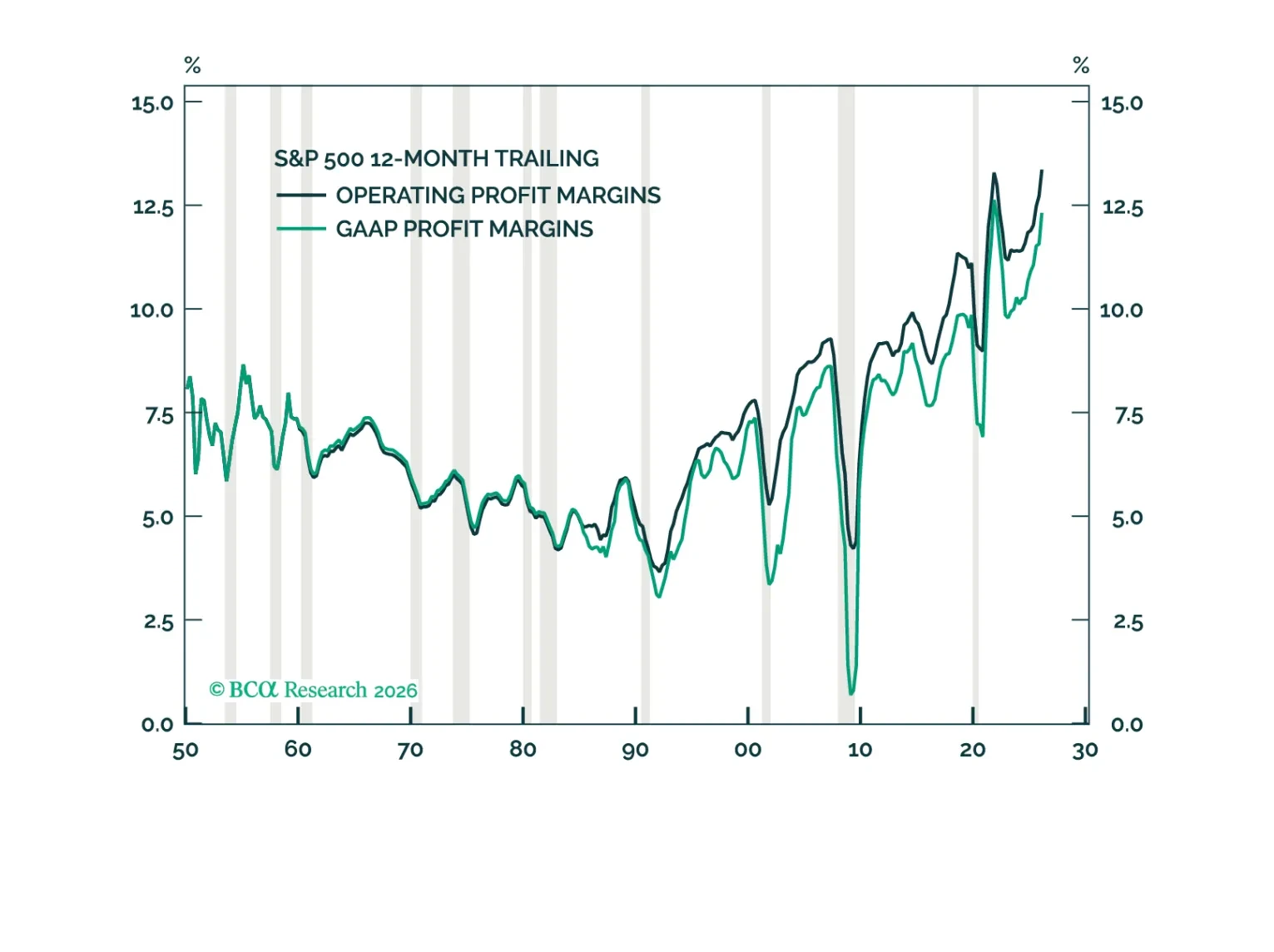

Corporate Profits

The Goldilocks environment for US profit margins should start to sour next year. Contrary to conventional wisdom, AI could end up eroding margins for both producers and consumers of artificial intelligence.

