Debt Trends

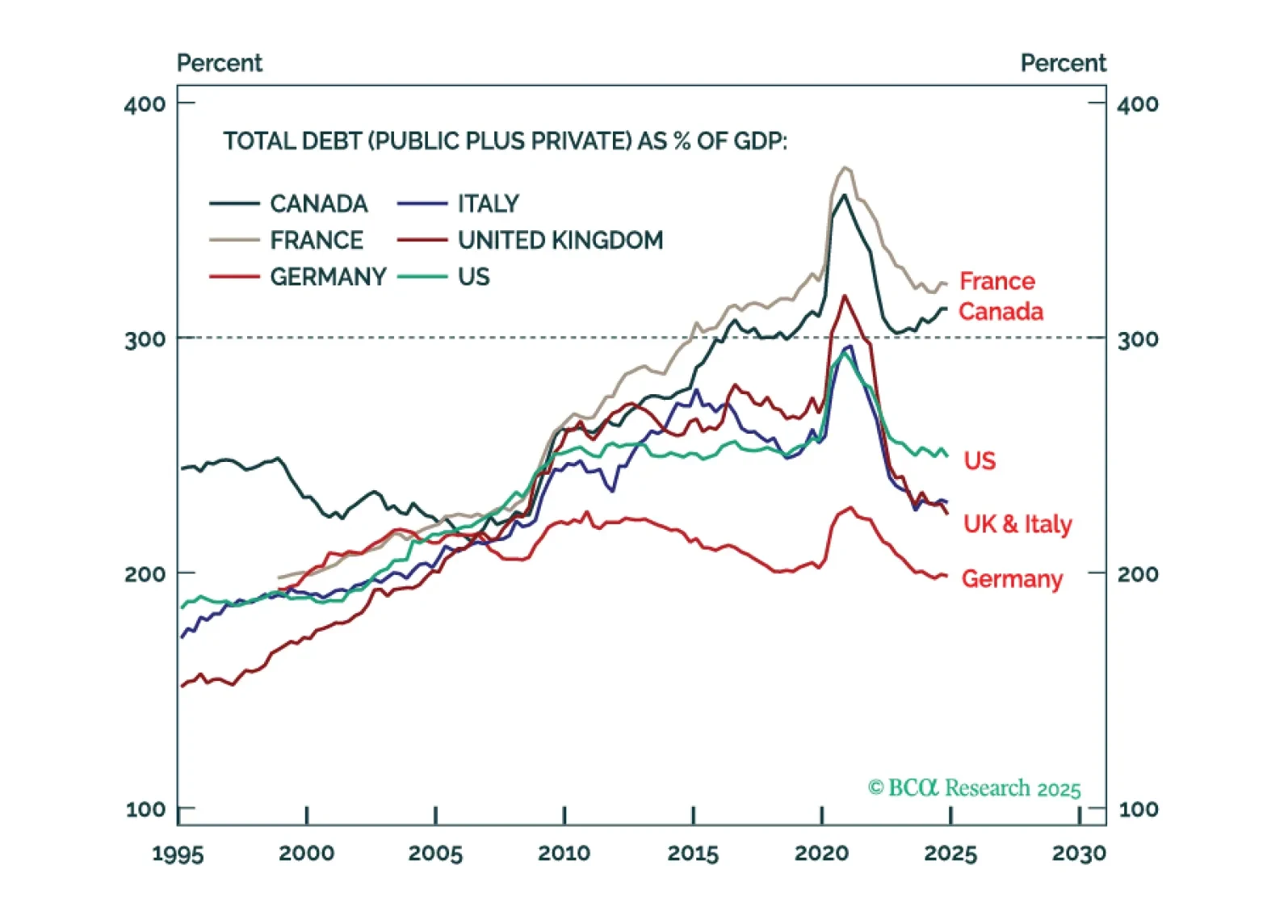

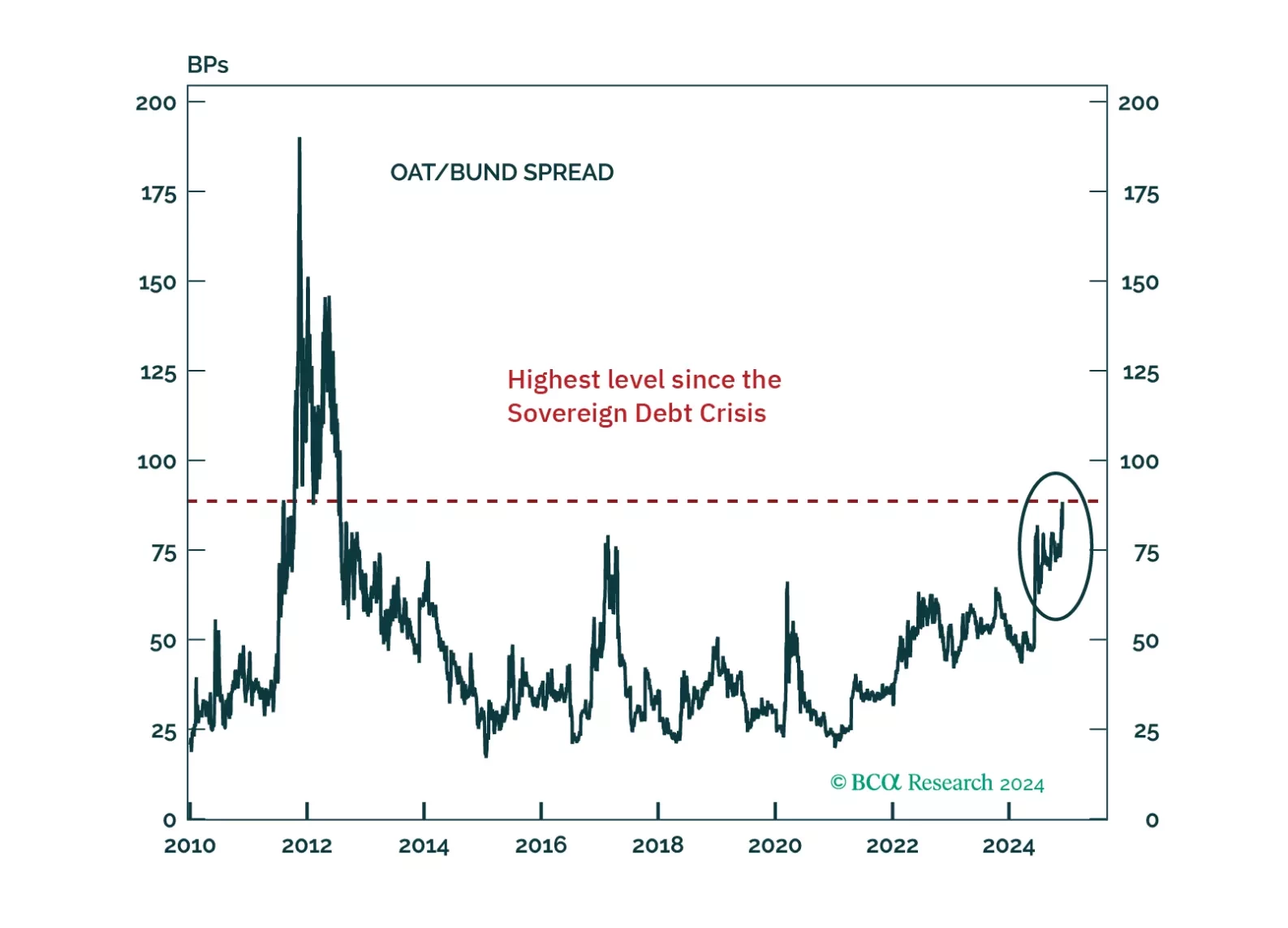

The bond vigilantes are circling over several targets right now: France, the UK, and Japan. But France is the most vulnerable because of a toxic combination: a total debt ratio well above 300 percent plus the worst primary deficit in the G7 plus political gridlock, which will get even worse if Prime Minister Francois Bayrou loses the September 8th vote of confidence in his minority government. We explain why the ECB cannot save France, and the investment implications. Plus, we unveil our brand-new complexity ‘heat map’ for global asset allocation which leads to a new tactical trade to underweight world communication services (WTEL).

