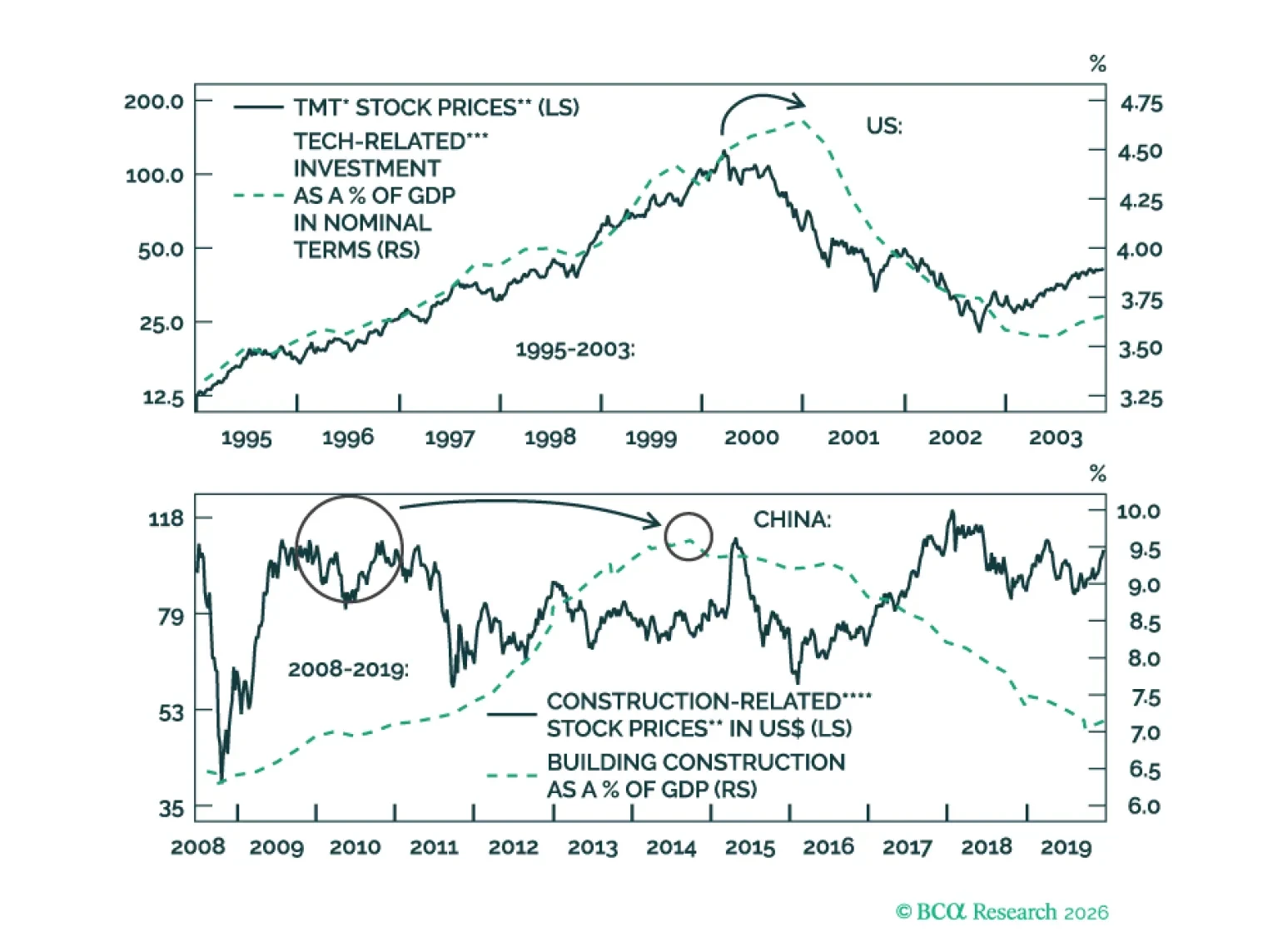

Bubbles

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

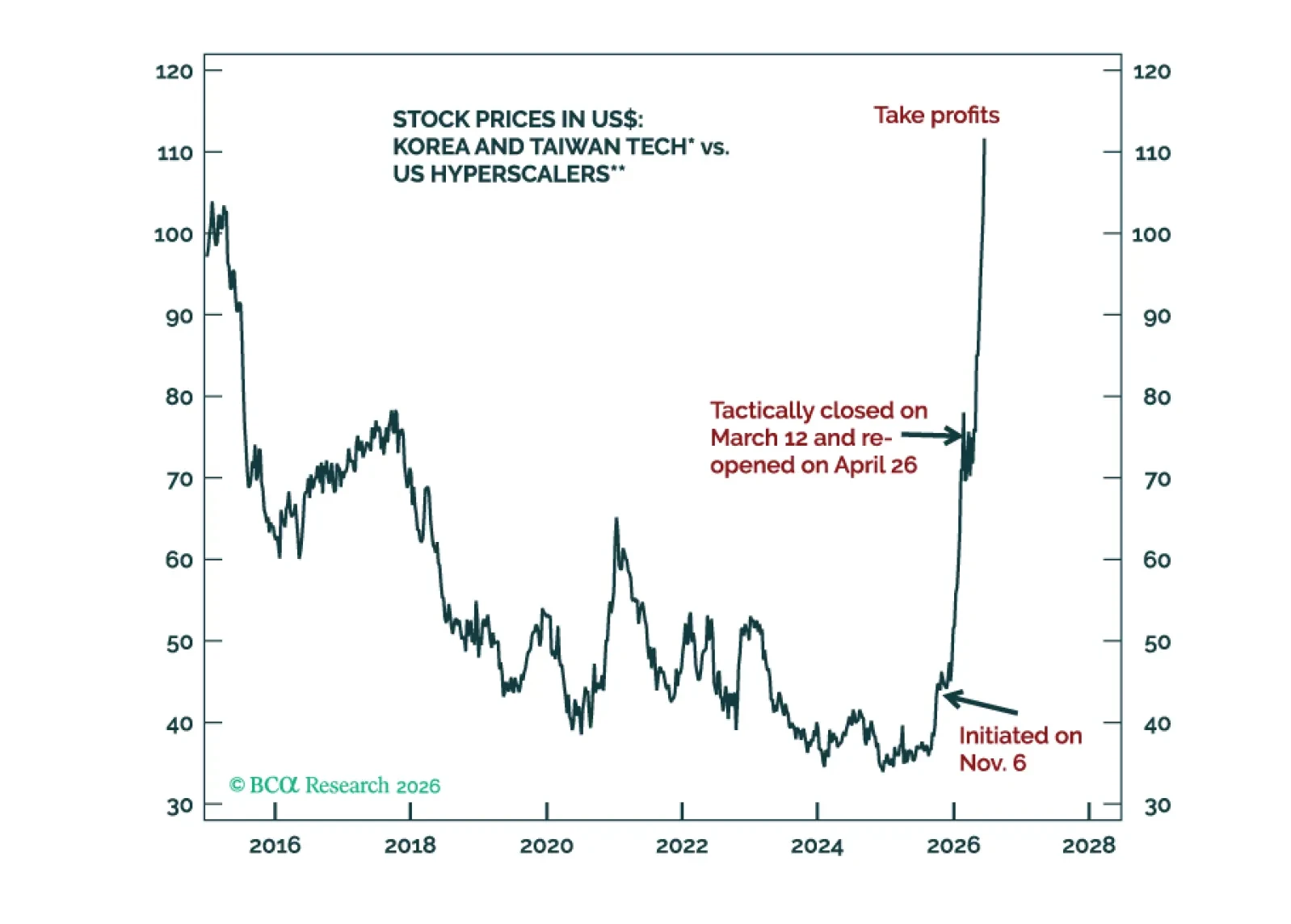

Korea’s recent equity market tantrum is a warning signal for global risk assets. We are booking profits on the long Asian semiconductor stocks / short US hyperscalers trade and downgrading Korea from overweight to neutral in an EM equity portfolio.

