Emerging Markets

The attacks on Red Sea commercial tankers by Iran’s Yemeni proxies, the Houthi movement, are an inflation risk inasmuch as they lengthen voyage times for any shipping forced to avoid the Bab el-Mandeb Strait. The risk of an expansion of these attacks is, in our view, limited, given Iran’s inability to project naval power in the region.

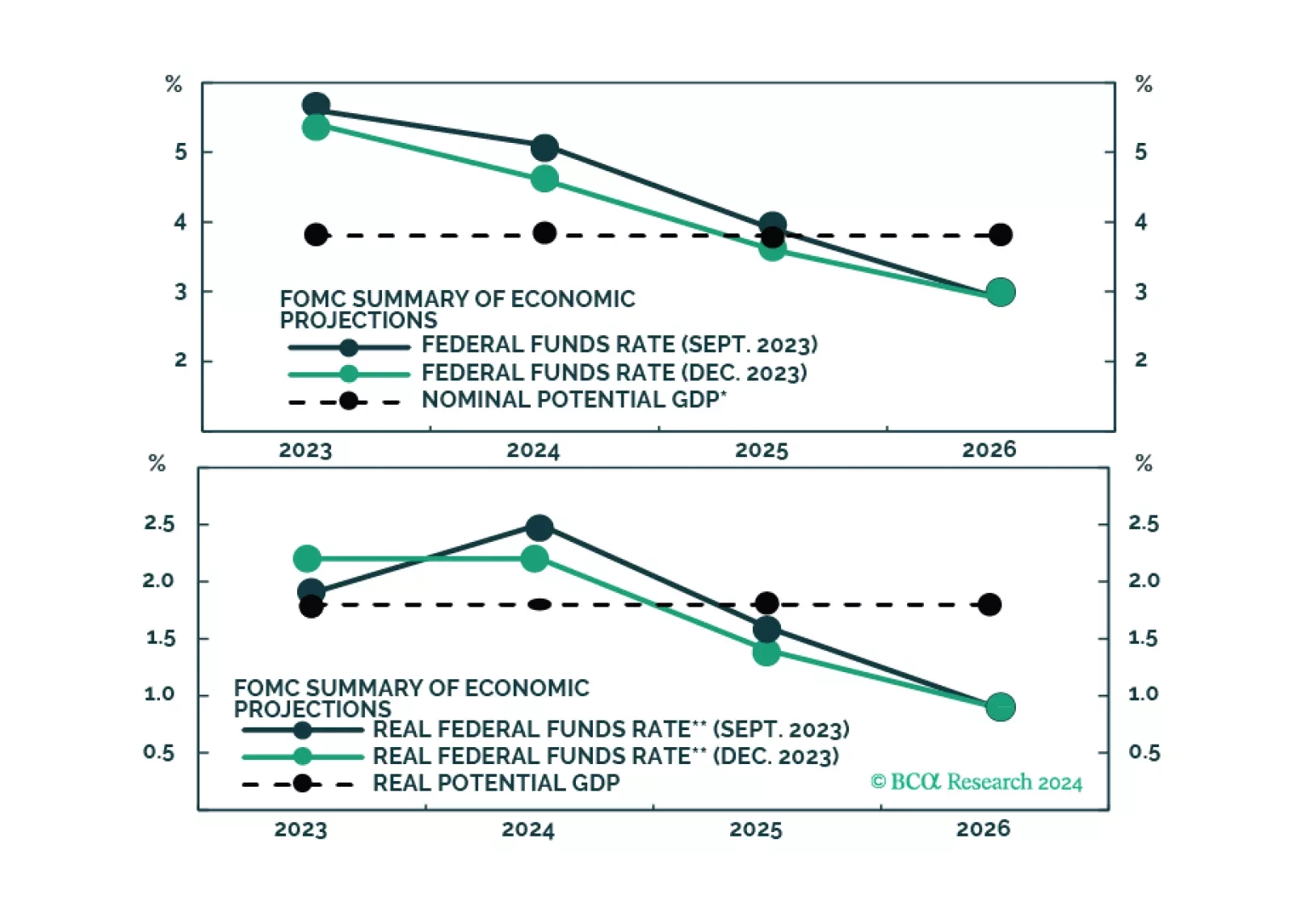

The market is excited by the idea that the Fed will cut rates early this year, even without a recession. But is that likely, with inflation still set to be around 2.8% mid-year?

