BCA Indicators/Model

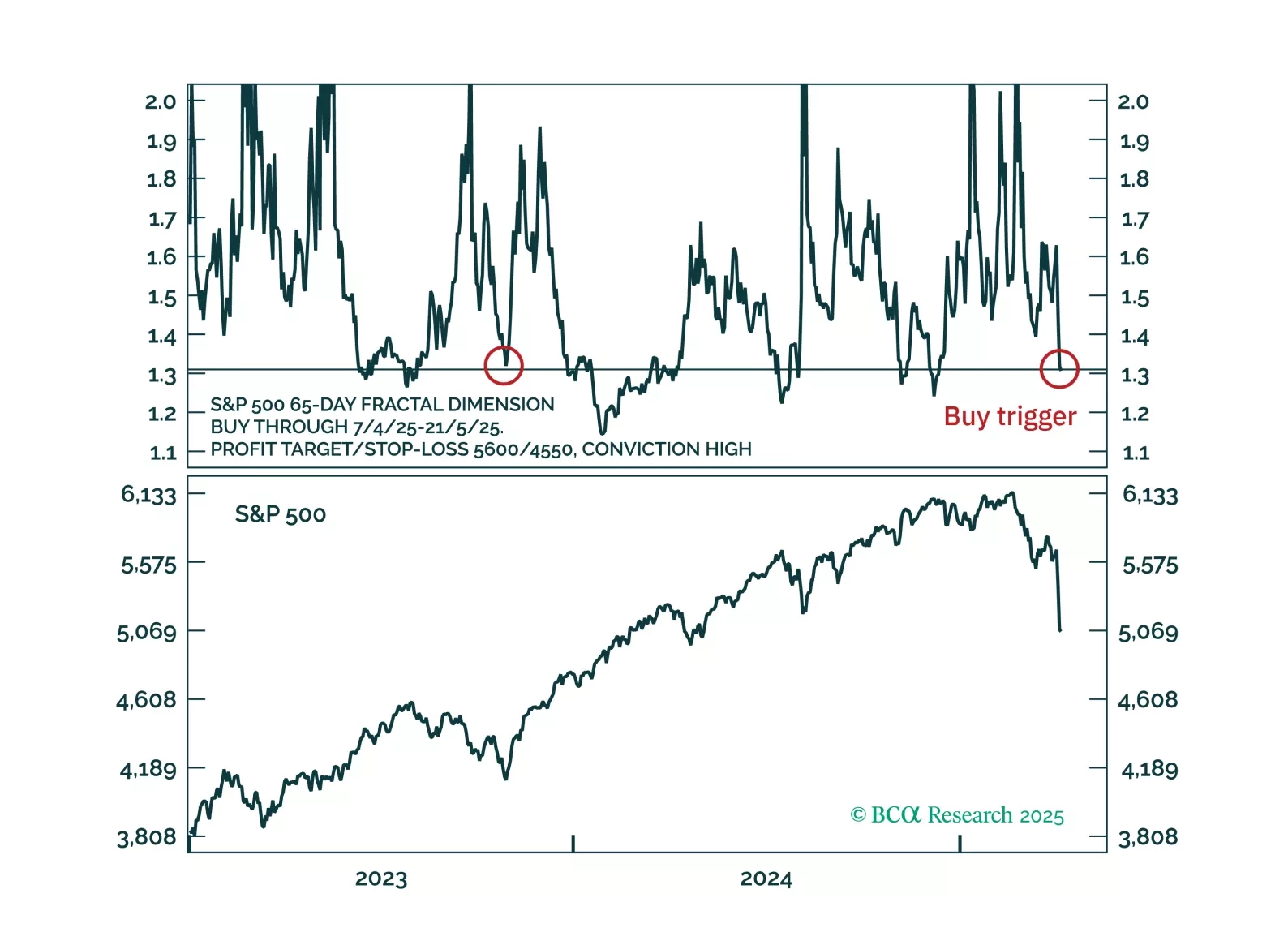

Countertrend buy triggers have been activated for the S&P 500, Nasdaq and Nasdaq versus 30-year T-bond.