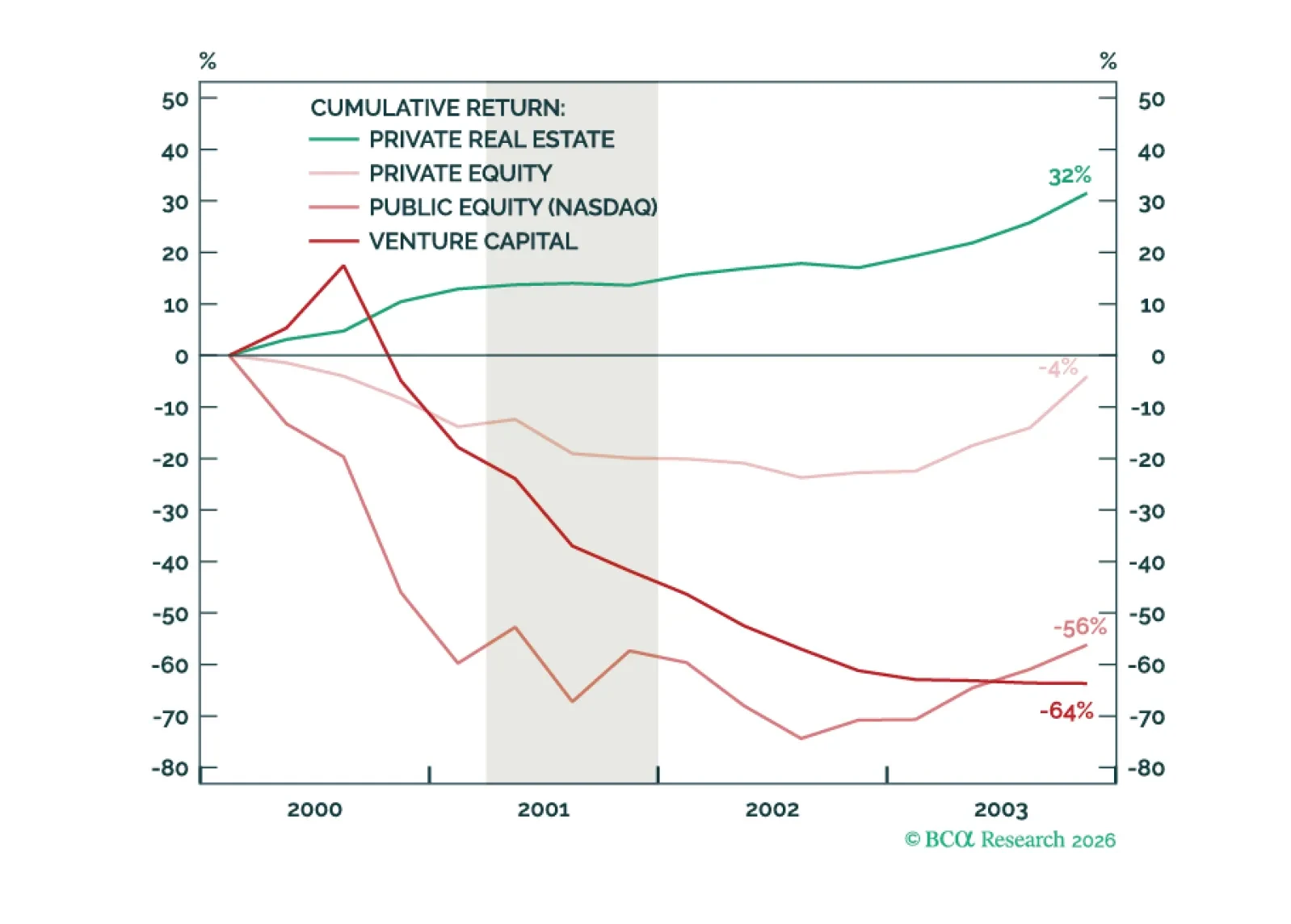

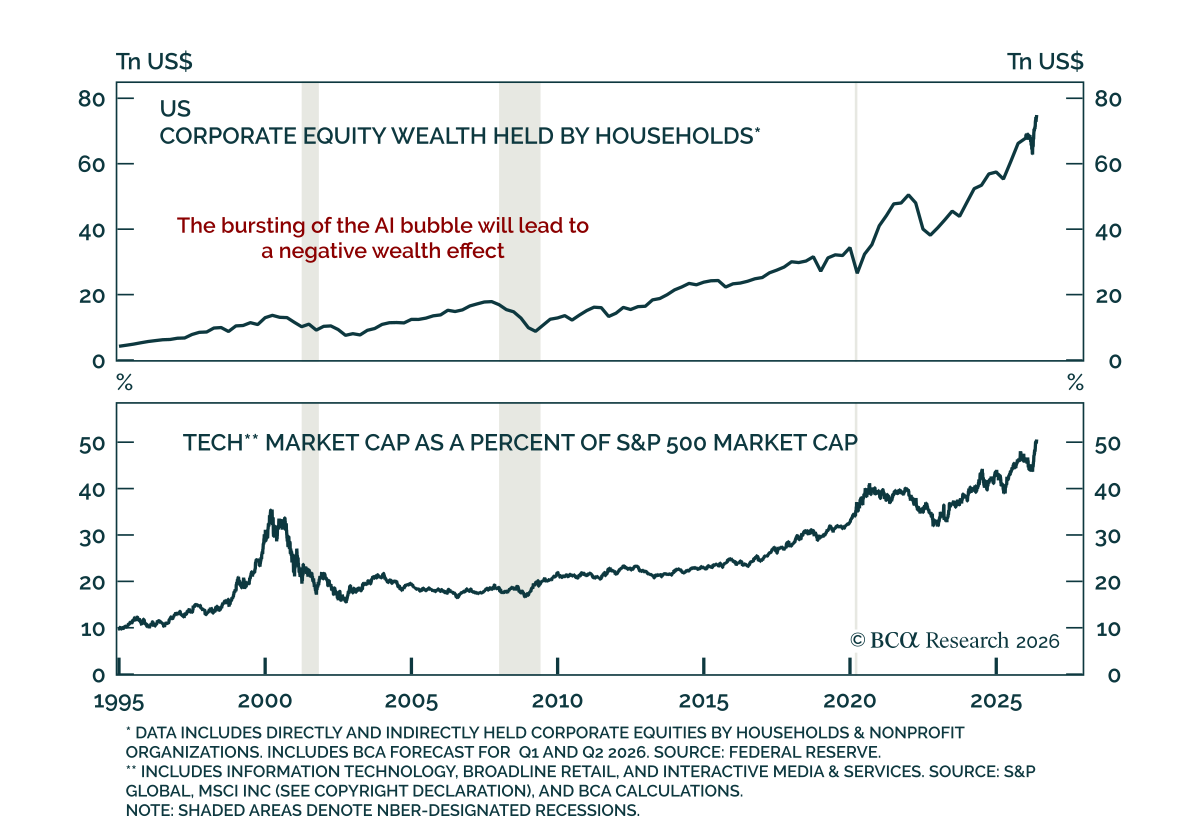

AI dominates markets, but concentration is risk. Real Estate is the diversifier. It outperformed during the Dot-Com bust and will do so again if the AI trade unwinds. Even Office, the sector arguably most exposed to AI disruption, will prove more resilient than bears expect.