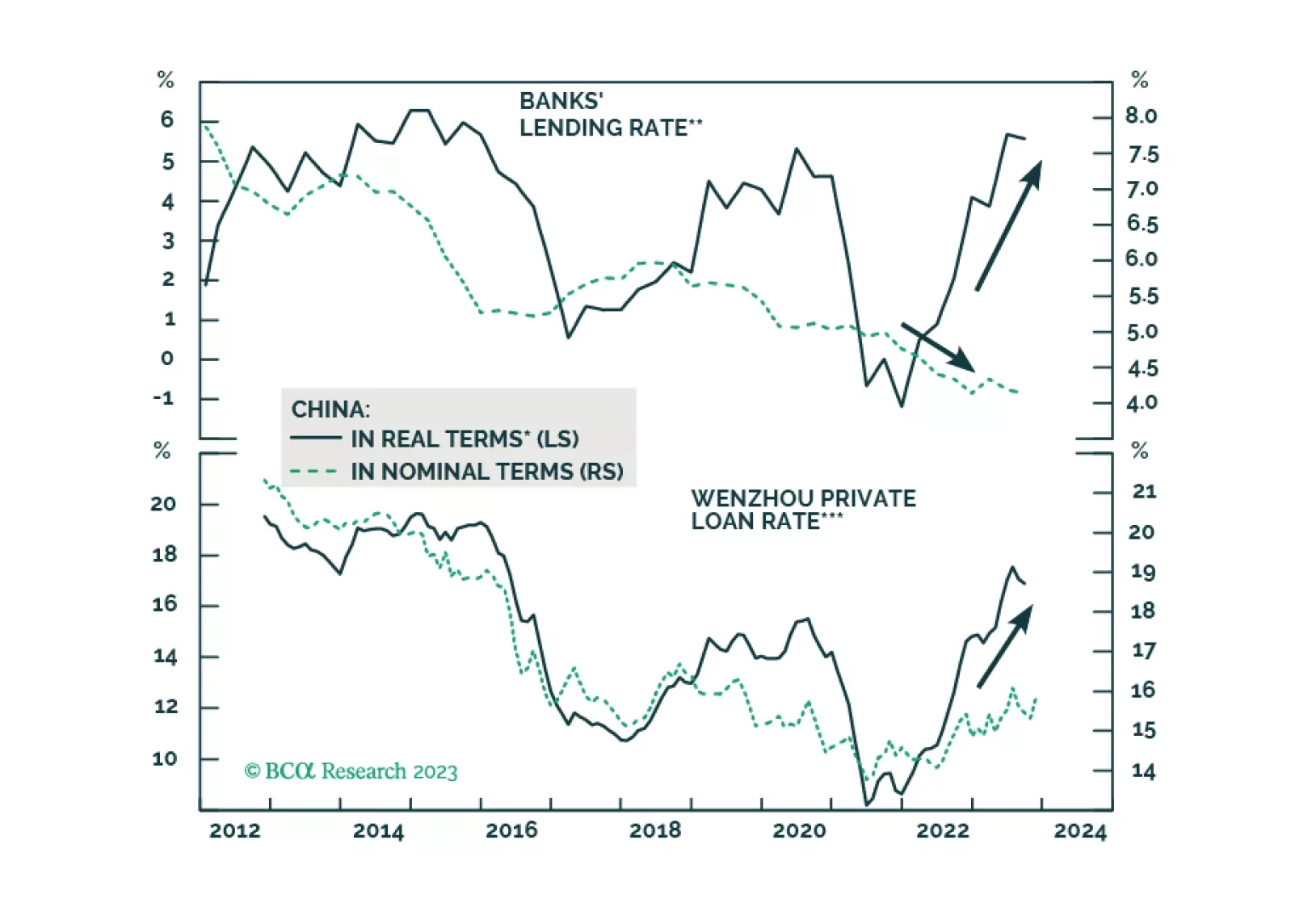

The statement from last week’s Central Economic Work Conference indicates that Chinese authorities are still not considering large-scale stimulus in 2024. Odds are that a full-fledged business cycle recovery in 2024 is unlikely. Chinese share prices remain vulnerable, and strengthening in the RMB will be short-lived.

