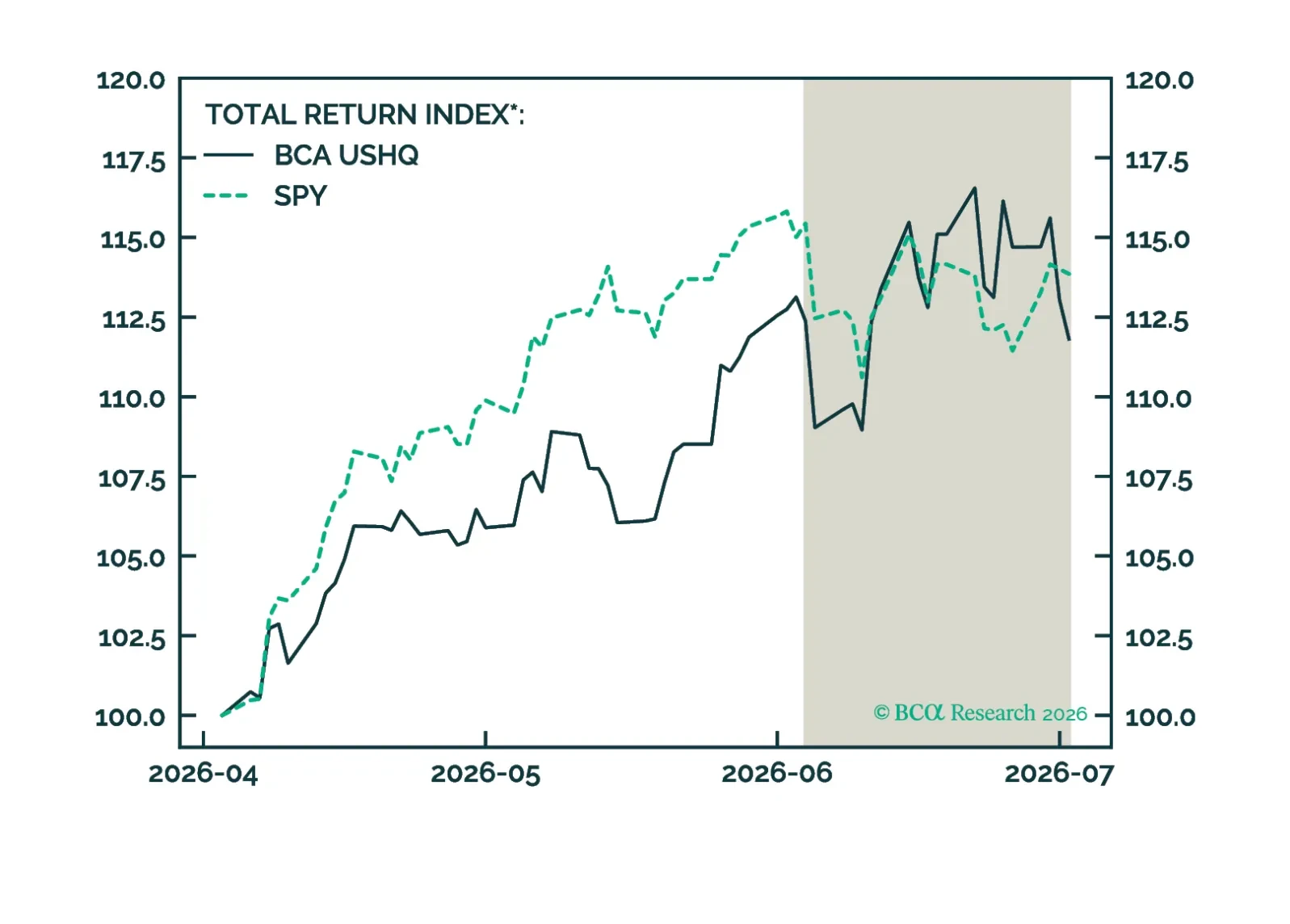

The US High Quality (USHQ) portfolio outperformed its benchmark through June, returning -0.50%, while its SPY benchmark returned -1.37%. On a trailing three-month basis, the USHQ portfolio’s performance was weaker than the benchmark, with USHQ underperforming by approx. 205bps.