AI is transformative, yet tech stocks may not produce positive returns. Market cycles have not disappeared. Greed and fear will still produce large share price fluctuations. Meanwhile, US inflation is the key near-term risk. Global non-tech capex aspirations also look overstated.

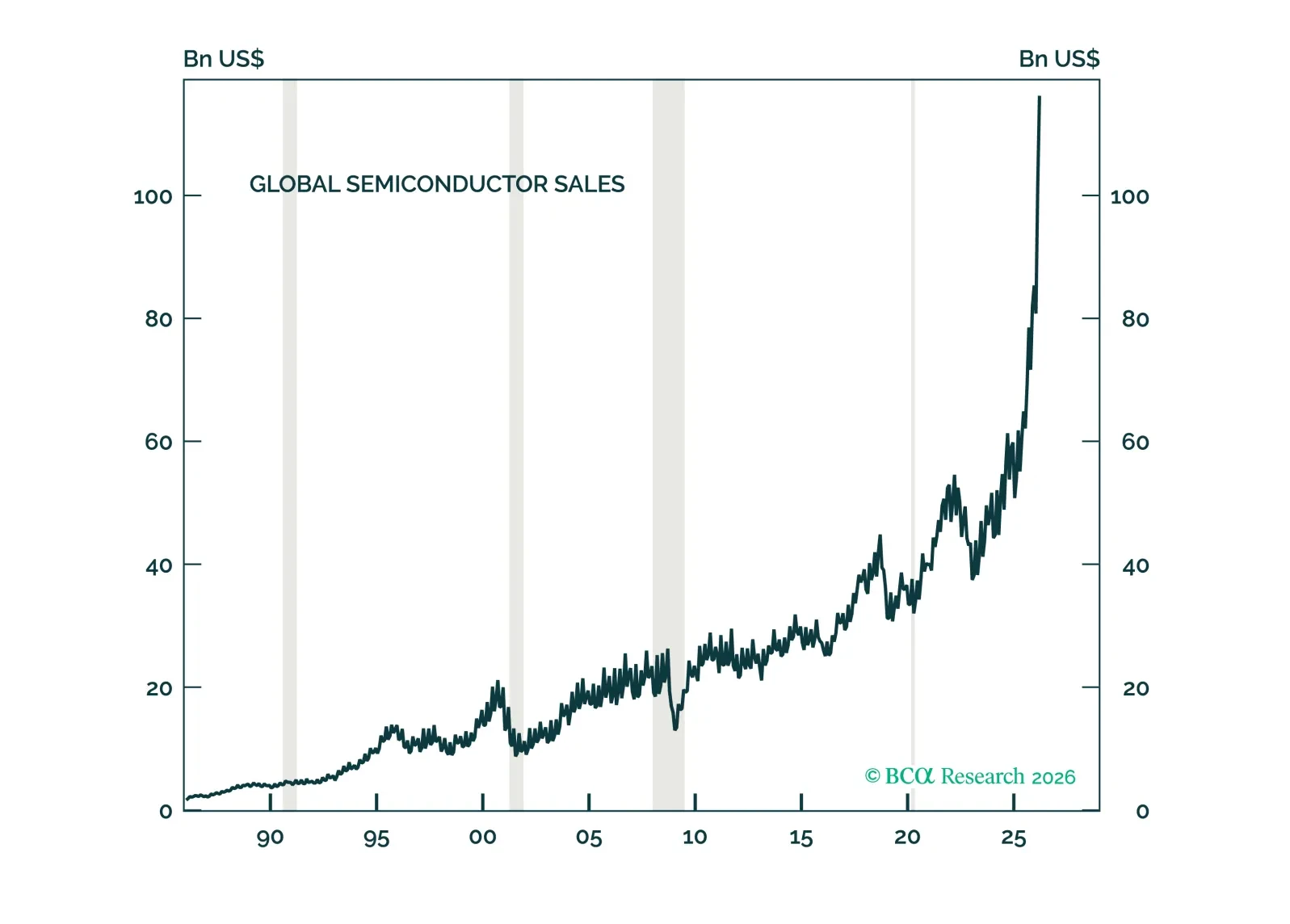

The AI bubble is a different type of bubble. It is primarily an earnings bubble rather than a valuation bubble. Like all bubbles, the AI bubble will burst. For now, however, our AI demand indicators do not suggest that this is imminent.

