Insights

Access expert research, timely insights, and exclusive webcasts to help you make confident, data-driven decisions.

Insight

New Fed Chair Kevin Warsh wants to make Fed-watching great again. The Warsh Fed will speak less and guide less. There is, however, an important nuance to the communication changes so far. While explicit guidance was removed, some implicit guidance remains, as inflation was prioritized over employmen...

Read more

Insight

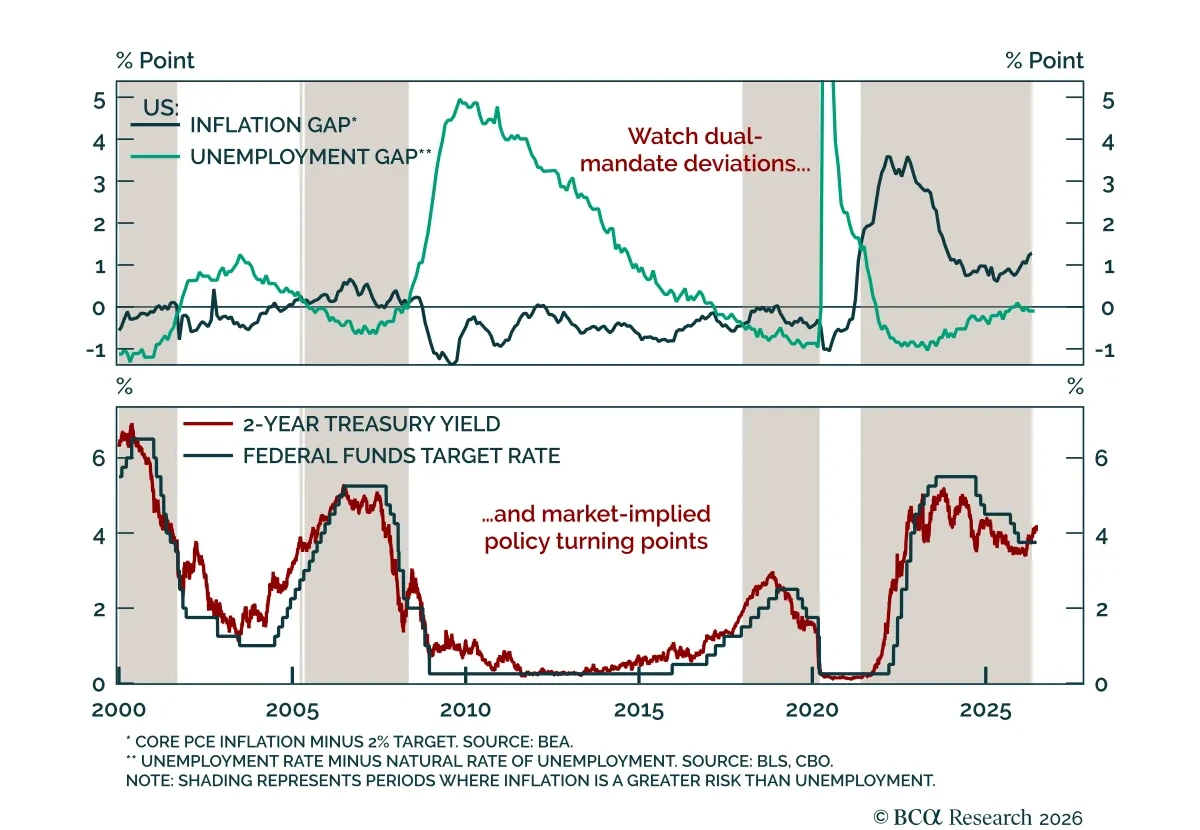

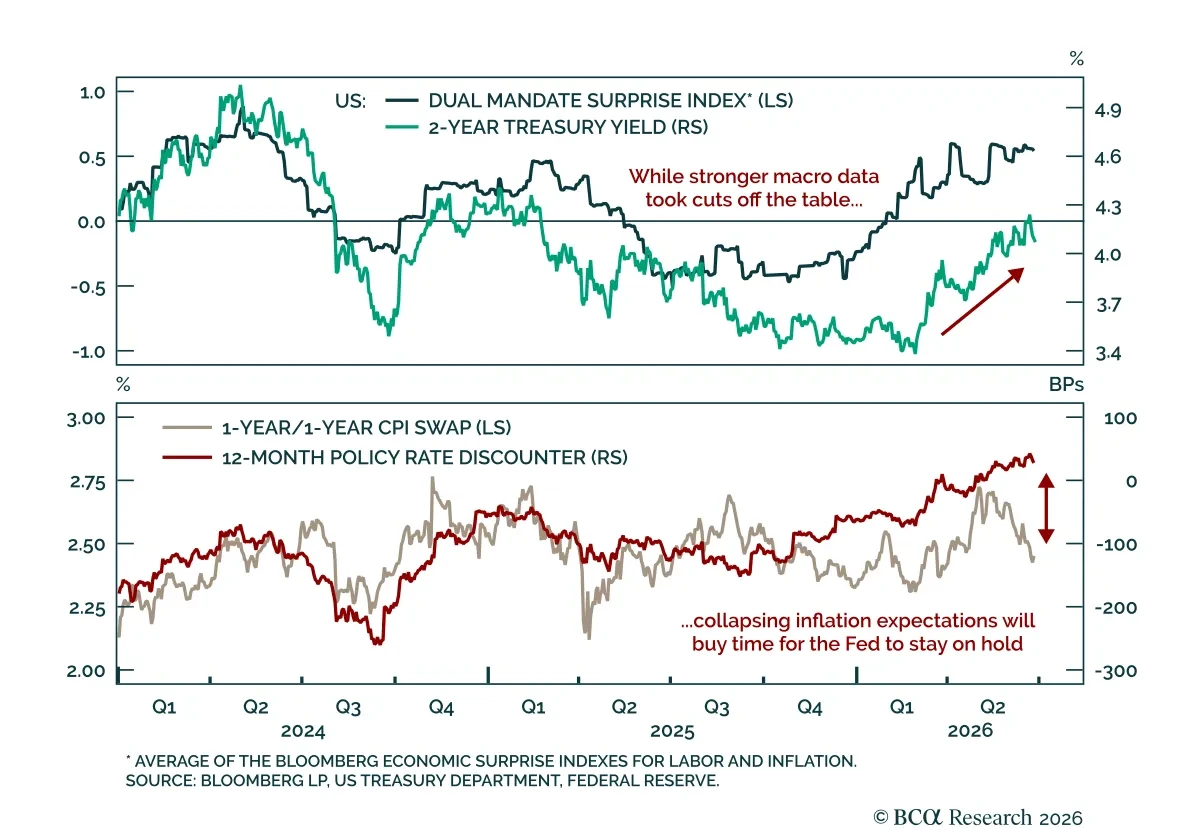

