Emerging Markets

There are several widespread market narratives regarding US inflation, the Fed’s policy, global manufacturing/trade and China’s recovery that we disagree with. In this report, we explain our reasoning and where it puts us in terms of investment strategies.

The Gulf’s political economy – particularly that of KSA – drives the supply side of oil-price discovery. This has been evolving since 2017, when OPEC 2.0 was formed. It is now fundamental to the market. We expect Brent to average $95/bbl this year, unchanged from last month, and $115/bbl (up $5/bbl vs. last month). WTI will trade $4-$6/bbl below Brent over the forecast interval. We remain long the XOP and COMT ETFs.

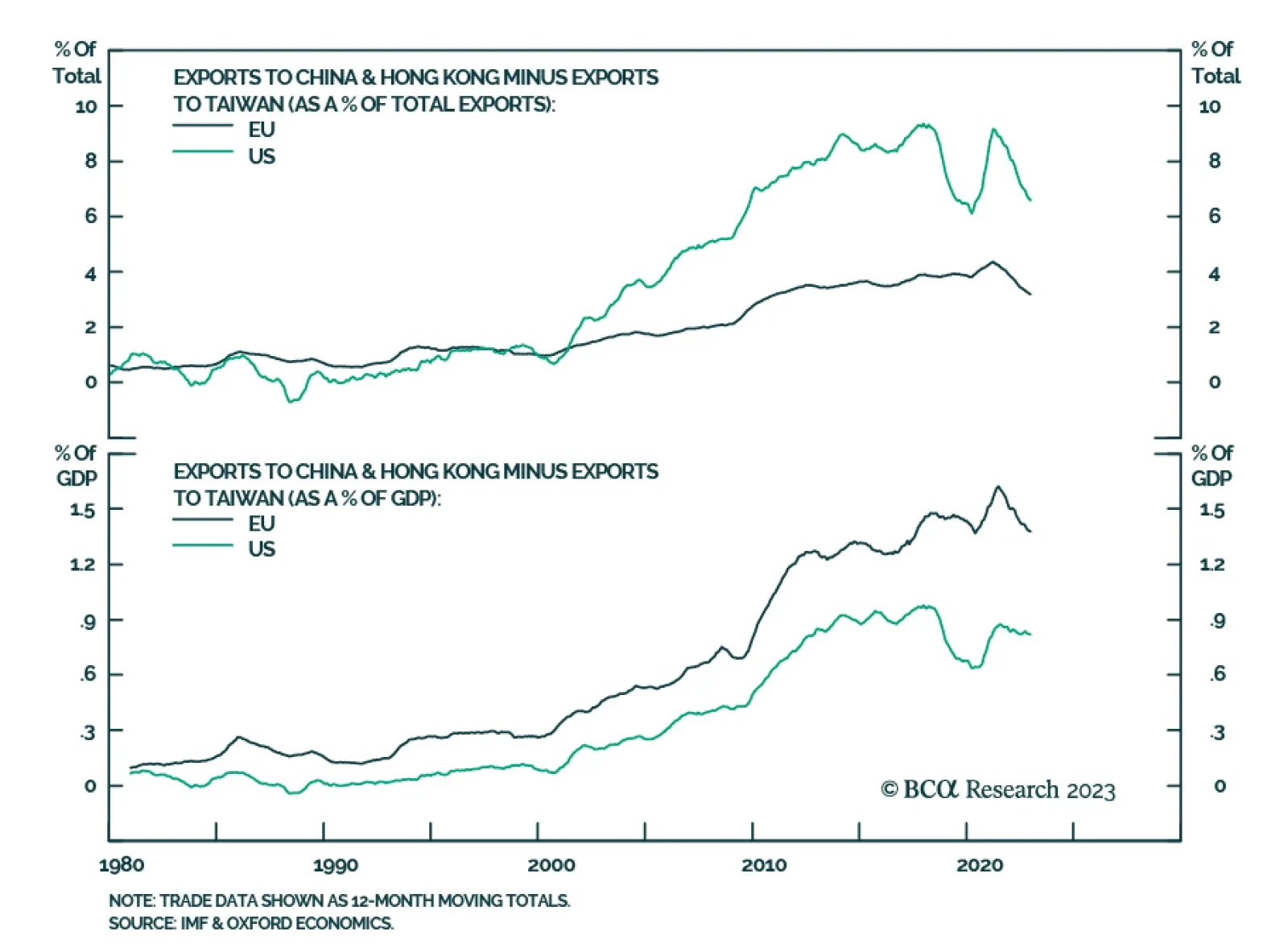

No, the secular rise in geopolitical risk has not peaked. EU-China trade ties underscore the multipolar context, but this multipolarity is unbalanced, as the US has not reached a new equilibrium with its rivals. While the second quarter is murky, investors should stay defensive this year on the whole.