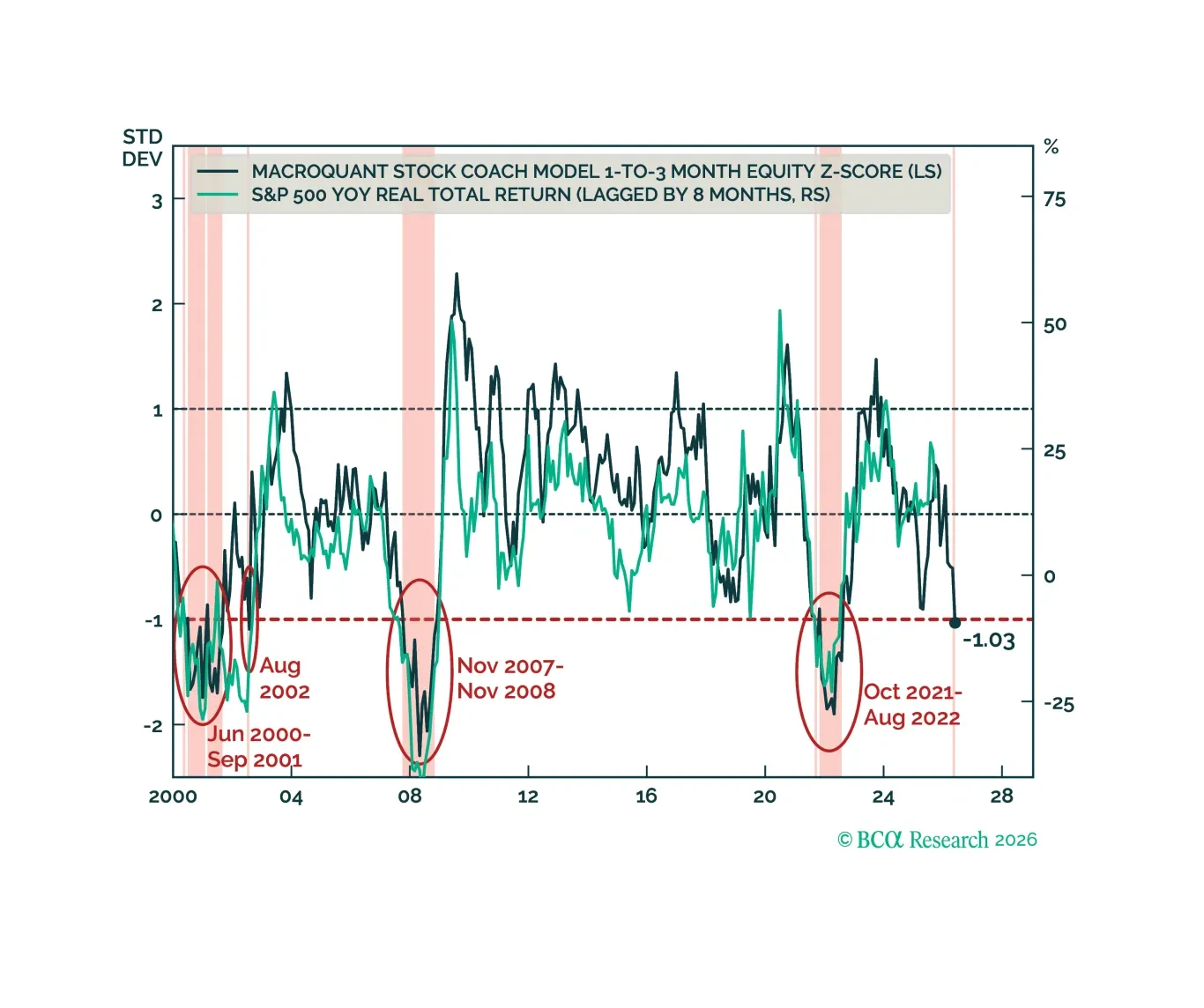

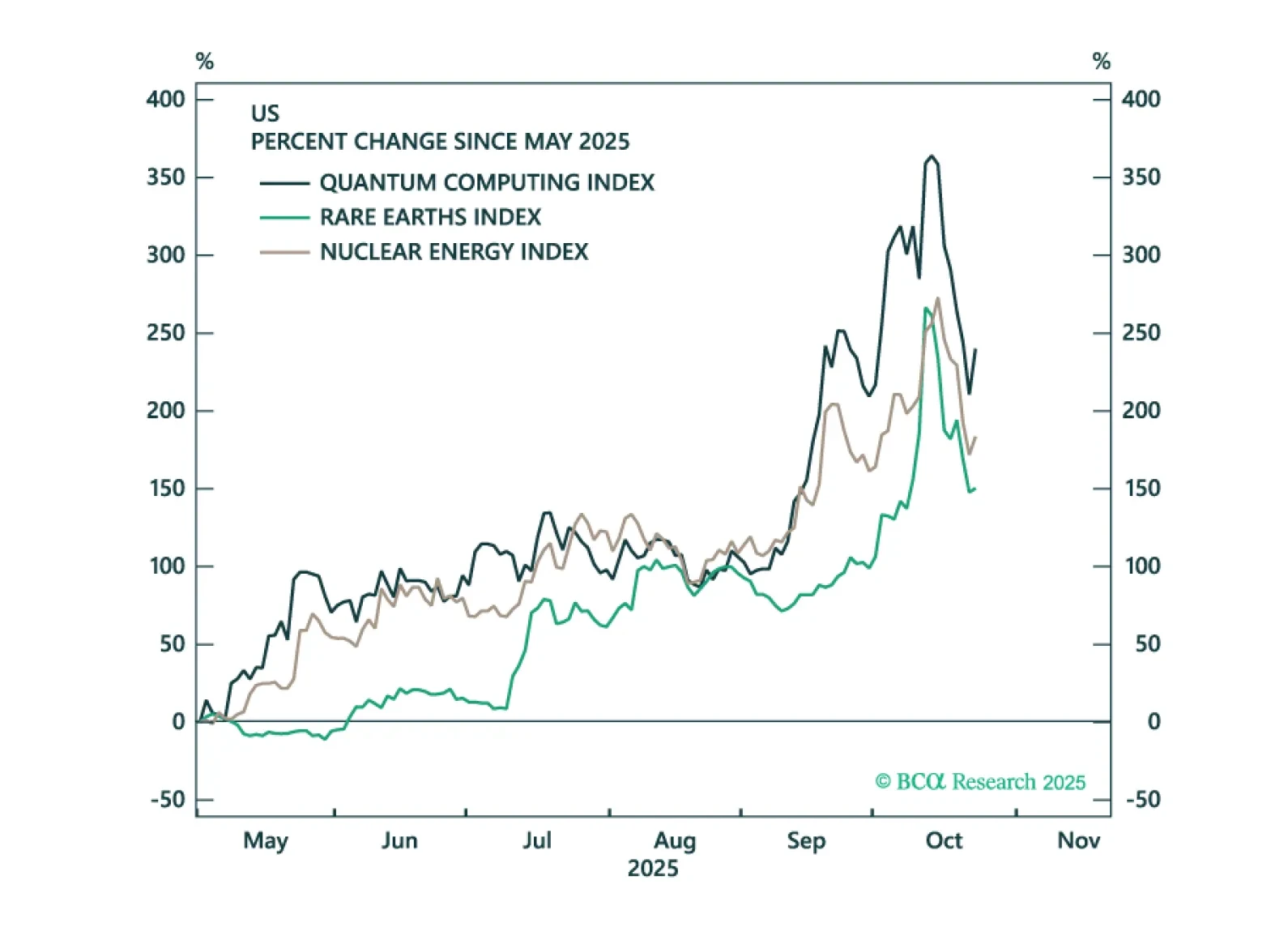

Precious metals, corporate credit, and tech stocks are all showing signs of late-cycle euphoria. We identify various trigger points that investors should monitor to turn more bearish.