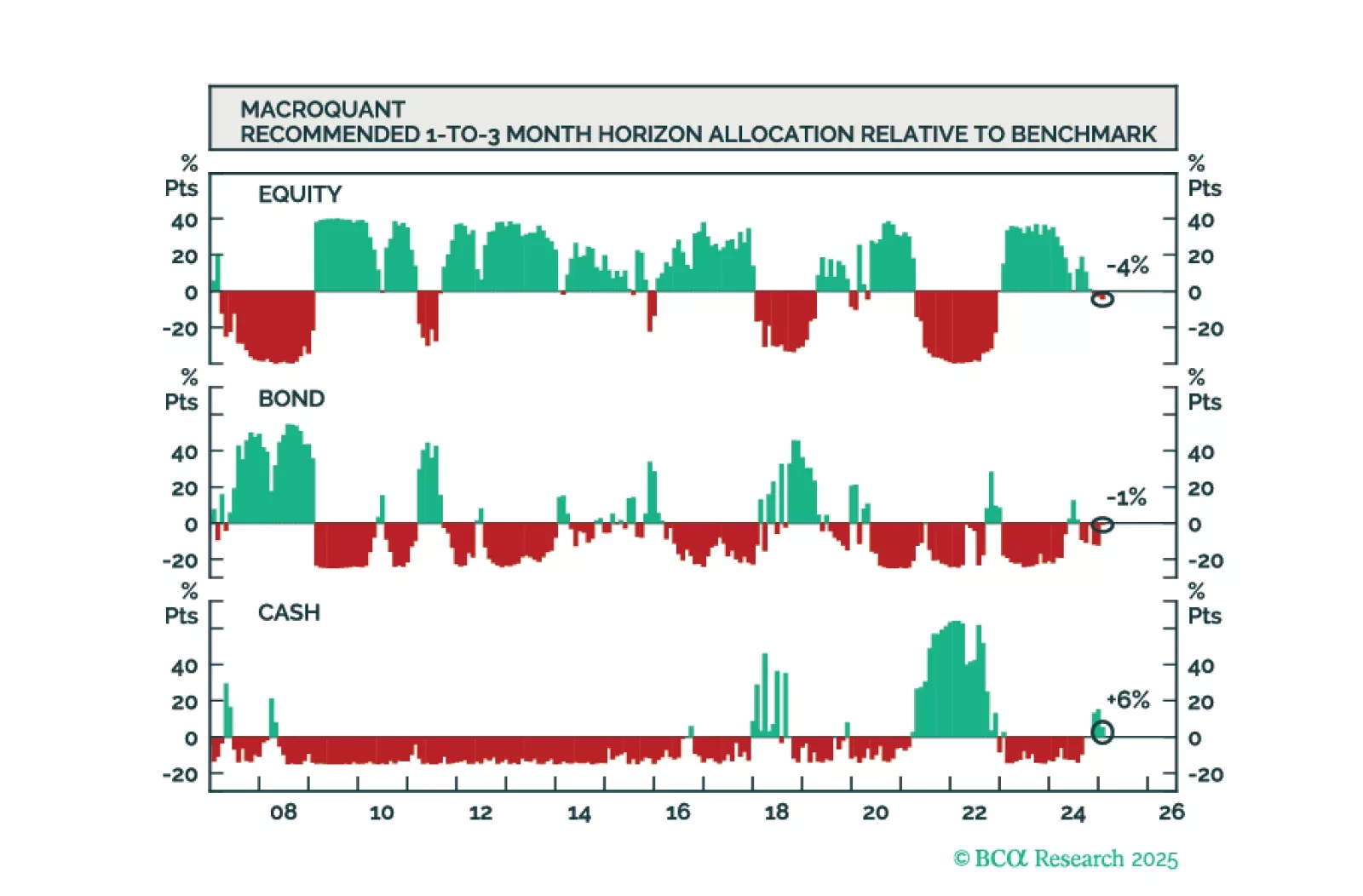

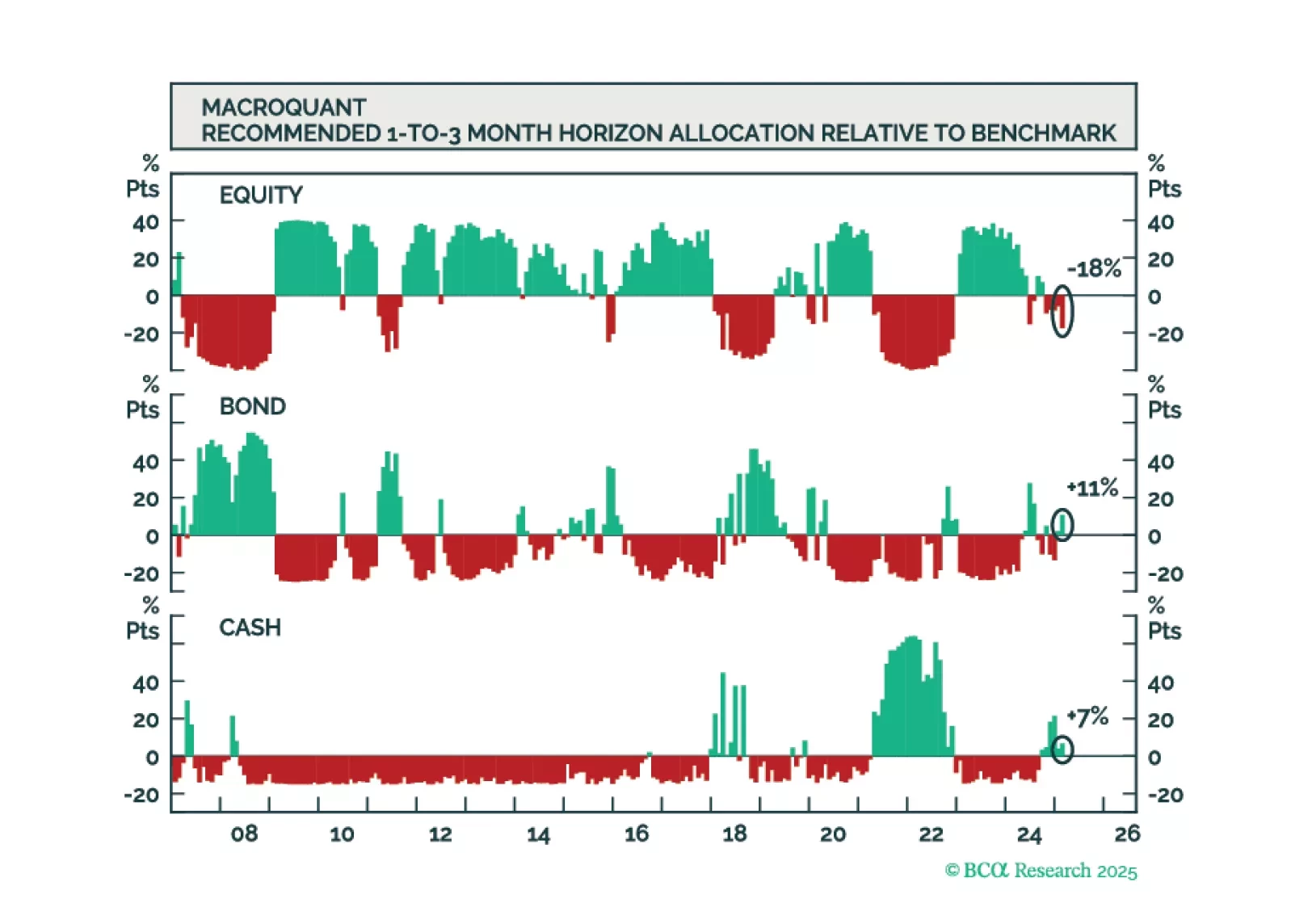

Going into April, MacroQuant recommends a modest underweight on stocks, offset by an overweight on bonds and cash. While MacroQuant is modestly bearish on stocks, we suspect that the downside risks to equities may be greater than what the model assumes.

Going into April, MacroQuant recommends a modest underweight on stocks, offset by an overweight on bonds and cash. While MacroQuant is modestly bearish on stocks, we suspect that the downside risks to equities may be greater than what the model assumes.