Most of the increase in S&P 500 earnings estimates this year has stemmed from shortages. The oil shortage, which has pushed up estimates for energy companies, will fade once the military conflict is resolved. However, the shortage of semiconductors and other AI paraphernalia could persist for a while longer. As such, we are moving our recommended 12-month equity allocation from a slight underweight to neutral. We are already neutral on a 3-month horizon.

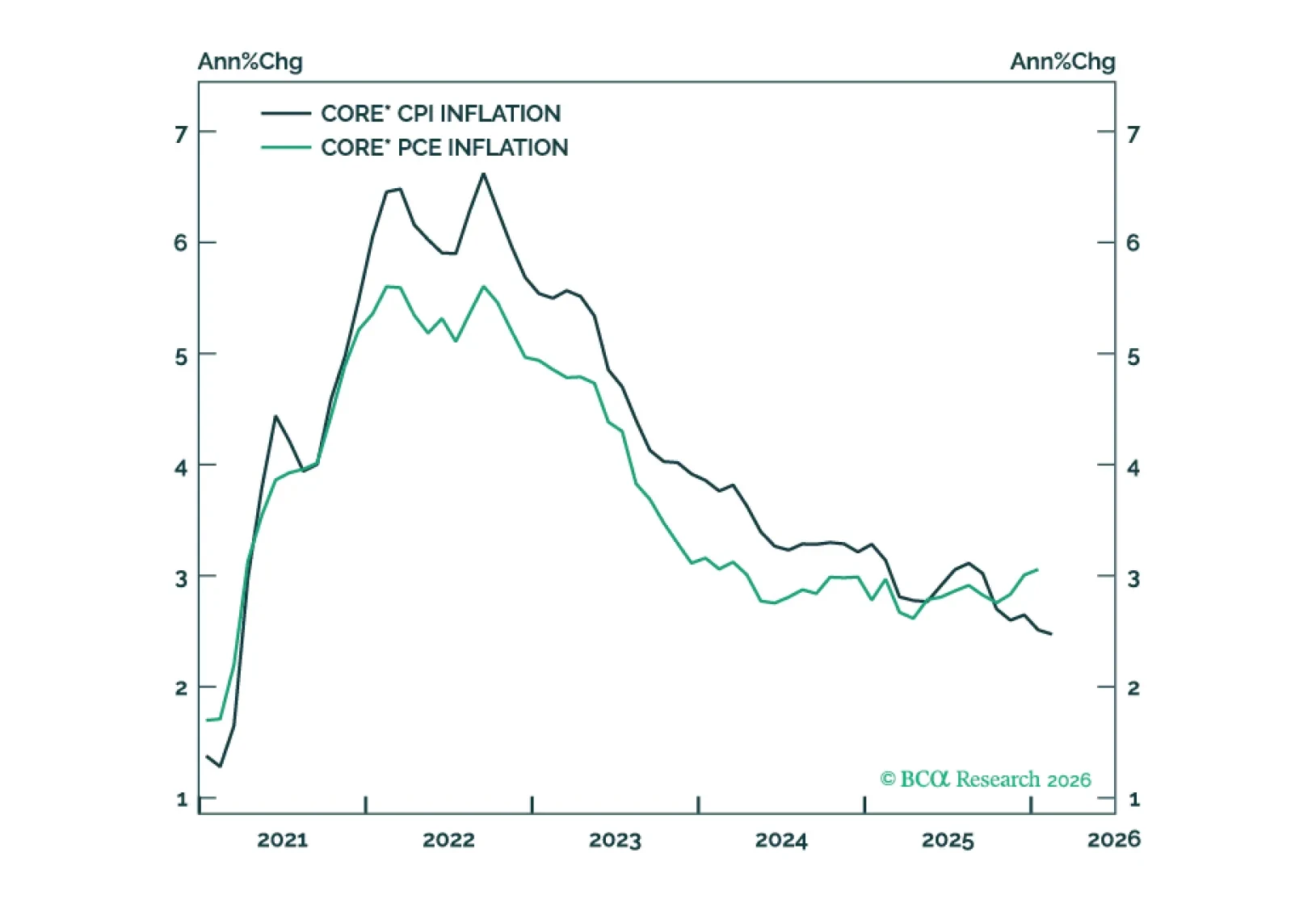

The gap between PCE and CPI inflation will narrow within the next few months, mostly driven by core PCE inflation converging toward its trimmed mean.