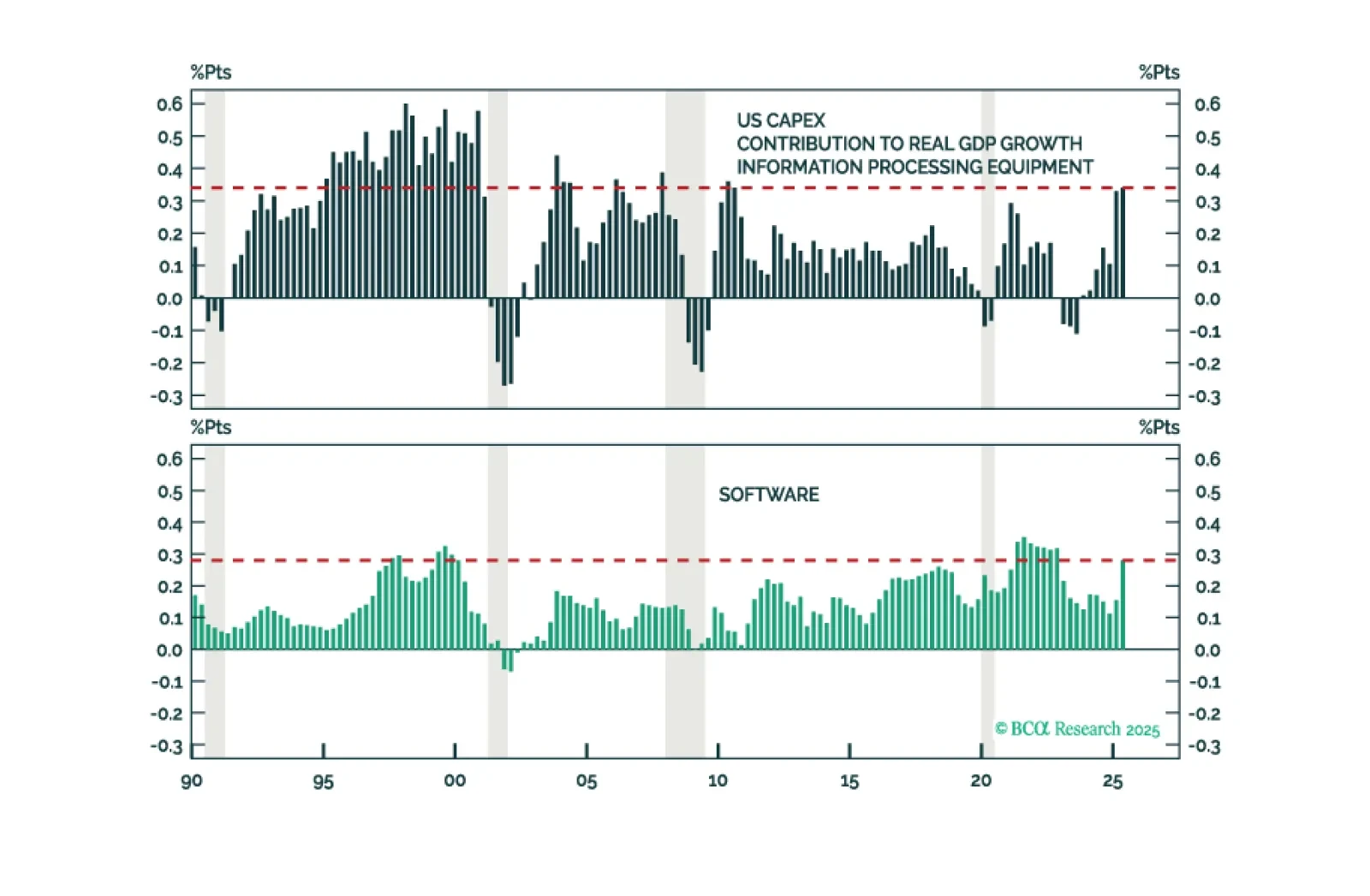

The AI capex boom is having a measurable impact on the economy but, so far, it is more muted than often cited.