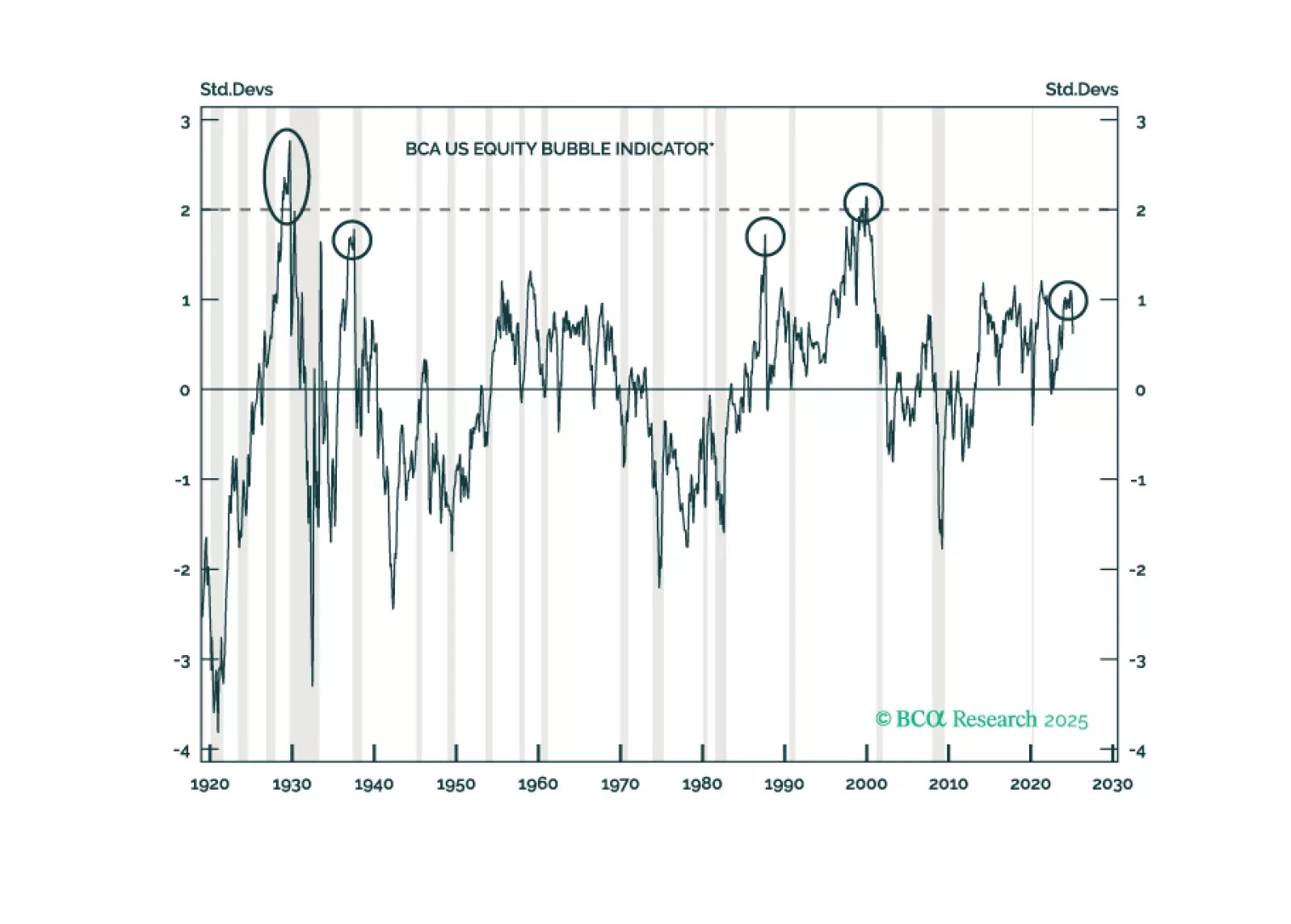

In Section II, Jonathan presents a new indicator that investors can use to track the odds of bubble formation in real time and shows how it fits into a larger framework that accurately explains US bear market severity over the past century. The US equity market is not in a bubble today, but it is meaningfully overvalued. Investors should expect a relatively severe cumulative loss from equities in a recession scenario.