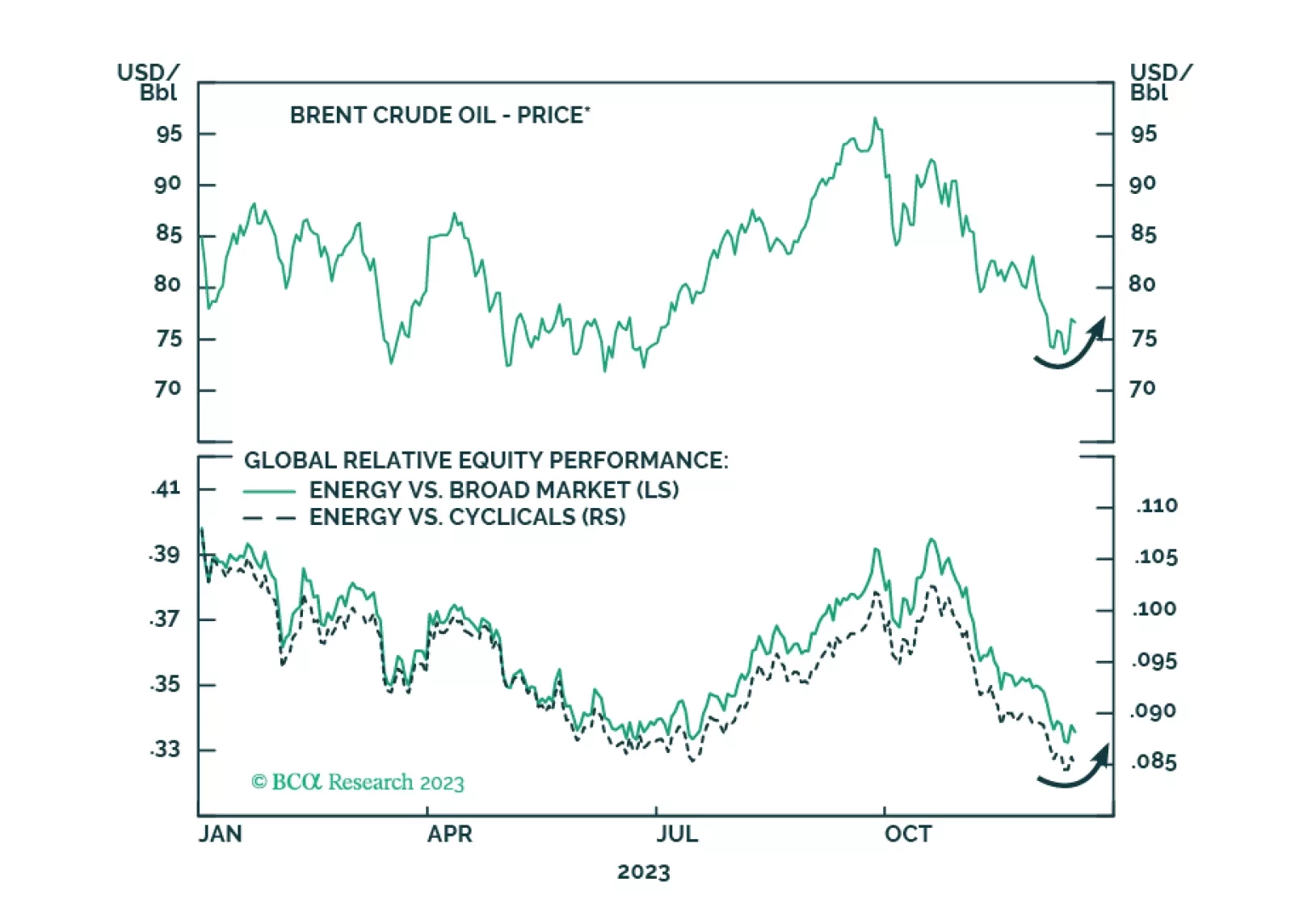

Oil prices will rise tactically due to supply risks. Recent developments indicate escalation of the conflict with Iran in the Middle East and confirm our expectation of energy supply disruptions and oil price spikes in the short run.

Explore the eight main themes that will drive the returns of European assets in 2024.