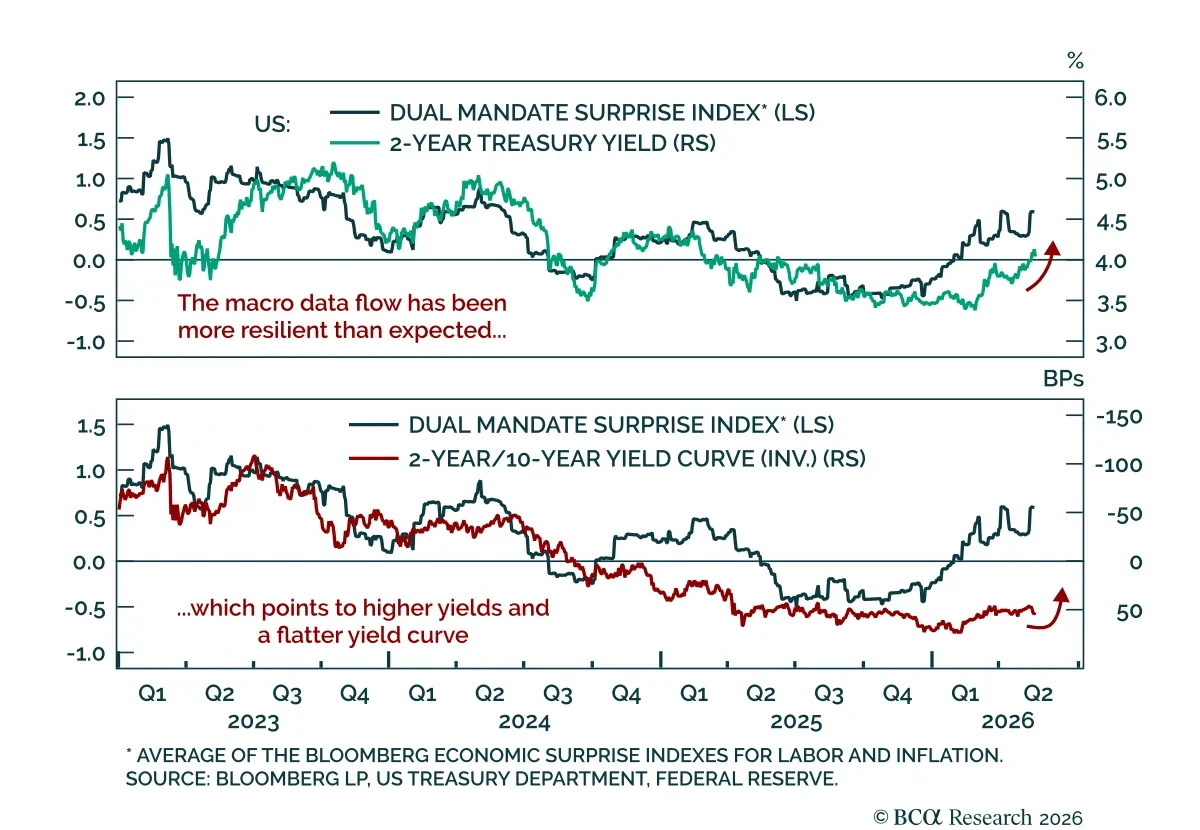

Mixed labor and inflation data should create a window for the Warsh Fed to keep rates on hold. We recently highlighted an important nuance to the communication changes so far: explicit guidance is removed, yet implicit guidance remains. The Warsh Fed will also aim to take more guidance from markets....

Read more

Insight

The April FOMC minutes clarified the hawkish shift that marked the meeting. The Fed held at its last meeting, but there were four dissents. While