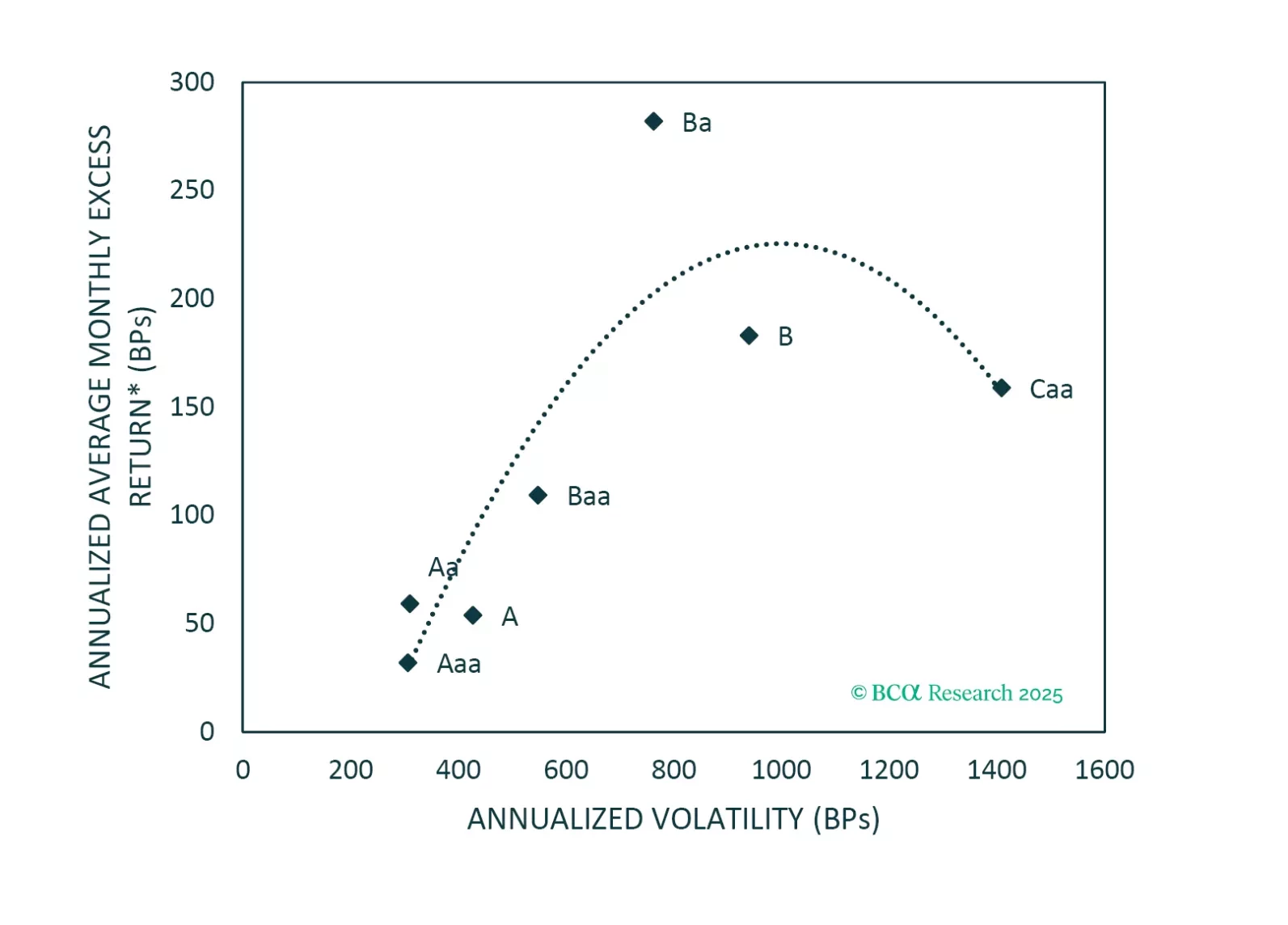

An analysis of historical data shows that Ba-rated bonds outperform other corporate credit tiers in the long-run on a risk-adjusted basis. That said, today’s fragile macro environment warrants a more cautious allocation.