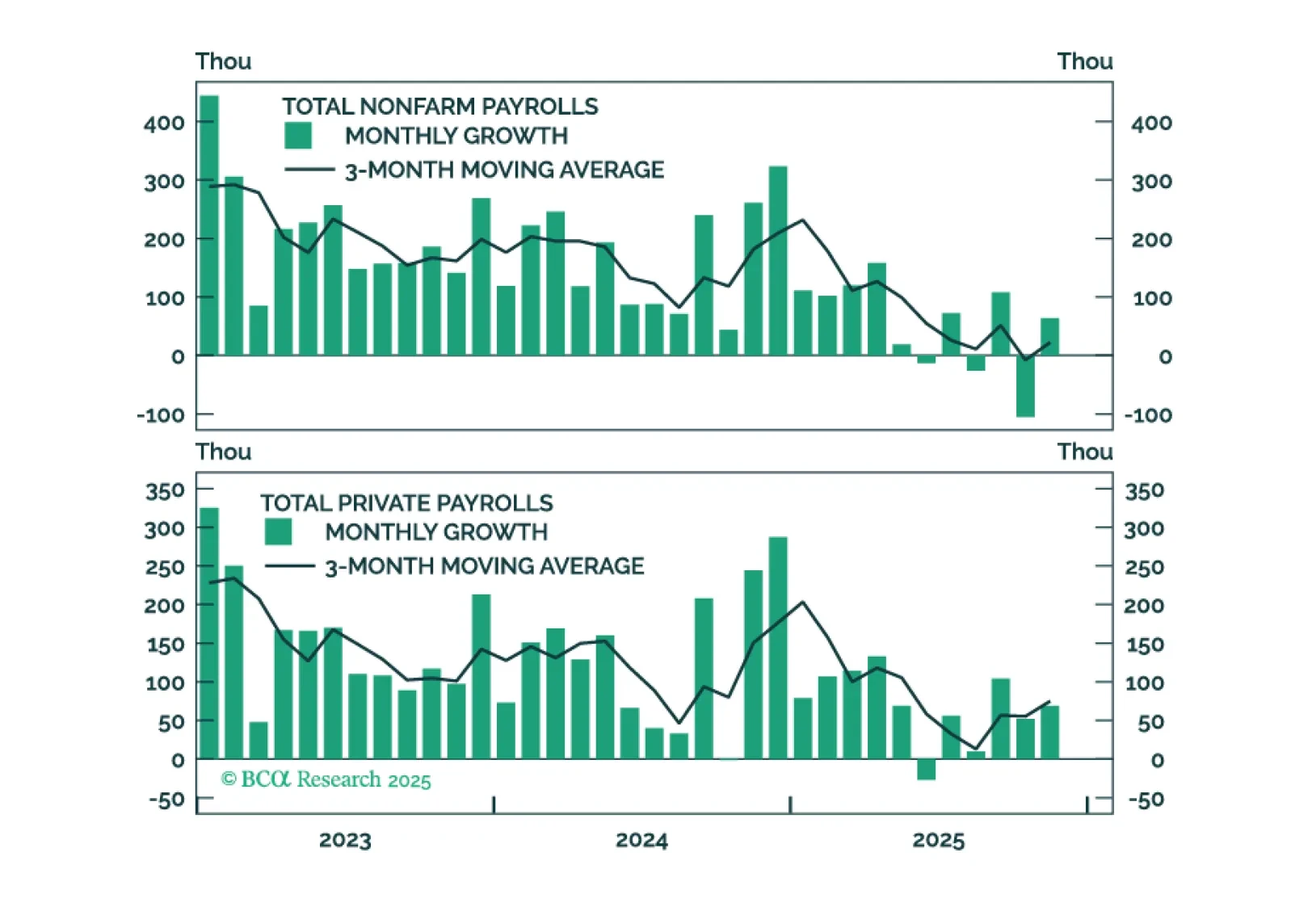

Employment Data Point To Dovish Policy Surprises In 2026

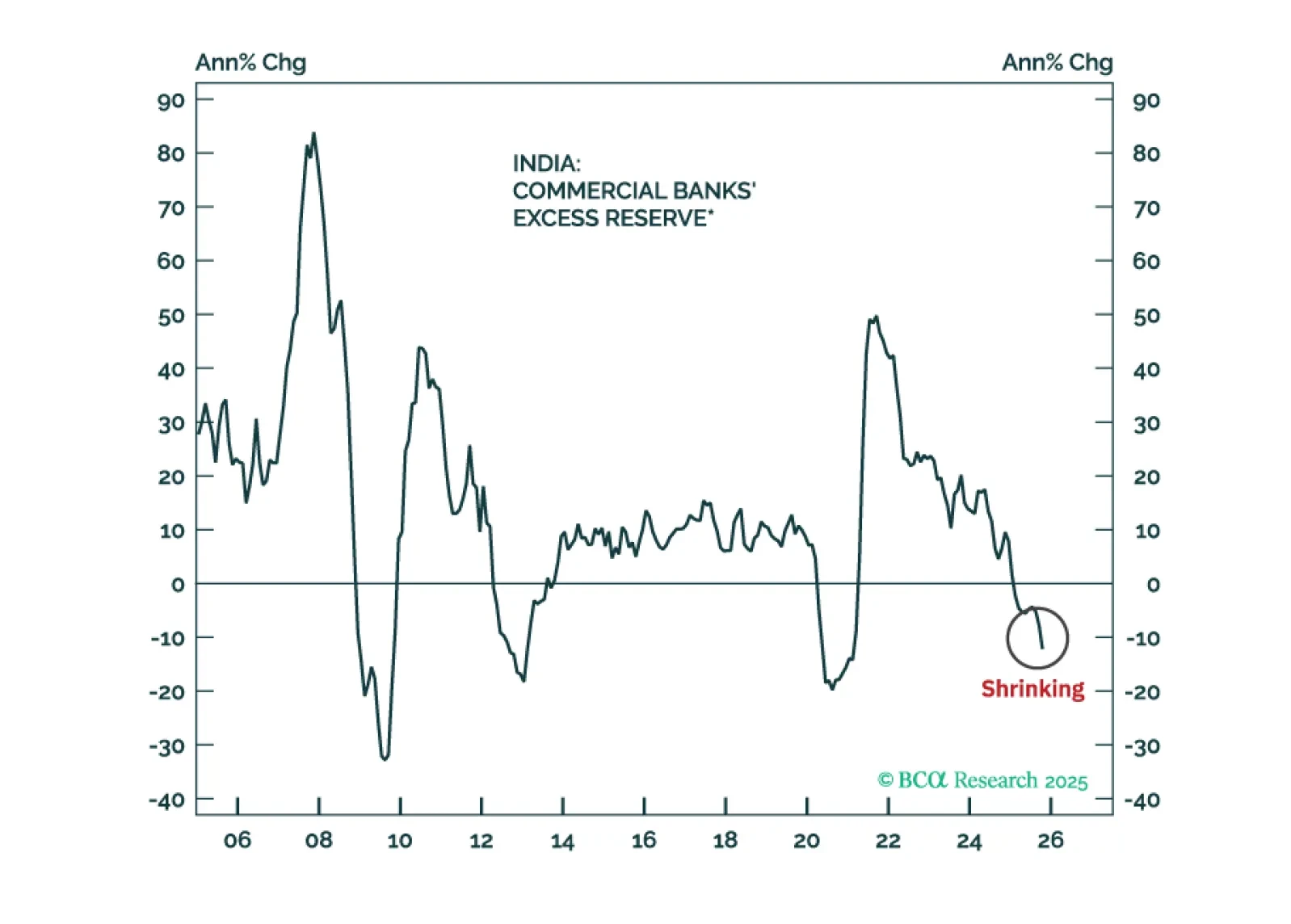

Indian stocks have further downside in absolute terms as profits disappoint. Their underperformance versus the EM equity benchmark, however, is late, which warrants a shift from underweight to neutral allocation.