Governor Miran favored a 25 bps cut, regional presidents Hammack, Kashkari, and Logan supported a hold but voted against the easing bias in the statement....

Read more

Insight

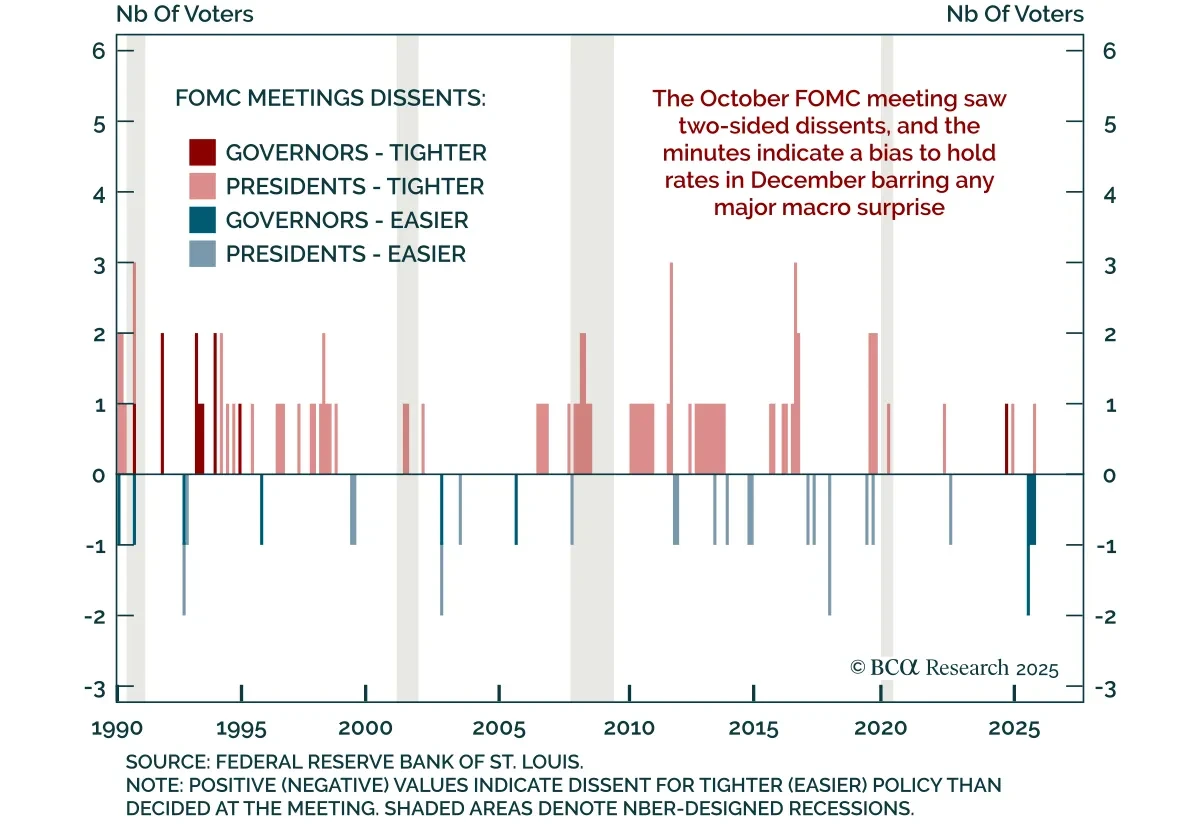

The October FOMC minutes underscored deep divisions over the Fed’s next move, reinforcing expectations for a December hold but keeping the easing bias intact. The 10–2 vote for a 25 bps cut included dissents on both sides (Governor Miran for a 50 bps move and Kansas City Fed President Schmid for no ...