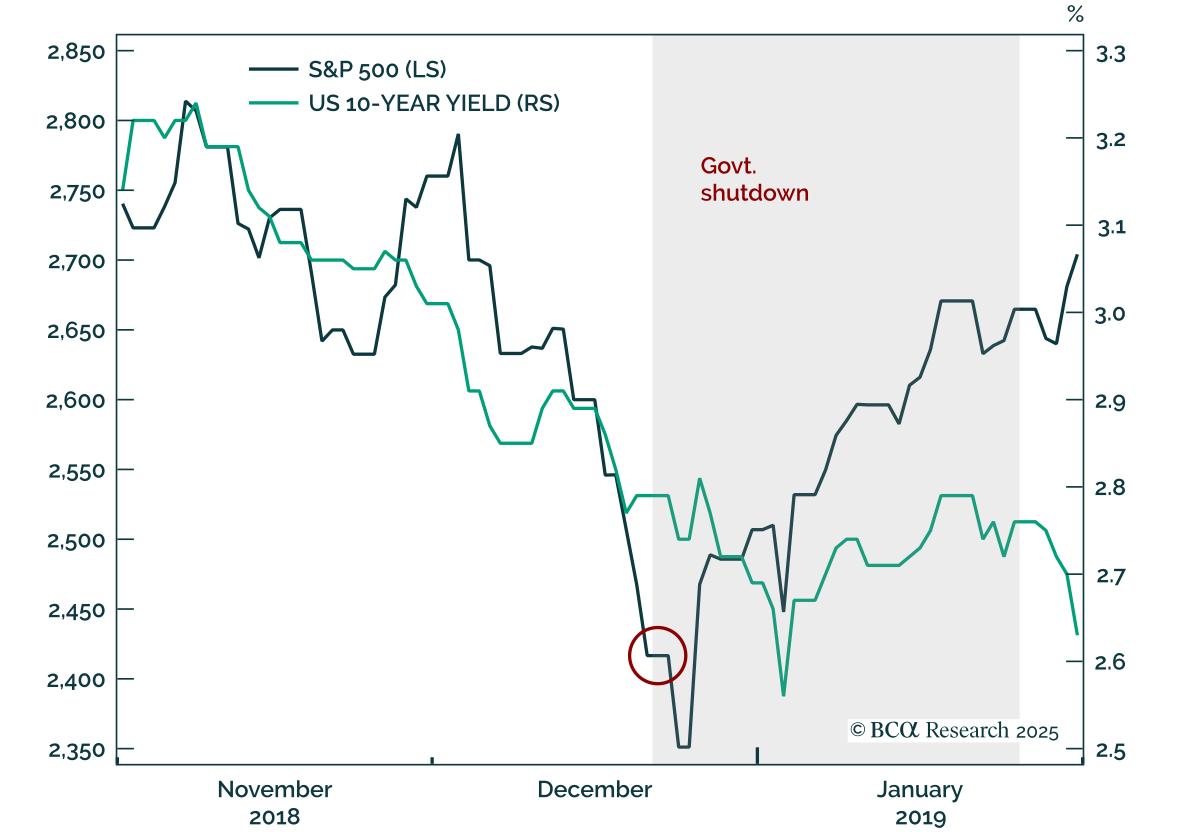

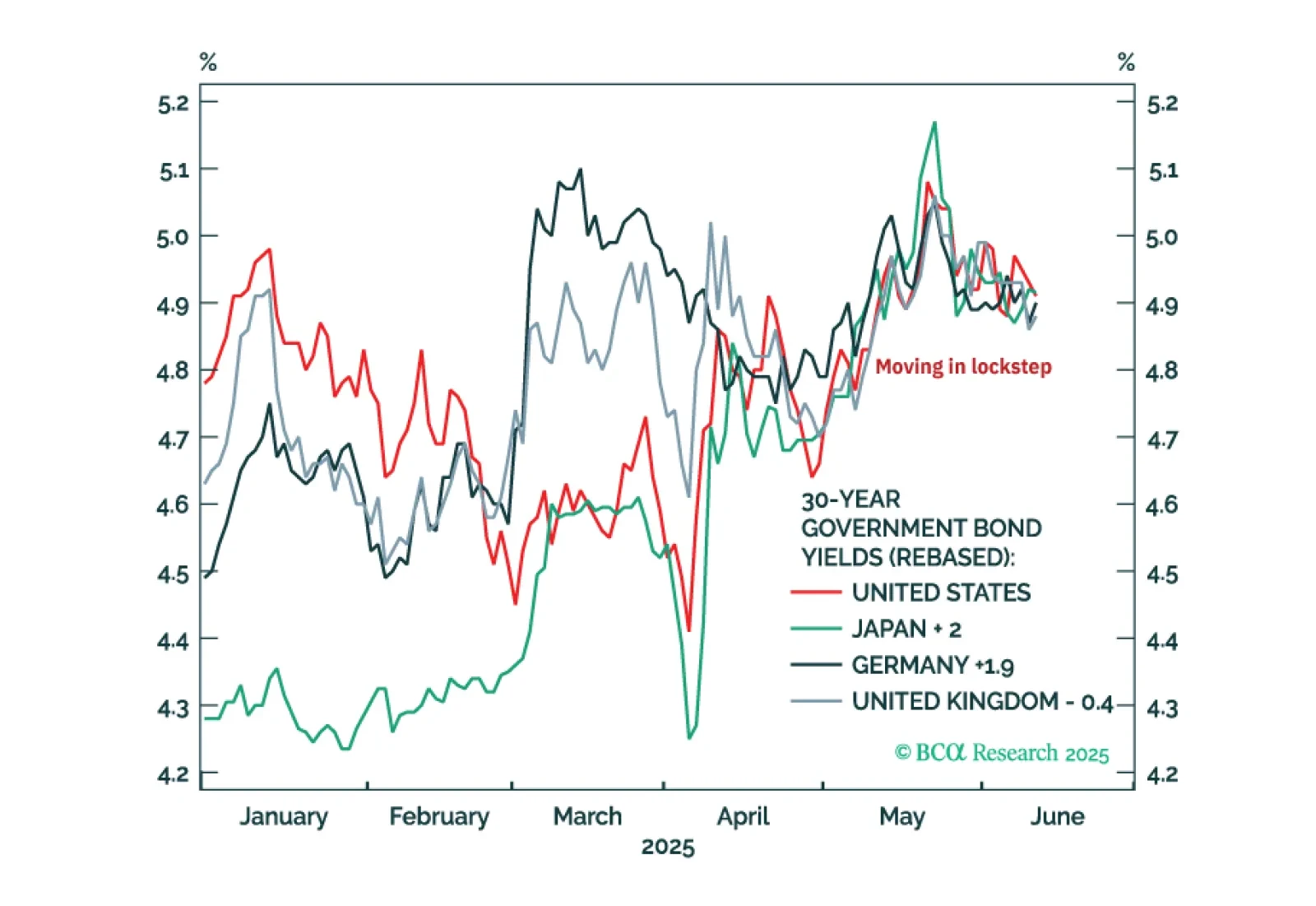

The perfectly synchronised moves in US, Japanese, German, and UK 30-year bond yields through the past two months are odd… and irrational. These irrational moves present compelling investment opportunities.