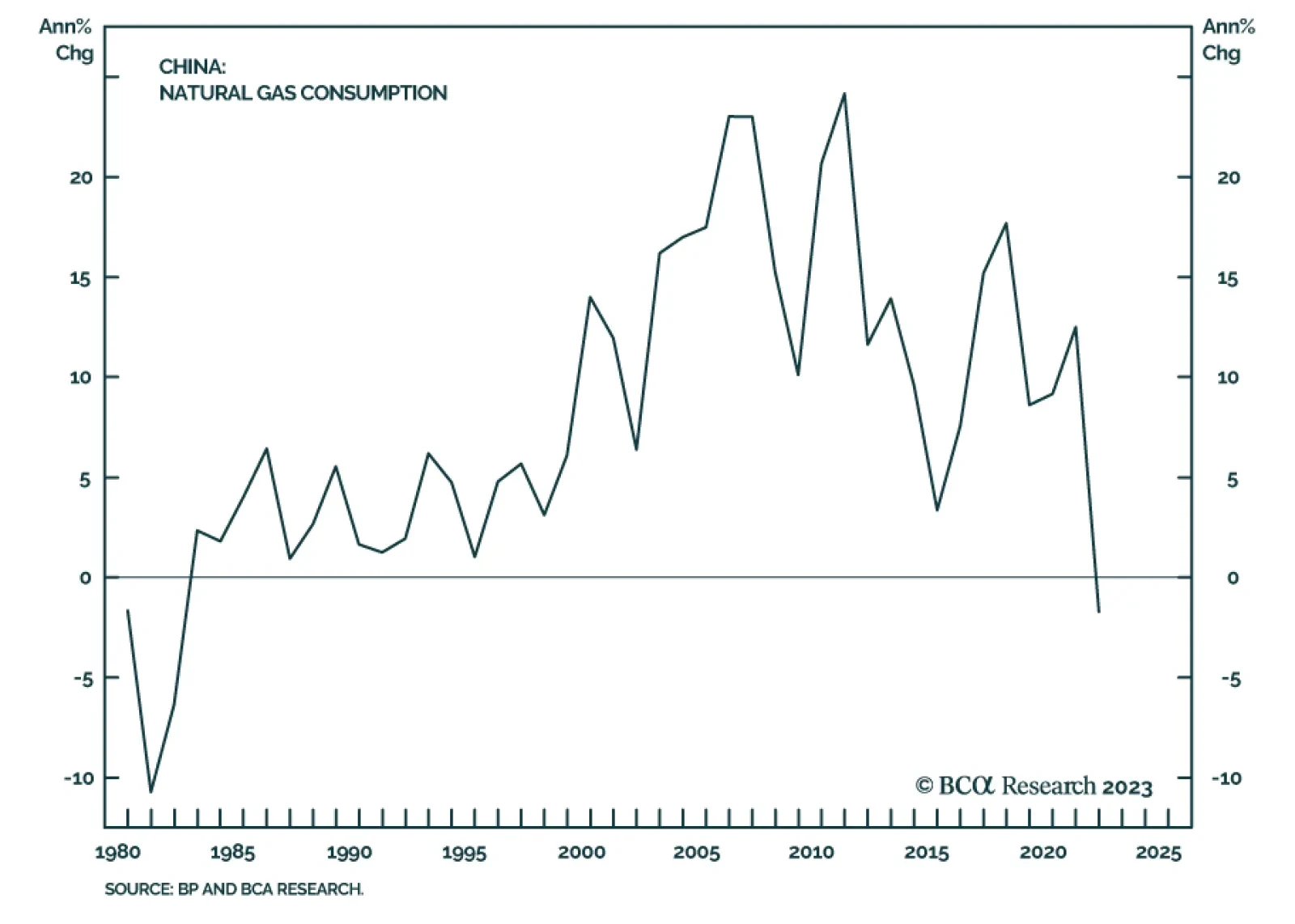

China’s appetite for liquefied natural gas (LNG) is set to rise this year, spurred on by collapsing international LNG prices and a moderate recovery in domestic demand. Global LNG prices will face upward pressure on recovering worldwide demand and a limited supply increase in the second half of the year. We expect LNG prices in China and globally to be 20-30% higher than current levels by the end of this year.

Is there a lot of cash on the sidelines ready to be deployed? Would the US recession not be bearish for the US dollar and help EM like it did in the early 2000s? Why can the US investment playbook of the past 15-25 years not be used in this cycle?

Bullish equity sentiment may persist in the second quarter on the Fed’s pause, but tight monetary policy, financial instability, elevated recession odds, extreme US polarization and policy uncertainty, and still-high geopolitical risk should encourage investors to maintain a defensive position for the coming 12 months.