The major question facing EM investors in 2024 is whether or not EM will cross the Rubicon. The path to a soft landing in the US remains elusive. The recent improvement in global manufacturing/trade will likely prove to be a mid-cycle bounce rather than the beginning of a cyclical recovery.

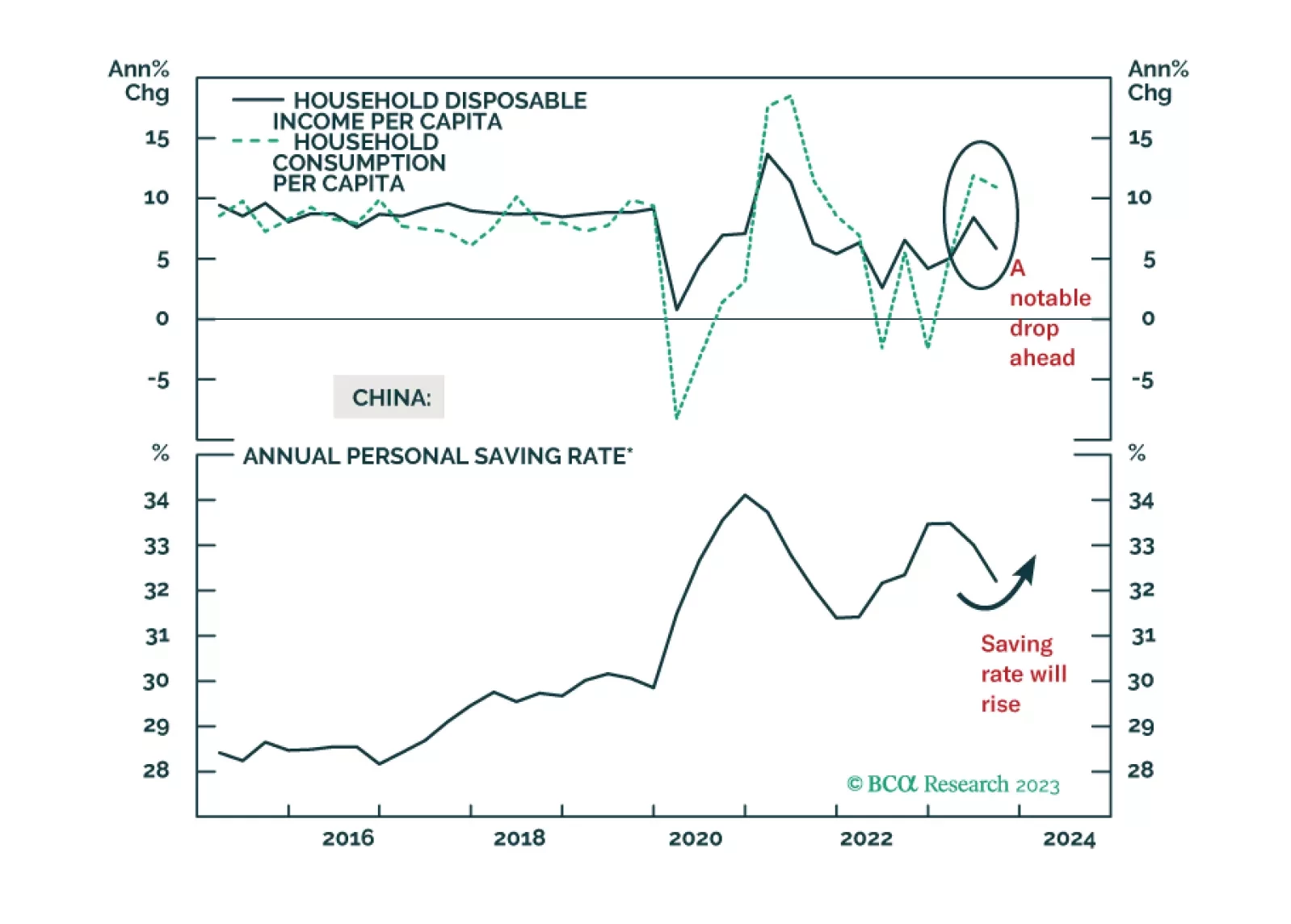

Nominal household spending growth in China will slow in 2024. Strong headwinds will arise from a slower household income expansion, falling house prices, a downbeat employment outlook, and shrinking exports. Spending on healthcare services will post solid gains but durable goods consumption will experience anemic growth in 2024. We favor consumer staples and healthcare stocks versus the domestic benchmark.

