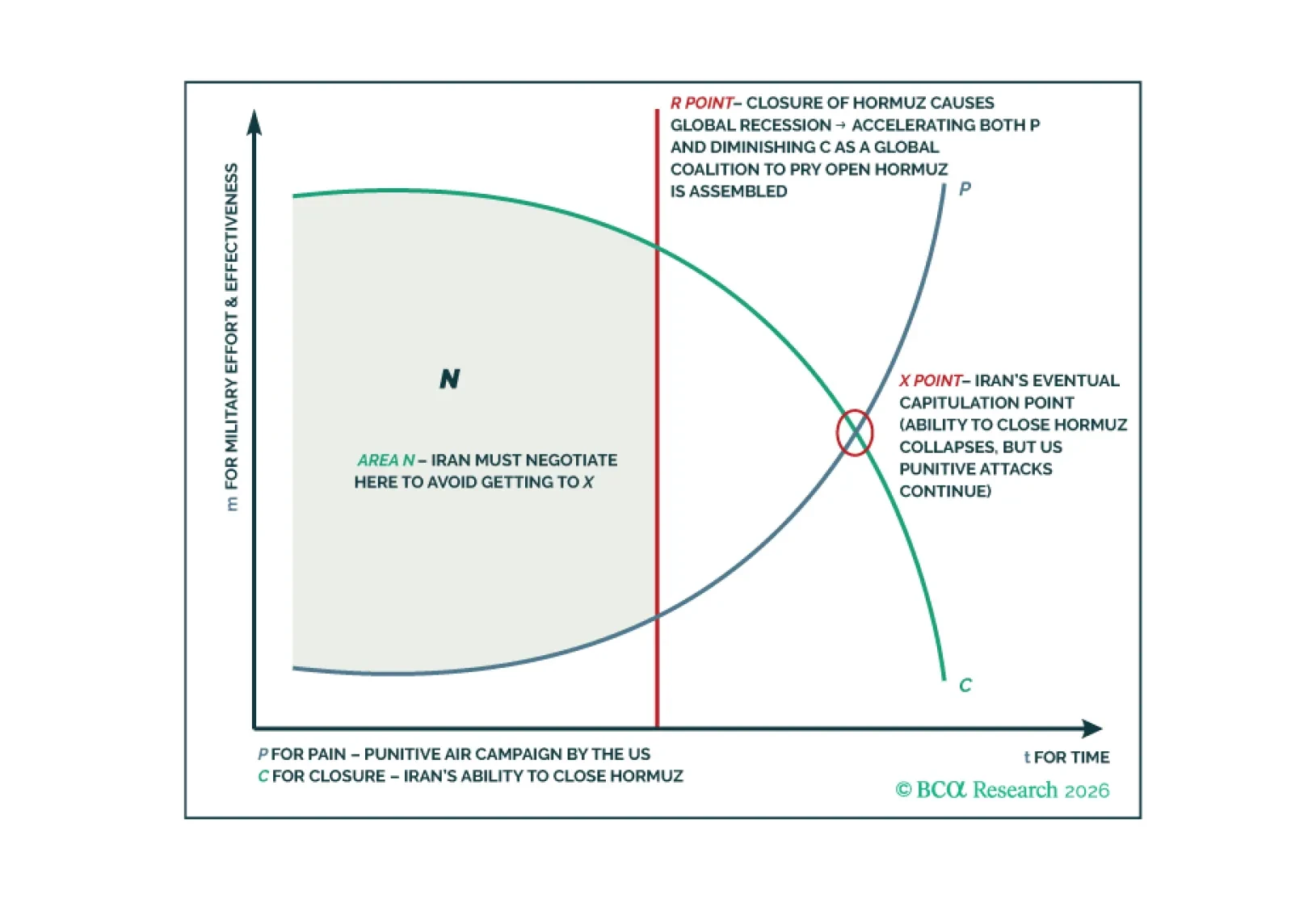

Iran

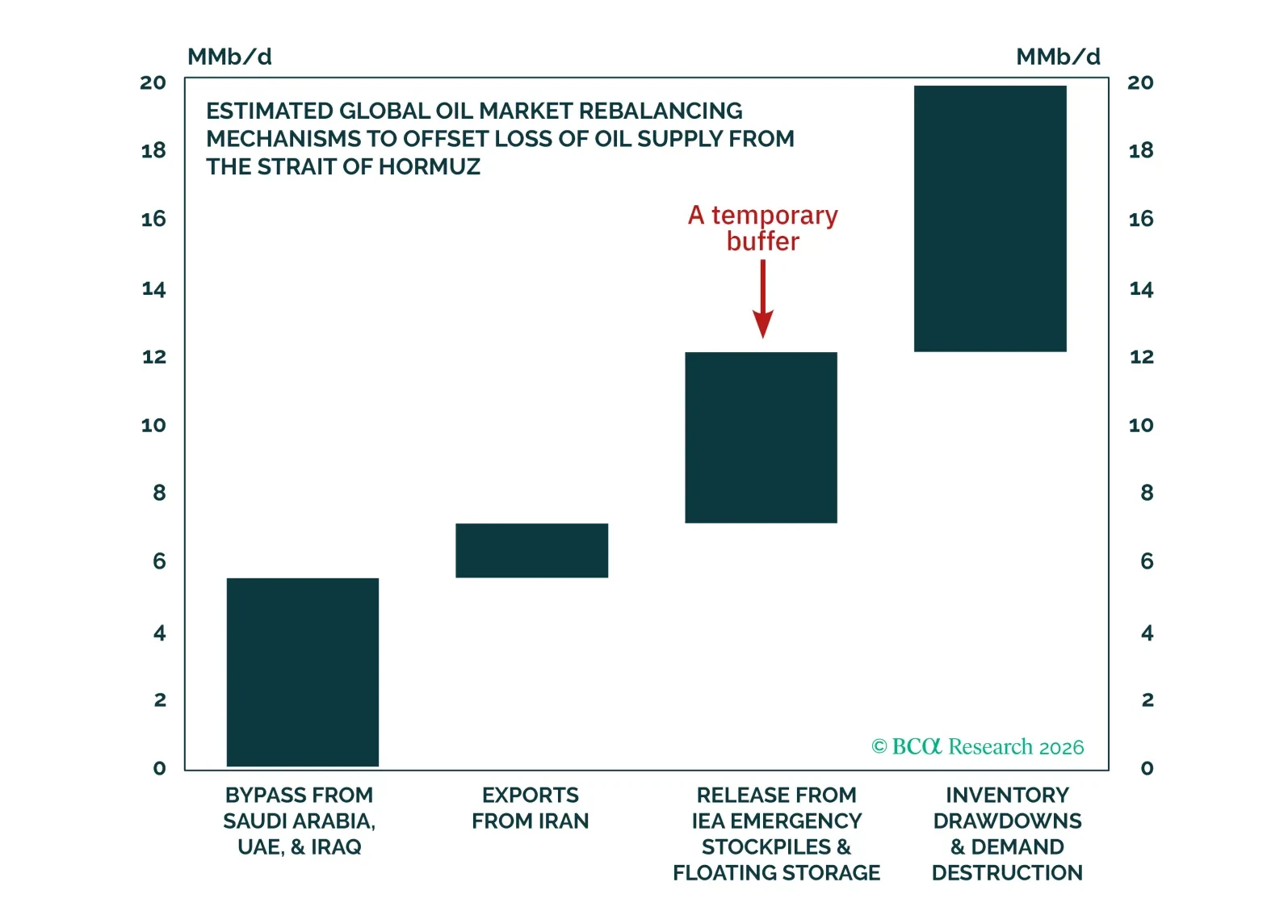

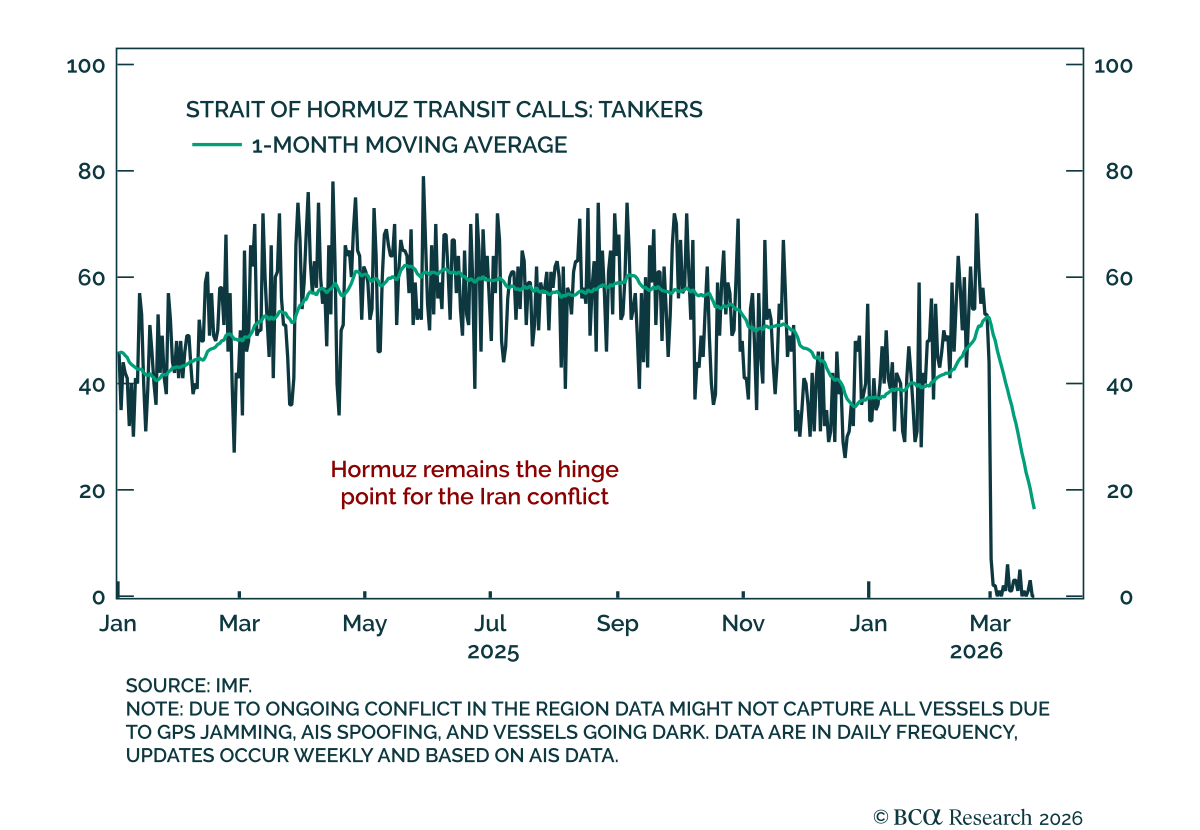

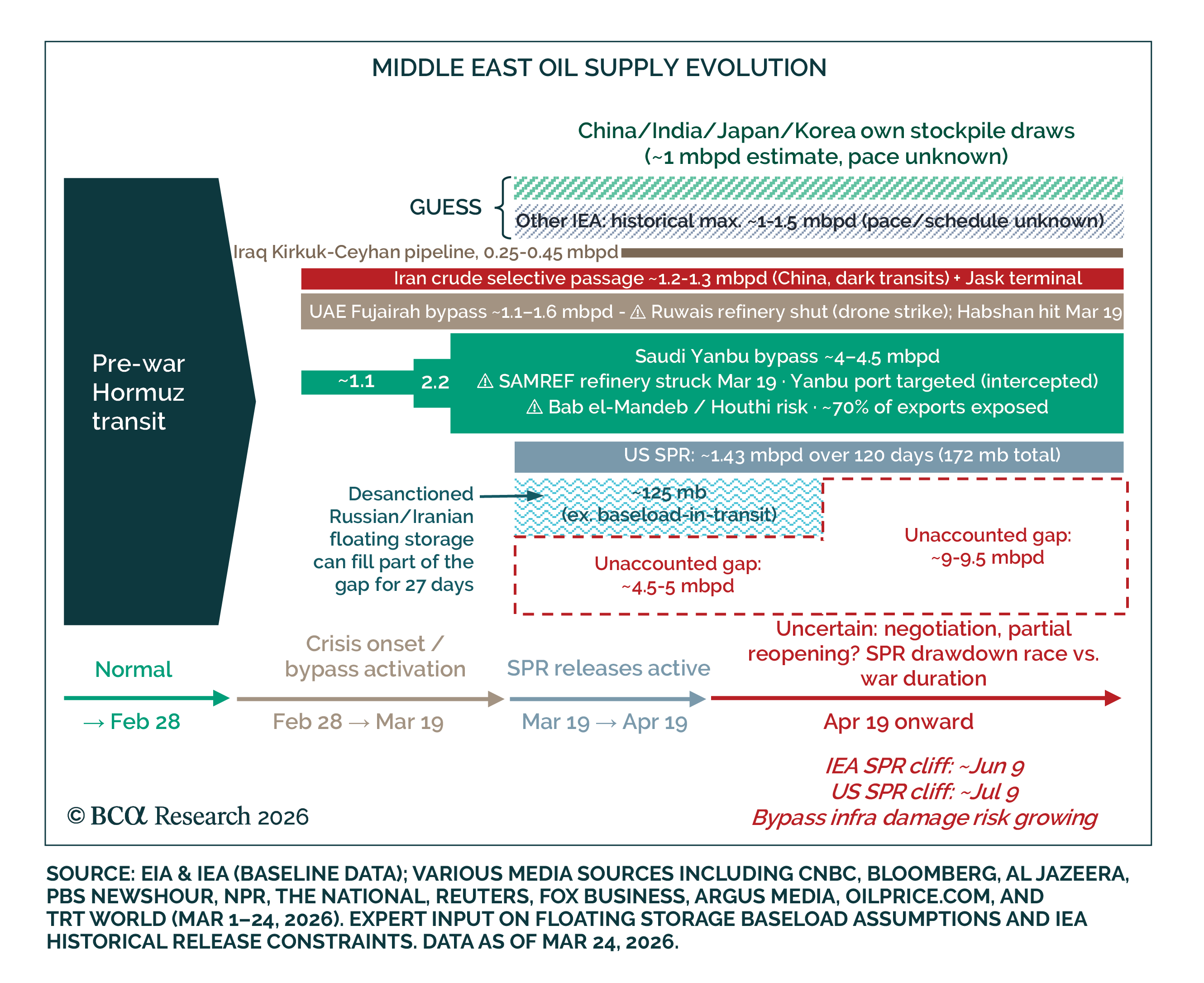

Over the past month, oil market participants have scrambled to fill the gap in global oil supply caused by the Strait of Hormuz’s closure. While these efforts have been impressive, the scale of the disruption means they are ultimately insufficient. Upside pressures will continue to dominate energy prices until transit through the Strait of Hormuz is restored.

One month into the Iranian conflict, we take stock of how markets have moved so far and how some of the big open questions might influence them going forward. A long opportunity may be developing at the long end of the Treasury curve.

In Section I, Doug argues that investors should maintain mildly defensive positioning while awaiting the restoration of normalized shipping flows through the Strait of Hormuz. In Section II, Jonathan examines the humanoid robot segment of the emerging physical AI landscape, concluding that humanoid robots are a potential but not yet imminent investment theme.

