Business Cycles

The June swoon looks like a rotation and rebalancing-driven air pocket, not a regime break. Economic growth, earnings revisions, and AI-driven capex demand remain firm, but rising yields, inflation concerns, Fed uncertainty, and a looming IPO wave are likely to constrain further multiple expansion. But progress toward a resolution of mid-east tensions, rallying bonds, and falling oil prices, have motivated us to add a tactical long consumer discretionary trade.

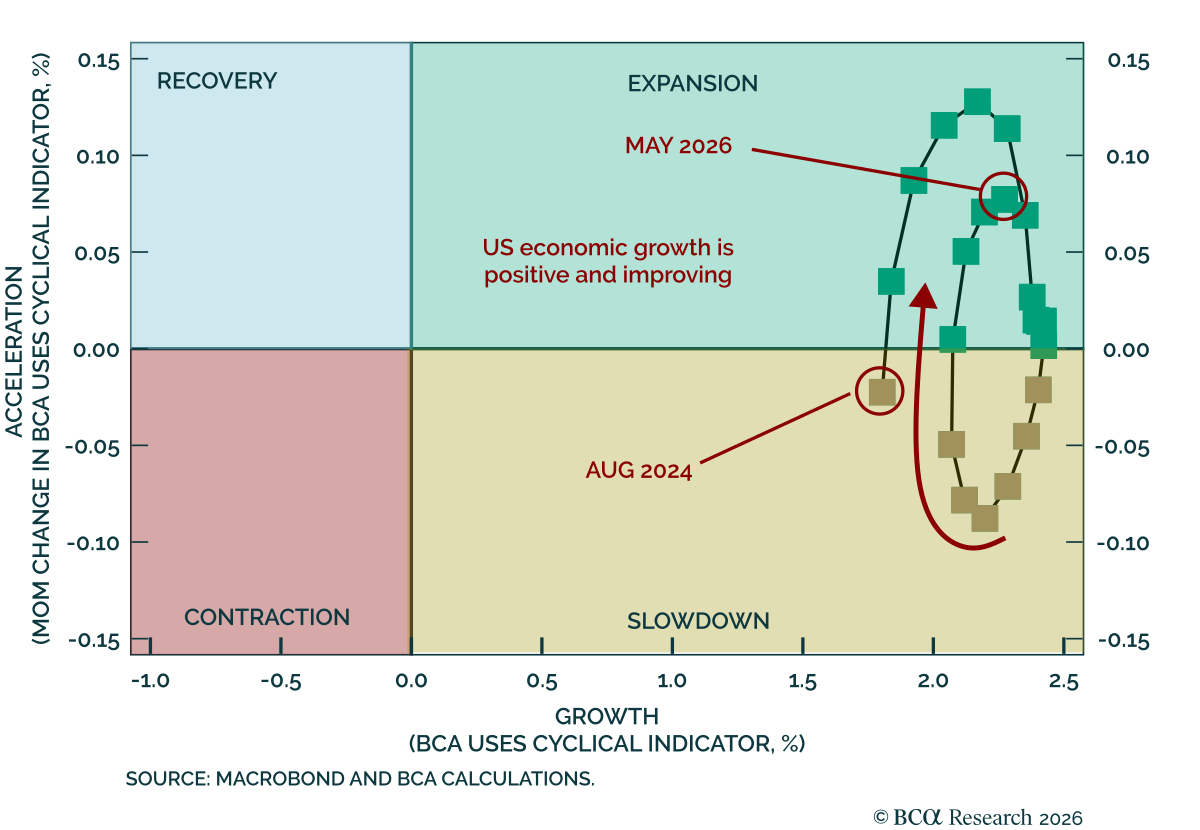

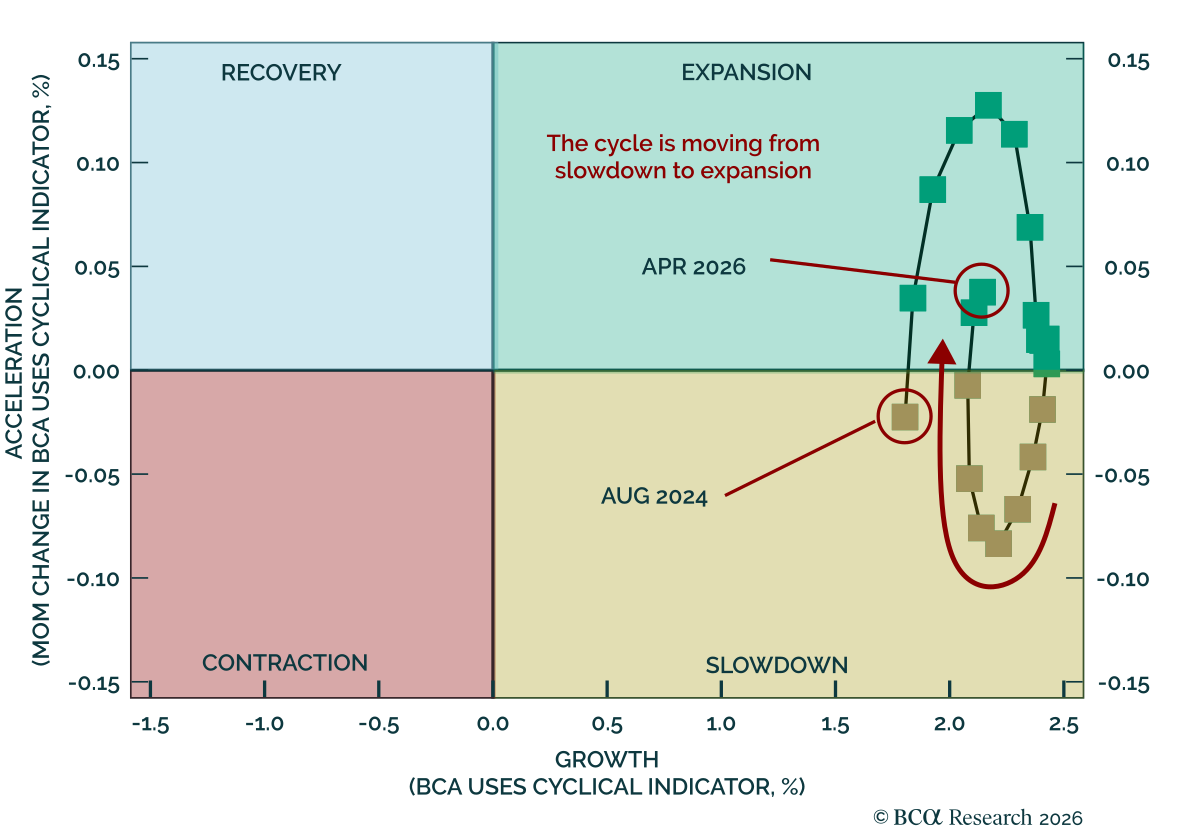

US growth remains positive and is now improving, with the economy seemingly exiting Slowdown and proceeding into Expansion. Markets are reflecting the shift, rewarding revenue growth and capex growth, while earnings expectations continue to advance. The backdrop remains supportive, but expectations are rising and risks from financial conditions linger.