Read more

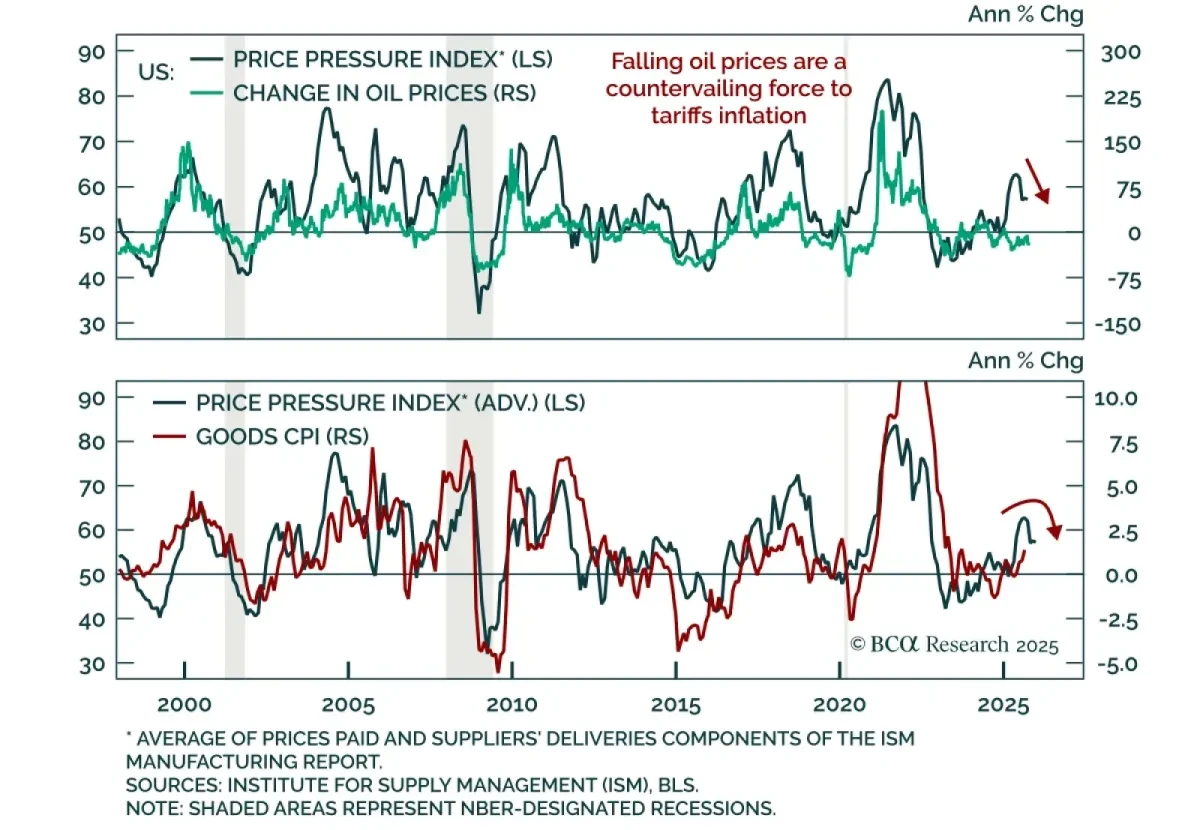

Insight

Falling oil prices are countering tariff-driven inflation which, along with a weakening labor market, is reinforcing a long duration stance. Brent crude broke below the $65/bbl support level held since June and WTI is now down 16% from a year ago. Falling oil prices are significant at this stage of ...