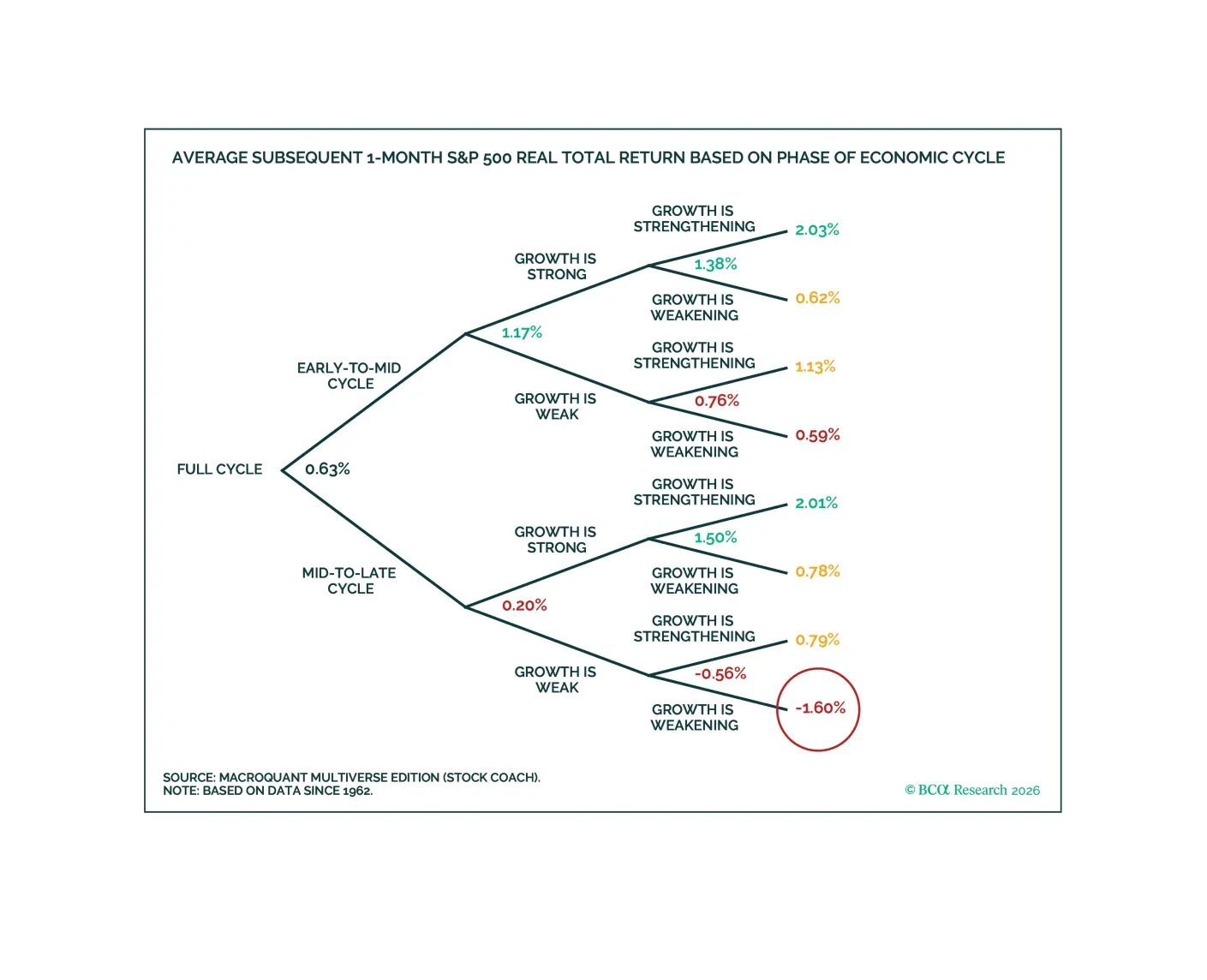

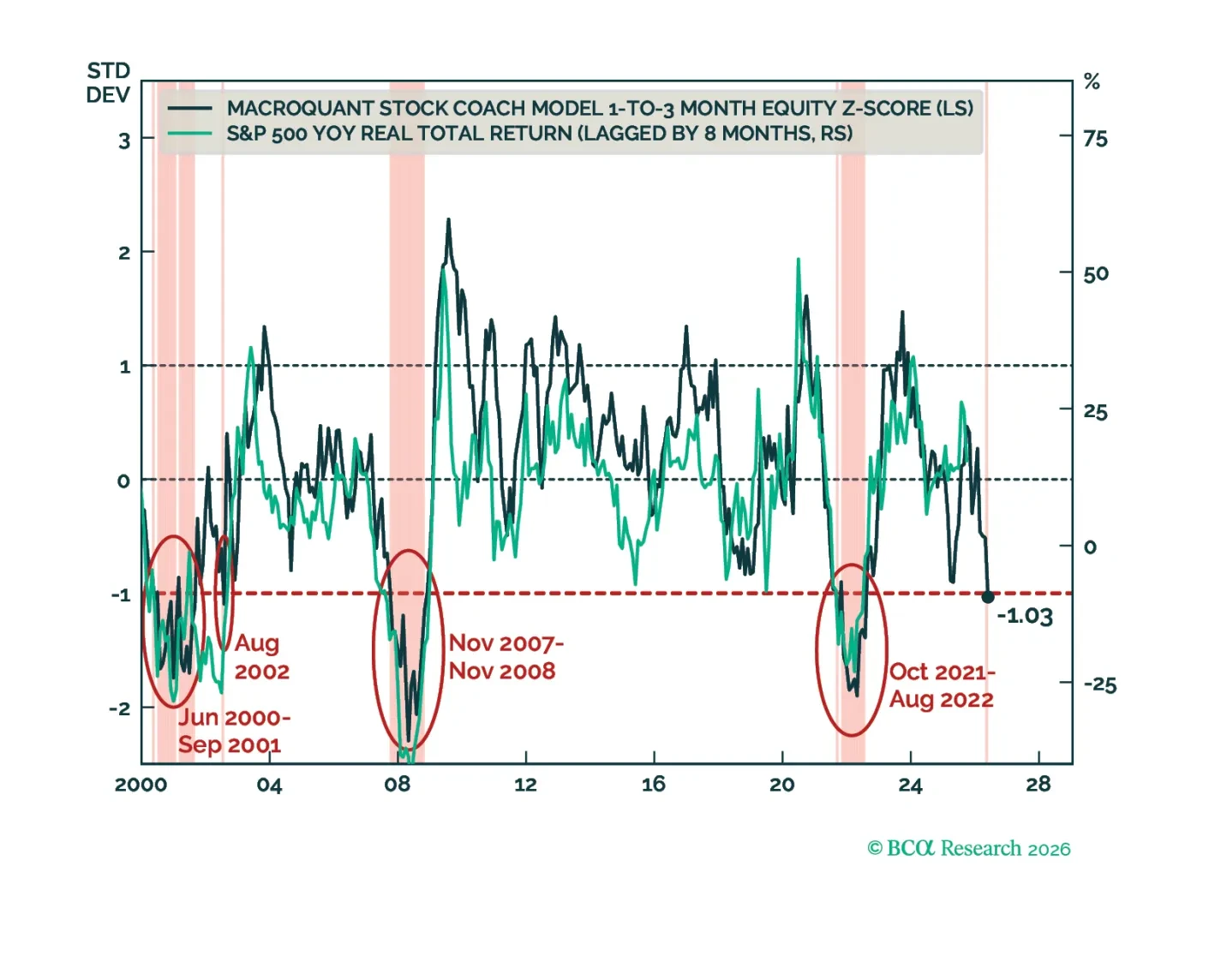

MacroQuant recommends underweighting equities and adopting a benchmark duration stance in fixed-income portfolios. The model is very positive on the US dollar, bearish on gold, neutral on copper, and bullish on oil.

