Economic Growth

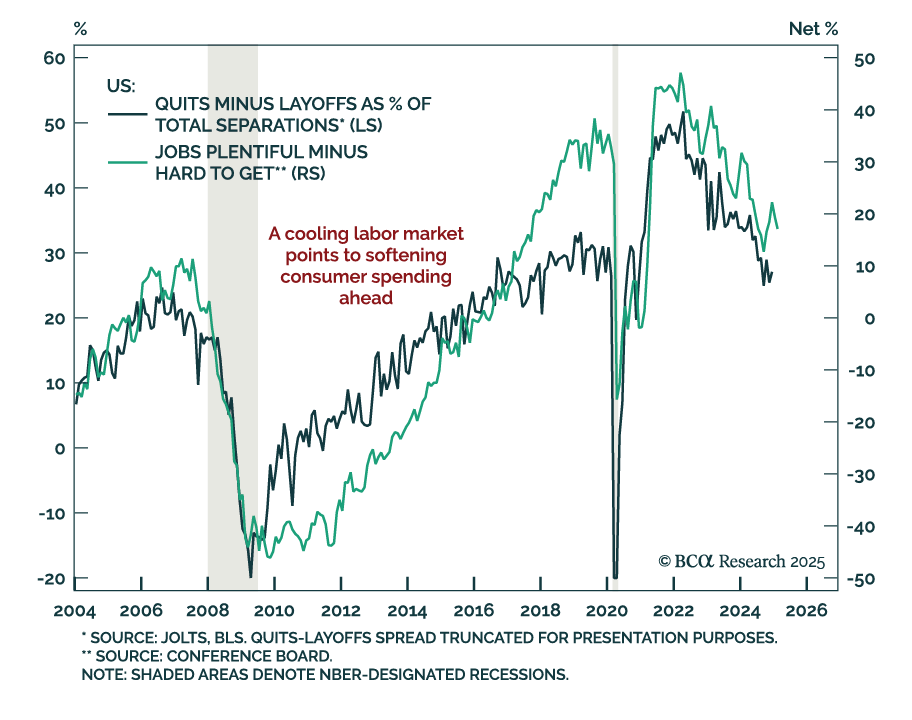

The February Conference Board Consumer Confidence index missed estimates for the third month in a row, falling to 98.3 from 105.3. Consumers’ assessment of both their current situation and their expectations worsened, with the latter falling close to 10…