Read more

Insight

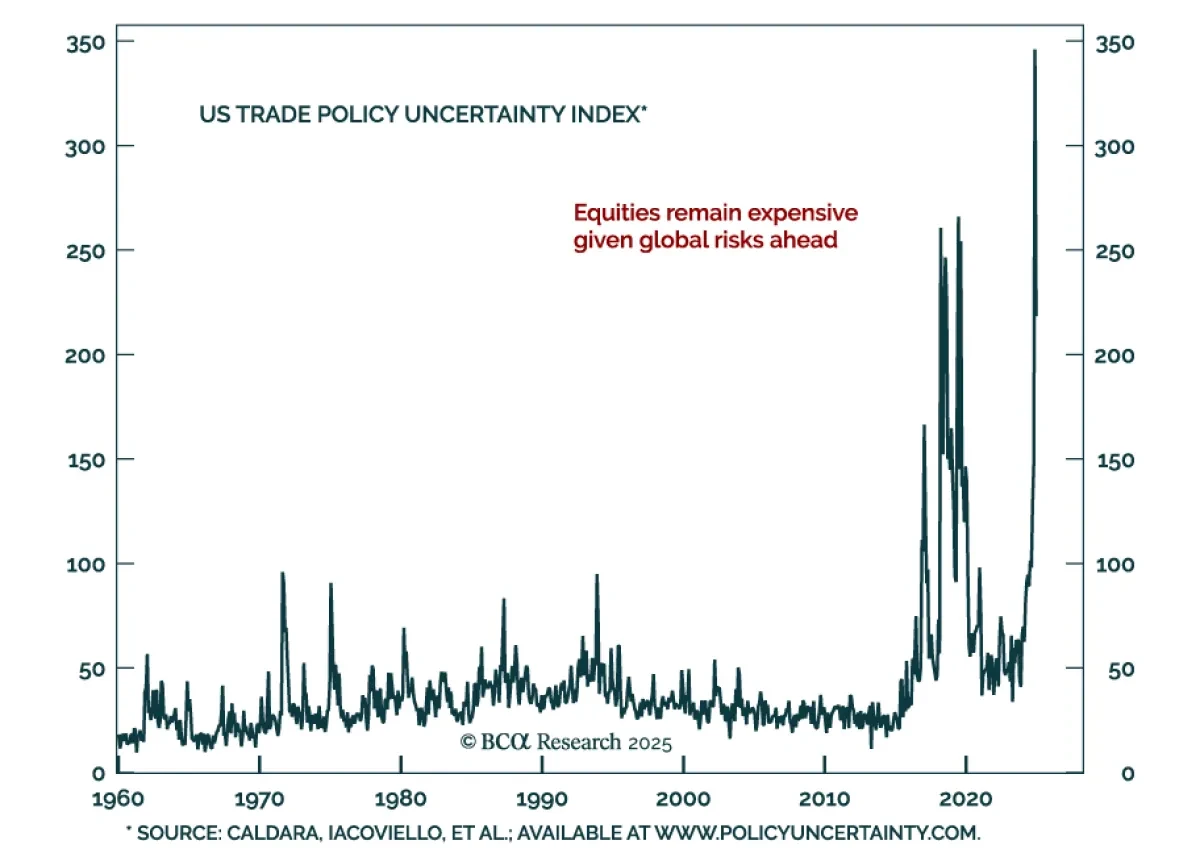

President Trump’s inaugural speech outlined his second term agenda. The theme was that the US will become “far more exceptional” than it already is. Trump pledged to reverse America’s decline, rebalance the justice system, streamline government, protect borders, pare back inflation, restore manufact...