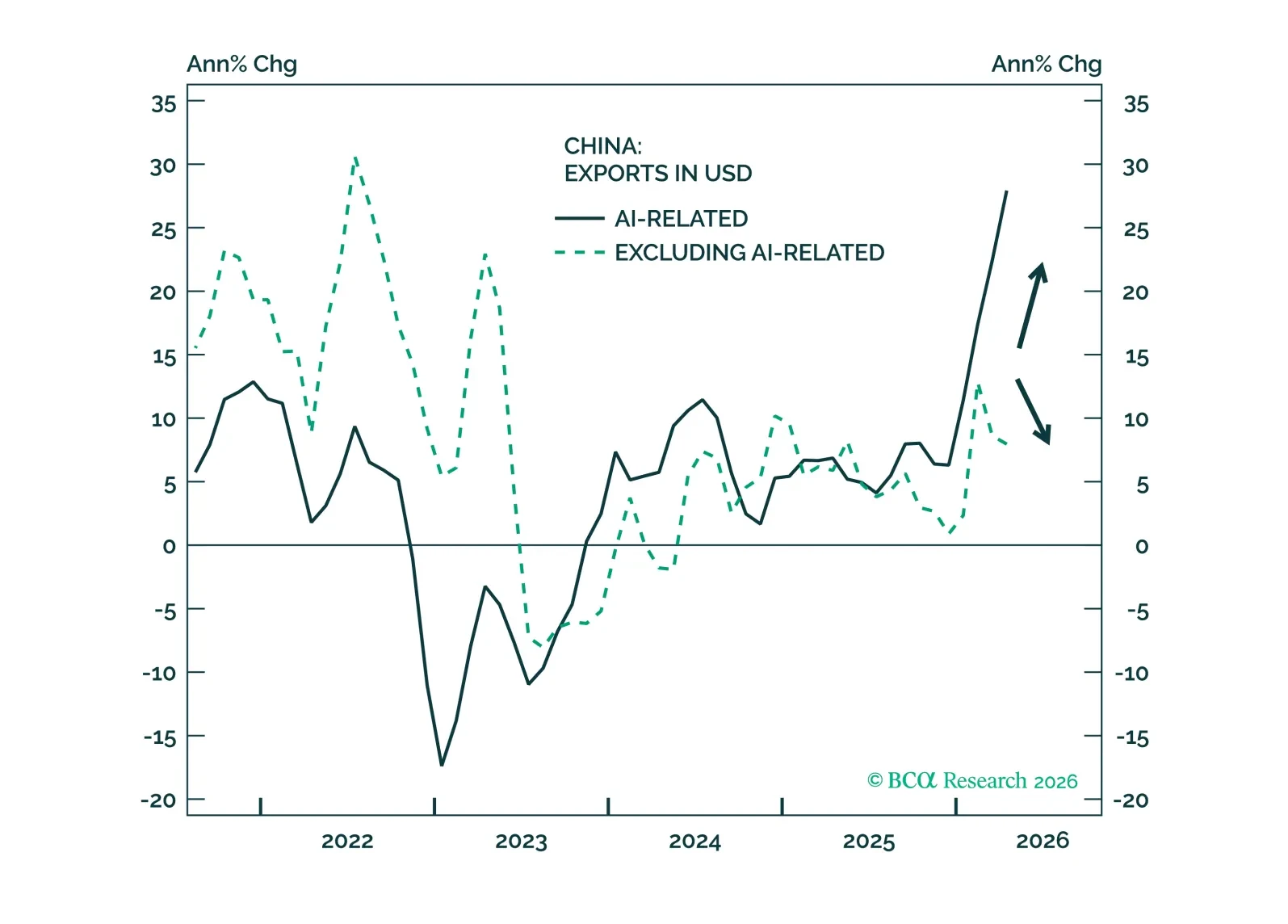

China’s K-shaped economy is widening, with resilient exports and subdued domestic consumption. Over the next 6–12 months, we see a higher probability that global capex momentum persists than China delivers meaningful consumer-focused stimulus.