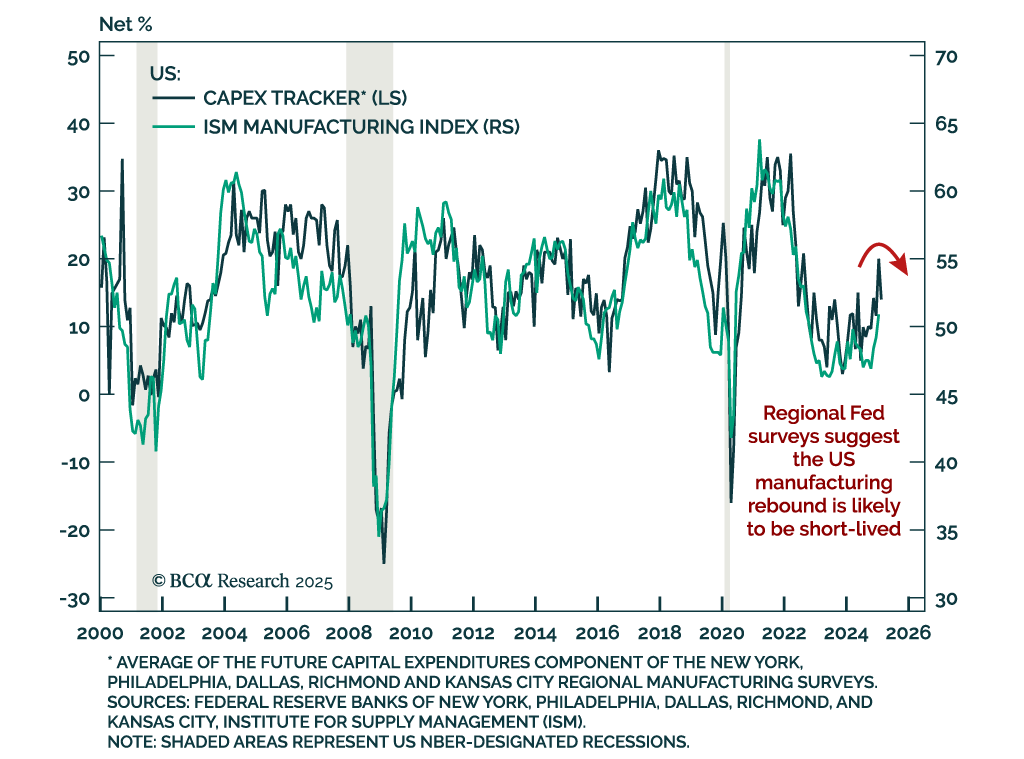

The February Dallas Fed Manufacturing index missed estimates, contracting at -8.3 vs. expanding at 14.1 in January. The underlying details of the report were quite poor, with current and future measures of activity broadly ticking down after increasing since…

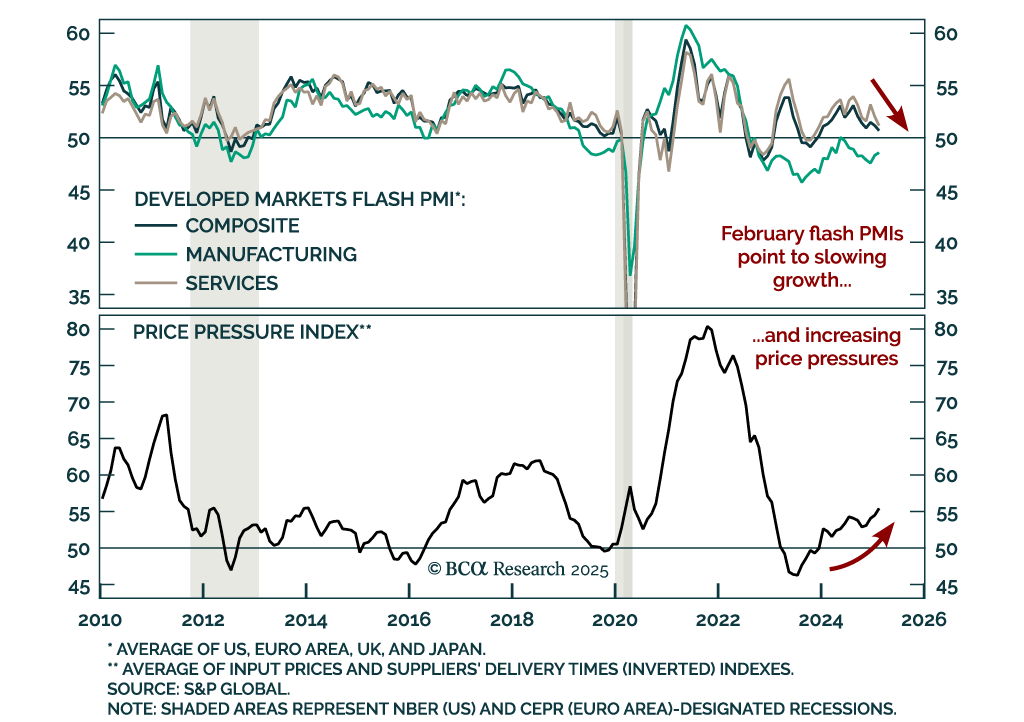

February’s flash PMIs for the major developed markets showed softening growth, and rising price pressures. The US composite index missed estimates and decreased to 50.4 from 52.7 in January. Services were a big contributor to the decline, with the index…