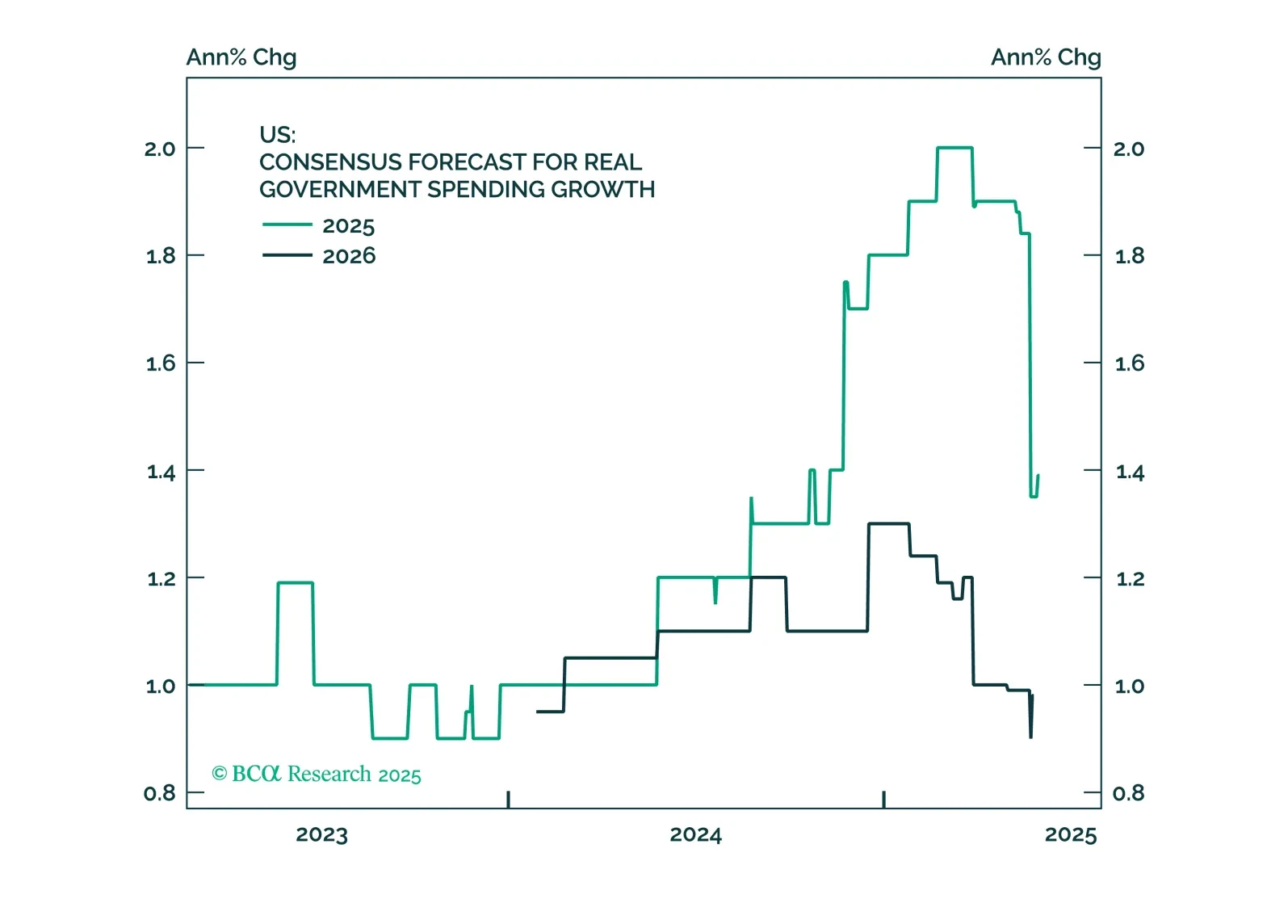

This month, we focus on the One Big Beautiful Bill Act (OBBBA). Our assessment in the Alpha report is that there won’t be any remaining alpha to harvest by shorting duration. The team that coined the “Human Steepener” moniker for President Trump is, effectively, throwing in the towel on looking for more upside to yields. There are many reasons for that view, but the main one is that the OBBBA legislation is just not that profligate, especially not relative to the investors’ expectations in the early days of the Trump 2.0 term.