Read more

Insight

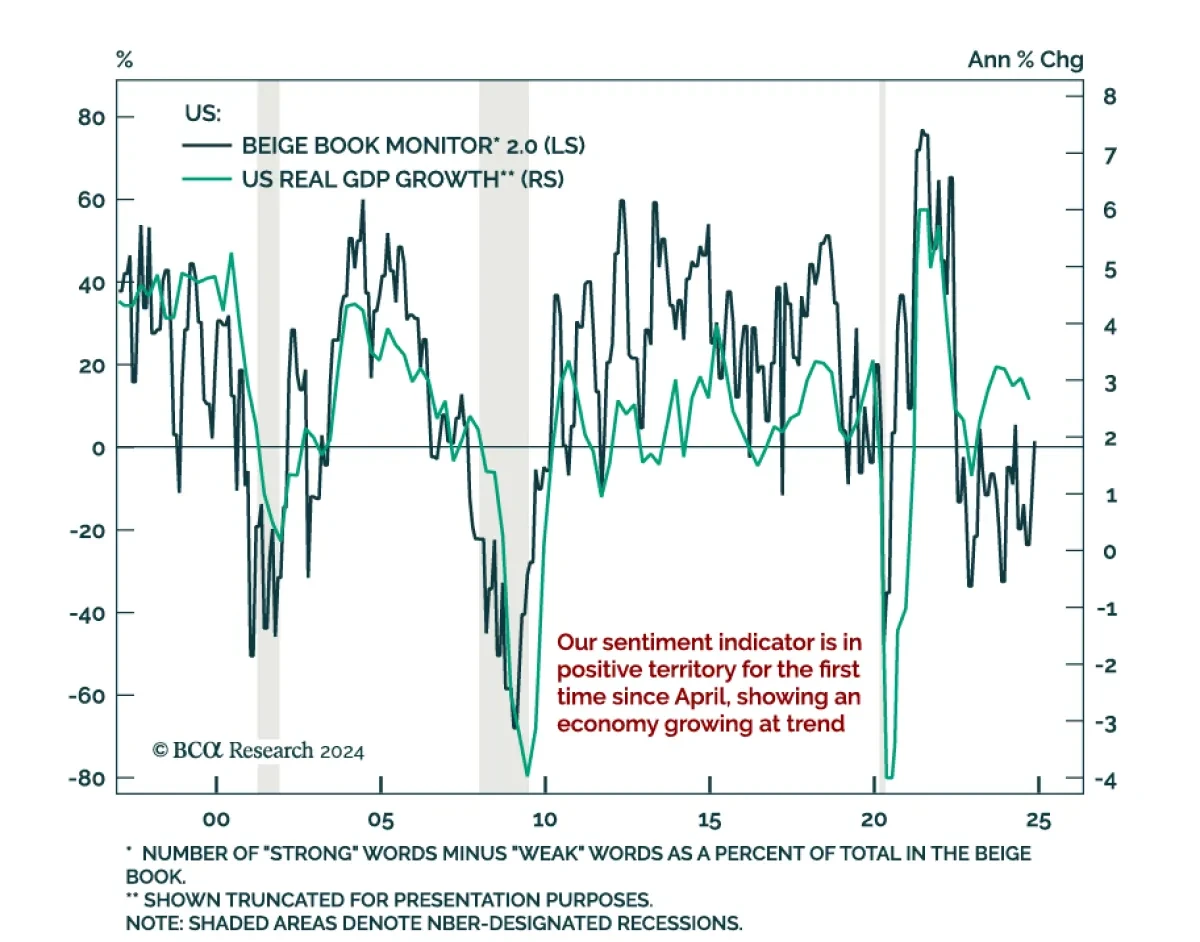

The Federal Reserve’s Beige Book shows a modestly growing economy imbued with post-election optimism, while highlighting some caution about employment. The latest Beige Book is in line with other sentiment indicators showing modest growth but increased post-election expectations. The pict...