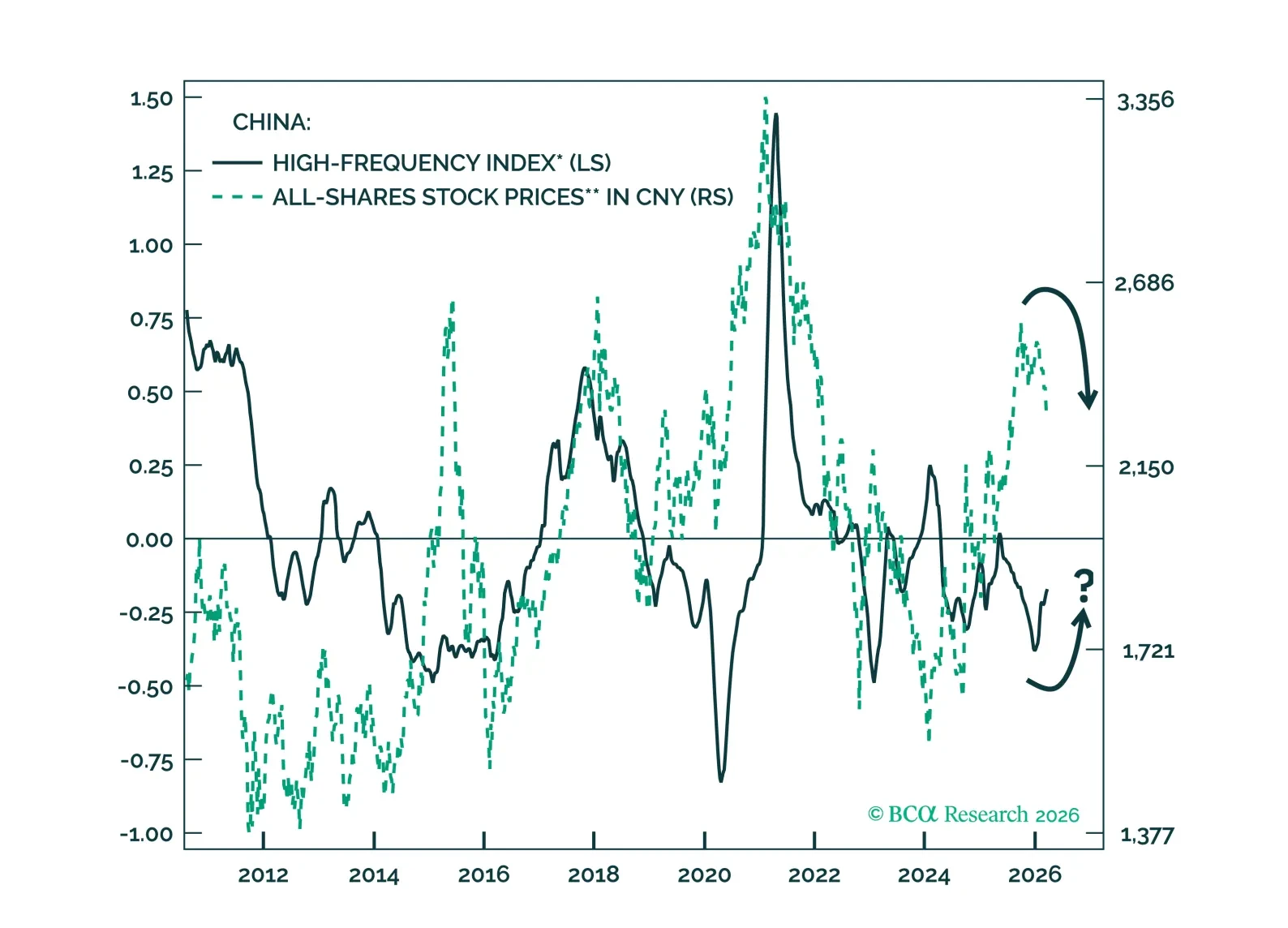

Chinese stock prices are converging with economic growth after a 2025 rally. While the country can endure a short-term oil price shock, it remains susceptible to extended supply disruptions and a global slowdown.

This screener report builds on the US Equity Strategy and Equity Analyzer collaboration published on 23 February 2026, where we introduced our latest framework for assessing the US business cycle. Here, we apply the framework to our screener to identify how bottom-up equity positioning should adapt as the cycle evolves.