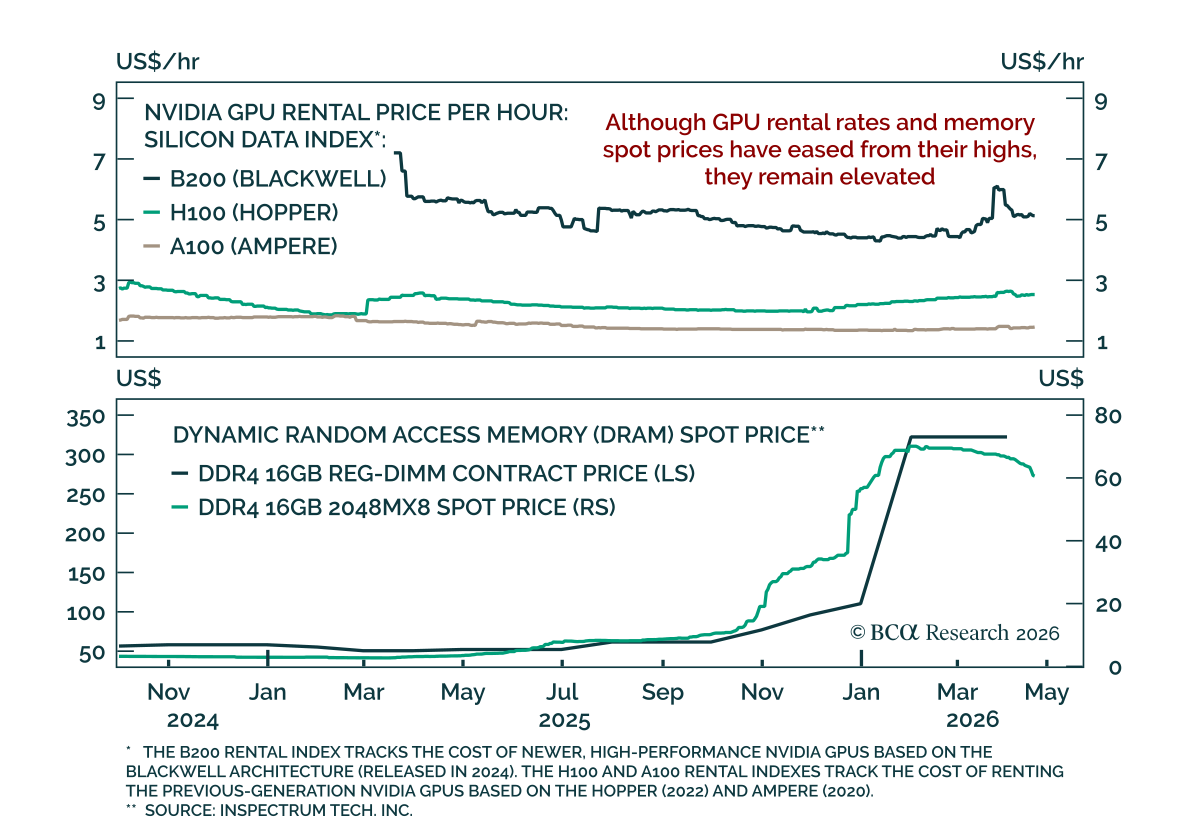

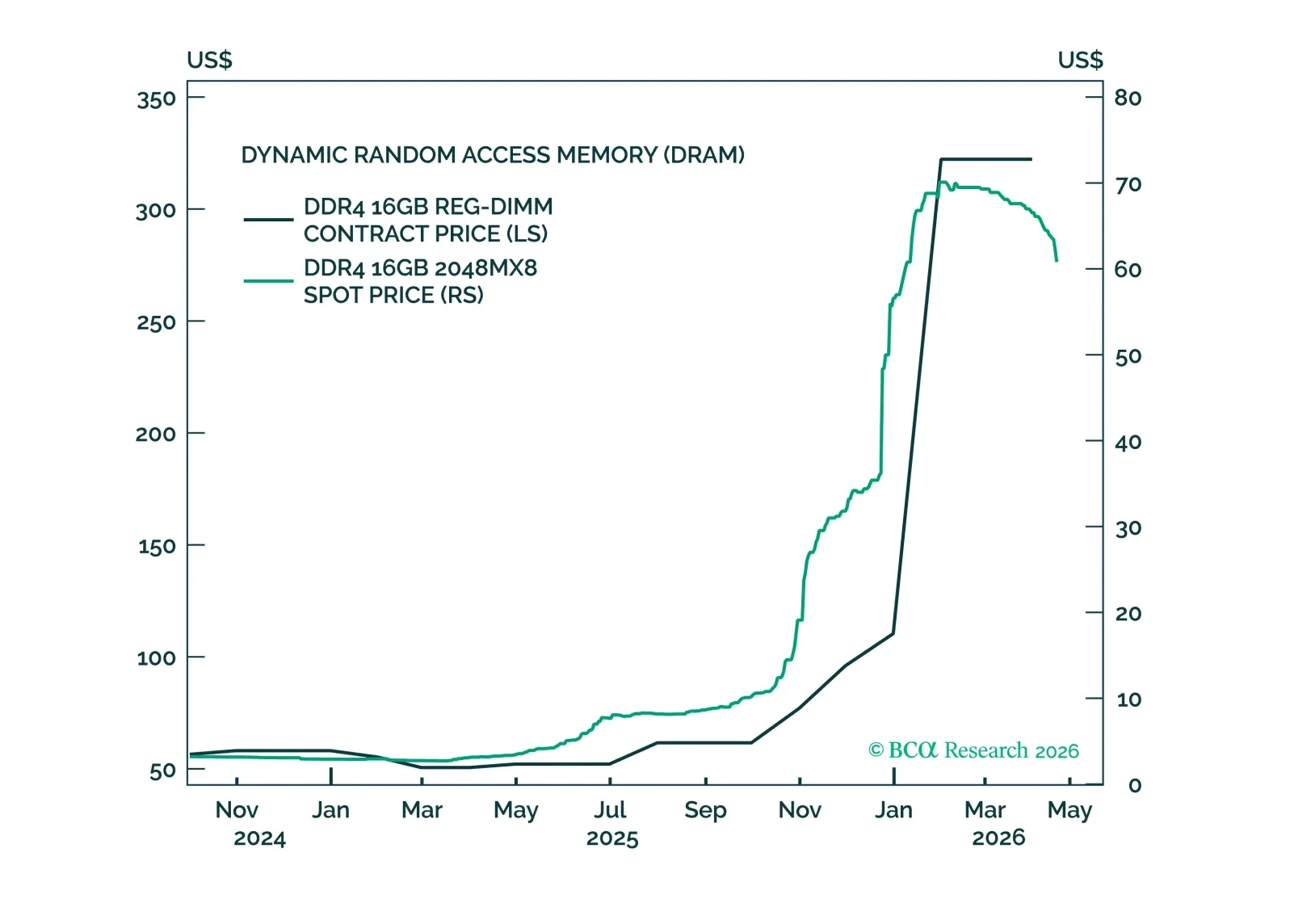

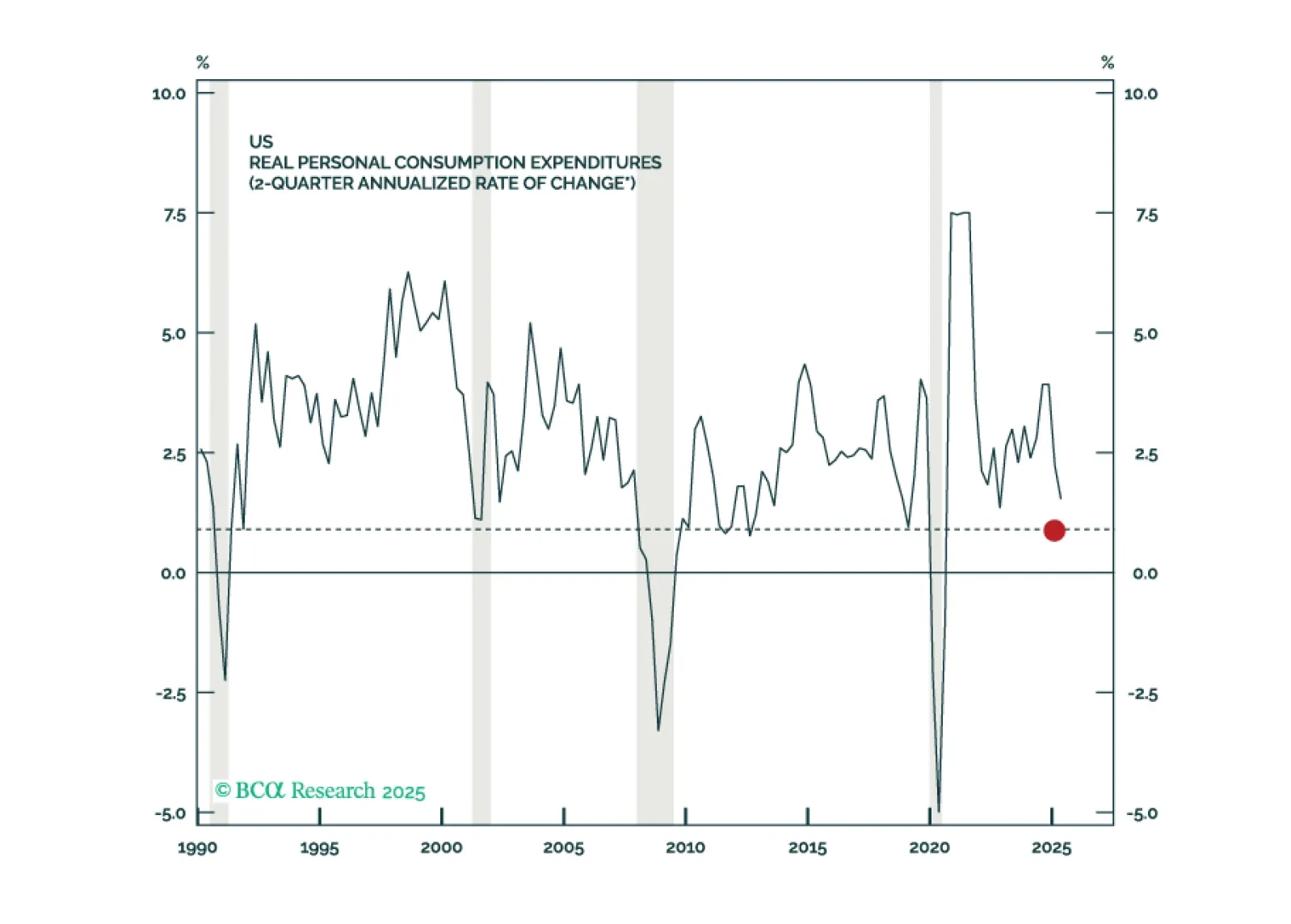

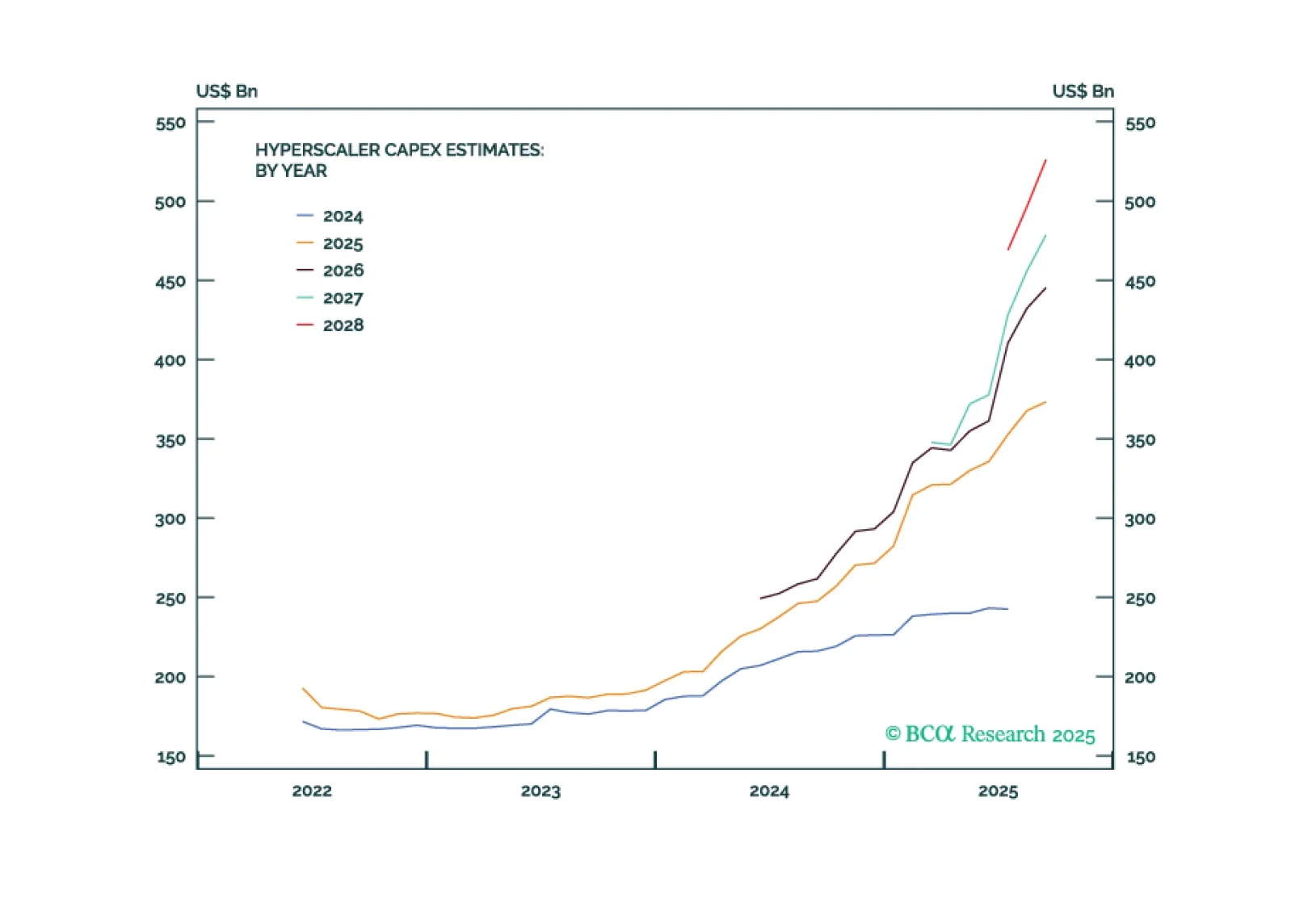

In Section I, Doug explains how the sharp upward revision to second-quarter consumption in the final GDP estimate has reduced our recession conviction and could lead us to abandon our recession call altogether. The situation is fluid, though, as typified by the striking weakness of stocks in consumer-facing and cyclically exposed subindustries. In Section II, Doug and Global Investment Strategy’s Miroslav Aradski consider the implications of the AI investment boom.

In Section II, Doug and Global Investment Strategy’s Miroslav Aradski consider the implications of the AI investment boom.

The rush to build AI infrastructure is based on a false premise: that there are significant advantages to being the first to come to market.