Read more

Insight

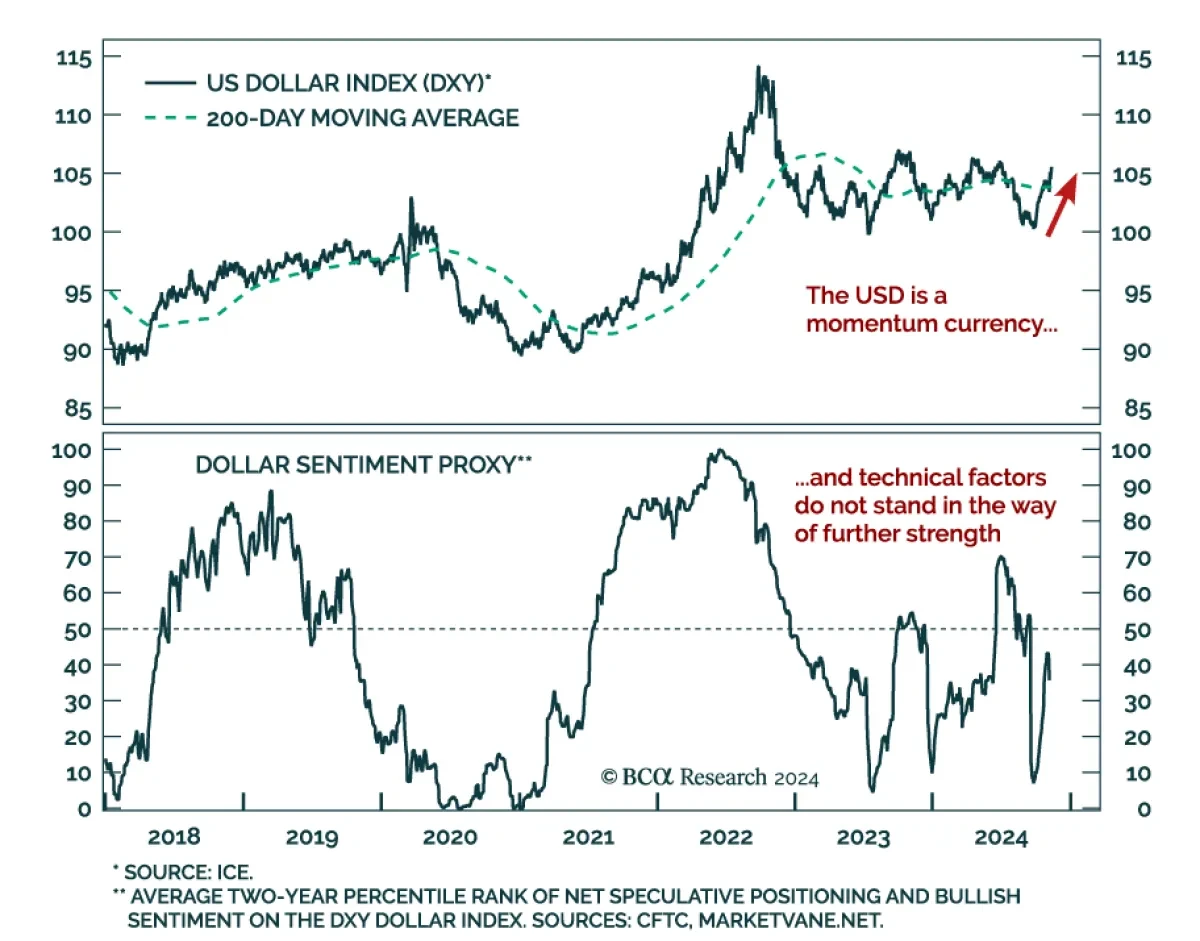

The US dollar steamrolled its peers since early October. After breaking out above its 200-day moving average, it is now fast approaching recent highs. Multiple factors drove this rally, among them are the stronger-than-expected US economic data, weaker data overseas, and Trump’s victory. ...

Read more

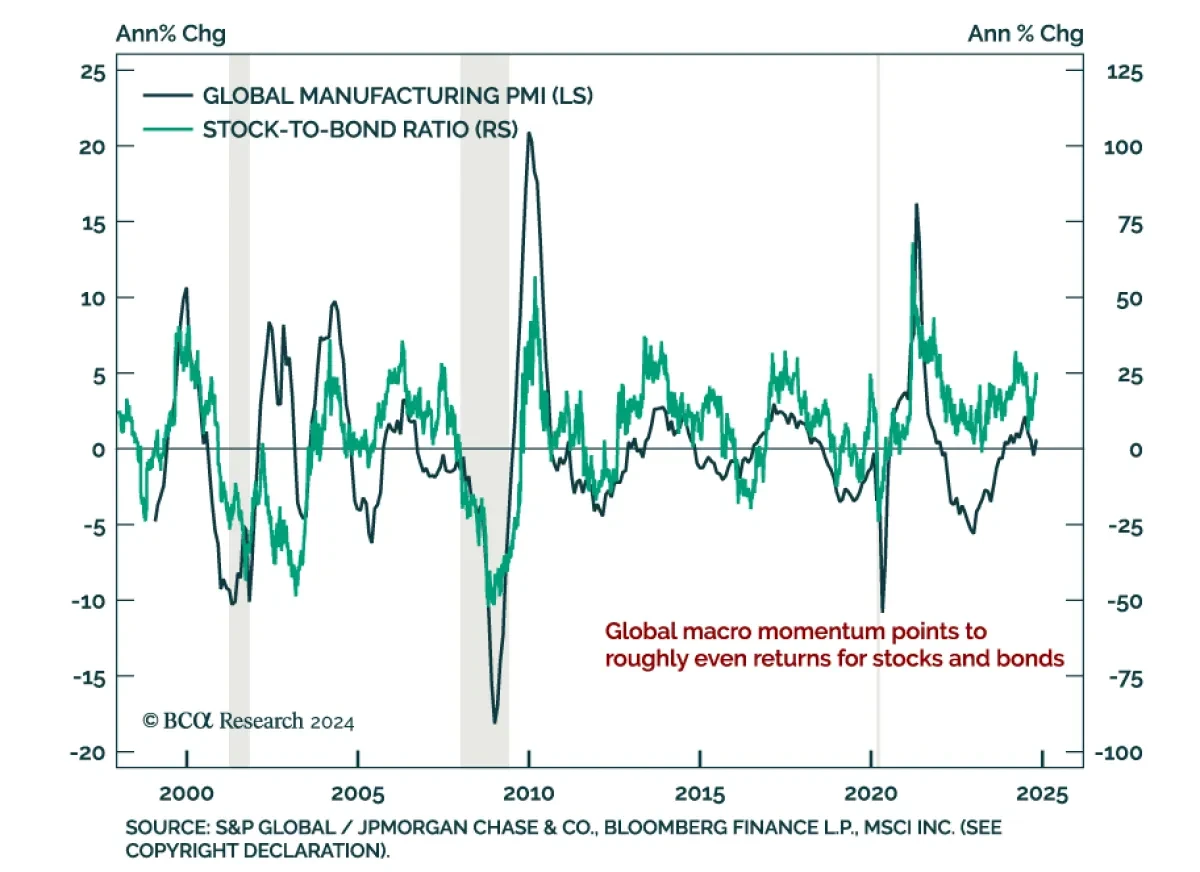

Insight

The October global manufacturing PMI printed at 49.4, up from 48.7 in September but still in contractionary territory. While output stabilized at 50.1, new orders (48.8) and new export orders (48.3) remain in contraction, as is the case for the new orders-to-inventories spread. This rebound is ...