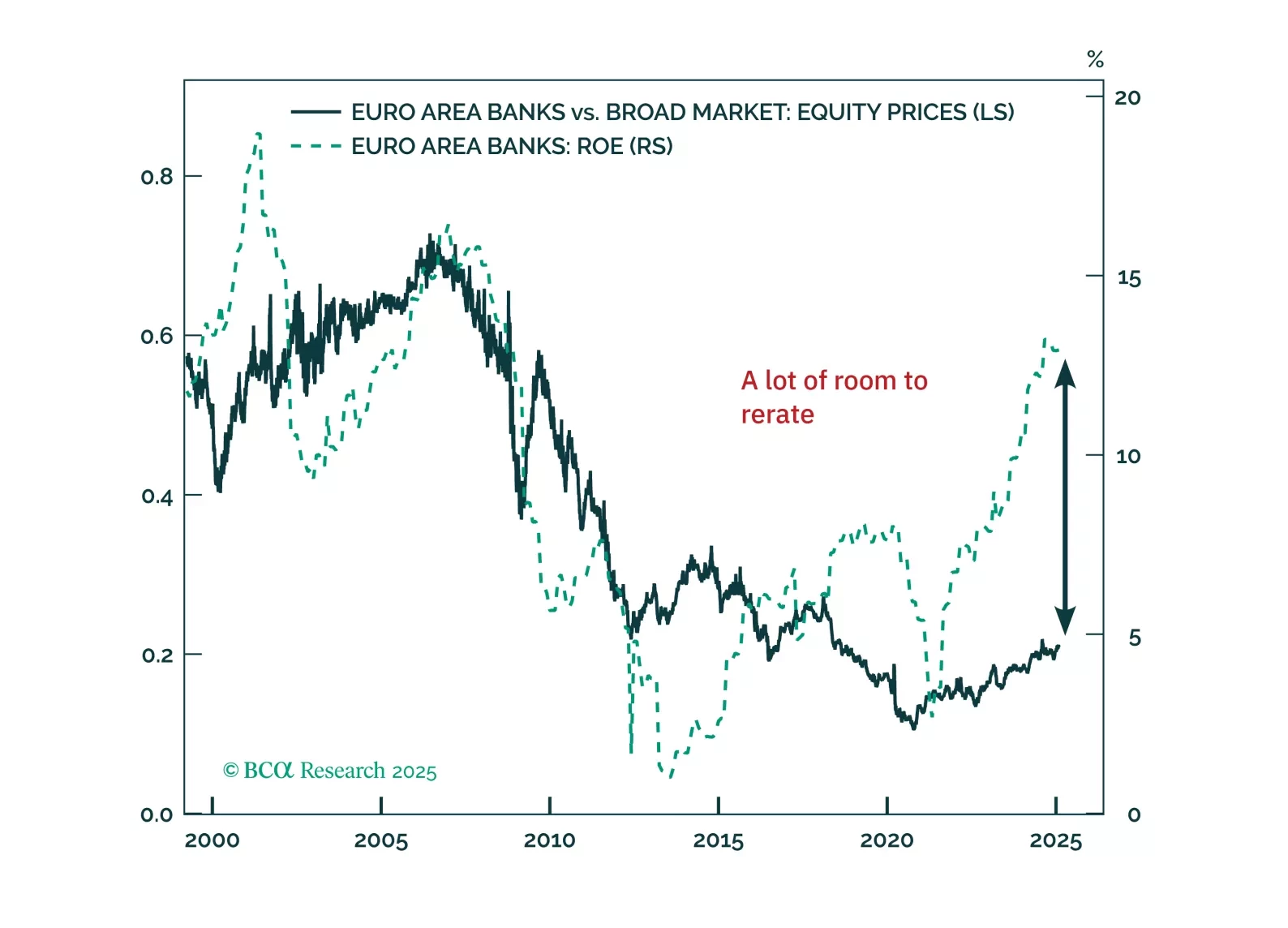

Eurozone banks have quietly outpaced the Magnificent 7—can they keep winning? With strong balance sheets, rising profitability, and structural tailwinds, European lenders still offer value despite short-term risks. Meanwhile, German equities continue to defy expectations, but is a near-term pullback on the horizon?

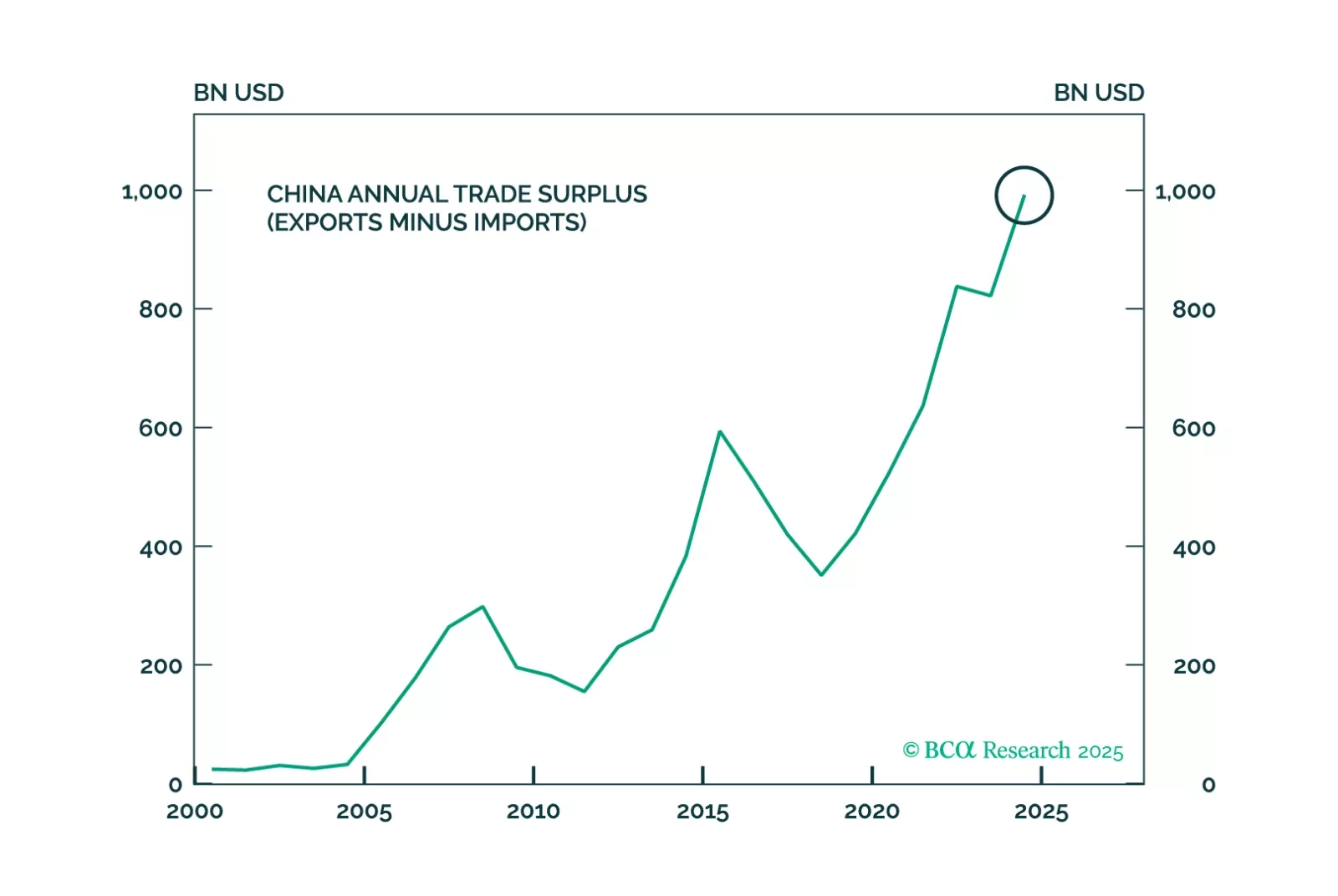

China barely hit its growth target in 2024 by shifting back to its old model of exports, racking up a record trade surplus with the world – right as Donald Trump walks back into the White House. Tariffs will elicit larger fiscal stimulus even as China rolls out innovations such as DeepSeek to meet its 2025 industrial goals, creating a volatile mix this year.