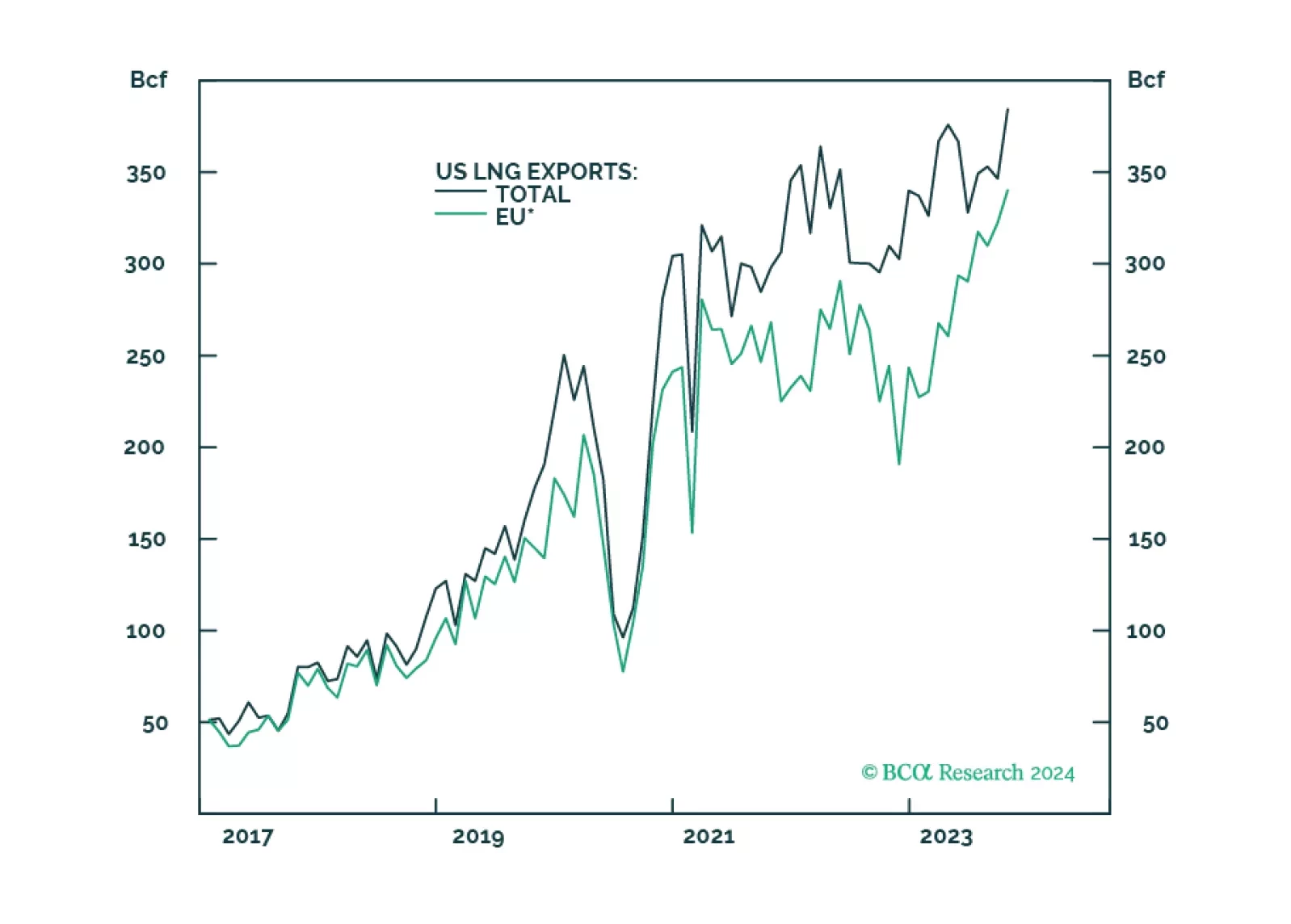

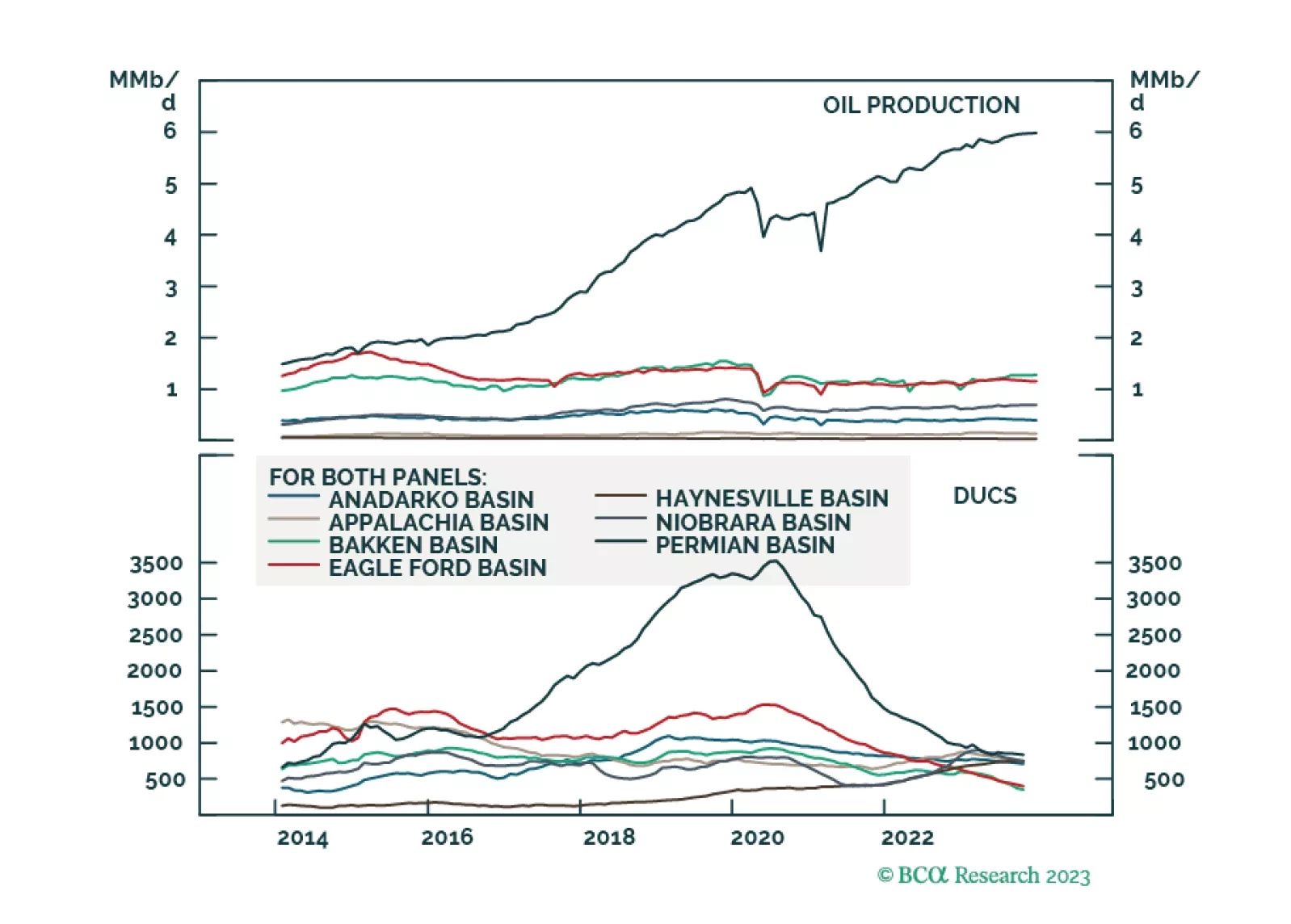

Political economy dominates fundamentals going into 2024, as states prepare for war and de-risk supply chains. Asynchronous global growth will elevate commodity-price volatility. We expect oil to trade above $100/bbl in 2024 and continue to favor equity exposure to oil-and-gas producers. Given weak capex, we also favor metals miners and refiners. We remain long the Gold, the XME and COMT ETFs We were stopped out of our XOP ETF with a 12.5% gain; we will re-establish it at tonight’s close.