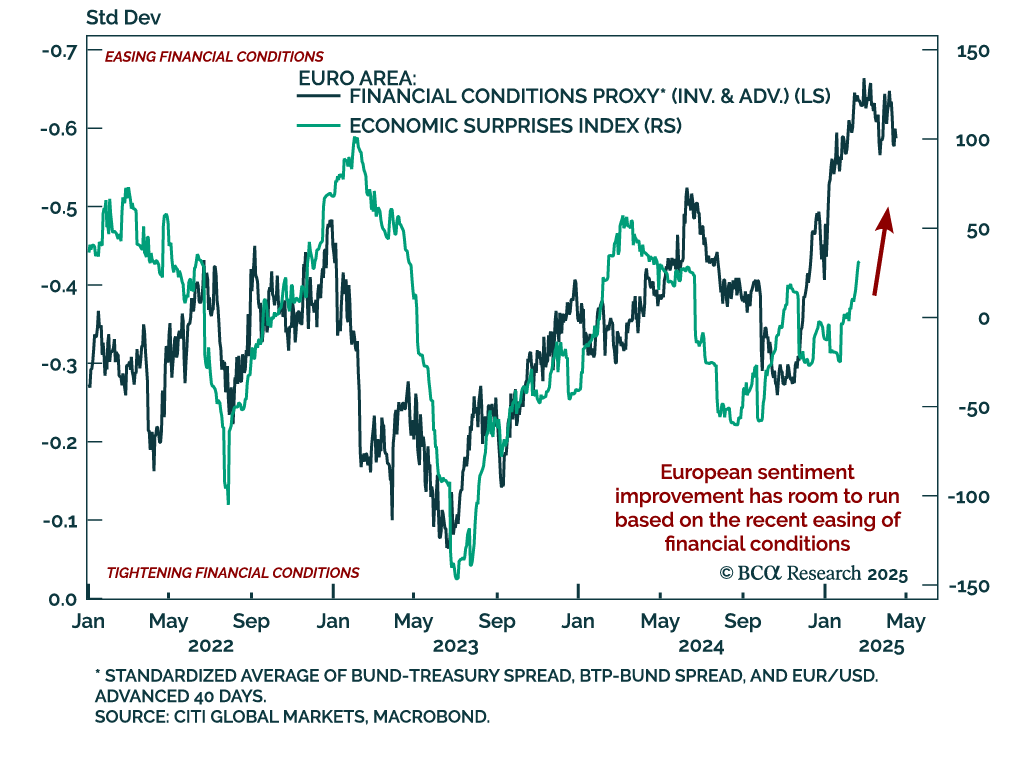

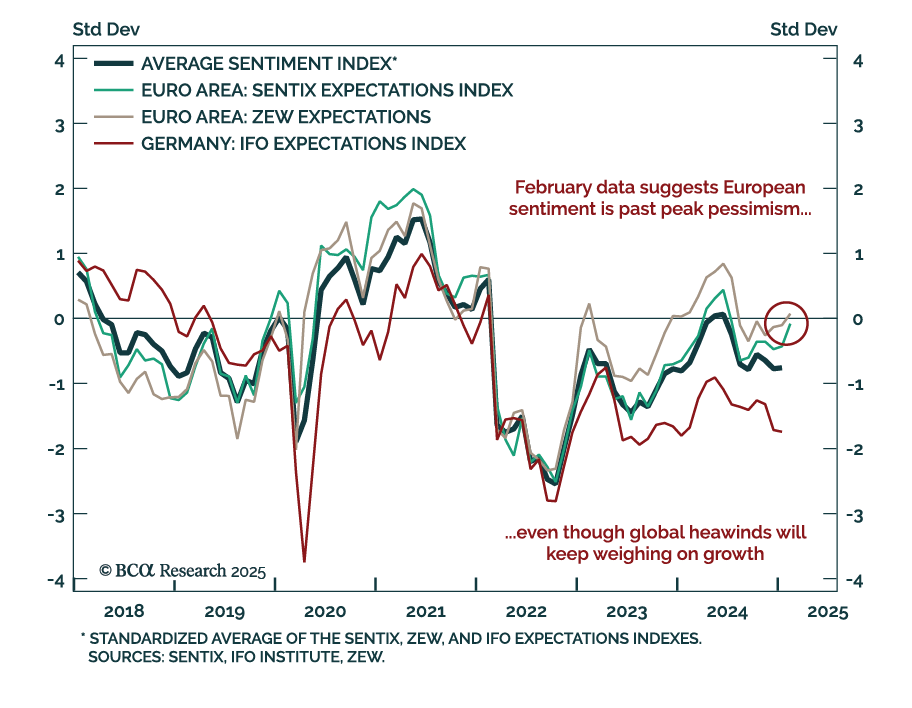

A nascent theme in the latest data is the broad improvement in European sentiment. The February Sentix and ZEW surveys both improved, and flash estimates for European consumer confidence beat estimates, ticking up to -13.6%. Confidence remains low, but…