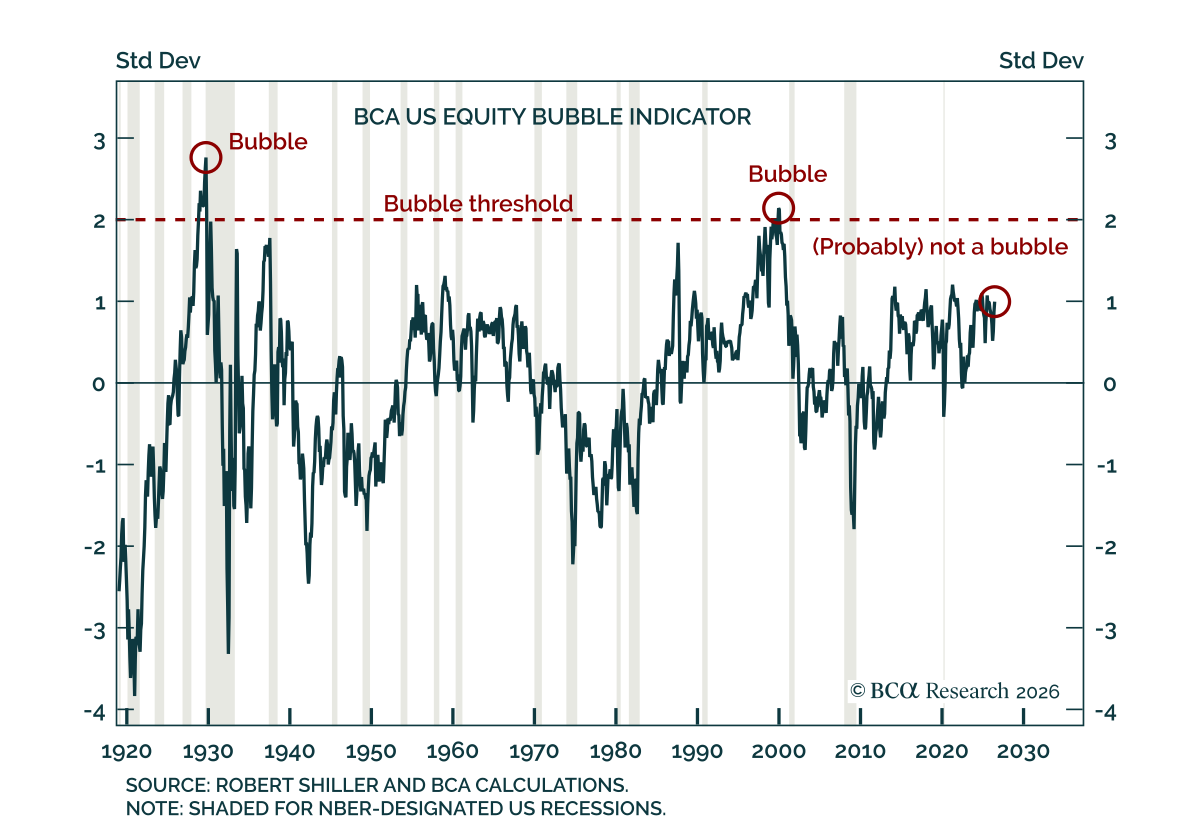

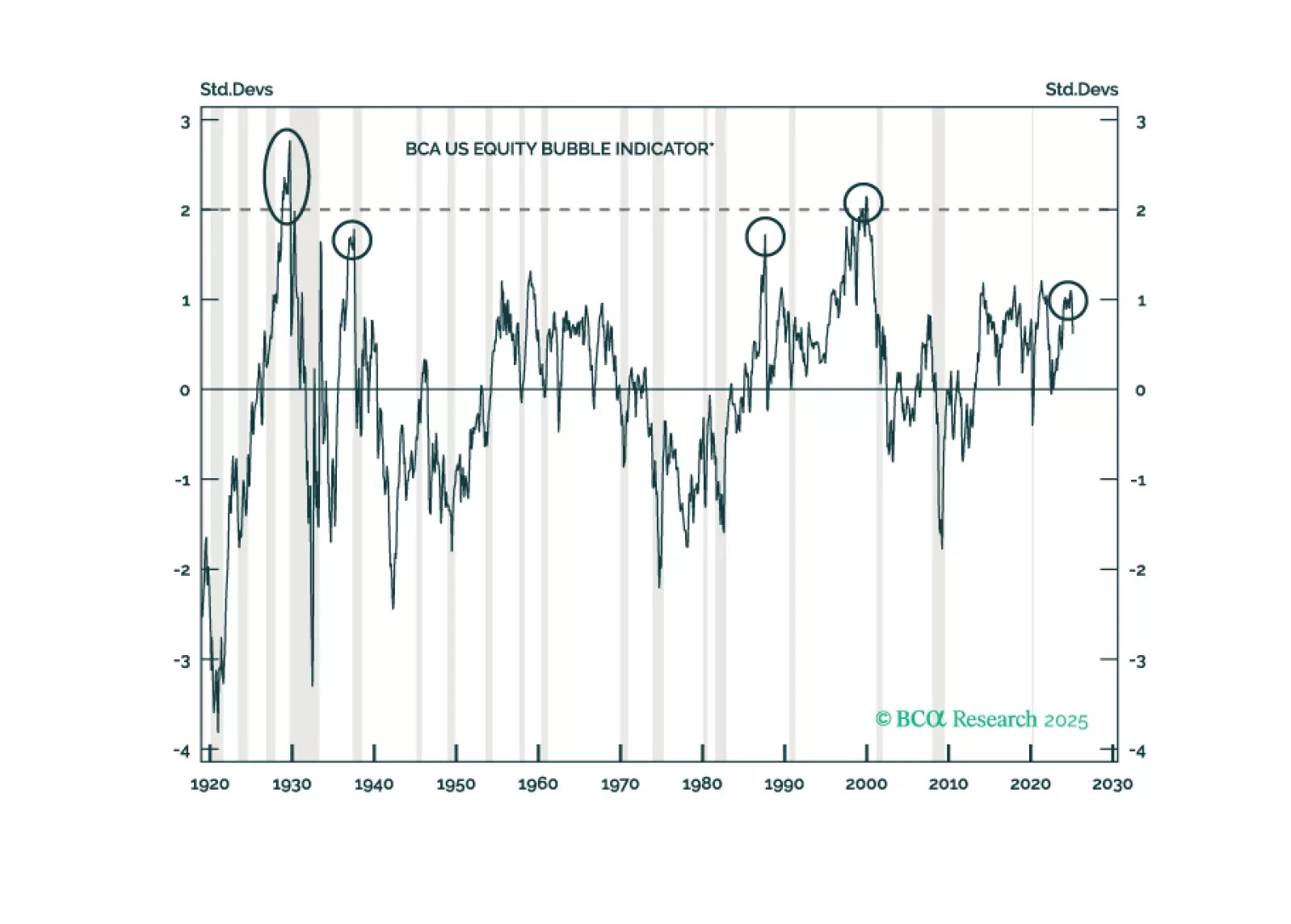

In Section II, Jonathan presents a new indicator that investors can use to track the odds of bubble formation in real time and shows how it fits into a larger framework that accurately explains US bear market severity over the past century. The US equity market is not in a bubble today, but it is meaningfully overvalued. Investors should expect a relatively severe cumulative loss from equities in a recession scenario.