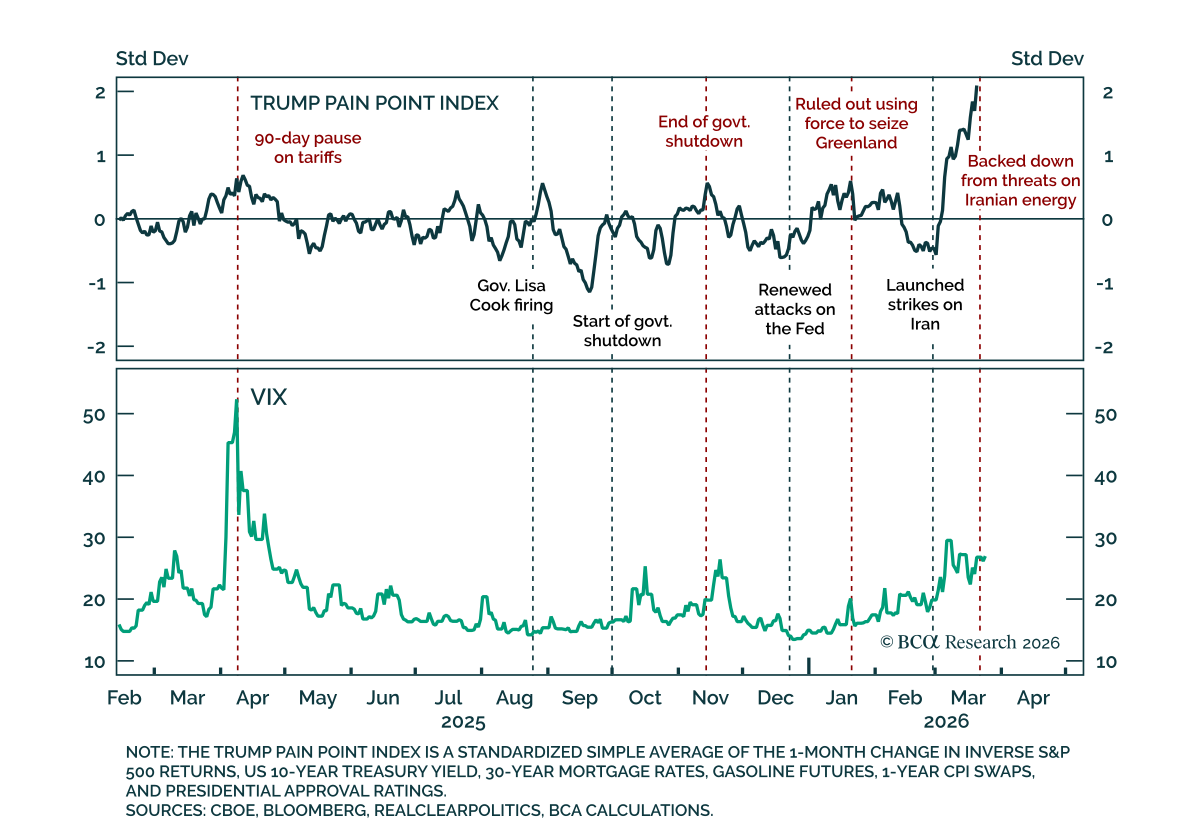

The Iran war may not deescalate in the near term, and if it does, it will likely reescalate later this year, suggesting investors should take a cyclically defensive outlook.