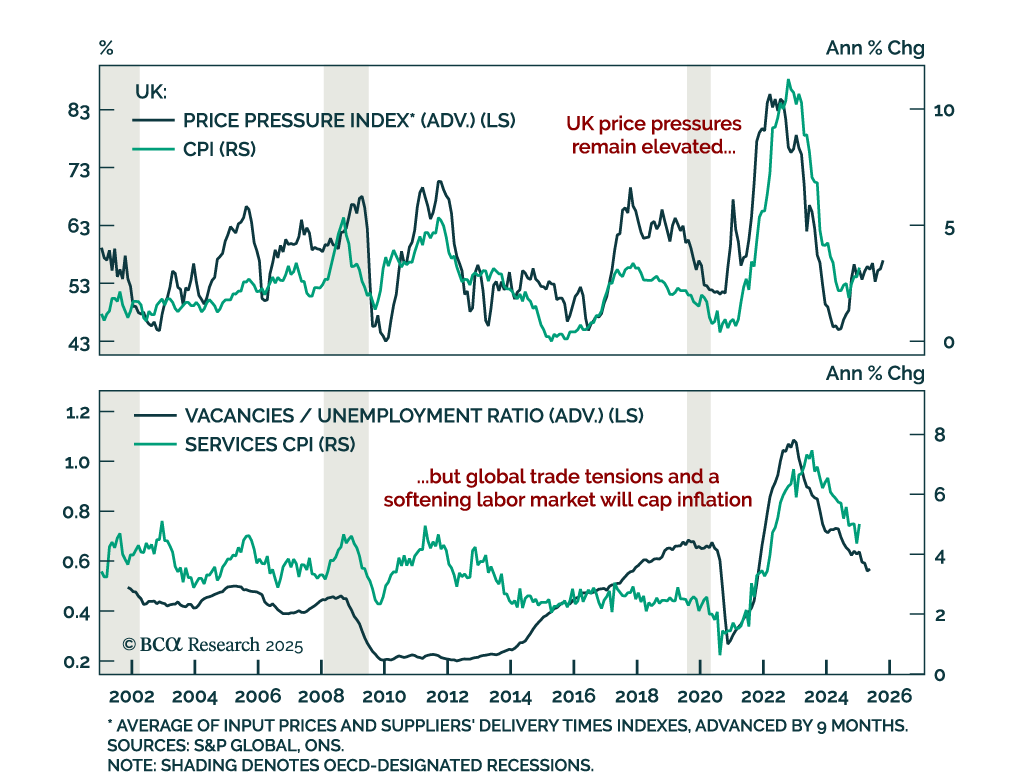

The January UK CPI was slightly hotter than expected. Headline inflation beat estimates, rising to 3.0% y/y from 2.5% in December. Core inflation also jumped but was in line with expectations at 3.7%. Services were strong, albeit slightly lower than expected…