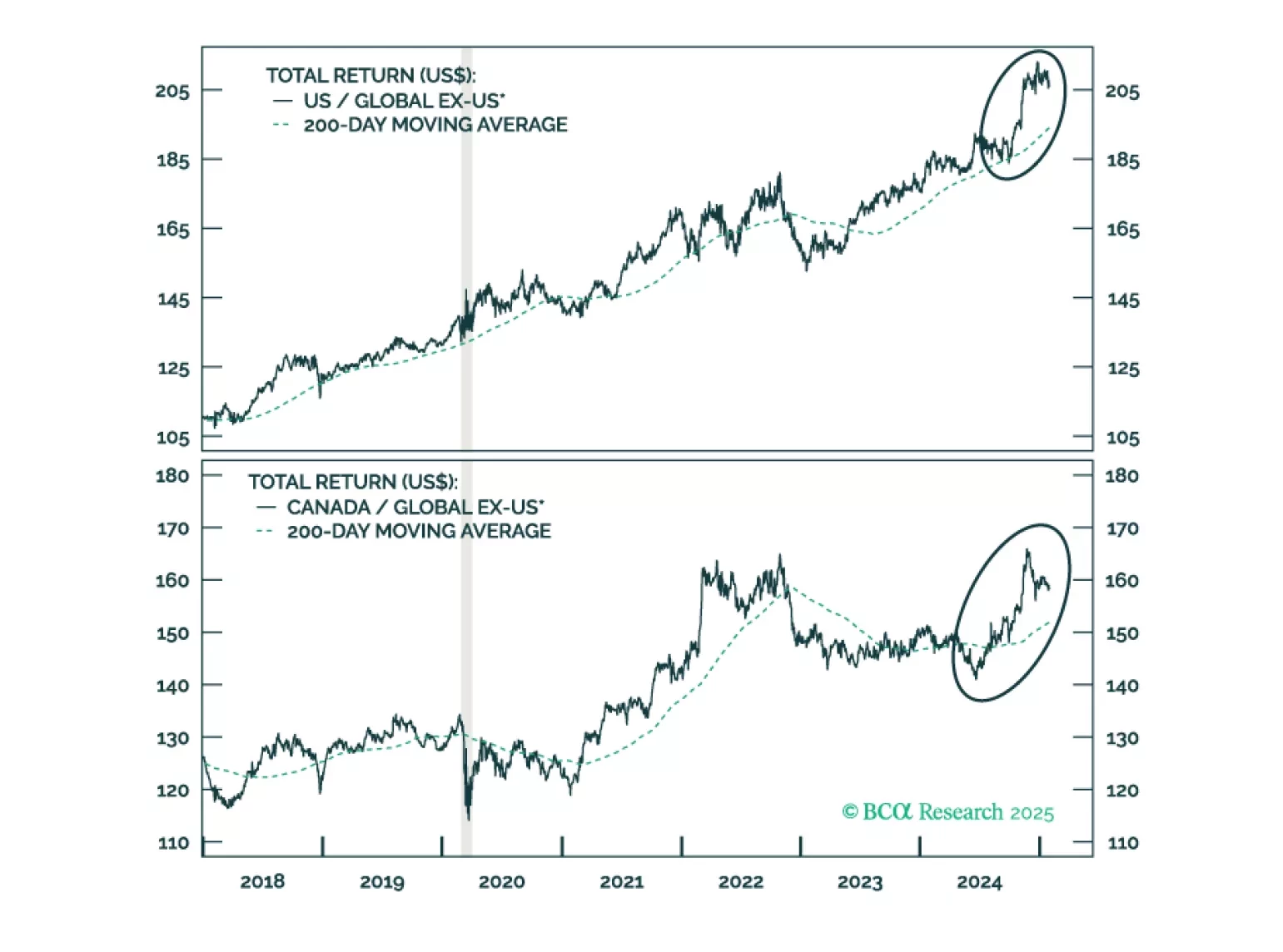

Jonathan provides an update on Canada following strong performance from Canadian stocks last year. On a tactical basis, underweight Canada versus global ex-US on the expectation of tariffs targeting Canada and Mexico. Following a sell off, or if a trade war is avoided, investors should place Canadian stocks on upgrade watch with the goal of moving to a modest overweight versus global ex-US.