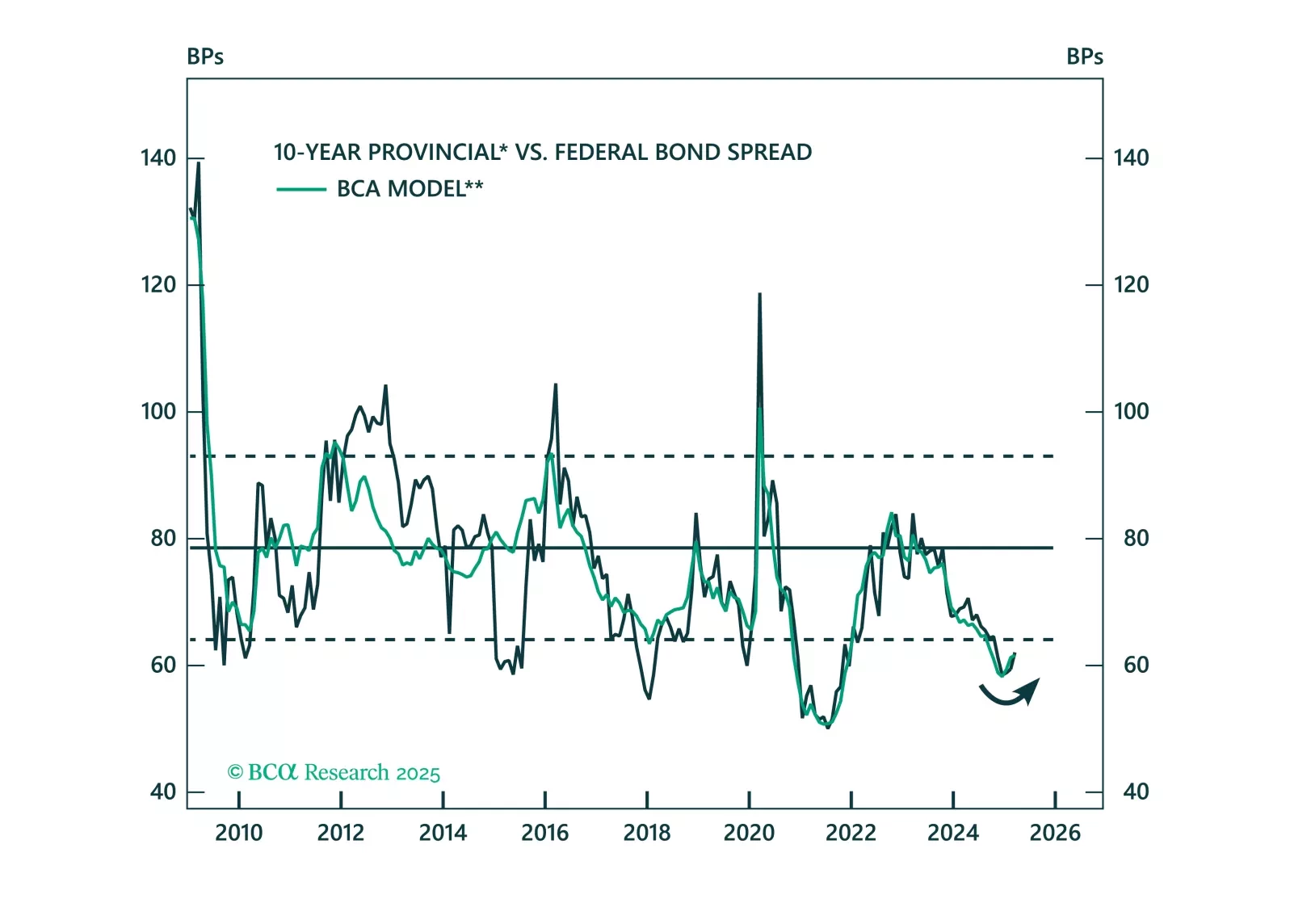

In this report, we explore the Canadian provincial bond market by developing a model to analyze its main drivers and understand the impact of a potential trade war between Canada and the US.