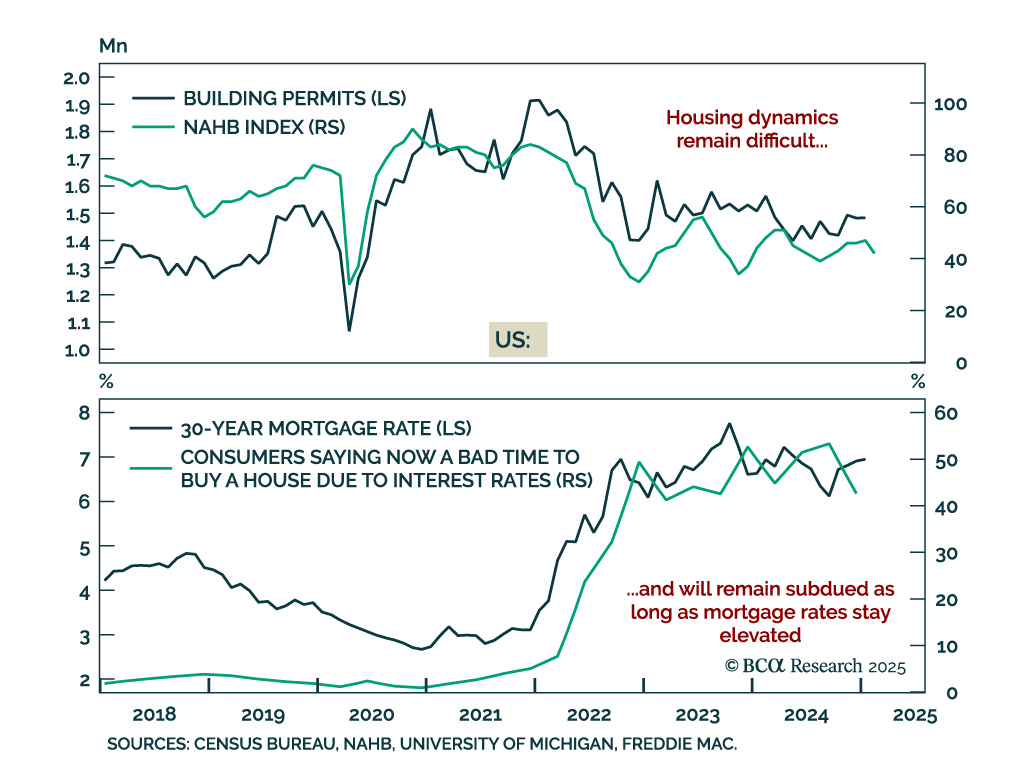

US January housing data disappointed, with housing starts falling 9.8% m/m after expanding 16.1% in December. The February NAHB Housing Market Index also weakened, falling to 42 from 47 in February. Building permits were the one positive surprise, growing…

The February ZEW index for Germany and the eurozone beat estimates, with the expectations component rising to 26.0 from 10.3 a month prior. The current situation assessment also improved, although it remains deeply negative at -88.5. The improvement…

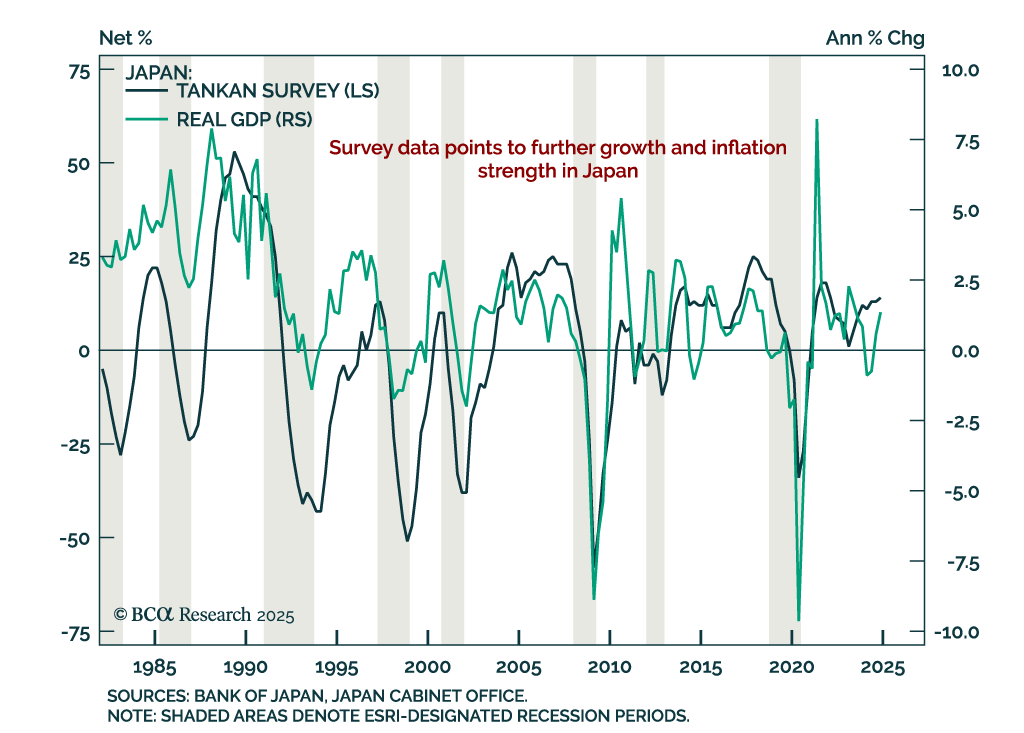

Preliminary estimates of Q4 real GDP growth in Japan was stronger than expected, rising to 2.8% q/q annualized from 1.7% in Q3. Domestic demand remained strong, and the GDP deflator increased to 2.8% y/y. Japan’s economy is running hot, sustaining price…