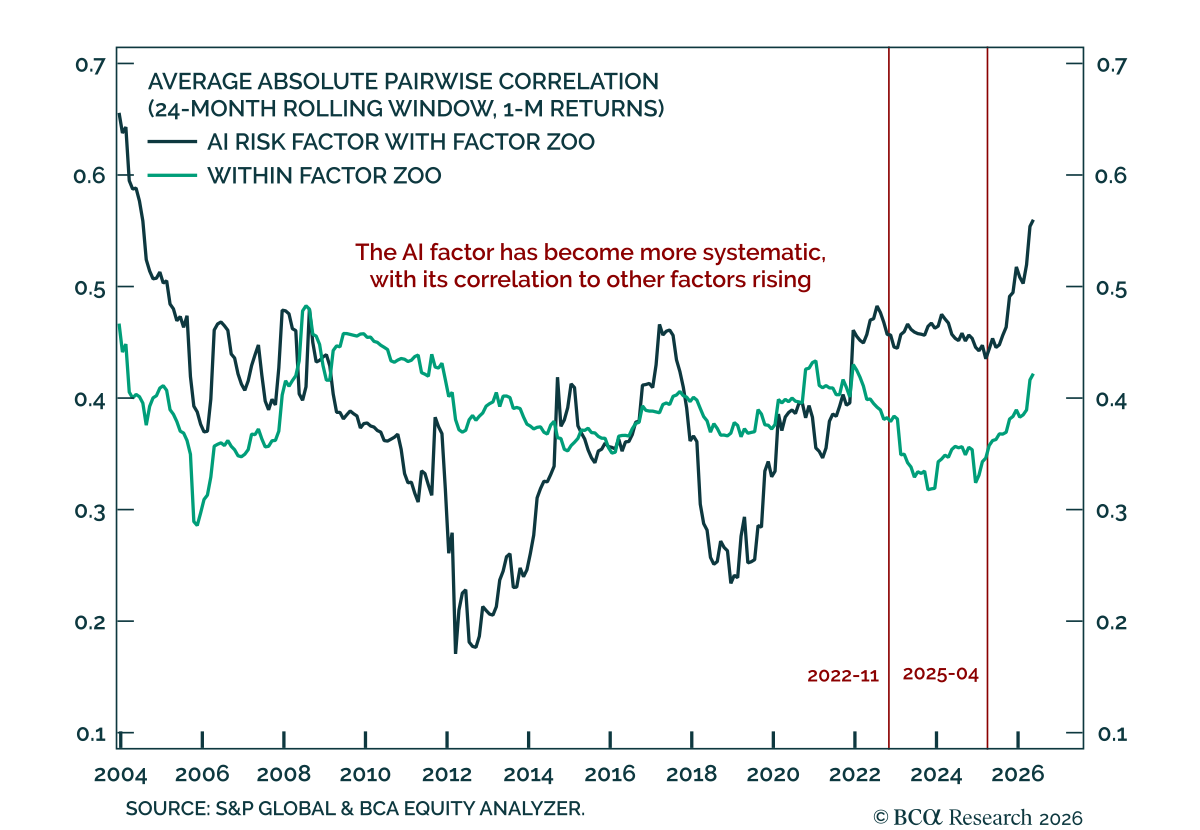

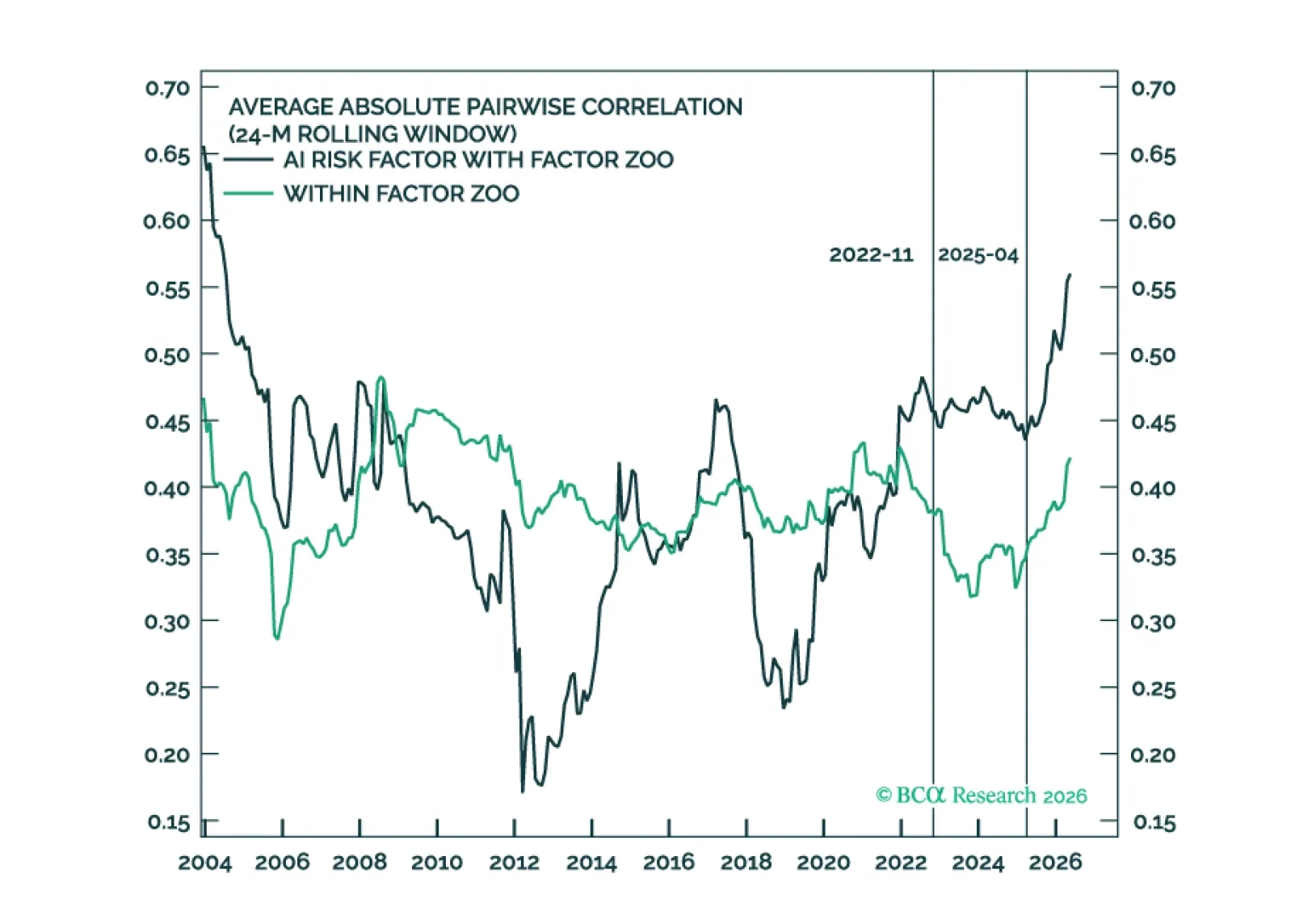

The S&P 500 has become increasingly concentrated. We know that. But the critical question is not how many stocks are driving the market; it is how many factors are driving stocks. We define an AI risk factor to test whether AI has become the dominant common exposure throughout much of the factor zoo.