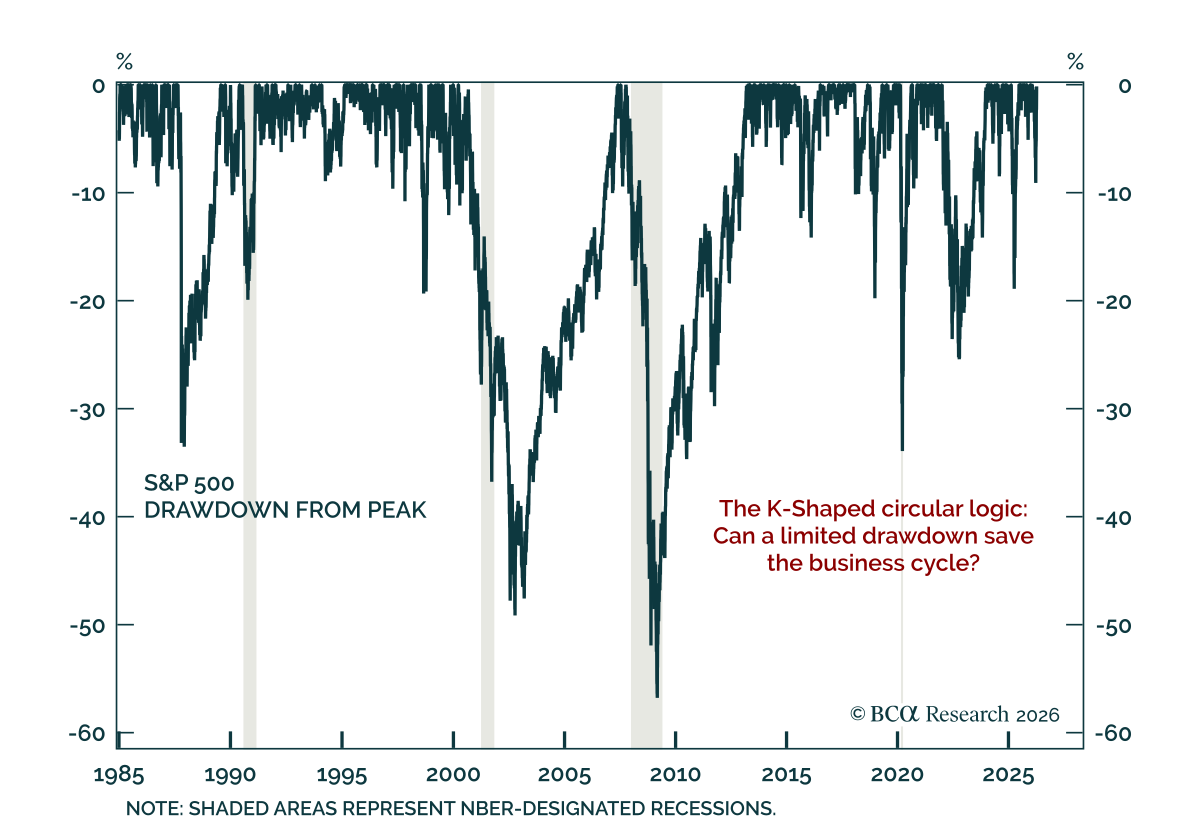

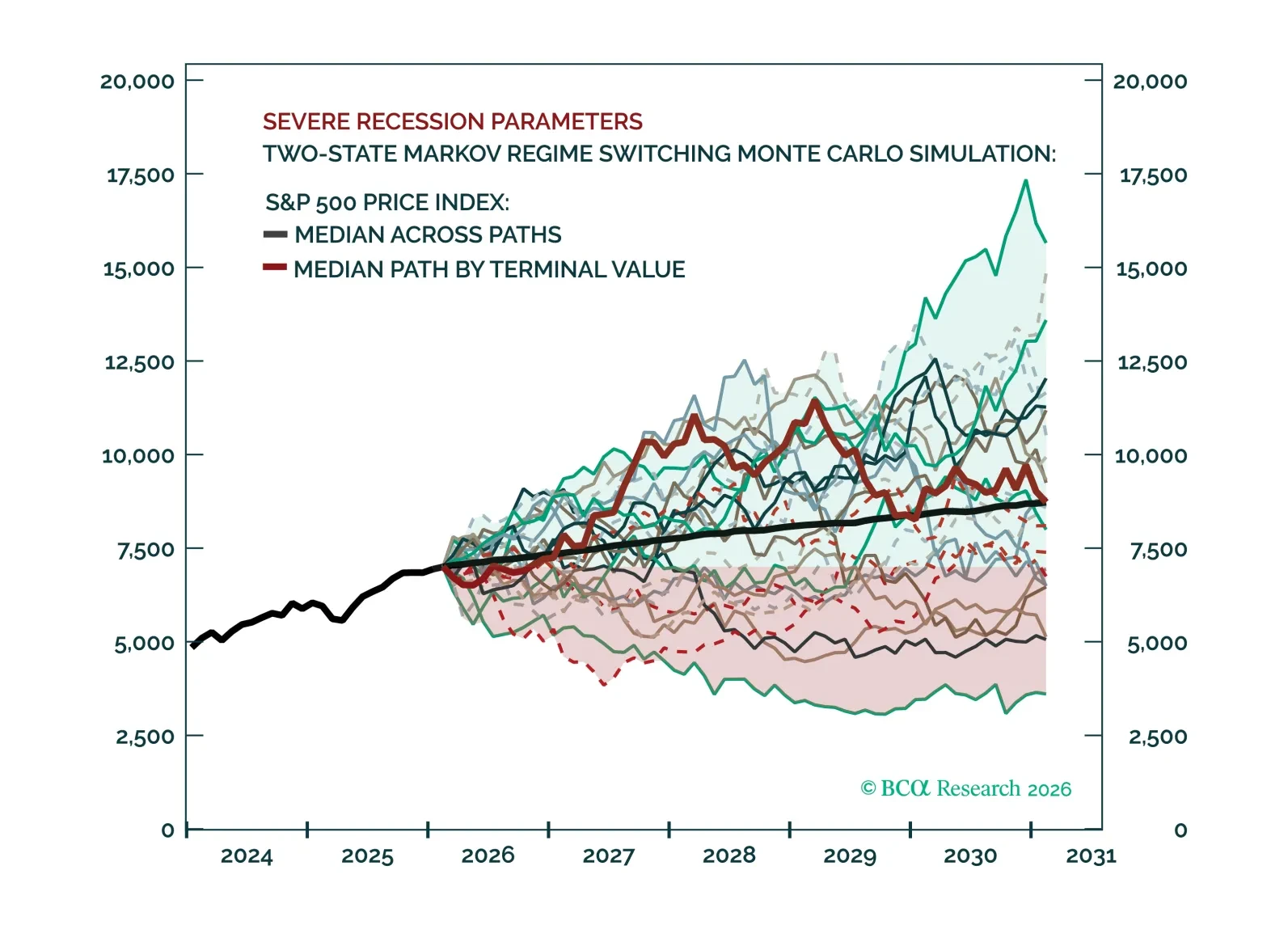

Recessions are inevitable but unpredictable. While earnings drive long‑term equity performance through the cycle, around turning points fundamentals follow a predictable sequence: multiples contract first, then prices, then earnings. Recessions can shift sector leadership, but simulations show that medium‑term index‑level upside remains intact unless future downturns are materially more severe than in history.

The US economy is in the Slowdown phase of the business cycle, according to our measure of aggregate US economic activity; growth remains positive but acceleration is negative. Historically, this phase more often resolves in reacceleration than recession. Recent market price action, from the index, to sectors, to relative industry performance, broadly reflects typical Slowdown phase dynamics.