France finds itself in a unique, thorny situation. Can it heave itself out of it? And what does it mean for investors?

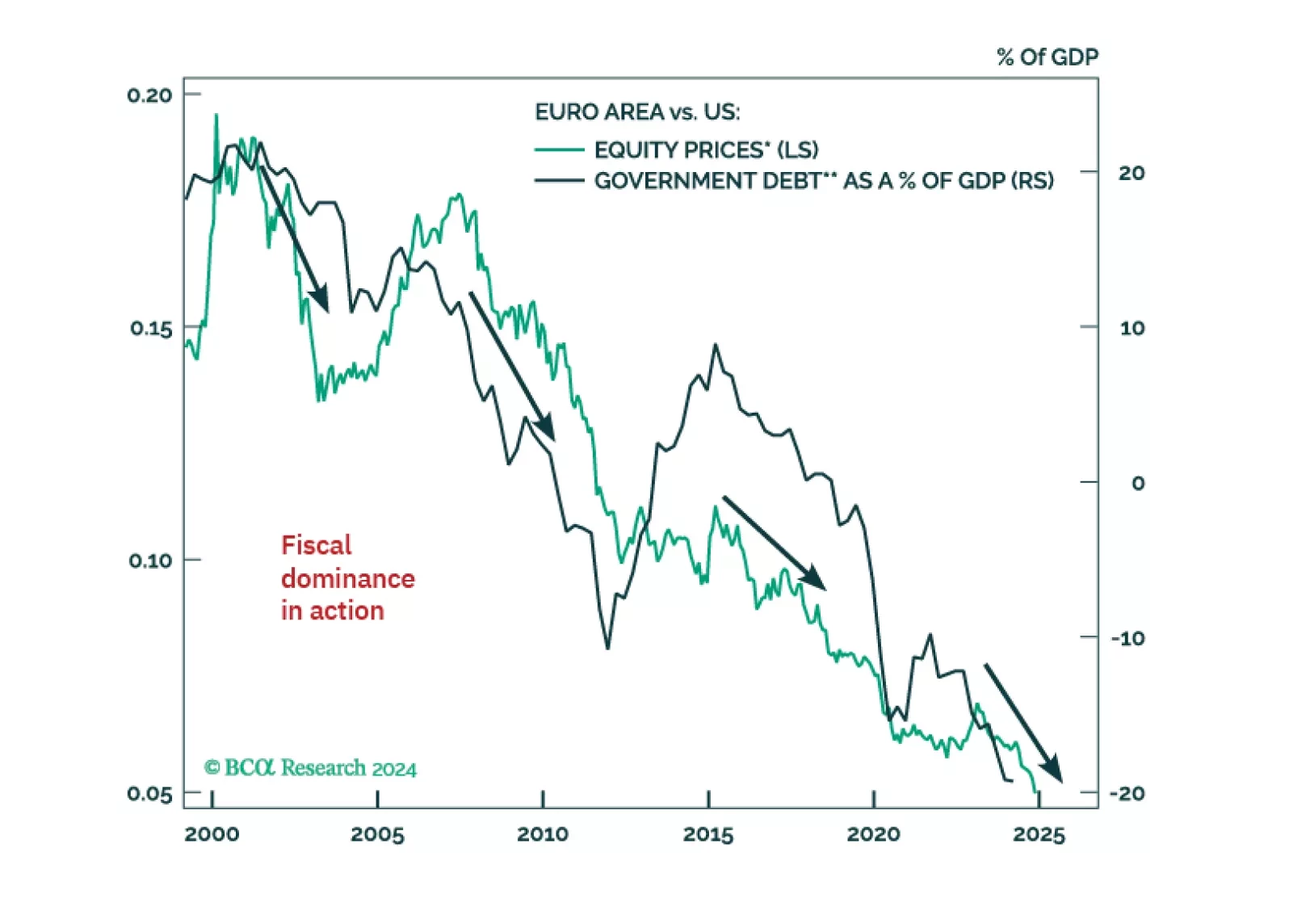

Investors have given up on European assets, which now suffer exceptional discounts to US ones. However, tighter US fiscal policy, the end of Europe’s austerity and deleveraging, the LNG Tsunami about to hit European shores, and the global capex fueled by the Impossible Geopolitical Trinity mean that Europe’s time to shine will soon come back.

Investors have given up on European assets, which now suffer exceptional discounts to US ones. However, tighter US fiscal policy, the end of Europe’s austerity and deleveraging, the LNG Tsunami about to hit European shores, and the global capex fueled by the Impossible Geopolitical Trinity mean that Europe’s time to shine will soon come back.