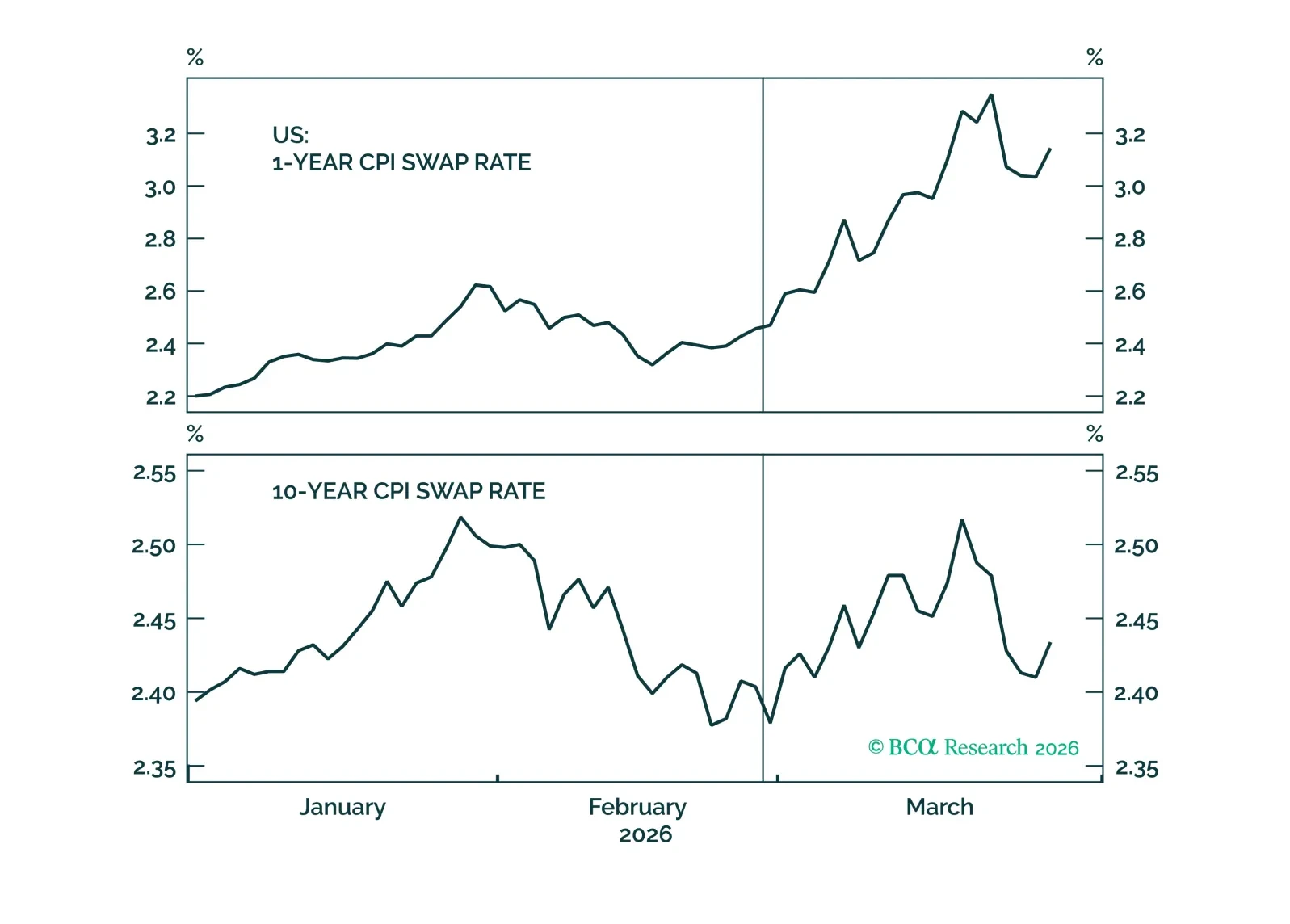

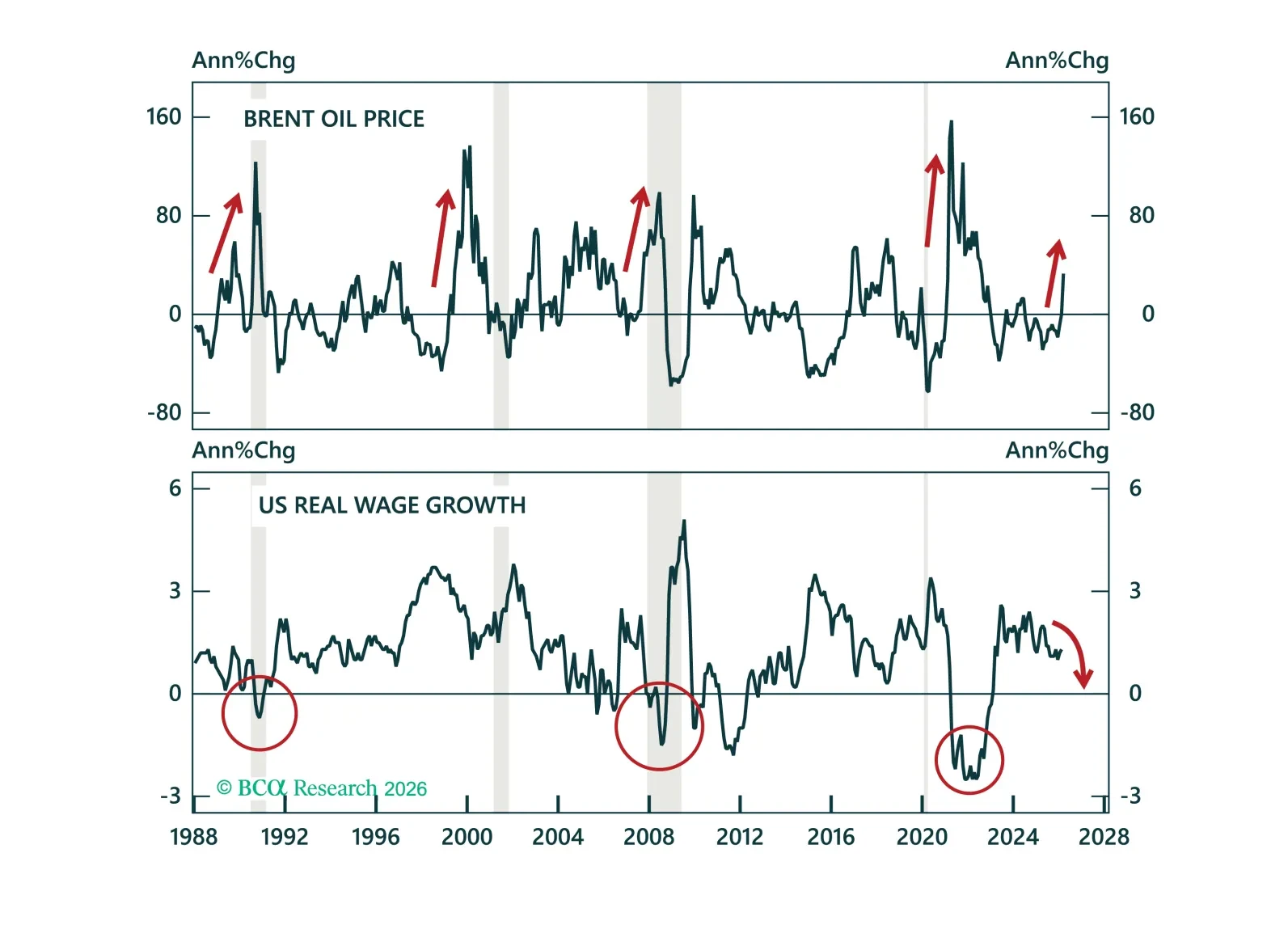

In today’s Strategy Insight, we show why both a quick resolution and a prolonged crisis ultimately point to lower yields.

When the fog of war is thick investors need hard facts and data to cut through the uncertainty. Unfortunately, when it comes to physical commodities, publicly available macro data obscures the reality of moving molecules around the world. Thankfully, we at BCA Research have spent the past eight decades building relationships with clients who do all sorts of things for a living. These folks may rely on us for help with the macro context, but they are all experts in their own subsets of the financial industry.