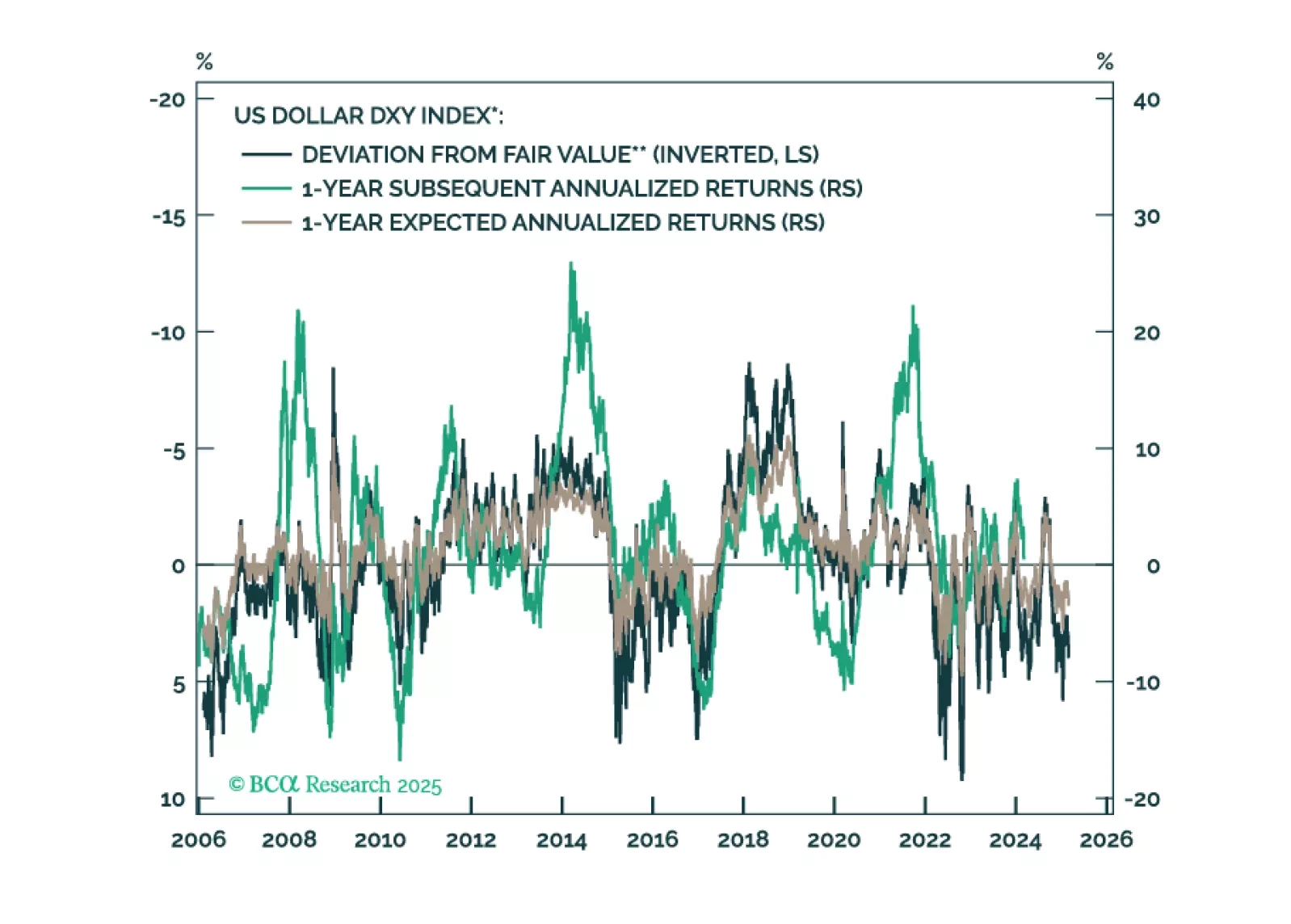

This report is our Part III series on valuation and subsequent returns, where we recalibrate our short-term models to emphasize signals over the next nine-to-twelve months. We will henceforth call these models STTM: Short Term Timing Models.