Read more

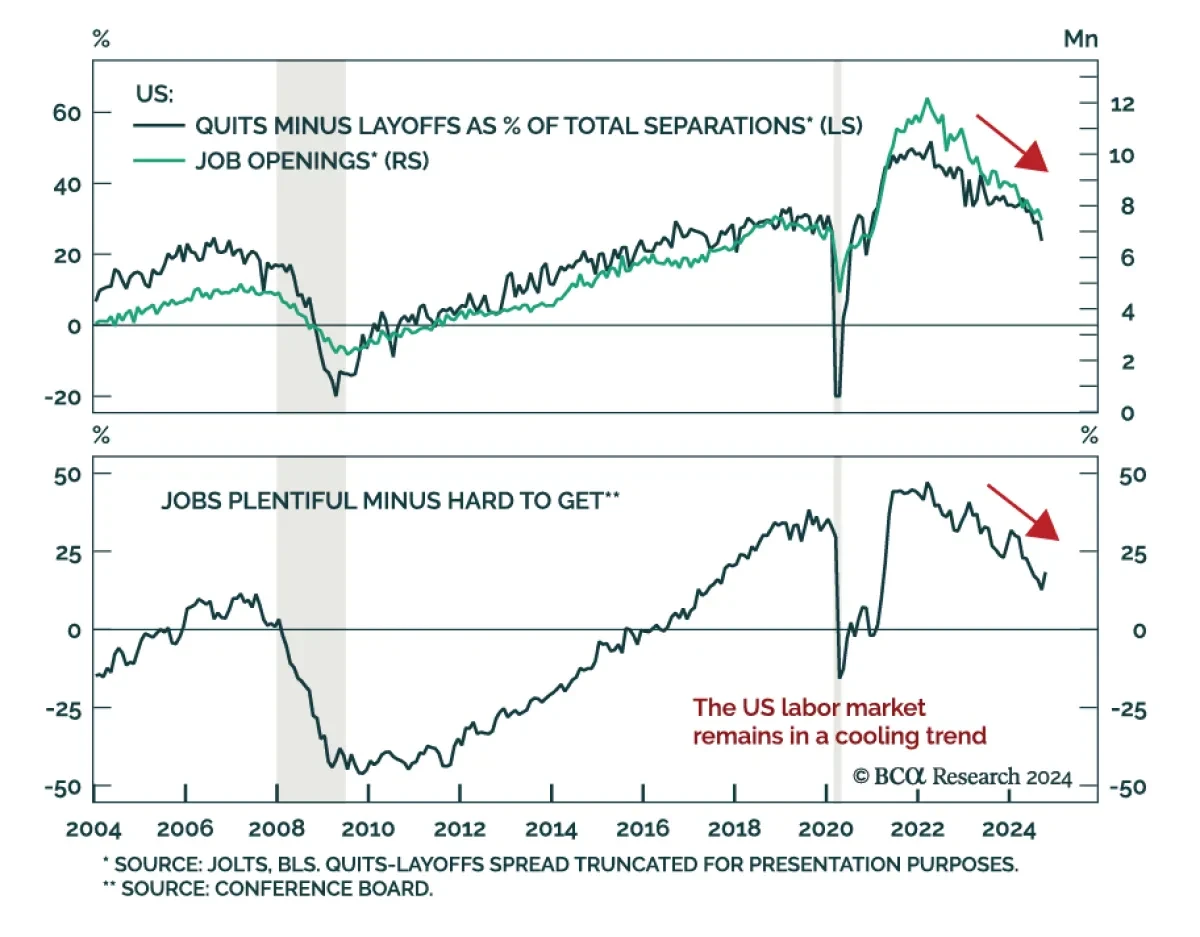

Insight

Job openings missed expectations at 7.44 million in September, a mild slowdown from August. The details of the JOLTS report were also negative, except for hirings which continue their June rebound. Meanwhile, consumer confidence for October data beat expectations. The Conference Board’s labor differ...

Read more