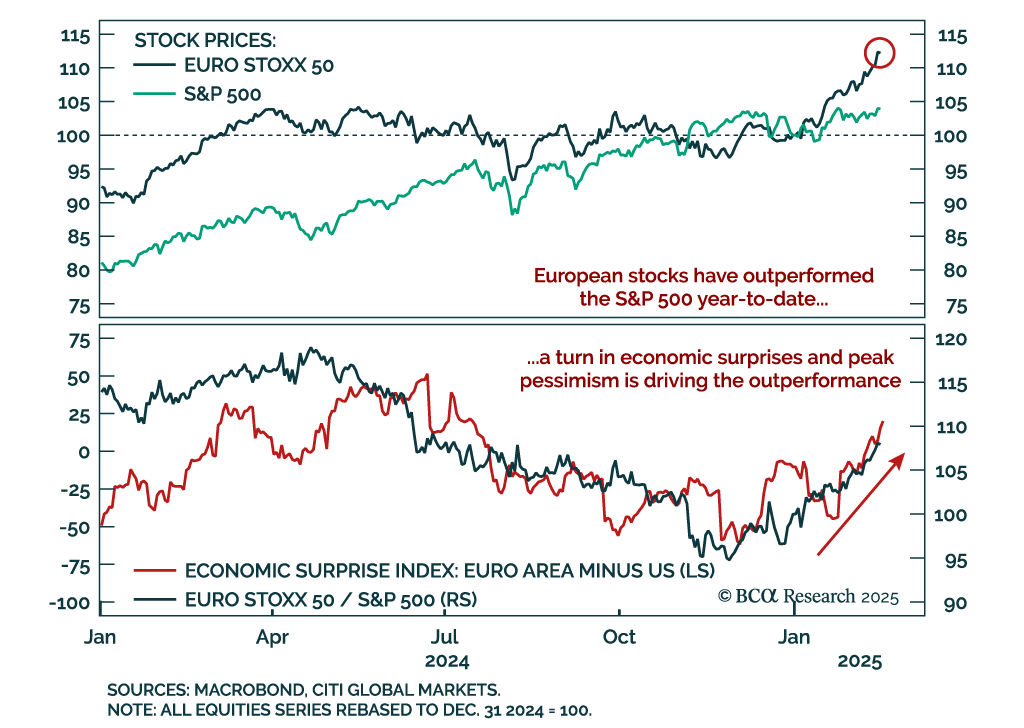

While the main Q1 2025 theme has been “America First”, the year-to-date market story has been more nuanced. “America First” would suggest an outperformance of US assets, but it is European assets that have started the year on a strong footing: The EURO STOXX…

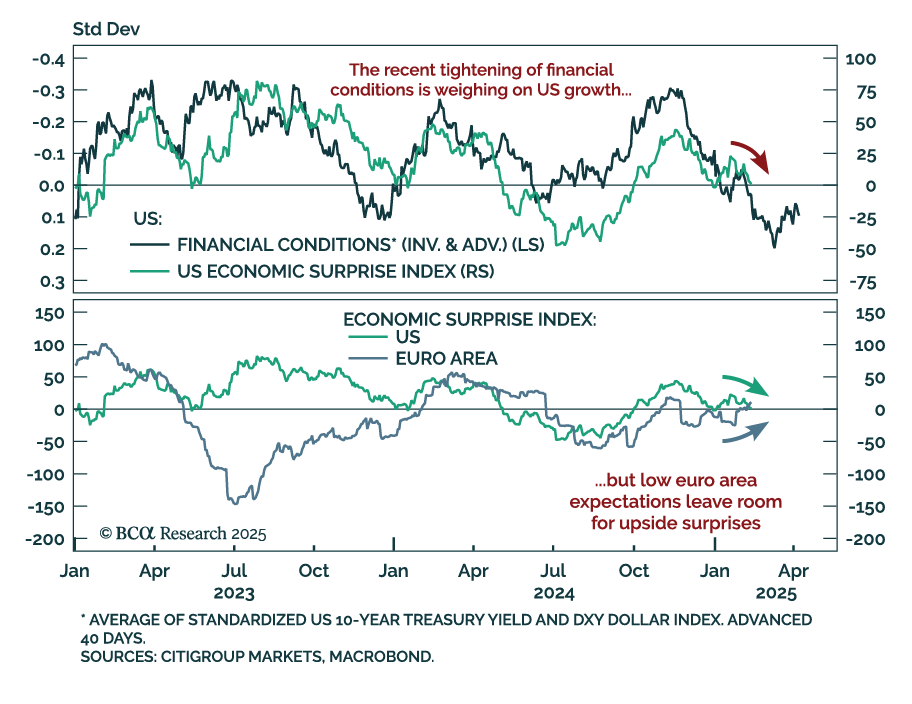

While geopolitics captured the latest headlines, Eurozone economic surprises have turned positive, while those in the US are on the verge of turning negative. Global economic surprises hinge on expectations and realized data, and they play a…