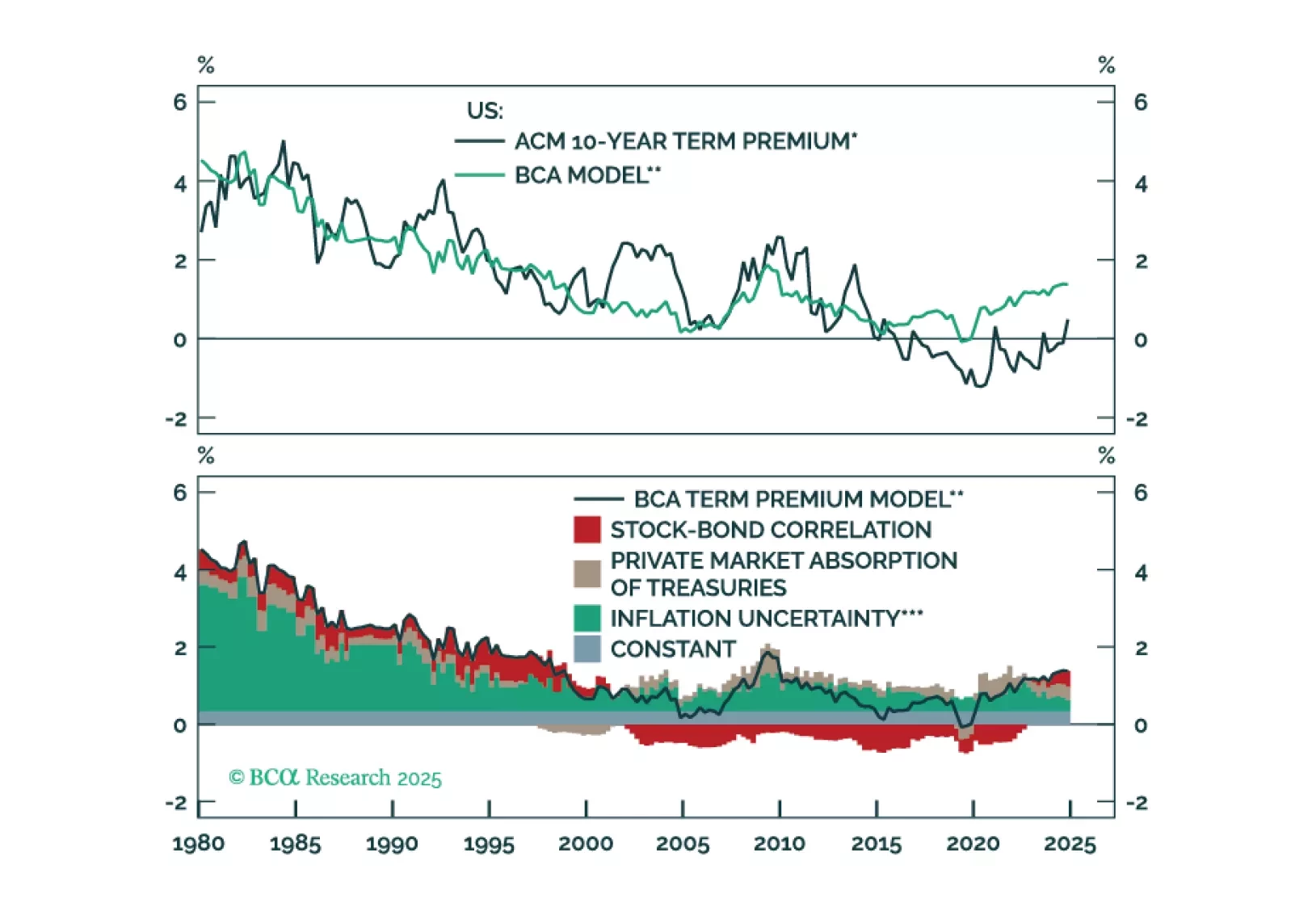

We attempt to model the term premium in this report with inflation uncertainty, the stock-bond correlation, and “Private Treasury Absorption.” Using our model, we estimate the fair value for the US term premium is 89 basis points above the current level. We also find that fiscal concerns are overrated as a term premium driver and instead, the hedging properties of bonds are more important. Over the cyclical horizon, we continue to recommend an above benchmark duration, given our expectations of an economic slowdown. However, if our term premium estimates are correct, US Treasuries still do not have a high enough risk premia to warrant a large structural allocation in a multi-asset portfolio.