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

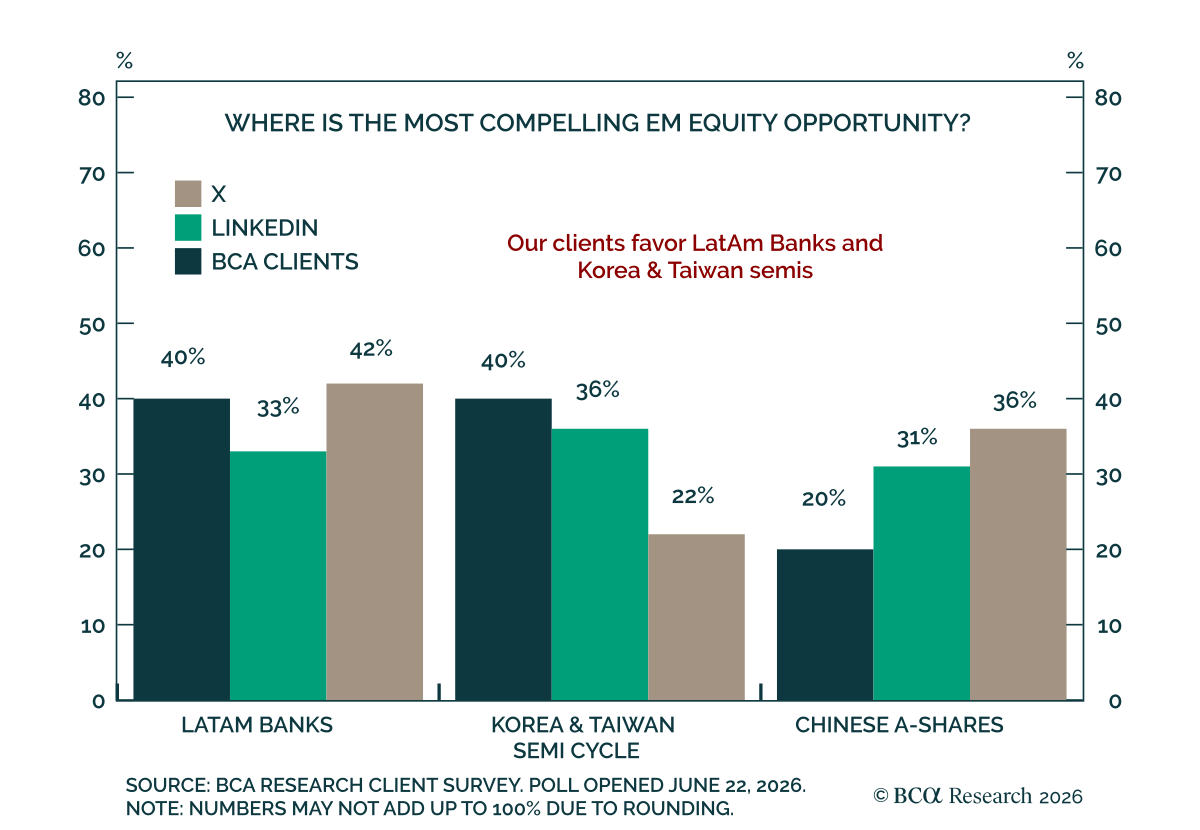

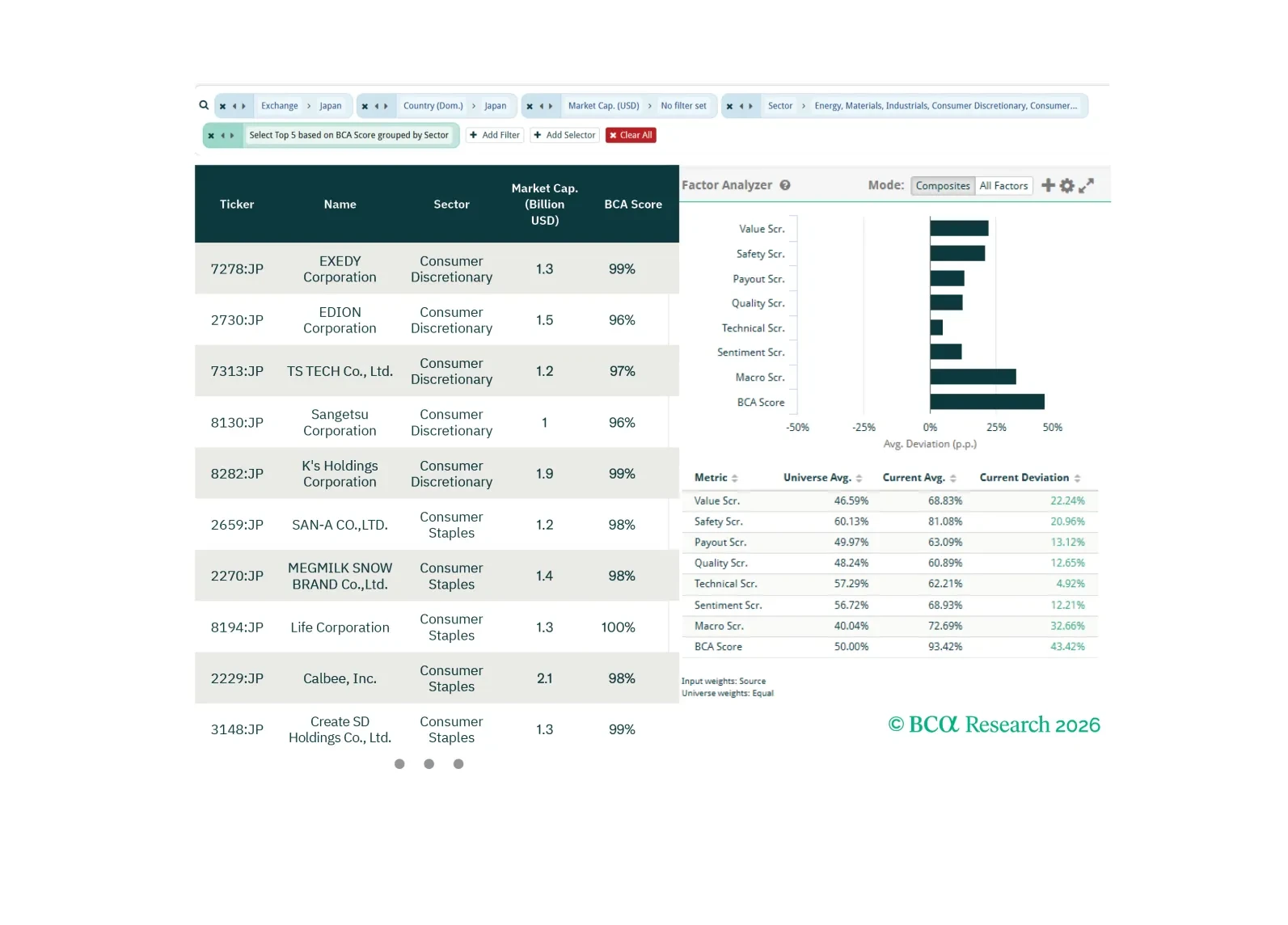

In this screener report, we explore opportunities in Japanese Non-TMT equities, El Niño hedges, and US consumer-facing equities.